Who Can Challenge Johnson & Johnson and Abbott in the Fastest-Growing Artificial Heart Market?

Artificial hearts are the fastest-growing market in interventional cardiology.

Multiple rounds of related financing have emerged both domestically and internationally in this sector.

Since 2023, Core Medical has completed two rounds of financing amounting to hundreds of millions of yuan this year. Overseas, Johnson & Johnson made a massive $16.6 billion acquisition last year of Abiomed, a company specializing in interventional artificial hearts. Johnson & Johnson’s entry does not signal the endgame for this sector; recently, OrbiMed has newly invested in another interventional artificial heart company overseas: Magenta Medical.

The technology in the field of artificial hearts is undergoing continuous iteration, with companies being eliminated from the market over decades of development. Medtronic once discontinued sales of its left ventricular assist device, HeartWare; Abbott also failed in its development of the percutaneous heart pump, HeartMate PHP; even Abiomed, acquired by Johnson & Johnson, nearly went bankrupt due to its development of a total artificial heart.

The Dynamic Landscape of the Artificial Heart Sector Underscores Its Limitless Potential. As New Players Enter the Global Arena, How Will the Field Be Reshaped? VCBeat Provides an Overview.

The story in the field of artificial hearts continues, with multiple blockbuster products making their debut recently.

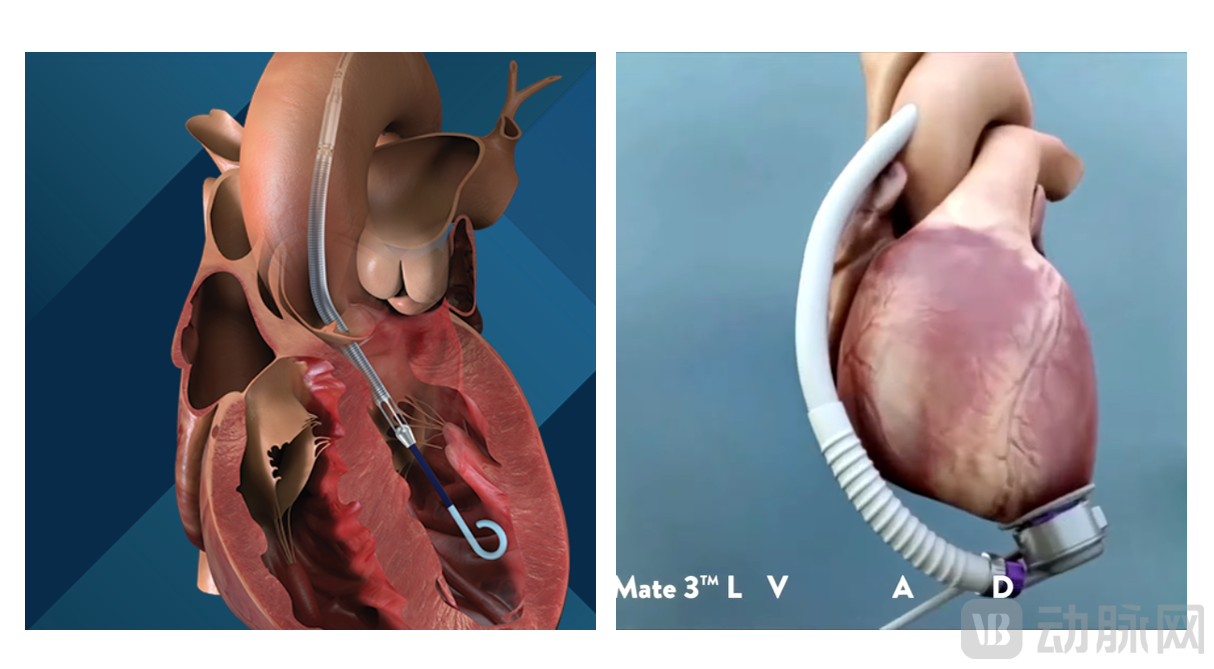

Artificial hearts can be classified into surgically implanted and catheter-based types according to the implantation method. After several years of development, Johnson & Johnson and Abbott have emerged as the dominant players in the artificial heart sector. Abbott leads the market for left ventricular assist devices (LVADs), while Johnson & Johnson dominates the percutaneous ventricular assist device (pVAD) segment through its acquisition of Abiomed’s Impella series.

Left: Johnson & Johnson's Abiomed Impella percutaneous heart pump; Right: Abbott's HeartMate 3 product

Abbott’s HeartMate 3 is indicated for end-stage heart failure, enhancing left ventricular pumping capacity through a long-term implanted cardiac pump connected to an external battery. The Impella series is designed for high-risk percutaneous coronary intervention (PCI) and cardiogenic shock, directly pumping blood from the left ventricle using a folded impeller and a miniature motor.

What directions are these two major products heading toward?

For percutaneous artificial hearts, physicians consistently have three major requirements for these devices: first, longer duration of clinical support (indicating superior hemolysis performance), with the goal of exceeding 30 days and even reaching one year or more; second, smaller device size, aiming to reduce it to that of an intra-aortic balloon pump (IABP) (7.5–8 Fr) or even smaller; and third, improved hemodynamic performance, capable of providing a blood flow rate exceeding 5 liters per minute.

Balancing these three factors is often challenging: reducing device size makes it difficult to achieve higher flow support, while extending operational duration increases the risk of hemolytic events. The ability to effectively address all three challenges simultaneously has become a key trend in the development of percutaneous cardiac pumps.

These three major requirements also create barriers for other market entrants. In terms of product design and R&D, this translates to how to design the motor, impeller, and optimize the overall performance of the product.

The design of the motor affects the overall size of the interventional heart pump. The structure of the interventional artificial heart pump is miniaturized, with the overall diameter of the product being only a few millimeters. The miniaturized motor at the bottom has a diameter of only 3 millimeters.

However, the greatest challenge lies not in fabricating miniature motors, but in designing motors that meet medical implant-grade standards.

“An industry insider stated, ‘The technology behind micro-motors is not overly complex; the motors used in everyday devices such as electric toothbrushes and drones are only 6 millimeters in size. However, these motors cannot be directly applied to cardiac implants. The shedding of wear particles from the motor poses significant risks. Furthermore, heat generated during motor operation can lead to thrombosis. Implant-grade products require sealed bearings to minimize thrombus formation. It is important to emphasize that the motor technology for percutaneous cardiac pumps is also a heavily patented area protected by Impella, and other market participants must develop their own proprietary technologies.’”

Besides the motor, the design of the impeller cannot gain clinical approval through simple imitation. The impeller design affects the performance of blood compatibility. The Impella series provides cardiac output support ranging from 2.5 to 5 L/min, with a maximum motor speed of up to 51,000 revolutions per minute. High-speed axial flow pumps generate high-velocity blood flow; if the blade structure and angle are improperly designed or the rotational speed is too high, significant shear forces will be exerted on the blood as it passes through the artificial heart, leading to red blood cell fragmentation and an increased risk of hemolysis.

The design of the impeller is not a simple imitation or replication of rotational speed, structure, and angle; it involves fluid dynamics and flow field design. Merely mimicking the impeller shape of Impella does not ensure clinical efficacy. Impeller design must account for the internal flow field of the device, requiring extensive simulation testing and computational fluid dynamics (CFD) simulations.Core theoretical foundations such as flow field design.

Due to limitations in technological pathways, most market entrants have chosen to launch with high-flow Impella products. These high-flow devices are larger in size and have relatively lower requirements for the motor.

Addressing the aforementioned challenges, what new products have emerged in the field of percutaneous cardiac pumps from a product perspective?

The first major direction is to develop products with smaller dimensions and higher flow rates.

Impella ECP: Poised to Become the Smallest Artificial Heart

The standout feature of the Impella ECP is its smaller size, positioning it to become the world’s smallest artificial heart. With a diameter of only 9Fr (3 mm), it delivers a flow rate greater than 3.5 L/min. Its compact design enables smaller puncture sites, reduces the risk of complications, and expands eligibility to patients with smaller-diameter blood vessels.

The innovative technology enabling the smaller form factor of the Impella ECP is achieved through an externalized motor and a foldable impeller design. The Impella ECP positions the impeller within the left ventricle, while the motor is located outside the femoral artery (extracorporeal), connected to the impeller via a flexible drive shaft. During operation, the catheter draws blood from the left ventricle into the aorta, thereby increasing cardiac output. The ECP has currently received FDA Breakthrough Device designation and is undergoing clinical trials in the United States.

The technical approach of externalizing the motor is highly challenging. The required flexible drive shaft for an externally mounted motor necessitates a long transmission distance, which imposes stricter requirements on transmission stability and carries a higher risk of hemolysis and tissue damage.

Abbott’s interventional heart pump, HeartMate PHP, failed precisely due to its flexible drive shaft technology; Abbott terminated the development of HeartMate PHP in 2021 after it caused patient deaths.

Currently, intracorporeal motor design remains the mainstream approach. Determining whether an integrated or external motor configuration is superior requires additional clinical trial data from the Impella ECP.

Some investors believe that “built-in motors represent a relatively mature technology, whereas external motors warrant attention as a promising technological direction, with potential for further breakthroughs in flow support, timing, size, and even cost.”

Magenta Medical: Aobowei’s Interventional Pump with Smaller Footprint and Higher Flow Rate

Another funded company, Magenta Medical, features a product innovation that delivers robust flow support in a relatively compact form factor.

Magenta Medical’s Elevate is similar to the Impella series, also featuring a folded arterial pump. The key highlight of Elevate is its ability to achieve higher flow rates with a relatively smaller size. Magenta Medical’s device can provide flow support exceeding 5 L/min, with a diameter of only 10 Fr (approximately 3.3 mm). Capable of pumping more than 5 L/min (roughly equivalent to normal adult cardiac output), it reaches a peak flow rate of 7 L/min, making it the interventional heart pump currently offering the highest flow capacity.

The Elevate pump is highly likely to stand out, as no other device offers the unique and powerful combination of an ultra-small diameter and high flow rate. The Impella 5.0 has a catheter size of 21F, and the Impella 2.5 has a catheter size of 12F; both are larger in diameter than the Elevate, yet they provide flow rates of only 2–5 L/min.

Procyrion: Developing an Interventional Pump for the Treatment of Cardiorenal Syndrome (CRS)

The second major strategy involves expanding into more indications. Some overseas companies have positioned interventional pumps at the level of the diaphragm in the descending aorta, aiming to directly increase renal perfusion. For instance, Procyrion, an overseas company, places its interventional pump in the thoracic descending aorta for the treatment of cardiorenal syndrome (CRS).

Cardiorenal Syndrome (CRS) is a common syndrome characterized by inter-organ interaction, injury, and failure. The heart and kidneys are two vital organs in the human body, linked by complex and bidirectional pathophysiological mechanisms. Their interdependence can lead to a vicious cycle wherein deterioration of either organ results in acute or chronic dysfunction of the other. Patients with CRS are often the most challenging to treat. Renal insufficiency secondary to acute heart failure was previously attributed to prerenal hypoperfusion caused by reduced cardiac output.

Procyrion’s aortic pump is placed in the descending thoracic aorta via a percutaneous catheter-based procedure. The company states that it helps directly enhance renal perfusion while reducing cardiac energy demand.

The third major development direction is longer implantation duration, providing short-term transitional therapy for patients awaiting heart transplantation and reducing the incidence of hemolytic events. A representative product in this area is Abiomed’s Impella BTR.

Impella BTR: Expanding Indications to Bridge Therapy for Heart Failure

The Impella BTR is innovated to enable longer implantation durations. While previous Impella devices were typically implanted for periods ranging from a few days to several weeks, the Impella BTR supports implantation for up to 28 days. Upon regulatory approval and market launch, the Impella BTR is expected to expand the indications of the Impella series to include bridge-to-transplant therapy for end-stage heart failure.

Before awaiting a heart donor transplant, patients can first be implanted with left ventricular mechanical circulatory support devices, followed by the transplantation of the donor heart. The full name of BTR is "bridge to recovery," with "Bridge" referring to providing transitional therapy prior to heart transplantation. It is smaller and less invasive than current LVADs, allowing patients with chronic heart failure to opt for a long-term minimally invasive cardiac pump. The Impella BTR has completed its first patient implantation.

From the perspective of future commercial prospects, providing bridge-to-transplant support for heart failure patients is undoubtedly one of the most promising indications.

Heart failure is a severe and irreversible disease that affects more than 60 million patients worldwide. In China, data from the “2022 Report on Cardiovascular Diseases in China” estimate that there are 8.9 million patients with heart failure. In the future, if minimally invasive products can replace left ventricular assist devices (LVADs) in the management of heart failure, they will secure a place in the heart failure market. Currently, patients with end-stage heart failure have only two options: surgical heart transplantation or surgical implantation of a left ventricular assist device (LVAD).

GlobalData predicts that the LVAD market will reach $2.2 billion by 2030. Abbott currently dominates the LVAD sector with its FDA-approved HeartMate 3 device. The HeartMate 3 LVAD is indicated for patients with advanced heart failure who are ineligible for or awaiting heart transplantation.

Major domestic players include Tongxin Medical, Yongrenxin, Aerospace Taixin, Core Medical, and Xinqing Medical.

Heart failure, with its incidence and mortality rates rising year by year, coupled with the scarcity of donor hearts for artificial heart transplantation, has created an urgent need for both short-term and long-term circulatory support among patients in China and the United States. Various novel therapies worldwide are garnering significant attention, making this a key focus area for global companies.

What Kind of Product Will Be the Ultimate Game-Changer in the Future of Heart Failure Management?

Heart failure, as the final frontier in cardiovascular disease, cannot be adequately addressed by a single product to meet the diverse needs of different patients. The future landscape of heart failure therapeutics is likely to feature the coexistence of multiple products, with different offerings launched to address specific clinical needs.

Based on current product trends, it is unlikely that any single product will cover all scenarios or indications in the short term; instead, multiple products will coexist to meet varying flow rate requirements and support duration needs.

Amid this development trend, domestic artificial heart companies have also begun to diversify their product portfolios.

Tongxin Medical, which has received approval for its magnetically levitated left ventricular assist system, is strategically expanding into the field of percutaneous heart pumps through collaborations. The company has reached an agreement with VADovations, a developer of percutaneous heart pumps, to license two patents related to such devices. It is anticipated that Tongxin Medical will offer a diverse portfolio of products in the future.

Core Medical, which has initiated its IPO, has also established a multi-product pipeline in the field of percutaneous ventricular assist devices (pVADs), providing comprehensive therapeutic solutions for medium- to short-term circulatory failure to clinically high-risk patients with varying flow and support duration requirements.

Some companies are also entering the artificial heart market from their life support platforms.

Xinling Maide is building a cardiovascular innovation platform centered on life support. To date, its three independently developed percutaneous ventricular assist devices (pVADs) have all obtained type testing reports and are scheduled to initiate formal clinical trials in the near future. The first domestically produced polymer surgical heart valve has also completed animal studies.

LifeShield has also deeply cultivated the life support platform, completing the development of innovative products such as pVAD (percutaneous ventricular assist device), ECMO systems, and ECCO2R (extracorporeal carbon dioxide removal) systems, with its ECMO system currently entering the human clinical trial phase.

Xinqing Medical has laid out four product pipelines: the extracorporeal magnetically levitated artificial heart, the minimally invasive interventional artificial heart, ECMO (next-generation extracorporeal membrane oxygenation system), and the normothermic organ transport platform.

Innovation in the field of artificial hearts has demonstrated that the answer to the question, “What is the best ventricular assist device?” may always be the next generation of products. This, of course, also tests a company’s capacity for innovation and iterative development.