Golden Era of Consumer-Oriented Medications: Tapping into a Billion-Dollar Market Opportunity

Over the three years of the pandemic, the frenzied yet alluring bubble in consumer healthcare has dissipated. According to the “2023 iCapital China Health Industry White Paper,” based on private equity financing deals with disclosed transaction amounts, a total of 25 financing transactions were completed in the medical services sector in 2022, with total funding reaching nearly RMB 5.2 billion—a 17% decline from 2021 and the lowest level since 2018.

Specifically, leading consumer healthcare companies are operating at substantial losses, while small and medium-sized enterprises are facing even greater hardships, with widespread closures becoming the norm. Taking the medical aesthetics market as an example, data from Qichacha shows that from January to October 2022, a total of 811 medical aesthetics companies and institutions across China were shut down or deregistered.

Despite the cooling financing market and underwhelming market performance, consumer healthcare in the post-pandemic era continues to demonstrate robust vitality, as evidenced by its rapid market expansion. According to a report by Frost & Sullivan, the total market size of China’s consumer healthcare services was approximately RMB 1.26 trillion in 2022 and is projected to reach RMB 2.39 trillion by 2025, representing a compound annual growth rate (CAGR) of 23.78% over the next three years. With the advent of the post-pandemic era and the deepening of healthcare reforms, demands across various medical specialties have evolved. Beyond the traditional “big three” sectors—ophthalmology, medical aesthetics, and dentistry—multiple new consumer healthcare tracks have emerged, including New Traditional Chinese Medicine (TCM), New Rehabilitation, New Psychological Care, New Gynecology, and New Andrology.

Since 2015, a steady stream of policies encouraging private healthcare investment has emerged, drawing capital’s focus to consumer healthcare. Hot subsectors have rotated rapidly: medical aesthetics six years ago, dentistry and ophthalmology four years ago, and in the past two years, “New” Traditional Chinese Medicine (TCM), “New” mental health, “New” rehabilitation, and “New” andrology. According to statistics from the VCBeat Orange Database, there were 78 financing deals in China’s “New” consumer healthcare sectors over the past two years, with total funding approaching RMB 10 billion. Prominent investors such as Sequoia Capital, Matrix Partners, and Hillhouse Capital have all entered the market.

Consumer healthcare refers to medical services and products chosen by consumers to meet their needs for a better quality of life, pursue efficacy value and consumption experience, without relying on basic medical insurance coverage. When focusing on products, it primarily refers to consumer-oriented pharmaceuticals.

Consumer-oriented medications primarily include treatments for hair loss, weight-loss drugs, new traditional Chinese medicines, and men’s health products. These medications share two distinct characteristics: first, they are exempt from medical insurance coverage, with their primary consumption occurring outside hospitals and thus unaffected by medical insurance cost-containment policies; second, they rarely require physician prescriptions to drive demand, as patients can decide to purchase them on their own, exhibiting strong consumer goods attributes.

With the commercialization of the internet, online pharmaceutical transaction models have gradually emerged, allowing users to purchase medications independently. Sales from online pharmacies have grown rapidly, with their market share increasing year by year. Accelerated by the COVID-19 pandemic, the sales volume of China’s online pharmacies (including both pharmaceutical and non-pharmaceutical products) has expanded even more swiftly. According to statistics from Huajing Industry Research Institute, the sales volume of online pharmacies reached RMB 223.4 billion in 2021, a year-on-year increase of 40.02%, with a compound annual growth rate (CAGR) of 57.9% from 2015 to 2021.

As a key category of andrology medications that drive foot traffic to brick-and-mortar pharmacies, these drugs have also become a popular segment in online pharmacies due to their high demand, numerous patient pain points, and strong privacy requirements. According to data released by the Andrology Branch of the Chinese Medical Association, the overall prevalence of erectile dysfunction (ED) among men in China is 26.1%, rising to 40.2% among middle-aged men over 40 years old. The World Health Organization (WHO) predicts that the global number of individuals with erectile dysfunction will reach 322 million by 2025.

Data from Zhongkang CMH shows that in 2022, the market size of the national andrology category (including tier-2 and above hospitals, B2C channels, and retail pharmacies) reached RMB 10.074 billion. Among these, anti-ED drugs accounted for over 90% of the andrology category, with a retail pharmacy sales volume of RMB 6.081 billion in China in 2022, primarily driven by sildenafil and tadalafil. According to forecasts by Head Leopard Research Institute, the current penetration rate of ED drugs in China is less than 5%. In comparison, developed countries generally have penetration rates above 15%, suggesting that the market size of China's anti-ED drug industry could be at least three times its current level, with future market potential exceeding RMB 10 billion.

The anti-ED drug market primarily comprises three categories: foreign originator drugs, generic drugs developed by domestic pharmaceutical companies, and domestically developed originator drugs. Due to the slow development of domestic originator drugs, there are currently few varieties available; thus, the domestic market for andrological medications is mainly dominated by two categories: overseas originator drugs and domestic generic drugs.

Taking sildenafil as an example, originally developed by Pfizer, its annual sales have nearly exceeded $1 billion since its market launch in 1998. After its patents gradually expired in 2012, sildenafil faced fierce competition from generic drugs worldwide, with more than 10 pharmaceutical companies in the Chinese market entering this sector. Generic drugs rapidly captured market share from the originator product due to their high cost-effectiveness. According to various companies' financial reports, by the end of 2016, the market share of sildenafil generics surpassed that of the originator drug, exceeding 50%.

From its pilot launch in 2016 to its full implementation in 2020, the Marketing Authorization Holder (MAH) system has been in place for seven years. Driven by the MAH system, the landscape of China’s pharmaceutical industry is undergoing subtle yet significant changes. Pharmaceutical companies with R&D capabilities and scientific researchers are increasingly transitioning into MAHs. This also presents an opportunity for new retail pharmaceutical enterprises to transform themselves by leveraging the MAH system to develop generic drugs, utilizing their unique channel advantages to reshape the consumer healthcare market.

In recent years, the national volume-based procurement has become normalized, local alliance-based procurement has been continuously implemented, and DRG-based payment by disease type has been strictly enforced. Under the combined effect of multiple medical insurance cost-containment policies, drug prices have dropped significantly. In light of this trend, pharmaceutical companies must accelerate their transformation: either proactively engage in drug R&D, build branded generics, or explore new distribution channels.

A cautionary tale lies right before our eyes. On the first trading day after the 2022 Spring Festival holiday, Guangdong Tai’an Tang Pharmaceutical Co., Ltd., a time-honored brand in traditional Chinese medicine, hit its daily price limit down at the market open. This followed Tai’an Tang’s announcement on the last trading day before the Spring Festival that it had terminated the sale of equity in its subsidiary, Kang’ai Duo. By July 2022, Kang’ai Duo had become embroiled in multiple disputes and was burdened with substantial debt.

The 2019 revision of the Drug Administration Law introduced new provisions to encourage drug research and development and promote the Marketing Authorization Holder (MAH) system. It also lifted restrictions on the online sale of prescription drugs, aligning with electronic prescriptions under the “Internet + Healthcare” model. This created new growth opportunities for the O2O (Online-to-Offline) prescription drug market. Leveraging their e-commerce platform advantages, companies such as JD Health and AliHealth entered the market through pharmaceutical e-commerce operations and rapidly became leading domestic B2C pharmaceutical e-commerce platforms. Meanwhile, the operating space for new-retail pharmaceutical enterprises has been continuously squeezed, with terminal retail prices declining steadily and gross profit margins plummeting sharply. The phenomenon of “the more you sell, the more you lose” has become widespread in the new retail pharmaceutical sector. Clearly, for new-retail pharmaceutical companies, the strategy of opening up new channels is proving unviable.

Amid fierce external competition, new retail enterprises can only look inward—branding generic drugs has become a critical path to breaking through.

Branded generics are not a novel pathway; following the expiration of patents on various originator drugs, generic pharmaceutical companies worldwide have actively entered the market. Taking sildenafil, an anti-erectile dysfunction (ED) medication, as an example, domestically produced generic brands developed by traditional pharmaceutical companies have emerged successively since 2014, gradually capturing market share from the originator drug “Viagra” through competitive pricing and already establishing a certain level of influence.

However, the business models of traditional pharmaceutical companies suffer from numerous drawbacks. Sales channels relying on distributors, agents, and in-house medical representative teams not only incur substantial selling expenses but also fail to capture first-hand user data, resulting in limited customer insights and slower market decision-making. For consumer-oriented medications, particularly men’s health drugs that are highly private and urgently needed, timely identification of user needs and cultivation of brand loyalty are essential for new retail enterprises to break through and succeed.

Among the countless branded generic drugs that have achieved scale effects, “Guan’ai,” a new pharmaceutical brand built by a new-retail pharmaceutical enterprise, has emerged as a standout.

“Guan’ai” was incubated in 2021, entering the market with a focus on male health medications. Its product portfolio includes tadalafil, dapoxetine hydrochloride, sildenafil, and others. According to projections based on current sales performance, annual sales volume is expected to steadily exceed 100 million tablets in 2023. Tadalafil, the brand’s flagship product, is a generic drug that has passed China’s National Consistency Evaluation for Quality and Efficacy of Generic Drugs, offering affordable pricing. Reportedly, “Guan’ai” tadalafil achieved annual sales of over 30 million tablets in 2022.

Sildenafil, tadalafil, and vardenafil are medications indicated for the treatment of erectile dysfunction (ED), commonly referred to as anti-ED drugs. Sildenafil and vardenafil have a rapid onset of action; however, as short-acting inhibitors, they are metabolized more quickly, with a maximum duration of effect of up to 4 hours. Among these three agents, tadalafil is the only long-acting inhibitor and offers distinct advantages. It begins to take effect within 30 minutes after oral administration, reaches peak plasma concentration at an average of 2 hours, has a half-life of up to 17.5 hours, and maintains efficacy for 24–36 hours.

As the three major drugs for treating ED globally, sildenafil and vardenafil are generally recommended for on-demand use in patients with lower sexual demand. However, tadalafil is preferred for ED patients with higher sexual demand or younger age. Tadalafil is available in two regimens: long-acting on-demand use and regular therapy, which can meet the needs of most patients.

As an emerging force in the pharmaceutical industry, the “Guan’ai” brand of tadalafil has rapidly secured a foothold in consumers’ minds through new retail channels. In addition to its advantages in drug quality and pricing, “Guan’ai” has established a Chronic Disease Management Center staffed by professional physicians and pharmacists to provide consumers with comprehensive, full-cycle medication guidance.

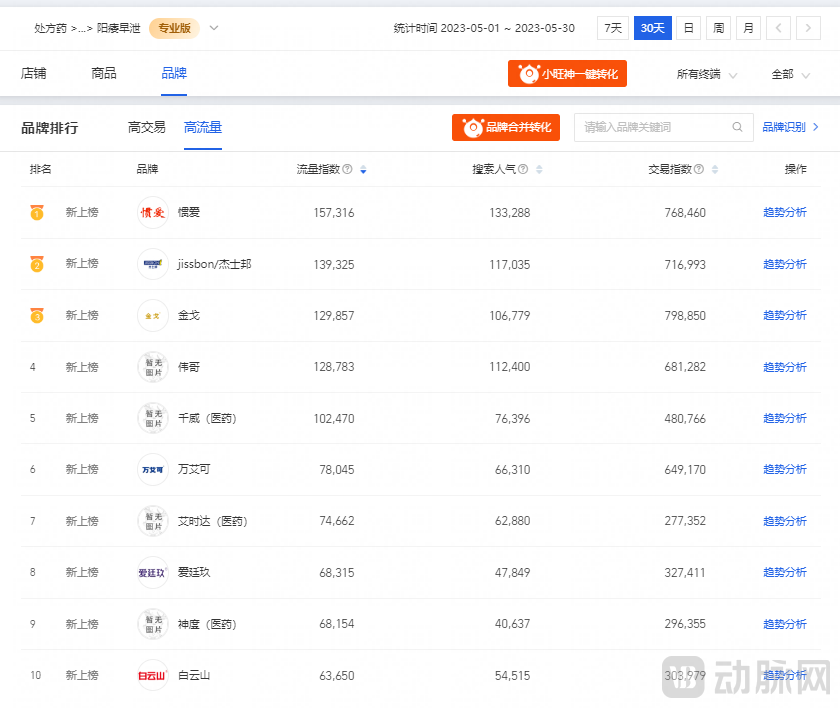

“The strong entry of new brands such as ‘Guan Ai’ is bound to usher in significant changes in the market for chemical drugs in andrology, a trend that is already beginning to emerge. Taking the 30-day brand ranking for the erectile dysfunction and premature ejaculation category on the Tmall platform as an example, ‘Guan Ai’ ranks first by leveraging its advantages in direct-to-consumer (DTC) and new retail models. The well-known family planning brand ‘Jissbon’ has also entered the andrology chemical drug market, capitalizing on this trend and securing second place due to its strong brand loyalty. ‘Jinge,’ the first domestic generic version of ‘Viagra,’ has maintained a leading position both online and offline in recent years thanks to its deep cultivation of the sector. However, it is showing signs of being overtaken in new retail channels and currently ranks only third. Meanwhile, ‘Viagra,’ which created the myth of the ‘little blue pill,’ has fallen from grace amid competition from multiple domestic generics and now ranks much lower.”

Top Brands in the Tmall Men's Health Category for Erectile Dysfunction and Premature Ejaculation (Past 30 Days) (Data Source: Tmall Business Advisor, as of May 2023)

Top Brands in the Tmall Men's Health Category for Erectile Dysfunction and Premature Ejaculation (Past 30 Days) (Data Source: Tmall Business Advisor, as of May 2023)

Consumer healthcare is a vital component of the broader consumer sector, continuously benefiting from demand-side dividends. In China’s pharmaceutical and healthcare market, there are significant discrepancies and contradictions between consumer demand and supply. This supply-demand imbalance will create substantial opportunities for the healthcare market, leading to the emergence of an increasing number of new brands like “Guan’ai” that enter the out-of-hospital pharmaceutical market through novel channels and approaches.

In the field of erectile dysfunction (ED) medication, according to analysis by Sinopharm CMH, ED is a star category in the B2C sector. In 2021, it accounted for 5.6% of the B2C market, with a growth rate as high as 105%. The growth rate of the ED category in e-commerce channels is significantly higher than that in offline retail pharmacies. Data from Sinopharm CMH shows that in June 2022, the year-on-year sales growth of the ED category in offline pharmacies was only 8%. In contrast, sales in the B2C channel grew by 50% year-on-year. Currently, the scale of the ED category in the B2C market has reached RMB 2.9 billion, and the importance of the B2C channel continues to rise.

Andrology medications, as typical consumer-oriented pharmaceuticals, are paving an unprecedented path forward for new retail pharmaceutical enterprises, marking a golden era for the development of consumer healthcare products.