A Lucrative Yet Overlooked Medical Beauty Sector: Why Has This Billion-Dollar-Q1 Industry Been Forgotten by Capital?

IMEIK

Developer of Biomedical Soft Tissue Repair Materials

Bloomage Biotech

Developer of bioactive substance products, producer of hyaluronic acid raw materials

Plum Ventures

Early-Stage Investment Firms

Turning the clock back to 2021, that was nearly the medical aesthetics industry’s most glorious moment.

First, in the secondary market, there emergedListed Companies’ Stock Prices “Rise at the Mere Mention of Medical Aesthetics”the booming phenomenon, among whichHuadong MedicineThe maximum growth rate once reached 120%; furthermore, in terms of revenue, multiple listed companies achieved market growth rates exceeding 80%, among whichBloomage BiotechRevenue in 2021 was RMB 4.948 billion, an increase of 87.93%.Imeik2021 revenue: RMB 1.448 billion, an increase of 104.13%.

Finally, in the primary market, according to incomplete statistics from the VCBeat Orange Database, a total of 68 medical aesthetics companies completed financing in 2021,ZhenFund, Plum Ventures, Fortune Capital, Northern Light Venture Capital, Sherpa Capital, Yuanhe YuandianMore than 100 top-tier investors, among others, rushed to enter the market.

However, this momentum did not continue,The “pigs on the wind” that were hyped up have ultimately come crashing down.Entering 2022, influenced by multiple factors including the pandemic, intensified industry regulation, and heightened market competition, the medical aesthetics market began to undergo significant changes: on one hand, listed companies experienced slowed revenue growth and varying degrees of narrowing net profits; on the other hand, financing in the primary market dropped sharply, with many institutions choosing to reduce their holdings or exit the medical aesthetics market.

So, did things improve in 2023?

Has the medical aesthetics boom stalled in 2022?

Jin Xing, Chairman and CEO of So-Young Group, stated at the beginning of this year, “2022 marked a true winter for the medical aesthetics industry, as the market not only contracted partially but also experienced its first negative growth in two decades.”。

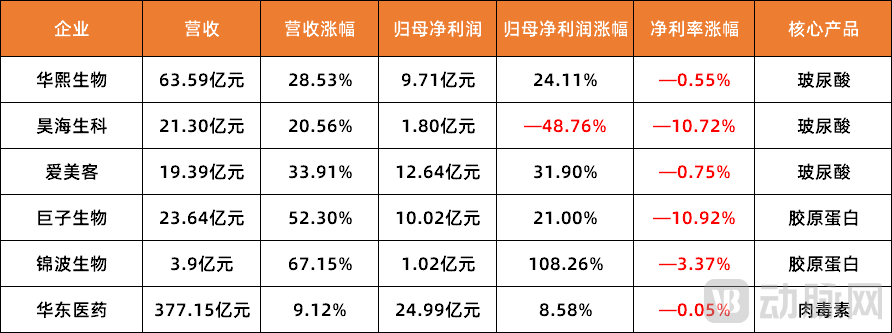

Figure 1. Financial Report Data of Upstream Medical Aesthetics Companies in 2022 (Data Source: Corporate Annual Reports 2022)

This is no exaggeration. A review of the 2022 annual reports reveals that upstream manufacturers, once considered to be capturing the lion’s share of industry profits, have all experienced a slowdown or even a decline in the growth rate of net profit attributable to shareholders of the parent company. Among them, those with hyaluronic acid as their core productHaohai Biological Technologyand with collagen as its flagship productGiant BiogeneThe decline in net profit exceeded 10% across the board. If the upstream segment of the medical aesthetics industry is facing such challenges, the downstream sector is faring even worse, with widespread closures becoming the norm. According to data from Qichacha,In 2022, more than a thousand medical aesthetics companies and institutions in China went bankrupt or were deregistered.。

So, what is the cause of all this?

First and foremost, of course, it is due to the pandemic.Medical aesthetics is a purely offline consumption scenario. However, in 2022, heightened uncertainty caused by the pandemic and successive lockdowns in multiple core cities forced many medical aesthetics clinics into an intermittent operational state of repeated closures and reopenings. Additionally, constrained by the pandemic, the overall economic downturn reduced consumers’ disposable income, leading to a significant decline in their willingness to pay for medical aesthetic services.

Secondly, it is due to strengthened industry regulation.According to incomplete statistics from VCBeat, the Chinese government issued as many as 10 industry policies related to medical aesthetics in 2022 alone. These policies covered the entire medical aesthetics industry chain. Notably, regulations such as the Regulations on the Administration of Medical Institutions and the Catalogue of Medical Devices Prohibited from Contract Manufacturing have brought controversial medical aesthetic products like “skin boosters,” “radiofrequency devices,” and “thread lifts” under Class III medical device supervision and prohibited their contract manufacturing. In addition, significant enforcement actions have been taken against illegal and non-compliant business operations.

Furthermore, product homogenization has intensified market competition.In the medical aesthetics market in recent years, although new products such as microneedling and energy-based devices have emerged, hyaluronic acid remains dominant in terms of market size. However, with increasing competition and technological maturation in this sector, prices for hyaluronic acid—from raw materials to end products—have been declining year by year. According to a report by Frost & Sullivan, the average price of hyaluronic acid raw materials decreased gradually from RMB 210 per gram in 2017 to RMB 124 per gram in 2021, representing a drop of over 40%, with a continued downward trend expected in the future.

Then there is the persistent trap of exorbitant customer acquisition costs.Although the medical aesthetics sector has continued to expand in recent years, driving growth in market size, this expansion has been heavily reliant on marketing efforts. Consequently, marketing expenses have surged, leading to a continuous decline in net profit margins for medical aesthetics companies. Taking Bloomage Biotech as an example, its annual report data shows that in 2022, the company’s selling expenses reached RMB 3.049 billion, a year-on-year increase of 25.17%. Of this amount, online promotion costs totaled RMB 1.722 billion, accounting for 56.48% of total selling expenses—far exceeding the industry average.

Finally, there is a lack of market innovation, making it difficult to achieve breakthrough technologies.An investor specializing in the medical aesthetics sector remarked to VCBeat, “The medical aesthetics industry has long been shrouded in excessive profits, leading to widespread impatience across the sector. Many companies seek shortcuts, while few are genuinely dedicated to research. In reality, China’s medical aesthetics industry started relatively late, and some key technologies remain at an early or rudimentary stage. Continuous R&D is still required to achieve domestic substitution. However, at present, much of what is labeled as innovation merely consists of repetitive R&D, with only a limited number of teams truly mastering independent innovative technologies.”

Therefore, following the industry boom in 2021, the medical aesthetics market has gradually reached saturation. Particularly in 2022, as the pandemic intensified and the overall market environment remained sluggish, this saturation accelerated and became more pronounced. Consequently, it is no longer easy for entrepreneurs or investors to achieve effortless success in the medical aesthetics sector; instead, they are all facing varying degrees of survival crisis.

Finding New Industry Inflection Points Amid the Vortex

In fact, during the peak of the medical aesthetics industry in 2021, traditional pharmaceutical companies, real estate developers, and internet giants were increasing their investments in the sector through various means. This trend declined in 2022 due to market conditions, but cross-industry entry into medical aesthetics emerged as a new trend in 2023.

At the beginning of this year,Yunnan Baiyaostated that its Shanghai Yunzhenni Medical Aesthetics Clinic and Kunming Yunzhen Medical Technology Chenggong General Clinic have both entered the trial operation phase, with the company’s medical aesthetics business progressing steadily; in April this year,Fosun PharmaAn announcement stated that the drug registration application for RT002 (daxibotulinumtoxinA), intended for the temporary improvement of moderate to severe glabellar lines in adults caused by corrugator and/or procerus muscle activity, has recently been accepted for review by the National Medical Products Administration. This marks Fosun Pharma’s formal entry into the botulinum toxin market.

“Outsiders” Are Stepping Up Their Efforts; What Are Publicly Listed Medical Aesthetics Companies Doing?By reviewing the Q1 2023 quarterly reports and the latest market developments of companies, VCBeat has identified some hidden new changes.

First, it is gradually expanding from a single market to permeate the entire industry chain.In the past one to two years, as the medical aesthetics market has gradually become saturated and industry competition has intensified, listed companies across various segments of the industrial chain have recognized their own business bottlenecks, creating an urgent need for business transformation.

withBloomage BiotechTake Bloomage Biotech as an example. As an upstream enterprise, the company has been shifting its focus from the B2B to the B2C market in recent years, launching a series of commercial products based on hyaluronic acid ingredients. These include three product categories: the hyaluronic acid water brand “Shuijiquan,” the hyaluronic acid food brand “Heiling,” and the hyaluronic acid fruit beverage brand “Xiuxiang Jiaoluo.” Additionally, its hyaluronic acid ingredients are gradually entering the milk tea and beverage markets.

According to industry insiders, after building the capability for self-sufficiency from raw materials to finished products, Bloomage Biotech is essentially spending heavily to forge a path from the “B-side” to the “C-side.” While the apparent reason is to enrich its product pipeline, the underlying objective is to facilitate customer acquisition for medical aesthetic institutions by directly educating consumers on the C-side, thereby boosting product market buzz and making it easier for downstream medical aesthetic providers to attract customers.

In addition, those continuously breaking through business boundaries includeNew OxygenUnlike Bloomage Biotech, So-Young operates in the mid-to-downstream segment of the industry. However, in recent years, as its business growth has slowed, So-Young has begun to expand upstream and launched its first hyaluronic acid brand earlier this year.AestheFill, demonstrating its determination to develop upstream agency businesses for medical aesthetics products and strengthen its supply chain. According to a representative from New Oxygen, the company’s ambitions extend beyond launching a single product like ElasTi; rather, it aims to drive a comprehensive restructuring of the entire industry chain through its product offerings.

Secondly, it is essential to cultivate new growth curves based on existing business operations to establish differentiated competitiveness.In fact, after a period of R&D and market exploration, the landscape of the medical aesthetics market has become relatively stable. In the hyaluronic acid segment, Bloomage Biotech, Imeik, and Haohai Biological Technology form the “Big Three,” collectively accounting for over 40% of the domestic market share. In the collagen segment, Giant Biogene and Jinbo Bio are the key players, while Huadong Medicine holds a prominent position in the botulinum toxin market.

However, as previously mentioned, hyaluronic acid was the first niche product to emerge in the medical aesthetics industry. Yet, with increasing competition and maturing technology, it has become difficult for hyaluronic acid to generate substantial profits. Consequently, the “Three Musketeers” of hyaluronic acid must proactively develop new business pipelines.

Therefore,Bloomage Biotech officially entered the collagen industry in 2022 by acquiring a 51% equity stake in Yierkang Biology.;Imeik has expanded its business into new categories such as regenerative materials and botulinum toxin., and thereby securing exclusive agency rights for its botulinum toxin products, while expanding downstream into the skincare sector;Haohai Biological Technology opted to start with equipment., in 2022, it spent RMB 205 million to acquire a 63.64% equity stake in Ohuaimeike, a manufacturer of laser medical devices, thereby expanding its business into the field of radiofrequency and laser aesthetics.

Finally, identifying new growth points in the medical aesthetics market through innovative technologies. Hampered by sluggish business growth, medical aesthetics companies have, in the past year or two, not only integrated the entire industry chain and laid out new product pipelines but also strived to introduce innovative technologies into the medical aesthetics field. By doing so, they aim to enhance the safety and efficacy of treatments, thereby opening up new market segments within the medical aesthetics industry.

·Integrated Diagnosis and Treatment,Combination of Drugs and Medical DevicesTrends Emerge: The Photoelectric Medical Aesthetics Industry Expands Its Potential

Amid the strong tailwinds in the light medical aesthetics sector, photoelectric aesthetic treatments are gaining widespread market acceptance. The underlying logic is primarily that, as non-invasive procedures, they offer a lower barrier to entry and reduced risk, while their relatively affordable pricing endows them with an inclusive nature. Furthermore, this field features high technical barriers and is characterized by continuous innovation and iteration. Finally, regarding the market environment, the medical aesthetic photoelectric equipment sector represents a high-certainty track poised for rapid growth over the next decade. It is currently experiencing a rare market window of opportunity driven by the triple advantages of regulatory compliance upgrades, domestic substitution, and source innovation, creating fertile ground for the emergence of industry giants.

· Lower Costs, Enhanced Efficacy, and Greater Safety: “Synthetic Biology + Medical Aesthetics” Is on the Eve of a Major Transformation

As a new force in the scientific community,Synthetic BiologyIn recent years, it has also demonstrated broad application prospects in the field of medical aesthetics. According to a company executive, upstream raw material production in the medical aesthetics sector relies heavily on animal- and plant-derived substances or chemical compounds, which poses challenges for scaling up, incurs high costs, and carries safety risks. The advantages of biosynthesis lie in its high purity, safety, and homology, making it highly significant for addressing the current need to expand raw material production in the medical aesthetics industry. Once breakthroughs are achieved in technology and industrialization, it will undoubtedly create greater opportunities for the upstream segment of the medical aesthetics supply chain. It is precisely for this reason that, includingGiant Biogene, Bloomage Biotech, Tichuang BiotechMultiple medical aesthetics companies, among others, are continuously increasing their strategic investments in synthetic biology.

· Rewriting the "Anti-Aging Code": The Era of Regenerative Aesthetic Medicine May Be Arriving

As an innovative technology centered on the “holistic and systemic replacement of damaged human tissues,” the integration of regenerative medicine with medical aesthetics enables the restoration, reshaping, and enhancement of human appearance, form, and function by repairing, replacing, or regenerating cells and tissues. It is reported that in 2022, among emerging medical aesthetic procedures, regenerative plastic material fillers experienced the most rapid surge in popularity, further underscoring the significant potential of regenerative medicine in the future medical aesthetics market.

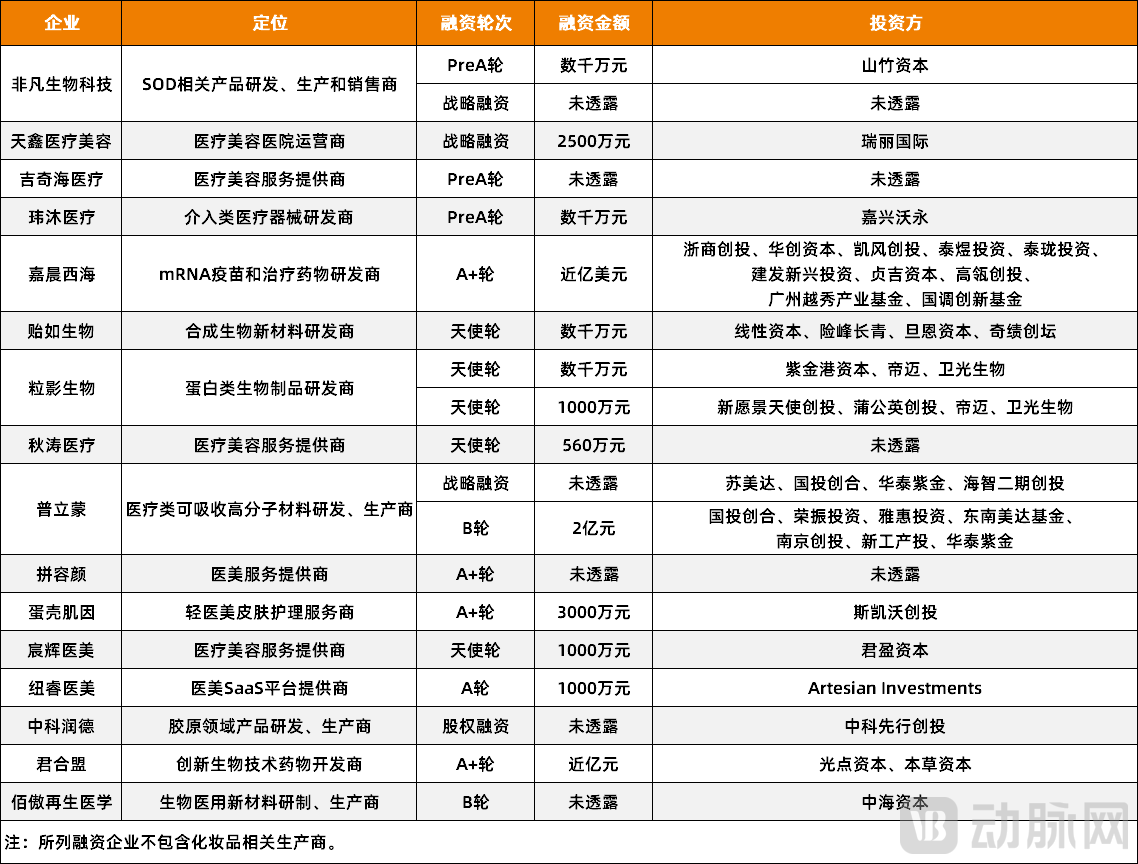

Figure 2. Medical Aesthetics Companies That Completed Financing in 2023 (Data Source: VCBeat)

Figure 2. Medical Aesthetics Companies That Completed Financing in 2023 (Data Source: VCBeat)

These trends have also been validated by startups that completed financing this year. Observations indicate that they have either taken actions in online operations, such asNewRay Medical Aestheticsand# Beauty Face-Off, all aiming to further precisely segment customer groups through digital platforms, thereby achieving customized medical aesthetic services; in addition, there are technological innovations, such asYiru Biotech, primarily leveraging synthetic biology technologies to develop bio-based medical aesthetic materials, whilePulmonis based on biodegradable polymer materials to create a product pipeline of “medical consumables + consumer aesthetic medicine” series.

It is evident that the three-year pandemic, compounded by the advent of an era of stringent regulation, has brought the extensive growth model of the medical aesthetics industry to its peak. The industry is now entering a new development cycle, urgently requiring more disruptive products or business models to stimulate market growth. At this critical juncture of industrial transformation, identifying new market growth curves and making proactive strategic deployments have become shared objectives for enterprises and investors in this sector.

When the Wind Stops, Who Can Still Fly?

After the ups and downs, one cannot help but ask:Is Medical Aesthetics Truly a Good Business?

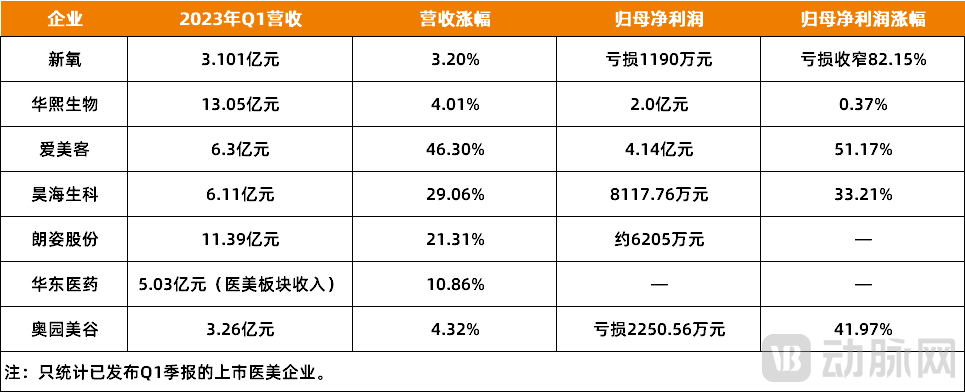

The answer is affirmative. From a short-term perspective, an analysis of the Q1 2023 quarterly reports of multiple listed medical aesthetics companies reveals significant revenue growth across the board. For instance, Imeik achieved Q1 revenue of RMB 630 million, a year-on-year increase of 46.30%, and net profit of RMB 414 million, up 51.17% year on year. New Oxygen also delivered respectable performance, with Q1 revenue reaching RMB 310 million, a 3.2% year-on-year increase. Moreover, amid positive revenue growth, its non-GAAP net loss narrowed substantially, decreasing by 94.3% year on year.

Figure 3. Financial Report Data of Listed Medical Aesthetics Companies in Q1 2023 (Source: Corporate Financial Reports)

Figure 3. Financial Report Data of Listed Medical Aesthetics Companies in Q1 2023 (Source: Corporate Financial Reports)

From a long-term perspective, the medical aesthetics industry in China remains a high-growth sector with strong certainty. According to a report by Frost & Sullivan, China has become the world’s third-largest medical aesthetics market,The market size reached RMB 189.12 billion in 2021 and is projected to reach RMB 399.81 billion in 2026, with a compound annual growth rate (CAGR) of 16.2% over the next five years.。

The remarkably high market growth rate is underpinned by substantial market demand, as well as technological and industrial transformations.First, from the demand sideCurrently, the market penetration rate of China's medical aesthetics industry remains relatively low. In 2018, the number of medical aesthetic procedures in China was 14.8 per 1,000 people, which was only half that of Japan and less than one-fifth of South Korea’s, indicating substantial room for growth compared with countries such as the United States and Brazil.

Furthermore, in the existing market, China's medical aesthetics industry still has significant room for growth driven by repeat purchases, owing to increased penetration rates and higher repurchase frequency among current users. According to the "2022 Medical Aesthetics Industry White Paper" by New Oxygen,In 2023, the number of medical aesthetics consumers in China is projected to reach 23.54 million.。

Secondly, from a technical perspective, as more innovative technologies continue to be integrated into the medical aesthetics field and existing technologies gradually mature, the future medical aesthetics market will see the emergence of more new products and the opening up of more new sectors. Meanwhile, treatment safety and overall efficacy will also improve significantly, and under the influence of a series of regulatory policies, the industry will gradually become compliant.

Finally, from the perspective of market changes, according to forecasts by multiple professionals, non-surgical aesthetic medicine, which constitutes the core of "light" medical aesthetics, will become the mainstay of the future medical aesthetics market. Unlike traditional surgical aesthetic procedures, the light medical aesthetics sector boasts sufficiently long user lifecycles and a high ceiling for user value. The industry’s current scale and growth rate are both significant. Driven by factors such as the accelerated commercialization of new products and services, high repurchase rates for consumer treatments, and strong customer loyalty, light medical aesthetics is poised to unlock even greater market growth potential in the future.

So, under the new landscape of the medical aesthetics industry, who will emerge as the leader first?

By synthesizing insights from multiple industry veterans, VCBeat has identified three distinct characteristics: First, leveraging digital technologies and platforms to further increase market penetration before new markets gain momentum. Second, possessing core products with high barriers to entry, rapidly achieving product branding, continuously investing in R&D, and implementing differentiated product strategies. Third, integrating the entire medical aesthetics industry chain to secure a more proactive position, reduce channel distribution costs to some extent, and thereby expand profit margins.

In retrospect, the consumer healthcare sector is arguably the most fertile ground for generating industry blockbusters. On one hand, it benefits from a mature market that does not require prolonged periods of explosive growth; on the other, its products can be rapidly validated in the marketplace, leading to swift commercial realization. A case in point is the recent surge in popularity of weight-loss products.Semaglutideas well as those that have sold out in the past year or twoHPV VaccineThese are all typical cases, and in the field of medical aesthetics, hyaluronic acid is no exception; over the past few years, it has almost single-handedly sustained the entire medical aesthetics market.

However, as the market gradually becomes saturated, the competitive advantage of hyaluronic acid has begun to wane, prompting the entire medical aesthetics industry to enter a new round of transformation. Therefore, many investors believe that interest in the sector has not diminished; rather, amid an unfavorable macroeconomic environment, capital is steadily converging on medical aesthetics. This is due to its consistent growth, mature market structure, and the rapid commercialization of products. The previous slowdown in pace was merely a period of anticipation for the next blockbuster medical aesthetic product akin to hyaluronic acid.

Therefore,Investment in the Medical Aesthetics Industry May Have Just Begun。