Over RMB 50 Billion Annual Investment Sparks Equipment Upgrade Wave in County Hospitals: Who Will Capture the Emerging Market?

SinoVision

Developer and Manufacturer of High-End Medical Imaging Equipment

United Imaging

High-end Medical Device Developer

Enhancing primary healthcare service capacity has become a key focus for future development. The term “county-level” appeared 13 times in this year’s No. 1 Central Document, highlighting the promotion of county-wide coordination of medical and health resources and the development of medical insurance service capabilities as the direction for future progress.

For primary healthcare institutions, represented by county-level hospitals, ensuring the health and safety of the 900 million people in county-level areas is crucial. The current initiative to enhance medical service capabilities, promote the decentralization of high-quality medical resources, and achieve balanced regional distribution presents a significant opportunity for the development of county-level hospitals. As these hospitals undergo development and upgrades, there will be an expansion in the configuration of medical equipment, creating market opportunities for medical device manufacturers.

The construction of county-level medical care continues to advance, and the wave of medical equipment procurement remains high.

A search on the China Government Procurement Network for winning bid information related to “county people’s hospitals” over the past six months yielded nearly 1,900 results, compared to only about 1,000 during the same period last year. The number of procurement events has nearly doubled, signaling an explosive growth in the county-level healthcare market, which had previously been overlooked.

Not only in terms of volume, but also in procurement expenditure, county-level hospitals have seen higher figures than in the past.

In February this year, the China Government Procurement Network released the “Announcement of Winning Bid for the Medical Equipment Procurement Project of the Xichong County People’s Hospital Chengnan Campus Construction Project.” According to the bidding documents, the project budget amounted to RMB 467.2431 million, with the final winning bid totaling approximately RMB 450 million. Such a large-scale procurement is uncommon among county-level hospitals in China.

The categories procured this time include non-invasive ventilators, imaging equipment, fully automated laboratory automation systems, linear accelerators, and other devices. Domestically produced equipment accounts for the majority of the share, and such procurement events are not isolated cases.

In March this year, the Chinese Government Procurement Network released the announcement for the “Ruijin City People’s Hospital Medical Equipment Procurement Project.” According to the document, Ruijin City People’s Hospital has allocated a budget of RMB 119 million for this procurement, which covers a total of 209 units across 61 categories of medical equipment, including critical care ultrasound systems, hemodialysis machines, multi-parameter ECG monitors, 4K ultra-high-definition laparoscopic systems, 3.0T magnetic resonance imaging (MRI) scanners, and 256-detector 512-slice or ultra-high-end spiral CT scanners.

It is worth noting that the bidding documents also explicitly require the procurement of domestically produced products, and imported products are not permitted to participate in the procurement process.

Since the outbreak of the pandemic, new healthcare infrastructure has entered a fast track of rapid development. With support from various national policies, a large number of county-level hospitals across China are accelerating their growth. According to data from the National Health Commission, as of 2020, there were approximately 16,800 county-level hospitals in China, accounting for 47% of the total number of hospitals nationwide. Their development and upgrading have undoubtedly exerted a significant driving effect on domestically produced medical equipment.

Facilities, talent, and equipment are the three major hurdles that county-level hospitals must overcome in their development.

For the vast majority of county-level hospitals, historical issues in urban planning and construction have left a significant proportion located in the crowded central areas of old town districts. Constrained by limited space and outdated equipment, these hospitals struggle to attract patients. Meanwhile, large tertiary Grade A hospitals at the provincial and municipal levels have continued to expand in recent years, siphoning off a substantial number of patients from primary care institutions. In response, whether through expanding and renovating existing campuses or preparing for the construction of new ones, upgrading hardware infrastructure has become a fundamental strategy for county-level hospitals to retain patients locally.

Hardware alone is not enough; what matters more is disciplinary capability. Many county-level hospitals have chosen to develop specialized departments as a strategic entry point to drive overall institutional growth. However, neither campus construction nor the development of specialized departments can be achieved overnight; both require sustained accumulation over time.

For a long time, county-level hospitals have experienced sluggish development due to the shortage and uneven distribution of high-quality medical resources. However, the challenges facing these institutions have not been overlooked by the state. In 2021, the National Health Commission issued the “Work Plan for Enhancing the Comprehensive Capabilities of County Hospitals under the ‘Thousand Counties Project’ (2021–2025),” which explicitly stated that by 2025, at least 1,000 county hospitals across China should achieve the service capacity level of tertiary hospitals.

With policy support, county-level hospitals across various regions have embarked on the path to achieving Grade III status.

In the 2022 edition of the county-level hospital rankings featured in the Blue Book on Hospitals: Report on the Competitiveness of Chinese Hospitals (2023), all top 100 hospitals were classified as tertiary hospitals for the first time, and the proportion of tertiary hospitals among the top 500 also increased compared to previous years. This indicates that the medical service capabilities of county-level hospitals have been steadily improving in recent years.

For county-level hospitals, achieving Grade III status is also a crucial component of discipline development.

According to the "Principles for the Structural Proportion of Professional and Technical Positions in Medical Institutions," the ratio of senior, intermediate, and junior title holders in secondary hospitals is 1:3:8, which changes to 1:3:6 upon upgrading to a tertiary hospital. This means that when a county hospital is upgraded to tertiary status, the proportion of professional titles will increase. The rise in the proportion of full senior and associate senior titles signifies greater career development opportunities for physicians, which is crucial for attracting talent.

Meanwhile, at the beginning of this year, the “Opinions on Further Deepening Reforms to Promote the Healthy Development of the Rural Medical and Health System,” issued by the General Office of the Communist Party of China Central Committee and the General Office of the State Council, proposed prioritizing primary care levels, accelerating the expansion and balanced distribution of high-quality medical and health resources within county-level jurisdictions, developing disciplines such as emergency medicine, obstetrics and gynecology, pediatrics, critical care medicine, traditional Chinese medicine, psychiatry, geriatrics, rehabilitation medicine, and infectious diseases, enhancing diagnostic and treatment capabilities for major diseases including tumors and cardiovascular and cerebrovascular disorders, and encouraging the establishment of specialized centers for specific specialties and diseases by leveraging existing resources.

The convergence of various favorable conditions has ushered in a significant opportunity for the development of county-level medical institutions. Since the beginning of this year, numerous county-level hospitals across different regions have been upgraded to tertiary hospitals. In March alone, nearly 20 county-level hospitals in Zhejiang and Yunnan provinces achieved this upgrade. Notably, the People’s Hospital of Guiping City in Guangxi was directly accredited as a Grade A tertiary hospital, becoming the first county-level hospital in Guangxi to receive national Grade A tertiary status.

As county hospitals gradually resolved issues related to facilities and staff compensation, the procurement of medical equipment also ushered in a wave of upgrades.

The enhancement of medical service capabilities at county-level hospitals is inseparable from the upgrading of medical equipment configuration.

Behind the Fierce Momentum of County-Level Hospitals Striving for Grade III Status Lies Intensive National Policy SupportIn addition to the “Thousand Counties Project” mentioned earlier, the Implementation Plan for Building a High-Quality and Efficient Medical and Health Service System during the 14th Five-Year Plan Period, jointly issued by the National Development and Reform Commission and the National Health Commission, stipulates that central government budgetary investment subsidies for projects aimed at upgrading standards and expanding capacity at eligible county-level hospitals can reach up to RMB 50 million. In February this year, the State Council’s Opinions on Further Deepening Reforms to Promote the Healthy Development of the Rural Medical and Health System once again emphasized increasing central budgetary investment in leading medical institutions within county-level healthcare service systems.

It is precisely due to strong national policy and financial support that the wave of county-level hospitals across China striving for Grade III status will continue to accelerate.

Henan Province and Hebei Province have both set a target of adding 70 new county-level Grade III public medical institutions within their respective provinces by 2025, while Hubei Province aims to have approximately 100 county hospitals reach Grade III standards by 2025.

For medical device manufacturers, the burgeoning county-level hospital market represents an opportunity that cannot be missed.

Meanwhile, the state has also assessed the current shortcomings of county-level medical institutions.

On May 15, the National Health Commission issued the “Letter on Communicating the Results of the Assessment of Medical Service Capabilities of County Hospitals for 2021–2022” (hereinafter referred to as the “Assessment Letter”), and simultaneously released several documents, including the “Ranking of Compliance with Basic Standards for Medical Service Capabilities of County Hospitals,” the “Ranking of Compliance with Recommended Standards for Medical Service Capabilities of County Hospitals,” “Compliance of Service Capabilities by Department in County Hospitals,” and “Departmental Setup in County Hospitals.” These materials may offer some clues regarding the future development of county-level hospitals.

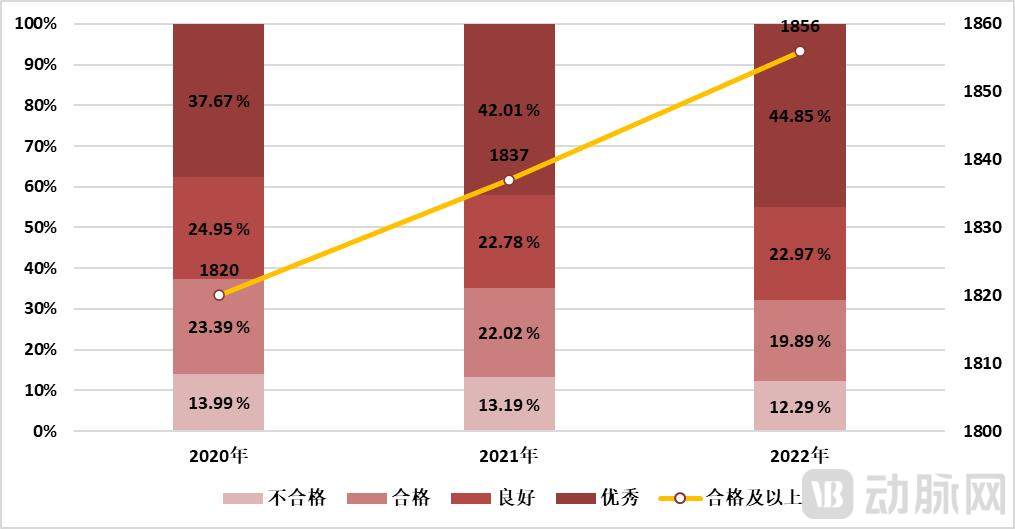

In the "Assessment Letter," the National Health Commission categorized the medical service capabilities of county hospitals into basic standards and recommended standards. The basic standards roughly correspond to the capabilities of secondary hospitals, while the recommended standards are equivalent to those of tertiary hospitals. A total of 2,116 county hospitals participated in the assessment. In 2022, 1,856 hospitals (accounting for 87.71%) met or exceeded the basic standards, and 964 hospitals (accounting for 45.56%) met or exceeded the recommended standards, representing an increase of 19 and 75 hospitals, respectively, compared to 2021.

Proportion of County Hospitals Nationwide Meeting the Basic Standards for Medical Service Capability. Source: National Health Commission

Overall, the medical service capacity of county hospitals continues to improve, which is also corroborated by referral data.

In 2022, 1,928 county hospitals established county-level medical communities. The number of two-way referrals reached 7.2406 million, representing an 8.62% increase compared to 2020. Among these, upward referrals totaled 4.1387 million, a decrease of 14.56% from 2020, while downward referrals amounted to 3.1019 million, an increase of 70.25% from 2020. County hospitals have played an increasingly important role in the healthcare system, serving as a link between urban and rural medical services.

In terms of discipline development, county-level hospitals still need to make further efforts to fully play their role as a bridge and link.

According to the data in the "Assessment Letter," among first-level departments, the establishment rates for psychiatry, otolaryngology, and ophthalmology remain below 80%; the proportion of hospitals whose service capabilities in psychiatry, pathology, ophthalmology, otolaryngology, and surgery meet basic standards is also less than 80%. Among second-level departments, the establishment rates for hematology, vascular surgery, and burn care are below 60%.

In contrast, the equipment configuration rate for 21 items across 12 specialties—including hematology, burn surgery, and thoracic surgery—at county-level hospitals nationwide remains below 30%. The imbalance in equipment configuration rates among the eastern, central, and western regions is more pronounced, with both the configuration rates and their growth rates showing a declining trend. The total value of equipment worth over RMB 10,000 at the bottom 10% of hospitals is only 14.91% of that at the top 10% of hospitals.

Regarding the future development of county-level hospitals, the “Assessment Letter” also points out that for diseases with high incidence and high rates of patient transfer outside the county, county hospitals should accelerate the establishment of departments or specialty groups with currently low coverage, implement relevant diagnostic and treatment services and techniques, and gradually promote appropriate technologies. Efforts should be made to enhance diagnostic and therapeutic capabilities for cancers, cardiovascular and cerebrovascular diseases, respiratory diseases, digestive diseases, and infectious diseases.

This means that these relatively weak departments are currently the focus of future development for county-level hospitals, and the procurement ratio of related equipment will also increase significantly. In addition, with the relaxation of the configuration certificate policy, large-scale equipment such as CT scanners with 64 slices or more and MR systems with 1.5T or higher will further penetrate the county-level market. The county-level market will also witness a wave of equipment procurement.

At the current pace of development, a large number of county-level hospitals will be upgraded to tertiary hospitals over the next three years.

“Promote the expansion and decentralization of high-quality medical resources.” Although this year’s Government Work Report used only 12 Chinese characters to outline the future development focus for county-level healthcare, medical device companies are already gearing up for a major push.

“Actually, many related companies have already started developing county-level markets since 2022,” a medical device sales representative told VCBeat. This trend is also reflected in the intensity of national fiscal support, including RMB 58.855 billion in subsidies for basic public health services, of which RMB 46.362 billion was allocated to central and western regions. Additionally, there were nearly RMB 8 billion in subsidies for comprehensive reform of public hospitals, nearly RMB 5 billion in subsidies for capacity building of healthcare institutions, and RMB 15.57 billion in subsidies for prevention and control of major infectious diseases.

In other words, in 2022, nearly RMB 90 billion in subsidy funds were allocated for medical and healthcare services, with over half—approximately RMB 45 billion—invested in primary healthcare institutions to enhance their service delivery capabilities. Furthermore, the state’s support in the second half of last year, through a phased incentive policy for “new loans for equipment procurement and renovation/upgrading,” has enabled numerous county-level hospitals to upgrade their medical equipment, thereby meeting the configuration standards for Grade II Class A or Grade III hospitals.

It is worth noting that in 2023, the subsidy funds for basic public health services alone amounted to as much as RMB 72.5 billion. Based on this estimate, the subsidy funds allocated this year to enhance the medical service capabilities of primary healthcare institutions will be at least RMB 50 billion.

The state’s sustained support has also strengthened the development confidence of numerous county-level hospitals.

For enterprises, the county-level market also has its uniqueness.

Unlike top-tier tertiary hospitals that prioritize equipment brands and undertake extensive scientific research tasks and exploratory projects, primary healthcare institutions, represented by county-level hospitals, are relatively pragmatic. “Price and payback period are their primary considerations,” said a medical device sales representative. “They are also more concerned about after-sales service; where equipment is prone to failure, as well as subsequent maintenance and associated costs, will all influence purchasing decisions.”

For many county-level hospitals, failing to upgrade may lead to being eliminated by the market, while blind upgrades can trap them in a cycle of high costs, low revenue, and difficulty in recouping investments. This dilemma is particularly acute for county hospitals located in cities with smaller populations.

Current realities have also prompted a shift in the mindset of many county-level hospitals regarding the procurement of medical equipment, particularly large-scale devices. In previous years, domestically produced equipment, such as CT scanners, received little attention during procurement processes. However, over the past two years, higher-level authorities have changed their stance on approving the purchase of domestic equipment. For instance, provinces such as Zhejiang, Guangdong, and Sichuan have issued “Lists of Imported Medical Equipment,” mandating that priority be given to domestically produced devices for those not included on the lists. This policy shift has led many county-level hospitals to begin accepting domestic brands.

According to Frost & Sullivan data, in 2020, CT scanners with fewer than 64 slices accounted for 65% of the Chinese market, while MR systems of 1.5T and below accounted for approximately 74.9%. In 2020, the market size of medical imaging equipment in China was approximately RMB 53.7 billion. Driven by the pandemic, the compound annual growth rate (CAGR) is projected to reach 7.3% in the coming years, with the market size expected to approach RMB 110 billion by 2030.

The vast capacity of county-level hospitals, coupled with varying economic conditions across regions, has led to a diversified market demand. In county-level hospitals located in more economically developed areas, the demand for mid-to-high-end products is growing day by day.

“Many county-level markets are not dominated by mid-to-low-end products as commonly assumed. After years of development, these markets have entered a positive cycle, with relatively rapid refresh cycles for medical facilities. For instance, CT scanners with 128 slices or more were once thought to be found only in large provincial tertiary Grade A hospitals, but in the past two years, many county-level hospitals have begun purchasing such equipment.” This sales representative told VCBeat, “Equipment at large hospitals has become relatively saturated, while the county-level market represents an incremental growth opportunity. Capturing this market is of significant strategic importance for enterprises.”

In late May, the Health Commission of Anhui Province issued the “Notice on the Approval and Licensing for the Allocation of Class B Large Medical Equipment in 2023,” which covered equipment such as positron emission tomography–computed tomography (PET-CT) scanners and conventional radiotherapy devices (medical linear accelerators), with county-level hospitals among the approved institutions.

At this year’s CMEF exhibition, numerous solutions tailored for county-level markets were showcased, featuring both domestic and multinational brands, underscoring a concerted industry focus on this segment. For instance, United Imaging deployed digital and intelligent technologies—including its Smart SkyEye CT, artificial intelligence applications, and regional imaging platforms—in six township health centers in Zhijiang, Hubei Province. This initiative enabled over 30,000 CT examinations annually, equipping these grassroots facilities not only with CT imaging capabilities but also bringing critical care for emergencies such as stroke and chest pain directly to villagers’ doorsteps.

Sinovision, in collaboration with Reed Exhibitions Sinopharm, has launched the Tianmu CT County-Level Healthcare Solution. This solution covers all clinical applications, including cardiovascular imaging, and meets the needs of county-level medical institutions such as county people’s hospitals, county traditional Chinese medicine hospitals, and county maternal and child health hospitals. Equipped with Sinovision Cloud and hospital information systems, it enables inter-hospital connectivity, supports the implementation of tiered diagnosis and treatment policies, enhances county-level healthcare service capacity, and facilitates the decentralization of high-quality medical resources to grassroots levels.

Meanwhile, multinational corporations represented by “GPS” are further penetrating lower-tier markets by continuously increasing their localization rates. For instance, the Voluson Z10 series of obstetric and gynecological ultrasound equipment released by GE Healthcare helps improve the accessibility of high-quality professional obstetric and gynecological ultrasound examinations in county-level areas, assisting county-level and primary care physicians in rapidly enhancing their examination techniques and accuracy.

Driven by new healthcare infrastructure development and compounded by the national emphasis on primary healthcare, exemplified by county-level hospitals, a wave of upgrades for county hospitals across China will inevitably arrive in the coming years. This nationwide surge in medical capacity enhancement will further stimulate demand for equipment procurement. To address the specific needs of the county-level market, enterprises must undertake targeted product iterations to secure a competitive advantage in future equipment procurement cycles; emerging market opportunities must not be missed.