Xishan Technology, the First Surgical Power Device Maker, Lists on STAR Market as More IPOs Follow in This Sector

On June 6, 2023, the field of minimally invasive surgery welcomed another IPO.

Chongqing Xishan Science&Technology Co.,Ltd. Successfully Lists on the STAR MarketChongqing Xishan Science&Technology Co.,Ltd. has successfully listed on the Shanghai Stock Exchange’s Science and Technology Innovation Board (STAR Market). The company publicly issued 13.250367 million new shares at an offering price of RMB 135.80 per share. The total actual funds raised amounted to RMB 1.799 billion, with net proceeds of RMB 1.632 billion after deducting issuance expenses.

Xishan Technology was established in late 1999, when Guo Yijun, a native of Zhuji, Zhejiang Province and a graduate of Chongqing University with a major in Biomedical Engineering, founded the medical device company Xishan Technology in Chongqing.

Xishan Technology’s core products are surgical power tools essential for craniotomy and bone drilling in neurosurgery, orthopedics, and otolaryngology. In clinical practice, physicians use these surgical power tools to resect and reconstruct hard bone as well as soft tissue.

According to the publicly available procurement data for surgical power tools in terminal hospitals, as compiled in Chongqing Xishan Science&Technology Co., Ltd.’s IPO prospectus, from 2019 to 2021, the company ranked second in the number of winning bids for surgical power tools in traditional hospital departments, with a 16.60% share of winning bids, demonstrating a strong market leadership position.

As a hidden champion in the field of surgical power tools in China, Xishan Technology achieved operating revenues of RMB 127 million, RMB 209 million, and RMB 262 million from 2020 to 2022, with a compound annual growth rate (CAGR) of 43.40%; its net profit attributable to shareholders was RMB 14.19 million, RMB 61.4294 million, and RMB 75.3516 million, respectively.

In 2022, surgical power systems generated RMB 250 million in revenue for Xishan Technology, accounting for 97.61% of its total operating income, with disposable accessories for surgical power systems contributing 64.74%. Except for the breast lesion vacuum-assisted biopsy system, which is classified as a Class III medical device, most of its surgical power system products are Class II surgical instruments. The breast lesion vacuum-assisted biopsy system was only approved in 2020, and Class II surgical instruments have contributed the majority of the company’s revenue.

Chongqing Xishan Science&Technology Co.,Ltd. has received investments from multiple institutions. In its Series D financing round in December 2022, the company secured investments from Sinopharm Capital and Jinhe Capital, reaching a valuation of RMB 1.8 billion. Previously, Xishan Technology had also received investments from firms including Jingxu Venture Capital, Junmao Capital, and Haneng Venture Capital.

It is no easy feat to emerge as an “invisible champion” in the surgical power tool market. This sector features multinational giants such as Medtronic, Stryker, and Smith & Nephew that dominate the landscape, alongside more than 30 domestic Chinese manufacturers holding regulatory approvals. How did Chongqing Xishan Science&Technology Co.,Ltd. carve out a path in this red-ocean market and become one of the domestic players with a significant market share? VCBeat (WeChat ID: vcbeat) has compiled an analysis.

In the early days of its founding, Xishan Technology attempted to develop a variety of products, including hemorheology analyzers, semen analyzers, and electric craniotomes. After a period of exploration, Xishan Technology developed an electric craniotome as part of its surgical power device system, thereby entering the surgical power device market.

The market for surgical power tools is characterized by a relatively small size, fragmented competition, and high technical barriers, with domestic manufacturers still lagging behind their import counterparts.

During surgery, the price of disposable consumables for surgical power tools, such as burrs, saw blades, and shavers, is approximately RMB 300–400 per unit, with an average consumption of about one unit per procedure. According to Chongqing Xishan Science&Technology Co., Ltd.’s prospectus, which calculates based on end-user prices, the domestic market size for complete surgical power tool systems is projected to reach RMB 586 million in 2025, while the market size for consumables is expected to reach RMB 5.488 billion.

Orthopedics, neurosurgery, and otolaryngology are the three specialties with the most extensive application of surgical power systems, and these three specialties also constitute the primary market for such devices.

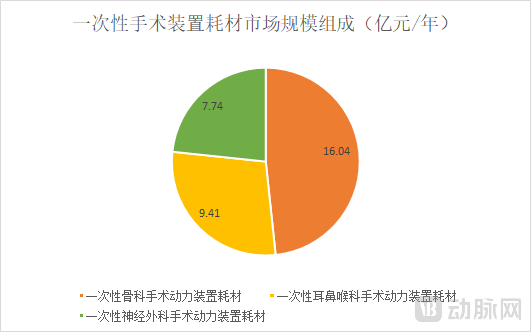

Based on terminal price calculations, and estimated from the average consumption per procedure and product selling prices, the market size for disposable orthopedic surgical power tool consumables was approximately RMB 1.604 billion per year in 2020; that for disposable otolaryngology surgical power tool consumables was approximately RMB 941 million per year; and that for disposable neurosurgical surgical power tool consumables was approximately RMB 774 million per year. Measured at terminal prices, the total market size for surgical power tool consumables in 2020 was around RMB 3.3 billion.

In terms of market size, orthopedics represents the largest application segment for surgical power tools. Surgical power tools are primarily used for osteotomy in joint replacement surgeries and drilling in trauma surgeries. Both joint and trauma procedures have a substantial volume base; in 2021, the number of total knee arthroplasty (TKA) and total hip arthroplasty (THA) procedures in China exceeded 1.2 million, spinal surgeries surpassed 900,000, and trauma surgeries exceeded 3 million.

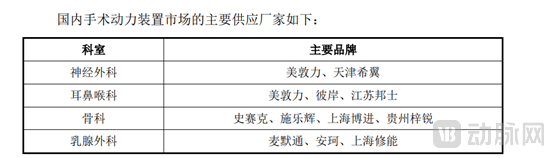

From the perspective of market structure, the domestic surgical power tool market is dominated by multinational corporations such as Medtronic, Stryker, Smith & Nephew, and Mammotome. Medtronic leads in neurosurgery and otolaryngology; Stryker and Smith & Nephew focus on the orthopedics sector; while Mammotome and EnCor specialize in breast surgery.

Why Have Multiple Giants Entered a Market That Is Not Particularly Large?

The fragmented competitive landscape of the surgical power tool market stems from the fact that surgical power tools are merely one component among many in surgical procedures, whereas industry giants typically provide comprehensive consumable solutions for entire subspecialties. The supply of surgical power tools is often bundled with higher-value implant products. Consequently, Stryker, as the leader in orthopedic implants, dominates the orthopedic surgical power tool market, while Medtronic, as the leader in neurosurgical implants, dominates the neurosurgical surgical power tool market.

Domestic companies have initially broken through the barriers in the surgical power device market. According to data from the National Medical Products Administration (NMPA) website, as of December 31, 2022, there were a total of 91 valid registration certificates for surgical power devices (complete systems), including 54 for domestically produced medical devices and 37 for imported medical devices.

However, there remains a certain gap between domestically produced products and imported brands, particularly in terms of product stability and refinement. Domestic products lag behind foreign brands in volume, temperature rise, noise, vibration, consistency, durability, and level of refinement.

Multinational corporations are able to supply a variety of solutions and products, and have accumulated a large base of end-user physicians. The usage habits of clinicians also create barriers for domestic substitution. Therefore, even though Chinese-made products hold as many as 54 registration certificates, they still remain at a disadvantage in terms of market share.

In recent years, the widespread implementation of centralized procurement in the orthopedics sector has accelerated the process of domestic substitution for surgical power devices.

In the past, power tools required for joint surgeries in orthopedics, along with consumables such as saw blades, suction devices, and bone cement, were typically provided free of charge by manufacturers and distributors. However, following the implementation of centralized procurement, channel profits have been squeezed, reducing the incentive for manufacturers and distributors to provide these items at no cost.

Documents issued by Tianjin, Fujian, Hainan, and Hunan provinces regarding the implementation of centralized volume-based procurement for artificial joints explicitly state that medical institutions are responsible for the cleaning and disinfection of non-dedicated power tools and related instruments, with the associated costs included in medical service fees. The introduction of new policies has driven more hospitals to purchase surgical power systems. Volume-based procurement has encouraged hospitals to independently procure surgical power tools, presenting a wave of growth opportunities for domestic manufacturers.

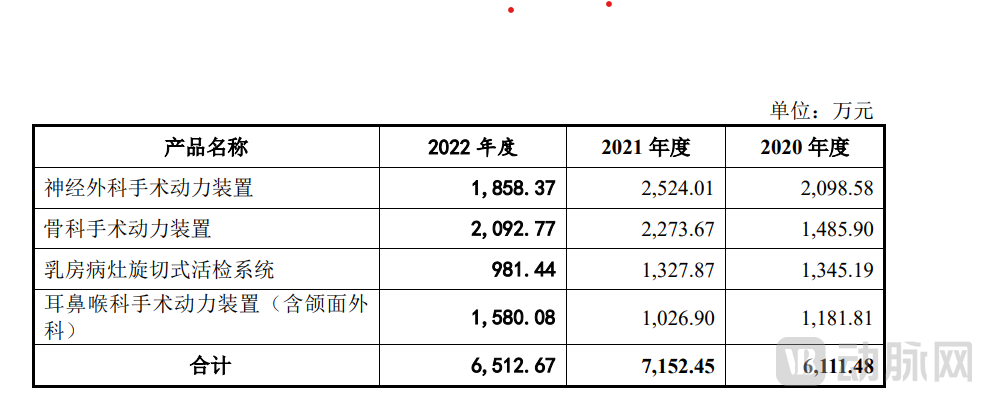

Xishan Technology’s revenue from complete systems clearly reflects this trend. Previously, Xishan Technology’s stronghold was in the field of neurosurgery. Over the past three years, despite the impact of the pandemic, its revenue from orthopedic surgical power tools has achieved overall growth and contributed the largest share of total system revenue.

Revenue from Complete Systems of Xishan Technology

High Barriers and Limited Market Size in the Surgical Power Device Sector: How Did Xishan Technology Grow into a Domestic Hidden Champion?

Unlike multinational corporations that provide all surgical instruments, Xishan Technology has adopted a horizontal layout to supply surgical power systems for multiple departments. As one of the few domestic manufacturers capable of offering multi-department solutions, Xishan Technology is the leading Chinese enterprise holding the largest number and variety of registration certificates for surgical power systems.

How Can Xishan Technology Maintain High-Speed Growth in the Future?

Chongqing Xishan Science&Technology Co.,Ltd. has bet its growth on the market for orthopedic surgical power tools, a key area of focus for the company.

The orthopedics market has seen its industrial structure reshaped by centralized procurement, creating opportunities for new entrants. Seizing this opportunity, Chongqing Xishan Science&Technology Co.,Ltd. has expanded its market share in the orthopedics sector through a price-reduction strategy.

Another major growth highlight for Xishan Technology in the future lies in its Class III medical device, the Breast Lesion Vacuum-Assisted Biopsy System, which received approval in 2020.

Breast tissue biopsy is the gold standard for diagnosing breast cancer. Biopsy methods include open surgical biopsy, fine-needle aspiration biopsy, core needle biopsy, and vacuum-assisted biopsy (VAB).

Vacuum-Assisted Biopsy (VAB) is a newer technology developed on the basis of core needle biopsy. It primarily consists of two components: a rotational cutter and a vacuum aspiration pump. Under imaging guidance, it performs repeated cutting of suspicious breast lesions to obtain histological specimens for biopsy in the diagnosis of breast diseases.

Multinational corporations entered this market decades earlier than domestic companies, giving them a competitive edge; Danaher (Mammotome) and Becton Dickinson (Encor) together command the majority of the market share.

Xishan Technology’s products have filled the domestic gap in this field. Its breast vacuum-assisted biopsy system, “Zhenxuan,” was approved in 2020. Leveraging the price advantage of domestically produced products, it is poised to capture a certain share of the market.

Consumables for breast vacuum-assisted biopsy systems have generated certain revenue for Xishan Technology. Revenue from breast vacuum-assisted biopsy needles increased from RMB 13.2805 million in 2019 to RMB 84.086 million in 2022, representing a compound annual growth rate (CAGR) of 151.63%.

Xishan Technology is also expanding its product portfolio beyond surgical power tools, with a strategic layout in minimally invasive surgical medical devices such as endoscopy systems and energy-based surgical equipment. Among these, Xishan Technology’s 4K endoscope has achieved initial sales on a small scale. Its energy-based surgical equipment lineup includes plasma surgical systems, high-frequency electrosurgical units, ultrasonic bone scalpels, and ultrasonic cutting and hemostatic devices.

However, the endoscopy and energy-based surgical device sectors are also highly competitive. In the endoscopy field, multinational corporations such as Olympus and Karl Storz are prominent players, while domestic participants including Sonoscape Medical, Aohua Endoscopy, Haitai Optics, and OptoMedic have achieved rapid growth. In the energy-based surgical device sector, Johnson & Johnson, Medtronic, and Smith & Nephew dominate the markets for ultrasonic scalpels, high-frequency electrosurgical units, and plasma scalpels, respectively. Meanwhile, numerous domestically produced products have obtained regulatory approval, and companies such as Anhe Jialier, Wuhan Banbiantian, Rich Surgical, Jiangsu Bangshi, Beijing Sumai, and Jessy Technology have also established a certain level of brand recognition.

As a latecomer, Chongqing Xishan Science&Technology Co.,Ltd. faces greater challenges in R&D and operational capabilities to establish a competitive advantage in the endoscopy and energy-based surgical device sectors.

Chongqing Xishan Science&Technology Co.,Ltd. is the second medical device IPO on the STAR Market in Chongqing, following Shanwaishan.

In addition to Chongqing Xishan Science&Technology Co.,Ltd., Chongqing is home to multiple companies specializing in minimally invasive surgery, forming a growing industrial cluster in this field. More initial public offerings (IPOs) from the medical manufacturing sector are expected to follow.

In the field of minimally invasive surgery, Chongqing is also home to Jinshan Science & Technology and Micro-Tech (Nanjing) Co., Ltd. Jinshan Science & Technology has developed a product portfolio that includes capsule gastroscopes, electronic endoscopes, and energy-based surgical instruments. Its products and solutions have been widely adopted in more than 80 countries and regions, including Spain, Italy, the United Kingdom, Germany, Russia, Canada, and India.

MicroPort has achieved breakthroughs in the field of surgical staplers, focusing on minimally invasive surgery. Its product portfolio covers minimally invasive surgical devices, energy-based platforms, and biological hemostatic materials. Since its establishment, MicroPort has remained dedicated to the field of minimally invasive surgical instruments, having built the largest R&D, production, and sales system for this niche market in Southwest China. It boasts the industry’s most comprehensive range of manual and powered endoscopic staplers and holds independent core intellectual property rights for related technologies.

Maikewei is a subsidiary of Haimoni Group, which had previously applied for an initial public offering on the ChiNext board. According to Haimoni’s prospectus, Maikewei is not yet profitable; from January to June 2020, Maikewei generated RMB 22.28 million in revenue.

In the field of oncology treatment, Chongqing is also poised to produce an IPO.During an institutional investor survey conducted on May 6, 2023, senior executives of Guizhou Bailing Pharmaceutical stated that its subsidiary, Chongqing Haifu Medical Technology Co., Ltd. (Haifu Medical), is applying for a listing on the STAR Market. Guizhou Bailing holds a 28.9% equity stake in Chongqing Haifu. Haifu Medical focuses on the field of ultrasound therapy and has achieved breakthroughs in key core technologies for focused ultrasound ablation in tumor treatment. In 2022, Haifu Medical reported net assets of RMB 1.139 billion, operating revenue of RMB 211 million, net profit of RMB 59.854 million, and a book value of RMB 373 million.

The development of Chongqing Xishan Science&Technology Co.,Ltd. in the field of surgical power systems reflects that the minimally invasive surgery sector is currently experiencing rapid growth, with a diverse range of products, many of which are undergoing import substitution by domestic alternatives. Although multiple industrial clusters have already taken shape in China’s minimally invasive surgery sector, domestic enterprises are generally small in scale, and the high-end segment remains heavily reliant on imports. Achieving autonomous and controllable supply chains in the future will require further breakthroughs.