Another Major Consumption-Driven Medical Device Included in Centralized Procurement: How Will the Market Landscape Transform?

Autek China

Rigid Gas-Permeable Contact Lens Manufacturer

Eyebright Medical

Ophthalmic Medical Product R&D Provider

Since the Hebei Provincial Healthcare Security Administration issued a notice on centralized procurement of medical consumables in 2022, discussions have persisted in the ophthalmology market regarding significant price reductions for orthokeratology lenses and the resulting impact on healthcare institutions’ revenues.

After more than half a year, various speculations can finally come to an end. Recently, the proposed winners of the first centralized procurement for orthokeratology lenses were announced, marking another major product in the consumer healthcare sector to undergo centralized procurement, following dental implants.

Based on the volume and price reduction magnitude of centralized procurement for orthokeratology lenses, the direct short-term impact on the industry is relatively limited. However, in the long run, it is inevitable that market penetration will increase due to price reductions from centralized procurement, innovative products will become increasingly diverse, and competition will intensify. At that point, the market landscape will undergo significant transformation.

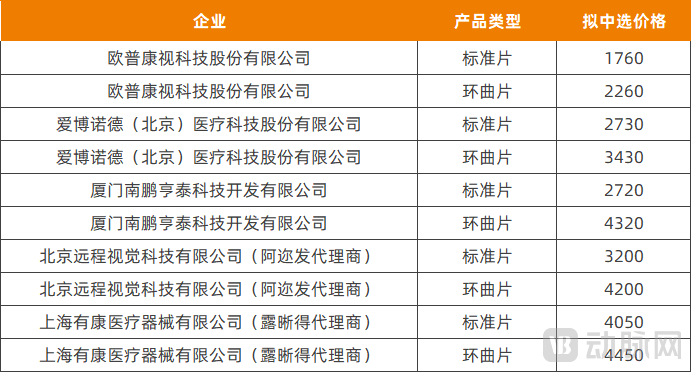

On June 2, the proposed winning bid results for the centralized procurement of medical consumables led by Hebei Province under the Sanming Procurement Alliance were announced. Five companies involved in the production or distribution of orthokeratology lenses were selected as proposed winners, covering ten products across two categories: standard lenses and toric lenses. Among the proposed winning products, the highest price was RMB 4,450 per lens for toric lenses, while the lowest price was RMB 1,760 per lens for standard lenses.

Proposed Winning Products and Prices for Orthokeratology Lenses in Centralized Procurement; Data Source: Hebei Provincial Healthcare Security Administration

According to the procurement documents, the regions participating in this centralized procurement include five provinces and autonomous regions—Hebei, Hainan, Qinghai, Jiangxi, and Guangxi—as well as members of the Sanming Alliance: Sanming, Yuxi, Xiangxi, Jixi, Luoyang, Wuhai, Yuncheng, Hohhot, Zhoukou, Zhaotong, and Xilingol. All public medical institutions and military medical institutions within the alliance regions that provide orthokeratology lens fitting services are required to participate, while other medical institutions are encouraged to join.

Due to the limited coverage area and the fact that demand was primarily reported by public hospitals, the contracted volume for this centralized procurement was not large, totaling only 14,342 lenses. It is understood that as early as 2018, the domestic usage of orthokeratology lenses had already reached 640,000 units, with continued growth in recent years. In comparison, the volume of this centralized procurement accounts for only a small fraction of the overall market.

Additionally, according to survey data from Soochow Securities, among the products proposed for selection, referencing prices in cities such as Hangzhou and Zhengzhou, Autek China’s price reductions were approximately 27%/34%, and Eyebright Medical’s reductions were approximately 22%/30%, which aligns with market expectations.

Overall, whether in terms of procurement volume or the magnitude of price reductions, this round of centralized procurement was “gentler” than industry expectations.For consumers, compared to the previously common practice ofOne pairTotal prices that once exceeded 10,000 yuan now have more options in the several-thousand-yuan range after centralized procurement.

“Within the optometry industry, private ophthalmic medical institutions hold the majority of the market share, while their volume within the public hospital system is relatively small; consequently, the volume involved in centralized procurement is also limited,” said Wang Zhen, a partner at Mingfeng Capital. He noted that the current impact of this centralized procurement on the industry is limited, but it is expected to expand in the future, gradually increasing market penetration.

Upstream medical device companies view centralized procurement with a positive outlook. Eyebright Medical disclosed in its annual report that pilot programs for the centralized procurement of orthokeratology lenses are currently underway. If the scope of centralized procurement expands, it will have a significant impact on product sales to public hospitals. The implementation of centralized procurement for orthokeratology lenses is expected to promote the separation of service fees from consumable costs in ophthalmic diagnosis and treatment expenses. Based on the results of centralized procurement for similar products, the anticipated reduction in the end-user price of orthokeratology lenses is projected to increase their sales volume and penetration rate in China, thereby benefiting more patients.

Ophthalmic healthcare service providers also view centralized procurement from a more comprehensive perspective. Aier Eye Hospital stated during an interview that the penetration rate of orthokeratology lenses in mainland China remains extremely low. If centralized procurement can lower barriers to some extent, trading price for volume could benefit more adolescents. The fitting of orthokeratology lenses is a medical service requiring professional qualifications and technical expertise; as the volume of business increases, economies of scale will become more pronounced. Moreover, there are diverse methods for myopia control, with orthokeratology being just one option, so there is no need to “panic at the mere mention of centralized procurement.” In addition,From the perspective of changes in medical insurance policies, relevant authorities are not solely focused on low prices; their intention to protect innovation and sustain its momentum is becoming increasingly clear.

Recently, Huaxia Eye Hospital also stated to investors that the previous revenue proportion of orthokeratology lenses was low, and after the price decrease, sales volume will increase, which is actually conducive to promoting growth.

In recent years, orthokeratology lenses have emerged as a hotbed for innovation in ophthalmic devices. The surge in demand has significantly propelled market development; over the past year, even amid adverse external conditions, orthokeratology lenses drove substantial growth for several ophthalmic device companies.

Autek China disclosed in its financial report that the revenue from rigid gas permeable contact lenses reached RMB 763 million in 2022, a year-on-year increase of 11.04%, with orthokeratology lenses accounting for the vast majority. This growth was primarily driven by the rising adoption of orthokeratology lenses and increasing demand for fitting services.

As of now, Autek China has two orthokeratology lens brands: “DreamVision” and “DreamVision.” Its products feature personalized customization, high corrective power, and short delivery cycles. The company demonstrates strong competitiveness in technical training, fitting support, nationwide networked services, and safety assurance, which has driven sales growth among its partnered endpoints. Notably, the DreamVision brand of orthokeratology lenses has been in use for 16 years, serving over 1.5 million users.

In 2020, Eyebright Medical’s PnuTong orthokeratology lenses generated RMB 174 million in revenue, a year-on-year increase of 62.09%; orthokeratology lenses accounted for 30.14% of Eyebright Medical’s core business revenue.

It is reported that the Procor Ortho-K lens adopts an aspheric base curve design, aiming to better slow myopia progression by improving peripheral defocus. Procor has demonstrated certain advantages in terms of corneal staining rate, fitting success rate, and breakage rate, enabling rapid market penetration within three years of its launch. By the end of 2022, Procor had reached more than 2,000 medical institutions across China, with cumulative sales exceeding 600,000 lenses.

Haohai Biological Technology has strategically focused on two key sectors: ophthalmology and medical aesthetics. In the ophthalmology segment, vision care end-products generated RMB 199 million in operating revenue in 2022, an increase of RMB 143 million from the previous year, representing a growth rate of 259.78%. Vision care end-products include orthokeratology lenses and related equipment and lubricating eye drops used during fitting and wear, soft contact lenses, and phakic intraocular lenses.

Previously, Haohai Biological Technology’s revenue from orthokeratology lenses was primarily derived from agency sales. Subsidiaries of Haohai Biological Technology held exclusive distribution rights in mainland China for Henritek Optics’ high-end orthokeratology lens product “myOK” and its orthokeratology lens product “Henritek Hiline.” In 2022, Nanpeng Optics, which operated the agency sales business for orthokeratology lenses, was consolidated into Haohai Biological Technology’s financial statements, resulting in a significant increase in revenue from optometric products such as orthokeratology lenses.

As the orthokeratology lens market advances at a rapid pace, the number of enterprises and brands entering this field is also increasing.

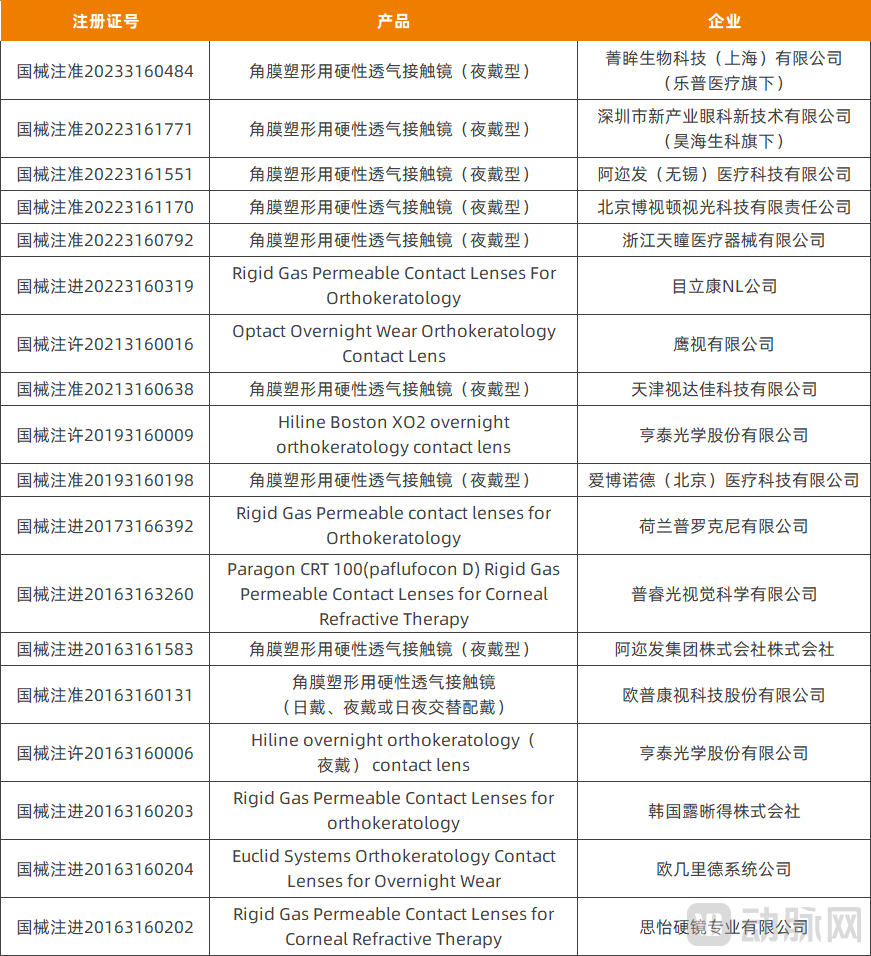

According to data from the National Medical Products Administration, five additional orthokeratology lens products have been approved since 2022; as of now, a total of 18 products have been approved, with an increasing proportion being domestic brands.

Approved Orthokeratology Lens Products, Source: National Medical Products Administration

Among the products approved since 2022, the Tiantong TTOS orthokeratology lens has expanded the eligible patient population through product iteration, meeting the needs of more patients. Combined with a simpler fitting procedure, it achieves superior visual quality and myopia control outcomes.

In addition to distributing orthokeratology lenses as an agent, Haohai Biological Technology’s self-developed “Tongxiang” orthokeratology lens received regulatory approval in 2022 and was launched for commercial sales in 2023.

Tongxiang is developed and manufactured using Contamac’s high-oxygen-permeability materials, a subsidiary of Haohai Biological Technology. It features a TFT (Tear Film Technology) design to address the instability of tear reservoir capacity and poor central positioning performance associated with existing products. Leveraging a customized myopic defocus system, it achieves a better balance between visual quality and myopia control. Additionally, the product’s free-axis design ensures more precise lens positioning.

Lepu Medical, which has an extensive portfolio of medical devices, has also entered the orthokeratology lens market. Its Jingmou orthokeratology lens was approved in April 2023 and quickly launched for sales. The annual report indicates that Lepu Medical is also developing another orthokeratology lens, “Xingtai,” which is expected to reach commercialization in 2024.

In 2022, the National Medical Products Administration approved Eyebright Medical’s registration application to expand the diopter range of its orthokeratology lenses, enabling coverage for a broader population of myopia patients.

In addition, companies such as Visioneering, Willsee, Leiming Vision Care, and YandeLe also have orthokeratology lens product lines and are at various stages from research and development to registration. Overall, in the orthokeratology lens market, domestic brands are accelerating their rise, with products covering a broader population and featuring more prominent personalized and intelligent design characteristics.

The initial phase of centralized procurement has been moderate. Uncertainty remains regarding whether its scope will be expanded and, if so, at what pace. Nevertheless, it is certain that substantial market space and opportunities still exist outside the scope of centralized procurement.

In fact, even if the scope of centralized procurement expands in the future, there is no need to “panic at the mere mention of centralized procurement,” as Aier Eye Hospital has stated. The current landscape of the orthokeratology lens market is undergoing changes to adapt to the industry environment, including the impact of centralized procurement.

First, the trend of “import substitution with domestically produced goods” is emerging.

Centralized procurement poses greater challenges for higher-priced imported brands; some brands have established R&D centers, set up factories, and registered products in China to achieve a higher degree of “localization,” thereby minimizing these challenges.

In 2020, Alpha Group Co., Ltd. of Japan decided to establish a production base in China, selecting Wuxi Xinwu District as the location and founding its wholly-owned subsidiary, Alpha (Wuxi) Medical Technology Co., Ltd.

On July 22, 2022, the registration application for Aierfa orthokeratology lenses was accepted by the National Medical Products Administration (NMPA). The technical review was completed on November 11 of the same year, with a total review period of 112 calendar days, representing a significant reduction in the cycle time compared to previous practices.

Thus, Arifa also completed the entire process from company establishment to product approval within just two years.

In 2021, the U.S.-based Euclid Group signed an agreement with the Administrative Committee of Suzhou New District to establish a research and development and production base in the Jiangsu Medical Device Technology Industrial Park. According to announcements released by the Suzhou New District, this project marks Euclid’s first global production facility constructed outside its U.S. headquarters, with the Chinese market accounting for 85% of its global consumption rate. The project is expected to obtain registration certificates for Class III medical devices and achieve mass production by 2026, thereby meeting future product demand in the global market.

“Import Substitution with Domestic Production” has been a major trend in the medical device industry in recent years. Similarly, in the consumer healthcare sector, Invisalign has long established a production base in China’s “Dental Valley” in Ziyang. To date, it has obtained three registration certificates for clear aligners through its subsidiaries incorporated in China.

The “localization” of foreign brands facilitates more efficient product R&D and registration; by shortening the distribution channels and distances from production to end-users, it reduces the overall cost of products; furthermore, it enables better service to Chinese doctors and patients.

Second, distribution channels are being shortened, and collaboration between ophthalmic device companies and healthcare institutions is becoming closer.

In the view of Wang Zhen, a partner at Mingfeng Capital, the impact of centralized procurement for orthokeratology lenses is similar to that for premium intraocular lenses: upstream, manufacturers’ ex-factory prices are significantly lower than market prices; centralized procurement will reduce the profits of channels and intermediaries, which is beneficial for upstream enterprises with comprehensive product portfolios.

This means that the channels between upstream and downstream will be shorter and more direct.

In its annual report, Autek China stated that to mitigate the risks associated with centralized procurement, the company will not only increase new product development, enrich its product matrix, and enhance personalization but also reduce distribution layers and increase direct supply to hospitals to safeguard corporate earnings. A key measure is to strengthen the construction of majority-owned and equity-participated terminal outlets, compensating for the decline in revenue and profit resulting from product price reductions through high-quality services and service fees.

In fact, in recent years, Autek China has acquired controlling stakes in a number of optometry service terminals, including eye hospitals, outpatient clinics, general clinics, and vision care centers. In 2022, the company expanded its portfolio of controlled marketing and service terminals through investment, thereby boosting sales of orthokeratology lenses and increasing revenue from other optometry services.

Aier Eye Hospital and Remote Vision have launched the Aier Remote Vision Outpatient Clinic, offering services such as myopia control for children and adolescents, marking an attempt to foster closer collaboration between upstream enterprises and downstream service providers.

Nevertheless, regardless of how the future market landscape evolves, the wider adoption of orthokeratology lenses and the further increase in market penetration are inevitable trends. According to a research report by Haitong Securities, the penetration rate of orthokeratology lenses in China is approximately 1.6%, representing a significant increase from the less than 1% recorded a few years ago. Multiple research institutions have pointed out that, compared with the 5%-10% penetration rates in European and American countries as well as neighboring Asian nations, there remains substantial room for growth in China’s orthokeratology lens market.

Amid the rising trend in market penetration, medical device manufacturers and service providers that offer high-quality products and personalized fitting services, while addressing the practical needs of consumers across all segments, will always be able to maintain their footing amidst change.