Can RMB 260 Billion in Revenue Build a World-Class IVD Leader?

Sansure Biotech

Provider of Total Solutions for In Vitro Diagnostics

EasyDiagnosis

Developer, Manufacturer, and Seller of In Vitro Diagnostic Reagents and Supporting Instruments

Andon Health

Developer and Manufacturer of Health-related Electronic Products and Smart Hardware

Legend Capital

Early-stage venture capital and growth-stage private equity investment institutions

DaAn Gene

Clinical Laboratory Reagents and Instruments R&D, Production, and Sales

Fortune Capital

Venture Capital Institution

Over the past three years,IVD companies have reaped huge profits while helping to control the epidemic. According to media statistics, in 2022 alone,ChinaThe total revenue of 62 IVD-related companies reached RMB 263.96 billion, with a combined net profit of RMB 72.75 billion.Among them,COVID-19 RelatedofBusinessTotal RevenueUltra100 billionYuan.

Although domestic IVD companies have collectively generated over RMB 260 billion in revenue, they still lag behind overseas giants in terms of technology, brand recognition, distribution channels, management capabilities, production capacity, and R&D capabilities.

Now that conditions have returned to normal, can IVD companies, armed with substantial wealth, create a world-class industry leader by burning cash? How are IVD companies currently spending their funds? Which segments, stages, and technologies within the IVD industry can be accelerated through capital investment?

Currently, a large number of listed IVD companies are planning to deposit substantial cash reserves in banks to earn passive interest income.

The most representative example is Andon Health, which raked in RMB 14 billion in just three months. In February 2023, the company announced plans to use RMB 17 billion (or an equivalent amount in foreign currencies) of its own funds for entrusted wealth management and RMB 3 billion of its own funds for securities investment.

Meanwhile, in 2022, top IVD manufacturers by revenue, including EasyDiagnosis, Oriental Biotech, DaAn Gene, Wondfo, and Kehua Bio-engineering, announced plans to utilize RMB 5 billion, RMB 3 billion, RMB 2.5 billion, RMB 1.975 billion, and RMB 1.8 billion of their own funds, respectively, for cash management purposes. These funds are primarily intended for purchasing financial products or deposit products characterized by high security, strong liquidity, and principal protection.

It is worth noting that cash deposits in banks account for a significant proportion of these IVD companies’ assets. For example, as of December 31, 2022, Anxu Biotechnology’s balance of monetary funds was RMB 2.138 billion, representing 30.8% of its total assets; the book balance of investment and wealth management products purchased for cash management purposes was RMB 3.442 billion, accounting for 49.59% of its total assets.

Investors focusing on the IVD industry stated, “For enterprises, the most critical factor is stable development. Stability ensures longevity and creates more opportunities for growth and expansion. On the other hand, given that the current economic recovery has fallen short of expectations and the IVD sector is facing disruptions from centralized procurement, market conditions remain highly uncertain. Enterprises must strengthen risk management and secure sufficient capital reserves to support future development.”

In addition to capital-protected wealth management products, relevant IVD companies also mitigate risks by purchasing land and constructing buildings for corporate operational use.

For example, Sansure Biotech invested RMB 350 million to build its Shanghai Industrial Park; Baotai Biological spent RMB 1.2 billion to establish the Xiamen POCT Industrial Park; EasyDiagnosis invested RMB 1 billion to develop its Technology Industrial Park; and BGI Group allocated RMB 470 million to create the Qingdao Health and Medical Industrial Park...

In addition to building industrial parks, IVD companies are also establishing R&D centers, production bases, and operational hubs to accelerate the development of their core businesses. Notably, in April 2023, Autobio Diagnostics acquired the plot JG1801-M1-14 in the Digital Commerce City Unit of Hangzhou for RMB 17.09 million through auction, with plans to construct a high-end biomedical R&D, manufacturing, and management center. Upon completion, the center will support R&D and frontier technology layout across Autobio’s five major technology platforms—biological raw materials, immunochromatography, dry chemistry biochemistry, chemiluminescence, and precision diagnostics—as well as the manufacturing of medical devices and equipment.

Hybribio has made a substantial investment of RMB 1.512 billion to construct the Hybribio Medical Science Park. Covering an area of approximately 235 mu, the project will be developed around the entire in vitro diagnostics (IVD) industry chain, establishing production bases for high-end biomedical laboratory consumables and IVD raw materials, nucleic acid molecular testing reagents, and medical packaging materials, as well as a research, development, and intelligent manufacturing base for biomedical instruments, and an innovation research center. Reportedly, this project was designated as Chaozhou’s No. 1 Key Project in 2022 and was also included in Guangdong Province’s 2023 Key Construction Project Plan. Additionally, in January 2023, Hybribio acquired a plot of land for RMB 48.19 million to build a women’s and children’s hospital.

With the development of industrial parks, relevant IVD companies will gradually transition from production- or R&D-oriented enterprises to platform-based enterprises, thereby enhancing their risk resilience. Meanwhile, by establishing R&D centers, operational hubs, and manufacturing bases aligned with their own strategies, these IVD companies will accelerate their growth and more rapidly evolve into globally leading multinational IVD giants.。

In the medical device industry, there is a saying: “No M&A, no giants.”

Especially in the IVD sector, Danaher’s relentless acquisition strategy has earned it the reputation as the “King of M&A.” Today, domestic IVD companies, armed with substantial cash reserves, are following Danaher’s playbook and embarking on their own investment and M&A journeys.

Among them, Wondfo Biotech continues to increase its investment.Chemiluminescence Field, acquired Tianshen Medical in February 2022. It is reported that Tianshen Medical is a developer of in vitro reagents and POCT projects. Its portfolio includes five models of single-use chemiluminescence instruments capable of covering hundreds of test items, combining the operational flexibility of compact POCT products with the high-performance characteristics of chemiluminescence detection systems, thereby meeting the rigid global demand for high-quality POCT products across healthcare institutions of all levels.

EasyDiagnosis, meanwhile, is accelerating itsMolecular Diagnosticslayout, invested in Nanjing Nuoyin in November 2021. Established in 2020, Nanjing Nuoyin has independently developed comprehensive solutions for the rapid detection of common pathogens and the comprehensive testing of acute and critical infections, leveraging its two cutting-edge technology platforms: multiplex PCR and metagenomic next-generation sequencing (mNGS).

EasyDiagnosis stated that compared with hybridization technology and gene chips, PCR technology is currently the mainstream technical platform for molecular diagnosis, offering advantages such as high sensitivity and ease of adoption; however, it is limited by its ability to detect only single, known loci. As innovative technologies, digital PCR and multiplex PCR can achieve quantitative detection and multi-target diagnosis, respectively. As key directions for clinical development, digital PCR and multiplex PCR are currently in a phase of rapid adoption. By investing in Nanjing Nuoyin, the Company can acquire molecular diagnostic technologies for multiplex PCR and high-throughput sequencing, thereby increasing its market share in the field of pathogenic microorganism molecular diagnostics.

Additionally, EasyDiagnosis invested in Digifluidic Biotech Ltd. in September 2022. Founded in 2018, Digifluidic Biotech is a technology-driven enterprise centered on independent innovation, dedicated to building a life science analysis and operation platform based on digital microfluidics technology.

RainSure Scientific is one of the representative enterprises in the field of digital PCR. Currently, RainSure has successfully launched a range of products, including the DropX series digital PCR systems, over 100 RUO (Research Use Only) assay kits, the Fast-16 quantitative real-time PCR instrument, and nanoparticle synthesis systems. Notably, RainSure’s digital PCR systems have obtained three major medical certifications: NMPA, FDA-EUA, and CE-IVD, making it the only digital PCR system to receive such distinctions.

In addition, Cofoe Medical has strengthened itsPOCT Sectorstrategic layout, and announced plans in late 2022 to acquire 100% equity interest in Laihe Biotechnology. Founded in 2012, Laihe Biotechnology has remained focused on the research and development, manufacturing, sales, and services in the fields of POCT (point-of-care testing), monitoring, and health information technology.

Among the investments and M&A activities in the IVD sector since last year, the most notable has been Mindray Medical’s €532 million acquisition of an overseas in vitro diagnosticsUpstream Raw MaterialsHyTest Invest Oy and its subsidiaries. Through this acquisition, Mindray has acquired corresponding technologies and R&D capabilities for in vitro diagnostic raw materials, thereby establishing a cost advantage.

Overall, in China's IVD sector, chemiluminescence, molecular diagnostics, POCT, and upstream raw materials are currently the most sought-after segments, with numerous listed IVD companies and innovative startups vying for position.

In addition to directly engaging in investments and M&A, relevant IVD manufacturers have also made bold investments in venture capital (VC) firms to help implement their strategic layouts.

Notably, in September 2022, Andon Health invested RMB 340 million to simultaneously back five venture capital firms—Jifeng Capital, Yuansheng Venture Capital, Wuyuefeng Capital, Yaotu Capital, and Huixin Investment—sending shockwaves through the entire venture capital community. According to reports, the funds in which Andon Health participated primarily target investments in healthcare, as well as technology sectors such as information technology, advanced manufacturing, and new materials.

(Andon Health Invests in Five VCs)

Anxu Biologics also announced that it will jointly establish Hangzhou Zhongchuan Anxu Equity Investment Partnership with Zhongchuan Financial Holdings Equity Investment Fund and Guohan Investment Management, with a capital commitment of no more than RMB 500 million, to invest in enterprises or projects in the fields of pharmaceuticals, general healthcare, and biomedicine that are in their start-up or growth stages.

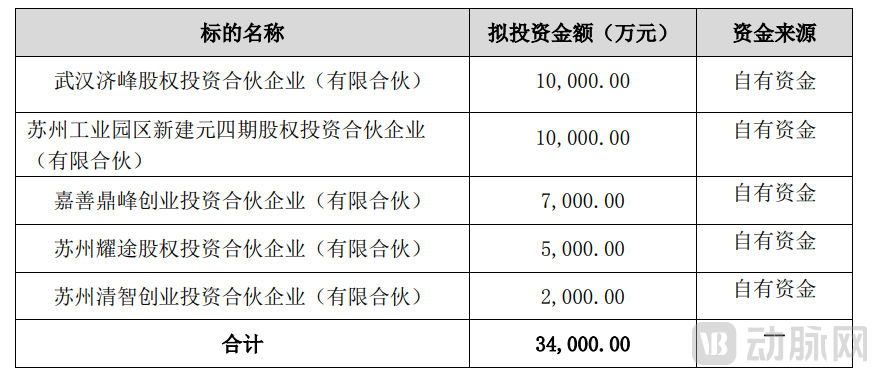

In addition, Sino Biological announced its plan to contribute RMB 200 million to jointly establish a private equity fund—Wuxi Qingsong Medical Health Industry Investment Partnership; Sansure Biotech intends to contribute RMB 200 million to jointly establish the Hunan Xiangjiang Sansure Biotech Industry Fund Partnership (Limited Partnership) with other partners, including Shengwei Rongquan; EasyDiagnosis signed the "Investment Cooperation Agreement" with Wuhan Mingxiang and Legend Capital to participate in the establishment of Mingxi Investment...

To date, numerous prominent healthcare-focused investment firms, including Legend Capital, Jefferies Capital, Yuansheng Venture Capital, and Fortune Capital, have secured stakes in relevant IVD companies. The funds involving these IVD enterprises primarily target the broader medical and health sector, with a portion of capital specifically earmarked for investments in the in vitro diagnostics (IVD) industry to support affiliated companies in acquiring new technologies and projects through investment and M&A activities.

Overall, while some IVD companies allocate funds to recruit R&D personnel, increase R&D investment, build R&D and production centers, invest in or acquire industry projects, and engage in venture capital investments, a significant portion of their capital remains deposited in banks. However, capital generates greater value and drives economic prosperity only when it is in circulation. Effective spending is key to creating greater value.

Although many IVD companies in China have generated substantial wealth over the past three years and spent heavily in the last two years to enhance their market competitiveness,However, China's IVD industry still faces numerous pain points and challenges.

From the perspective of market landscape, overseas giants such as Roche, Siemens, Danaher, and Abbott occupy the majority of the market share in China's in vitro diagnostics (IVD) industry, while domestic brands have a relatively low and fragmented market share.

In the in vitro diagnostics (IVD) reagent sector, upstream raw materials are also dominated by overseas enterprises, leaving domestic companies constrained and finding it difficult to achieve breakthroughs. Consequently, most Chinese IVD enterprises are confined to competing in the low-to-mid-end market, with competition primarily driven by price wars.

Meanwhile, there remains a certain gap between the domestic business and payment environments in China and those overseas. For instance, innovative products in the Chinese market have not received returns commensurate with their R&D investments, as specifically reflected in the reimbursement prices for new products after their launch.

In addition, constrained by limitations in capital, personnel, and distribution channels, Chinese IVD companies have predominantly adopted a distributor-led sales model. While this approach facilitated rapid expansion and market capture, the service capabilities of distributors vary significantly. As product homogenization intensifies and channel competition becomes fiercer, marketing competition in the IVD industry is gradually shifting toward service-based competition, posing substantial challenges to the established sales models of domestic enterprises.

From a problem-solving perspective alone, domestic IVD enterprises still have much to accomplish, such as accelerating the substitution of imported products with domestically produced ones, pursuing integration and M&A, having manufacturing companies secure upstream raw materials, innovating and developing market-leading products, and enhancing channel and service capabilities. However, initiatives such as consolidating with peers, acquiring upstream and downstream companies, strengthening R&D, and improving channel networks all require substantial financial support.

In addition to addressing the aforementioned gaps, domestic IVD companies must keep pace with the times by strategically deploying next-generation technologies and products to fully prepare for future industry competition.。

Dr. Wang Yaqi, Chairman of RainSure SCIENTIFIC, stated, “The IVD industry currently suffers from a lack of innovation and severe homogenization, necessitating greater R&D investment by more companies to develop new products.”

From a segmented market perspective, molecular diagnostics and point-of-care testing (POCT) will be the focal points of development for the in vitro diagnostics industry, as well as the primary arenas for future market competition.

Molecular diagnostics is the fastest-growing segment of the in vitro diagnostics (IVD) market, enabling early disease diagnosis, prevention, and tailored treatment plans. In the future, it will be widely applied in scenarios such as infectious disease screening, prenatal diagnosis, tumor genetic testing, and personalized medication. Currently, the gap between China’s molecular diagnostic technologies and those of overseas companies is relatively small, presenting significant opportunities for domestic firms to compete head-on with global giants in the future.

POCT offers numerous advantages, including convenience, high efficiency, high accuracy, low cost, and wide applicability, making it suitable for point-of-care, rapid testing, emergency response, and home self-testing scenarios.

Industry insiders state: Currently, seven categories of disruptive innovative technologies are emerging in the IVD industry, primarily including third-generation sequencing technology, single-molecule immunoassay, digital PCR, flow cytometry-based liquid bead arrays, microfluidics technology, photo-excited chemiluminescence technology, and mass spectrometry detection technology.

For IVD companies with substantial cash reserves, it is advisable to consider acquiring innovative firms that possess new technologies and products in fields such as molecular diagnostics and POCT, particularly overseas innovative technologies and product lines, followed by rapid integration and promotion.

Currently, a large number of IVD companies in China are expanding horizontally through investments and mergers and acquisitions to provide integrated services covering diagnostic reagents, diagnostic instruments, and diagnostic services; vertically, they are establishing full industry chain layouts spanning from core raw materials and diagnostic reagents to instruments and equipment as well as supporting consumables.

Notably, domestic IVD companies have primarily invested in and acquired innovative enterprises within China, with relatively few cases of acquiring overseas innovative technologies and products. Given the current market landscape and industry development trends, some industry experts suggest that domestic IVD companies consider mergers and acquisitions to introduce new technologies and products from abroad.

Having secured a commanding lead in technology and products, relevant IVD companies can aggressively increase investment in brand promotion, expand channel development, and capture a certain share of the global market. It is important to note that brand promotion and channel development hold value only when underpinned by high-quality products; otherwise, they are merely illusory.

Furthermore, drawing on the development trajectories of IVD giants, domestic companies still need time to build their brands and increase their global market share. However, there are multiple pathways to growth. For instance, Illumina has captured 80% of the global market by leveraging its absolutely leading sequencing instruments, while companies such as Roche Diagnostics, Danaher, and Abbott have become industry giants by relying on their extensive high-quality product portfolios, strong brands, and robust distribution channels.

Even after acquiring technology and investing heavily in building brands and distribution channels, relevant companies cannot rest on their laurels; they must also focus on comprehensive competitive advantages, including corporate development strategy, management capabilities, product selection expertise, and market tactics. These elements are indispensable for becoming an industry giant.

From domestic brands to global enterprises, from lagging behind to catching up and surpassing, from the low-to-mid end to the high end, and from the mid-to-downstream segments to the upstream, Chinese IVD companies still have many barriers to break through, numerous technologies to master, and various markets to penetrate. It is believed that with substantial capital infusion, these IVD enterprises will accelerate their development and achieve their strategic goals at the earliest possible time.