Over RMB 24 Billion Raised in Healthcare Venture Funds in 2023: Is It Easier for Startups to Secure Funding?

Qiming Venture Partners

Healthcare Investment Institutions

Recently, Qiming Venture Partners and Fortune Capital announced the completion of fund raisings amounting to billions of yuan, drawing significant attention from the venture capital community. Healthcare is one of the key sectors in which both firms have made strategic investments.

Looking back over the past year, investment firms have generally observed a decline in both the number of healthcare venture capital deals and the total investment amount in 2022, along with a significant slowdown in decision-making speed. This trend reflects, on one hand, a return to rationality following the investment boom of 2020–2021, and on the other hand, is attributable to reduced offline interactions and an unfavorable fundraising environment.

In 2023, government guidance funds have been highly active, with some industrial capital also stepping in. Offline interactions between GPs and LPs have become increasingly frequent, suggesting that the fundraising environment is warming up. With nearly half of the year already passed, has the fundraising landscape truly changed? Will there be more ample capital available for healthcare innovation venture investment? VCBeat has conducted multi-faceted observations on this matter.

VCBeat’s analysis of public data from the Asset Management Association of China and Qichacha reveals that from January to May 2023, a total of 58 new funds named with terms such as “medical care,” “biopharmaceuticals,” and “big health” completed filing, with a total scale of approximately RMB 24.3 billion. Both the number and size of these funds were slightly higher than those in the same periods of 2022 and 2021.

Top-tier institutions have made significant contributions to new fund fundraising.

In February 2023, the Ziyang Qiyang Industrial Development Fund, under CICC Capital, completed its fundraising with a total size of RMB 1.01 billion. Leveraging Ziyang’s local resource endowments in the specialized medical device industry, the fund will invest in projects along the medical device industrial chain, aligned with the development direction of Ziyang’s “China Dental Valley” industrial plan. In the future, it will further expand its investments in high-quality projects related to Ziyang’s industrial development, particularly in the fields of high-end manufacturing and consumer technology.

In early 2023, GTJA Capital also completed the fundraising for an industrial fund with a scale of RMB 500 million. This year, it plans to raise an angel fund, a VC fund, and a PE fund, targeting different stages to make strategic investments and precise layouts in the healthcare sector.

New players continue to enter the healthcare sector.

In May 2023, the first healthcare industry fund under HHF Fuyuan Investment completed its first closing, raising over RMB 700 million in initial commitments against a target size of RMB 1 billion. The fund focuses on vertical sectors such as medical devices, the upstream segment of biopharmaceuticals, and consumer healthcare. Against the backdrop of national strategies promoting import substitution and self-reliance in critical links of the industrial chain, it targets structural investment opportunities related to import substitution, clinically and commercially valuable innovations, and cost reduction and efficiency enhancement.

Established in late 2020, Qiji Investment completed the fundraising for its inaugural RMB fund in March 2023, with a total committed capital of nearly RMB 1 billion. The fund will primarily focus on investments in frontier technology-driven biopharmaceuticals, medical devices, and in vitro diagnostics.

New Healthcare Industry Fund Sees Fresh Developments Across Preparation, Fundraising, and Filing Stages

In addition to the RMB 24.3 billion healthcare venture capital fund mentioned earlier, other funds also have investment scopes covering biopharmaceuticals and the broader health sector; therefore, the total scale of relevant funds is theoretically far greater than this figure.

For instance, at the end of 2022, Oriental Jiafu completed the fundraising for its Technology Venture Capital Fund (Phase IV), achieving a first close of RMB 700 million against a target size of RMB 1 billion. The fund primarily invests in intelligent manufacturing and new materials, next-generation information technology, and innovative healthcare. In April 2023, Tsinghua Yinxiang completed the first close of its new Beijing-based fund at RMB 400 million, with investments mainly directed toward information technology, biomedicine, advanced manufacturing, and technology services.

Recent “official announcements” regarding two large-scale funds have drawn significant attention within the industry. On May 18, Qiming Venture Partners announced the completion of its RMB 6.5 billion seventh fundraise, continuing to invest in high-quality early- and growth-stage projects in the technology and consumer sectors, as well as healthcare. On June 3, Fortune Capital (Dachen Caizhi) announced the first closing of its latest comprehensive fund, the Chuangcheng Fund. With a total size of RMB 8 billion and a first-close amount exceeding RMB 5 billion, the fund will increase sustained investment in China’s hard-tech innovation and entrepreneurship.

Among the new funds, government guidance funds and industrial capital remain the primary limited partners (LPs). Are these LPs themselves undergoing changes?

Government guidance funds have become key investors in innovative venture capital, making them virtually indispensable entities for general partners (GPs) during fundraising.

According to Zero2IPO Research, by the end of 2022, China had established a total of 2,107 government guidance funds, with a target scale of approximately RMB 12.84 trillion and a committed capital of approximately RMB 6.51 trillion. Among these, the newly established government guidance funds in 2022 were predominantly industry-oriented, primarily focusing on strategic emerging sectors such as high-end manufacturing, new materials, information technology, and biopharmaceuticals.

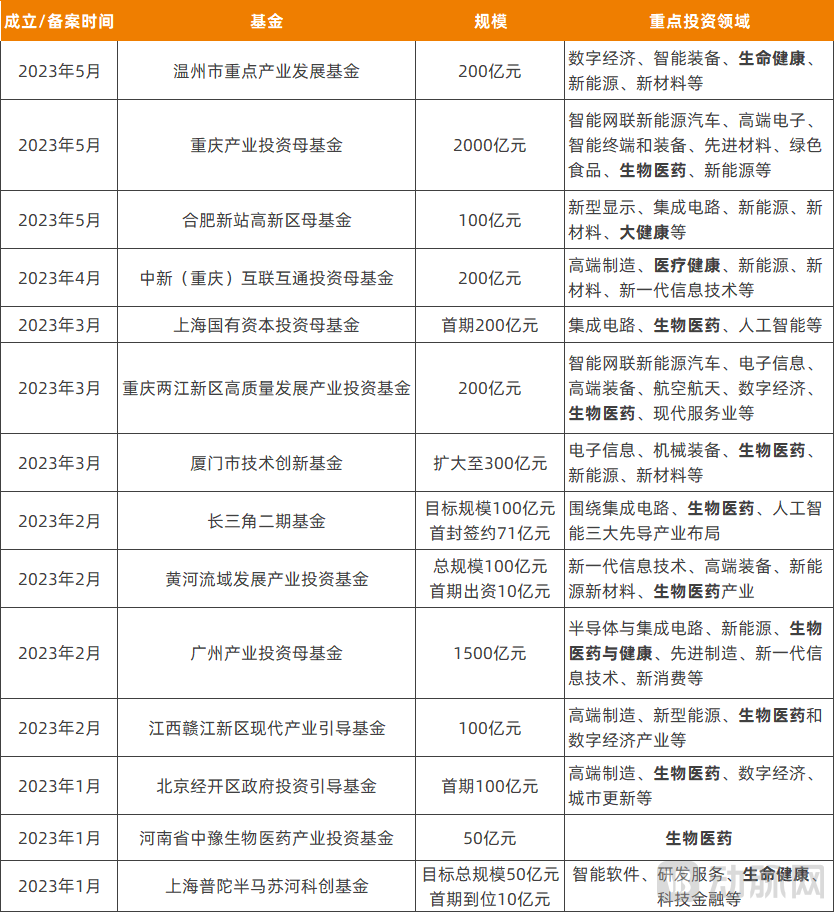

Since 2023, government-guided funds have remained active in the venture capital sector, with trillion-yuan-level fund-of-funds and fund-of-funds clusters emerging frequently across various regions.

Selected Government-Guided Funds Established Since 2023. Source: Public reports; chart compiled by VCBeat.

In February 2023, the Guangzhou Industrial Investment Fund of Funds, with a scale of RMB 150 billion, was established, focusing on investments in semiconductors and integrated circuits, new energy, biopharmaceuticals and health, advanced manufacturing, next-generation information technology, and new consumption.

In May 2023, Chongqing established an industrial investment fund of funds with a total scale of RMB 200 billion, operating under a “sub-fund + direct investment” model. The sub-funds are categorized into industry-specific funds, regional funds, and special-purpose funds. In principle, investments by the special-purpose funds and through direct investments are directed toward industrial projects located in or attracted to Chongqing, with biopharmaceuticals being one of the key investment sectors.

The concept of a “multi-hundred-billion-yuan fund-of-funds cluster” has been frequently mentioned. On May 18, the signing ceremony for Zhejiang Province’s “415X” Advanced Manufacturing Special Fund Cluster was held, officially launching the “4+1” special fund cluster with a target total size exceeding RMB 200 billion.

On May 31, Hangzhou, Zhejiang Province, announced the launch of three major RMB 100-billion funds. Building on existing foundations, the city has upgraded and established three hundred-billion-yuan fund-of-funds: the Hangzhou Sci-Tech Innovation Fund, the Hangzhou Innovation Fund, and the Hangzhou M&A Fund, thereby fostering the formation of a “3+N” Hangzhou Fund Cluster with a total scale exceeding RMB 300 billion.

In addition, multiple city- and district-level fund-of-funds with scales of RMB 10 billion have emerged across various regions. Nationwide, government guidance funds in central and western provinces such as Anhui, Chongqing, and Jiangxi are particularly active; in the first five months of 2023 alone, Chongqing officially announced the establishment of three fund-of-funds.

The vitality of government-guided funds has provided more abundant impetus for industry innovation and venture capital. However, at the same time,Driven by the focus on investment promotion, government guidance funds have raised their application thresholds and implemented more detailed terms.

Typically, government guidance funds impose basic requirements on general partners (GPs) regarding their management teams, investment capabilities, fundraising abilities, and risk control. Framed by legal and regulatory standards and evaluated based on the GP’s industry reputation, these requirements are mostly qualitative in nature; however, an increasing number of quantitative criteria are emerging.

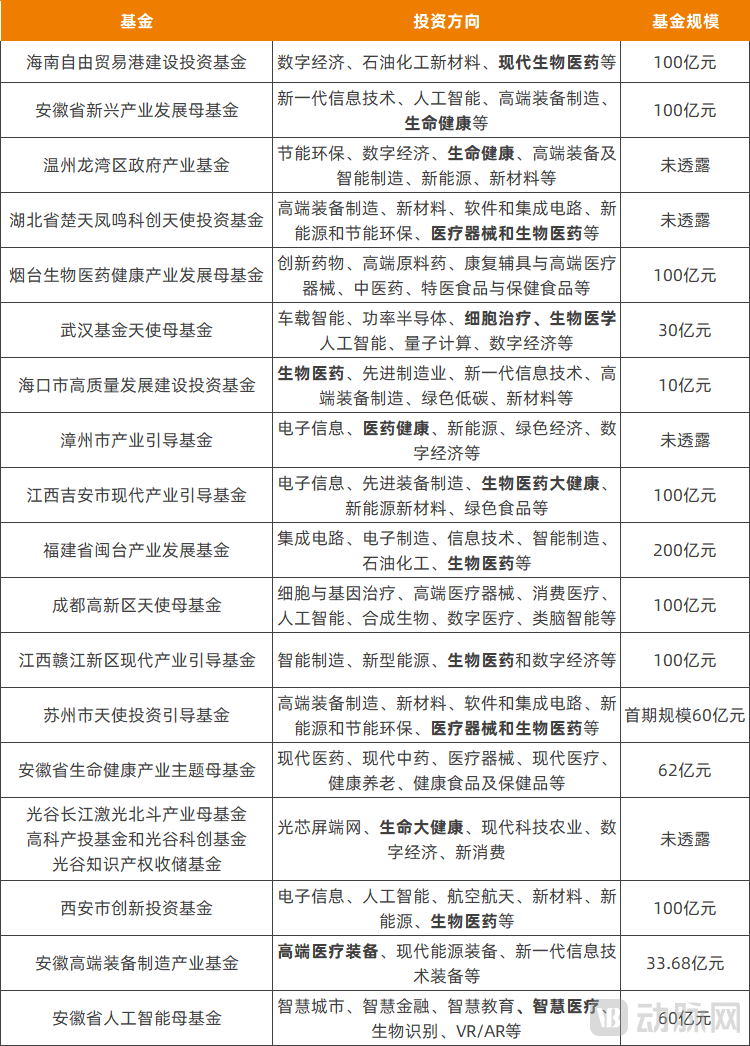

Guidance Funds Recruiting GPs in 2023, Source: Official Websites of Local Guidance Fund Management Agencies, Compiled and Charted by VCBeat

First,Guidance funds place greater emphasis on the GP’s ability to source projects, requiring a certain pipeline of reserved projects at the time of fund application.

For example, to enhance the operational efficiency of sub-funds, the Zhangzhou Industrial Guidance Fund requires that sub-fund management agencies provide, at the time of application, a pipeline of reserve projects with a total value no less than 50% of the sub-fund’s initial paid-in capital. These reserve projects must align with the sub-fund’s investment strategy and focus areas, and the proposed investment amount for reserve projects within Zhangzhou’s jurisdiction must exceed the initial paid-in capital contribution of the Guidance Fund.

The project list is always subject to uncertainty,More substantial progress in investment promotion serves as an entry or priority criterion for GP recruitment, such as having reached a landing intention with the local government or signed a cooperation agreement.

The GP recruitment requirements for the Jiangxi Ganjiang New Area Modern Industry Guidance Fund include: reserved projects must align with the industrial direction of Ganjiang New Area, demonstrate feasibility for implementation, have signed entry agreements or strategic cooperation agreements with Ganjiang New Area, and exert significant influence and a leading role on the new area’s key industries.

The Ji’an Modern Industry Guidance Fund imposes more detailed requirements on the progress of reserve projects. In addition to aligning with the investment strategies and sectors of subsidiary funds, proposed investment projects must demonstrate substantive progress, such as completion of preliminary due diligence, a strong intention to establish operations in Ji’an, or execution of letters of intent for investment. Subsidiary funds applying for participation must have at least one reserve project that has signed a letter of intent with the local government where the project will be located. Priority consideration will be given to cases involving the introduction and establishment of major projects.

“Over the years, government guidance funds have relaxed certain requirements for general partners (GPs). For instance, the overall local reinvestment ratio has been lowered, which has to some extent reduced the difficulty in the investment phase; furthermore, registration is not necessarily required to be local,” said Zhong Yu (a pseudonym at the interviewee’s request), Managing Director of a Beijing-based investment firm. However, he noted that the requirements during the application process have become stricter. “For example, some regions require that when applying to establish a sub-fund,”GP"Enterprises have already been introduced to establish local operations, which effectively requires the reinvestment obligation to be fulfilled upfront."

Meanwhile,Guidance funds have higher expectations for GPs' fundraising capabilities.

Among the general partners (GPs) prioritized by the Anhui Provincial Emerging Industry Development Fund, strong fundraising capability is a key criterion, quantified by the requirement that “at least 70% of the total proposed size of the sub-fund has been secured” at the time of application.

The Haikou High-Quality Development Construction Investment Fund also requires that, when submitting the application proposal for a sub-fund, the General Partner (GP) must have already raised at least 40% of the total target size of the proposed sub-fund, and provide materials such as capital commitment letters and proof of funding capacity from the sub-fund’s non-governmental investors.

Furthermore,Guidance funds also value the background of their cooperating LPs.

When soliciting General Partners (GPs) for the Anhui Provincial Life and Health Industry Thematic Fund of Funds, several priority criteria were established. These include: sub-funds in which listed life and health companies, industry leaders, or their affiliates participate with a capital contribution of no less than 10%; sub-funds with rapid fundraising progress, wherein 60% or more of the fund shares have secured committed investors excluding the Fund of Funds; and fund management institutions that have reserved multiple life and health projects capable of being introduced to Anhui Province, with at least one project having undergone in-depth discussions with the target municipal government for potential landing.

Listed companies are high-quality partners favored by government guidance funds. As limited partners (LPs), they possess not only the capacity to contribute capital but also the potential for cross-regional investments through expansion and acquisitions, making them still prospective targets for investment promotion.

“Overall, government guidance funds care about the local existing stock, but they care even more about introducing incremental growth,” said Zhong Yu.

Zhong Yu also noted that government guidance funds are placing increasing emphasis on early-stage investment and are establishing more funds dedicated to the commercialization of scientific and technological achievements. This shift is primarily driven by the following factors: Under policy guidance, venture capital in technological innovation has become an inevitable trend; meanwhile, having accumulated substantial experience over years of investment, guidance funds now possess the confidence to look further upstream into earlier stages; furthermore, there is a growing recognition that mid-to-late stage projects are not necessarily “safe,” whereas early-stage projects, with their more reasonable valuations, may in fact offer greater stability.

In any case, GPs need to operate on a market-oriented basis, while government guidance funds have demands for investment promotion and attracting businesses; the two parties still need to undergo a period of adjustment to seek a better balance.

Industrial capital, represented by listed companies, is also a major source of funding for venture capital funds, and the healthcare sector is no exception. Most funds invested in by healthcare-listed companies are strategically focused on areas such as biopharmaceuticals, innovative medical devices, and healthcare services, maintaining strong relevance with the parent companies or fostering ecosystem synergies.

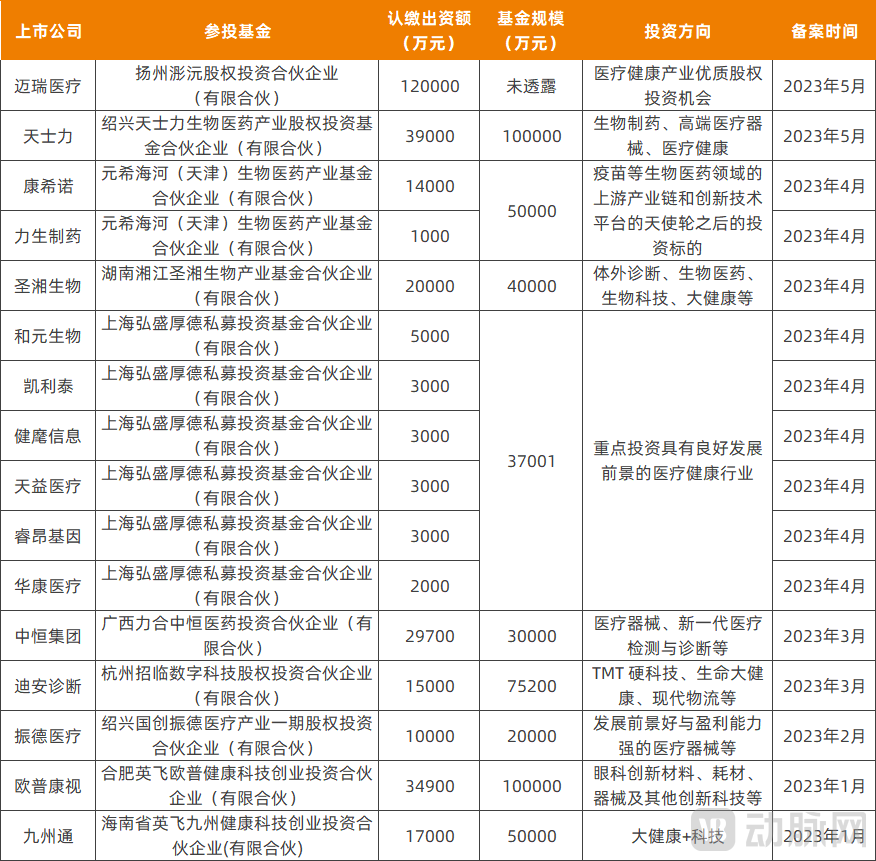

According to incomplete statistics compiled by VCBeat from public sources, more than 20 listed companies served as limited partners (LPs) in establishing funds with a primary investment focus on healthcare and medical services between January and May 2023.

January–May 2023: Investment Funds (Filed) Established with Participation from Selected Listed Companies in the Healthcare Sector; Source: Company Announcements

January–May 2023: Funds Proposed for Investment by Listed Companies in the Healthcare Sector; Source: Company Announcements and Public Reports

Companies in vaccines, in vitro diagnostics, and epidemic prevention supplies have shown active investment.Sansure Biotech committed RMB 200 million to establish the Hunan Xiangjiang Sansure Biotech Industry Fund, with a total size of RMB 400 million, accounting for a 50% contribution ratio. CanSino Biologics committed RMB 140 million to the Yuanxi Haihe Tianjin Biopharmaceutical Industry Fund, which has a total size of RMB 500 million. Dian Diagnostics and Zhende Medical also invested RMB 100 million or more each.

Relatively ample cash flows have prompted these companies to accelerate their investment pace and expand their investment scope, thereby enhancing the breadth of their strategic layout and overall competitiveness.

As previously mentioned, government-guided funds look forward to cooperating with listed company LPs; similarly,Listed companies investing in funds also value the ecosystem resources of national-level guidance funds and local governments.

In the Shaoxing Tasly Biopharmaceutical Industry Fund, in which Tasly has invested, the Company plans to leverage local government resources and the fund management expertise of professional investment institutions to identify high-quality projects in the biopharmaceutical industry and uncover more opportunities for industrialization collaboration.

Dian Diagnostics participated in the Hangzhou Zhaolin Digital Technology Industry Fund, with the National Guidance Fund for Innovative Development of Service Trade and the Hangzhou Local Government Guidance Fund serving as limited partners (LPs). Leveraging the strategic resources of central state-owned enterprises and the investment ecosystem of the national fund management platform, Dian Diagnostics can deepen strategic cooperation with its partners in fields such as service trade and medical diagnostics.

“The trend of ‘investing early and investing in small ventures’ is more evident among industrial capital.”

In 2023, Fosun Pharma planned to participate in the investment of two innovative medical device funds, both focusing on early-stage intervention in innovative projects within the fields of medical devices and medical diagnostics, thereby strengthening its reserve and early layout of innovative technologies and products.

Beta Pharma also focuses on early-stage projects. The investment scope of the funds it participates in covers innovative biotechnology, healthcare services, drug R&D and manufacturing, medical devices, and medical-related consumables and equipment, thereby complementing and synergizing with the company’s industrial strengths.

Aofu Kangshi’s invested funds focus primarily on new technologies and products, including those in ophthalmology and optometry. Investing in new technologies, products, and R&D-driven enterprises has become one of the company’s channels for expanding its product portfolio and constitutes part of its R&D investment.

Meanwhile,Listed companies also hope to identify potential M&A targets and even recruit talent through investments.

Nanjing Pharmaceutical’s co-invested new fund focuses primarily on “specialized, refined, distinctive, and innovative” enterprises in the fields of new medicine and life sciences. It aims to identify a cohort of technology-driven, R&D-intensive, and product-led companies within the broader healthcare sector, expanding industrial breadth through investment and deepening industrial depth through mergers and acquisitions.

Sansure Biotech leverages its industrial fund to build a high-quality project pipeline aligned with its strategic planning, introducing and cultivating high-end industrial projects and attracting top-tier industry talent through various approaches, including investment incubation, mergers and acquisitions, and asset restructuring.

Overall, corporate investors are providing capital with increasingly diverse investment objectives. For general partners (GPs), having a robust project pipeline and extensive resources from government bodies and guidance funds enables them to better meet these demands.

Among the healthcare venture capital funds newly filed in 2023, the largest was the Shenzhen Health and Elderly Care Fund, established with capital from Dajia Life Insurance, reaching RMB 5 billion. Insurance capital, as limited partners (LPs), is also one of the main contributors to healthcare venture capital. However, due to the unique characteristics of insurance capital, this article will not elaborate further on this topic.

Overall, it is not appropriate to make absolute conclusions about whether GPs face difficulties in fundraising.

Multiple investment institutions believe that the venture capital sector is showing this trend: while financial returns are certainly important, there are fewer and fewer LPs who pursue financial returns alone.

This also means that GPs areIndustry resource integration capability,Insights into regional economic development and investment capabilities must continue to be enhanced. During this process, some participants may fall by the wayside; yet one thing is certain: the mutual support among all stakeholders in healthcare venture capital, along with their shared confidence in expecting and facilitating socioeconomic recovery, will remain unwavering.