Early-Stage Investment Dilemma: More Projects Reviewed, Fewer Deals Closed

“The fundraising environment this year is similar to last year’s; many investors review projects but are reluctant to invest,” remarked the CEO of an innovative medical device company. Although “investing early and in small-scale ventures” has become a cyclical trend in the development of the healthcare industry, some of the bubbles inflated during the frenzy of 2021 and 2022 have since burst.

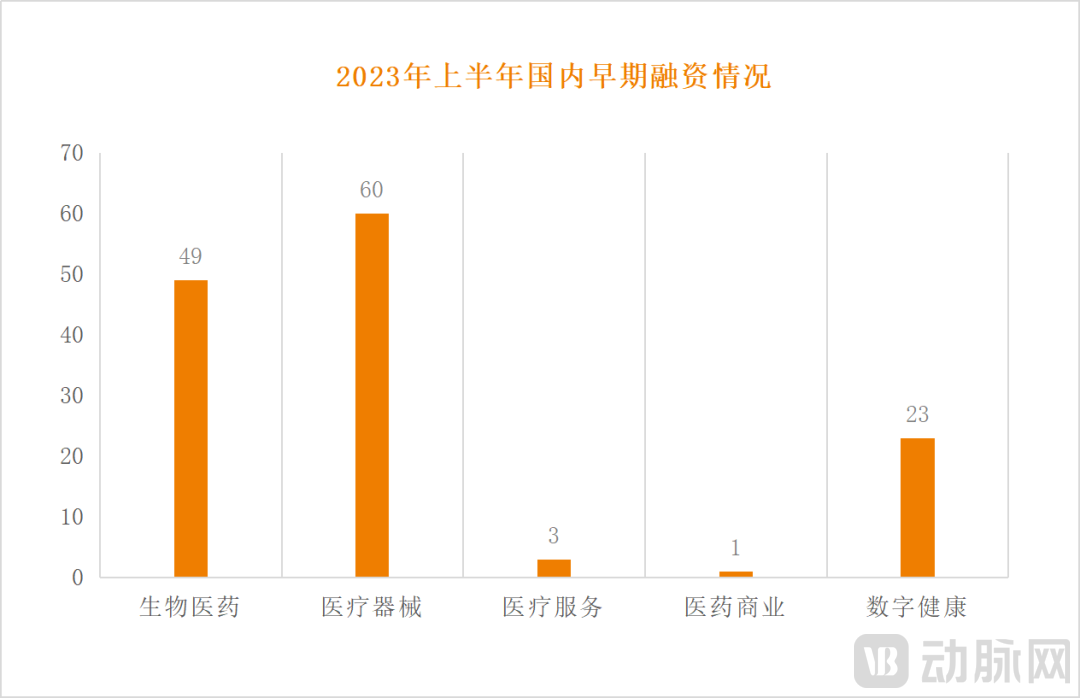

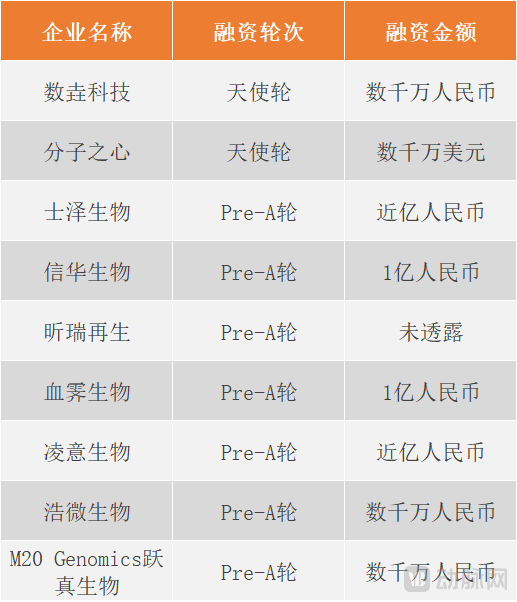

According to statistics from Chengguo Bureau, a total of in the domestic medical field were completed in the first half of 2023 (as of June 13, 2023)136 Early-Stage Financing Rounds(Seed round, angel round, Pre-A round), the number of financing events decreased by 67 compared to H1 2022.

▲ The chart shows early-stage healthcare financing in China in H1 2023 (Data source: VCBeat, compiled from public information)

The drivers behind this phenomenon are, on one hand, a process of eliminating the false and retaining the true, and on the other, a cooling of the healthcare market. Early-stage financing trends in the first half of the year indicate a rational recalibration of investment in early-stage healthcare projects, as well as a period of waiting for the next breakthrough.

Key Metrics Decline, Cooling Early-Stage Investment

An investor focused on early-stage investments told Chengguo Ju that the overall financing situation was relatively difficult in the first half of 2023. As expected, many investment institutions have chosen to "tighten their belts" at present.

On the one hand, in terms of quantity, not only has the number of financing deals decreased as mentioned earlier, but Orange Bureau has also found thatThe enthusiasm of top-tier investment firms for early-stage investing is also sharply declining.

WithHillhouse CapitalFor example, in H1 2023, Hillhouse Capital participated in two early-stage healthcare investments: the Pre-A round investment in Yirijian and the Pre-A round investment in Dishui Medical. Looking back at H1 2022, we found that, in addition to a higher number of investment deals, Hillhouse Capital’s participation in early-stage funding rounds was more diverse; it not only invested in Pre-A rounds but also focused on angel-round investments.

▲ Chart showing Hillhouse Capital’s early-stage investment activity in H1 2022 (Data source: VCBeat and public information)

This is not an isolated case,Sequoia ChinaA similar phenomenon has also emerged. In H1 2023, Sequoia China participated in four early-stage investment deals, representing a decrease of five transactions compared to H1 2022.

▲ The chart shows Sequoia China’s early-stage financing activities in H1 2023 (Source: VCBeat and public information)

▲ The chart shows Sequoia China's early-stage investment activities in H1 2022 (Data source: VCBeat, compiled from public information)

Notably, in 2018, Sequoia China established a seed fund, focusing on technology, consumer goods, healthcare, and other sectors. In 2021, Sequoia China announced that it had increased the proportion of early-stage investments to 80%, particularly ramping up its allocation to angel and seed-stage deals.

In 2022, Hillhouse officially launched the “Aseed+” Seed Program, aiming to invest in approximately 100 seed-stage companies over a three-year period.

In order to seize early-stage investment opportunities, these two leading investment firms have previously and independently increased their allocation to angel and seed rounds. However, in H1 2023,The scene we had hoped for did not materialize.They appear more inclined to focus on innovative enterprises that have met the minimum commercial requirements, continue to test the market, and refine their operational models. At the Pre-A round, they help these innovators further promote their products or services and scale up their businesses.

It is not difficult to see that, at this time,Sequoia and Hillhouse are more inclined to invest in innovative enterprises that have already achieved a certain scale and pursue steady, solid growth.

On the other hand, in terms of investment amount,Both the total amount and “unit price” showed a sharp decline.First, regarding the total financing amount: in the first half of 2023 (1H 2023), early-stage healthcare financing totaled RMB 4.454 billion, a significant drop from RMB 10.315 billion in 1H 2022, representing a year-on-year decline of 56.8%. Second, concerning “average deal size”: early-stage financing amounts in 1H 2023 remained relatively stable, with 80% concentrated in the tens of millions of yuan range. There were only 11 deals worth close to or exceeding RMB 100 million, marking a notable decrease compared to the 34 such early-stage deals recorded in 1H 2022.

So, what are the reasons for the early investment cooling down?

First, from a macro perspective, the spring of the capital market has not truly arrived in 2023. Despite the easing of pandemic restrictions and some economic growth, “the chill is still being felt by everyone,” with both primary and secondary markets currently in a relatively tight state. Therefore, investment institutions are more cautious in making investments than before.

Secondly, from an investment logic perspective, unlike the initial “frenzy” to snap up early-stage projects, many investment institutions have gradually cooled down after a period of consolidation. They have developed a new set of early-stage investment logics based on market benchmarks. The evaluation criteria used by investment institutions for early-stage projects are becoming increasingly refined and rationalized, with full consideration given to their risk profiles and return rates.

Finally, from the perspective of healthcare enterprises themselves, although the potential rewards for success are substantial, the difficulty of monetization has long been a point of criticism in the market. In the healthcare industry, many projects require significant capital investment to achieve profitability. Furthermore, technological complexity, stringent regulatory oversight, and policies such as centralized procurement and national medical insurance reimbursement may all restrict the sales and monetization capabilities of innovative healthcare companies.

Moreover, the industry is currently experiencing intense involution, with fierce competition in the healthcare sector. Companies are vying for market share against one another; established healthcare firms are capturing an increasingly larger portion of the market, while innovative startups find it difficult to gain entry.

From fervor to cooling and then returning to a state of rationality is the fundamental development pattern for the vast majority of things; the early-stage medical investment sector is no exception. After a year and a half of intense activity, investors have become more cautious in the 2023 early-stage investment market.

After Investment Returns to Rationality, It Becomes a Fiercely Competitive Battlefield for Healthcare Entrepreneurs

An analysis of projects funded in the first half of 2023 reveals that most have strengthened their core competencies. The investment landscape has evolved from initial concept-driven funding to a rigorous selection process during the capital winter. Investors now place greater emphasis on a project’s ability to address tangible problems, as well as the strength of its team and R&D capabilities. Under these heightened expectations, startups have been compelled to engage in intense internal competition.

An industry insider told Chengguo Bureau that, at present, they typically only invest after the founding team is fully in place and the data is comprehensive.

First, let’s examine the teams. Based on the backgrounds of early-stage project teams that have secured financing, it is evident that investorsIncreasingly High Requirements for Entrepreneurs' BackgroundsAmong these 136 funded companies, the founding teams are largely bolstered by industry backgrounds; most are former executives of large enterprises with at least ten years of experience and managerial expertise in the healthcare sector. Many of these founders are serial entrepreneurs, with some having prior successful exits and IPO experience.

WithZeWei BiotechTake Dr. He Wei, the founder, as an example. He previously worked in the R&D departments of pharmaceutical companies such as Novartis US, successively serving as a Research Scientist, Senior Scientist, and Principal Investigator. With over 15 years of experience in biomedical research and new drug development, he has extensive expertise in target discovery and validation, as well as preclinical development of novel oncology therapeutics.

Meanwhile, clinicians are also entering the entrepreneurial arena, with their presence being more common in specialized fields such as cardiovascular medicine and dentistry. For example,Yuewei Medical, was co-founded by three cardiac surgeons from Beijing Anzhen Hospital, Capital Medical University: Yang Yu, Wen Yuan, and Liu Hongli.

Moreover, scientists launching startups has also become a trend.Among these 136 companies, the core teams of 16 originate from research institutes.As the source of innovation, scientists increasingly favor technology-driven sectors. For instance, Professor Ding Baoquan, a researcher and doctoral supervisor at the National Center for Nanoscience and Technology, founded in May 2022Dina Yuansheng, commercializing its over-a-decade of research achievements in drug delivery at the Nano Center, and constructing targeted carriers based on self-assembled nucleic acid structures to achieve precise delivery of small nucleic acid drugs at the organ and cellular levels.

For scientist entrepreneurs, investors have higher expectations. Many investors have stated that scientific teams need to possess the “two essential elements of intense competition.”Building a “PI + CEO” Founding TeamScientists join forces with reliable, trusted, and experienced CEOs to co-found startups, forging deep ties with these ventures while continuing to explore frontier technologies.

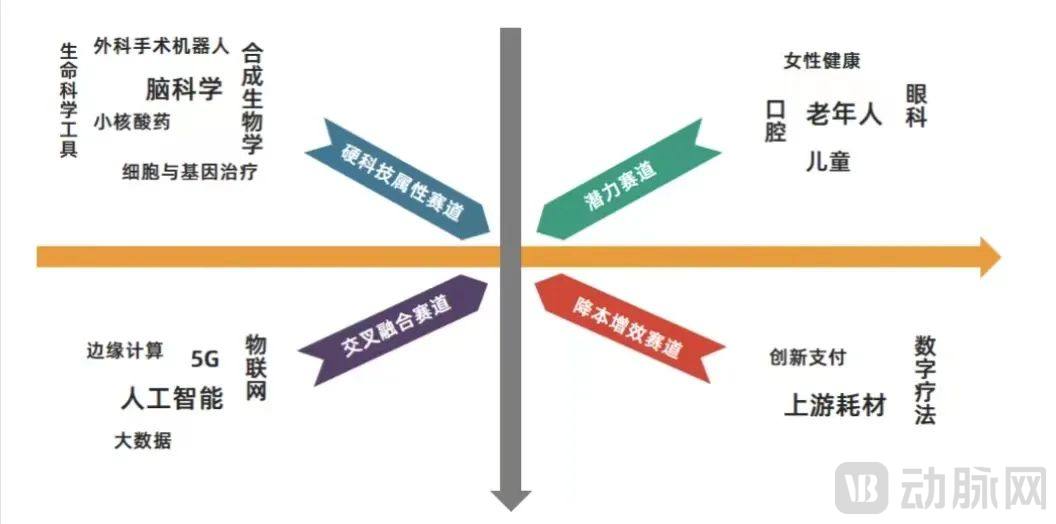

Next is the intensifying competition in technology. From the perspective of R&D, early-stage projects that have secured investment are atHard Technology Sector, High-Potential Consumer Sector, Cross-Disciplinary Integration Sector, and Cost-Reduction & Efficiency-Enhancement SectorAll of the above areas have been strategically covered.

▲ The figure shows the quadrant of early-stage investment tracks in H1 2023. Image source: VCBeat’s article “Conversations with 13 Top-Tier Investment Firms: The 2023 Healthcare Investment Logic Is Now Complete”

In early-stage investment, hard technology is undoubtedly the hottest sector at present, mainly includingCell and gene therapy, nucleic acid drugs, brain science, synthetic biology, life science tools, surgical robots, etc.. In H1 2023, these cutting-edge medical sectors continued the momentum seen in 2022. Among 136 early-stage financing deals, 80% of startups were focused on hard-tech sectors.

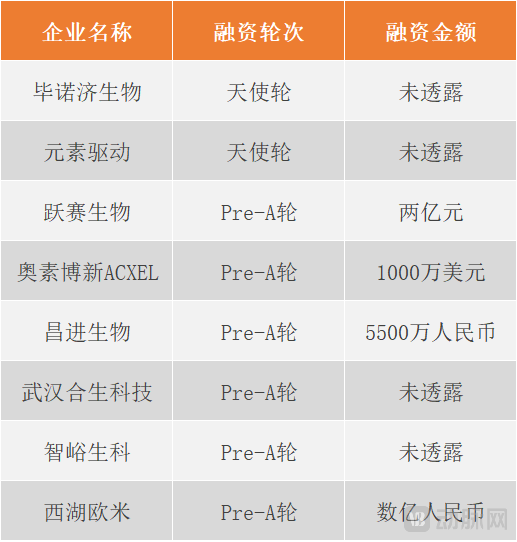

Taking synthetic biology as an example, six synthetic biology startups secured financing in the first half of 2023. According to Synbiobeta data, global funding in the synthetic biology sector reached approximately $18 billion in 2021, equivalent to the total amount raised over the previous 12 years. In recent years, as an emerging interdisciplinary field, synthetic biology has seen its potential vastly expanded, directly fueling a frenzy across investment, industry, and even academia. It was precisely during the 2020–2022 period that a cohort of synthetic biology companies, backed by capital, began their step-by-step transition from the laboratory to industrialization. Founded in 2022,InnoKecoIt is a synthetic biology company dedicated to the research, development, and production of green biological products, and it rapidly secured angel-round financing in early 2023.

Potential sectors with vast market space but still in the early stages of development are exemplified by the “silver economy,” which refers to the health needs of the elderly in medical settings. Within this category, ophthalmology and dentistry have demonstrated outstanding performance. In the first half of 2023, a total of 10 ophthalmology startups secured financing. These companies were highly concentrated, with the majority focusing on the medical device segment.

An investor focused on ophthalmic devices told Chengguo Bureau that the reason ophthalmology is so popular is becauseIt exhibits strong consumer attributes and substantial market demand, with a high incidence of age-related pathologies, yet there is a scarcity of ophthalmic drugs.Many startups have taken the lead in positioning themselves within the medical device sector to gain market entry.

The rapid development of the healthcare industry over the past decade is closely linked to the influx of internet technologies. Currently, as clinical needs undergo another round of iteration, stakeholders are seeking new breakthroughs by attempting to deeply integrate global innovative technologies with unmet medical needs. Financing data from the first half of 2023 shows that 11 AI-concept companies secured funding, primarily focusing on drug R&D, insurance payment, and care services, indicating that this cross-sector integration is deepening further.

In the field of drug development,Junji BiotechDeveloping life science laboratory automation solutions based on robotics technology to realize automated production lines for products such as gene synthesis, oligonucleotide synthesis, Sanger sequencing, and recombinant antibody preparation. Leveraging its clustered advantages, the company announced in May 2023 that it had completed an angel financing round worth tens of millions of yuan.

As a high-value sector capable of reducing costs and increasing efficiency, the upstream consumables and scientific instruments in the healthcare industry are currently enjoying policy dividends, with companies in the field continuously achieving breakthroughs and rising prominence. Particularly after weathering the downturn caused by the pandemic, China’s domestic scientific instrument industry has seen an influx of capital. In the first half of 2023, enthusiasm for financing among domestic instrument enterprises remained high, with eight Chinese scientific instrument companies completing early-stage funding rounds, each raising amounts exceeding RMB 10 million.

Among them, those that secured tens of millions of yuan in Pre-A round financingHuaYi NingChuang, to date, 18 types of instruments and equipment have been successfully developed for market applications in public safety, food and drug safety, and precision medicine, including six mass spectrometers, thereby addressing the shortage of high-end mass spectrometry instruments in China.

The Future: Neither Optimistic Nor Pessimistic

What will early-stage medical investment in China look like in the future?"The early-stage investment market in future healthcare is not overly optimistic, but there is no need for pessimism either.“An industry insider said.”

There are two reasons for the lack of optimism: First, the healthcare industry is highly susceptible to policy shifts and market fluctuations, which significantly impact the innovation and investment vitality of innovative startups. When faced with volume-based procurement (VBP), investors tend to be more cautious about future market prospects. Second, while the economy is slowing down, industry bubbles have not yet fully dissipated. The healthcare sector is awaiting the market entry of truly promising and commercially viable technologies.

There is no need for pessimism, as there are also advantages when the market responds. With innovations in medical technology and the development of new technologies such as deep learning and big data, the future healthcare sector may establish a stable and highly promising market. Both currently and in the future, China’s early-stage healthcare market will remain a high-risk, high-reward domain, where various innovative enterprises will continue to emerge and create substantial value.

For startups, in the context of a cooling healthcare market and a return to rationality in investment, it is not only necessary to actively seek financing opportunities, but also toFocus on Revenue Growth and Cost Control, on one hand saving costs and on the other achieving profitability. First, ensure the enterprise’s survival.

Therefore, for scientists and clinicians embarking on entrepreneurial ventures, it is essential not only to develop projects that are truly innovative and meet market demands but also to consciously strengthen their core competencies in corporate operations and management. Only in this way can startups gain a competitive edge in the early-stage medical investment sector, which is filled with both opportunities and challenges.

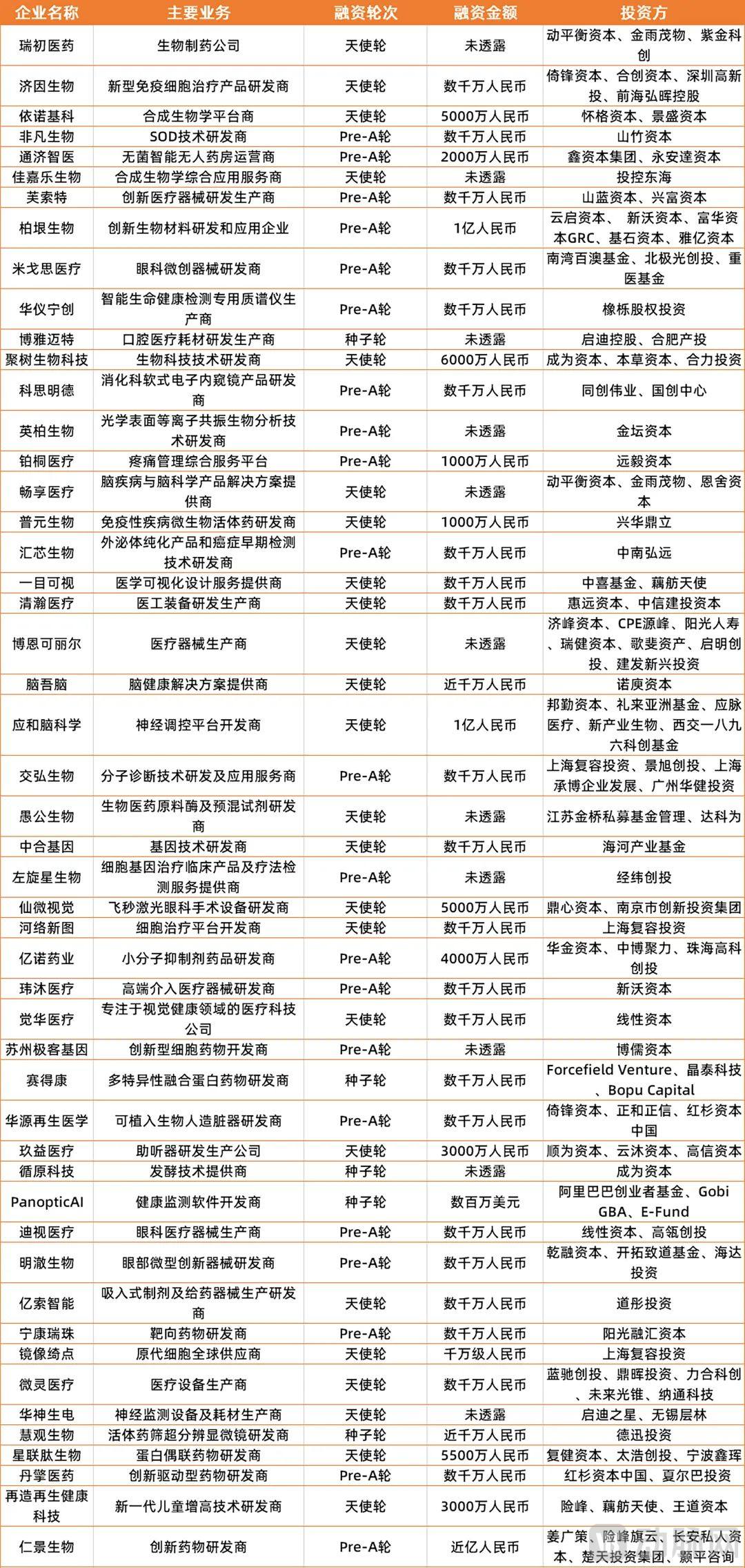

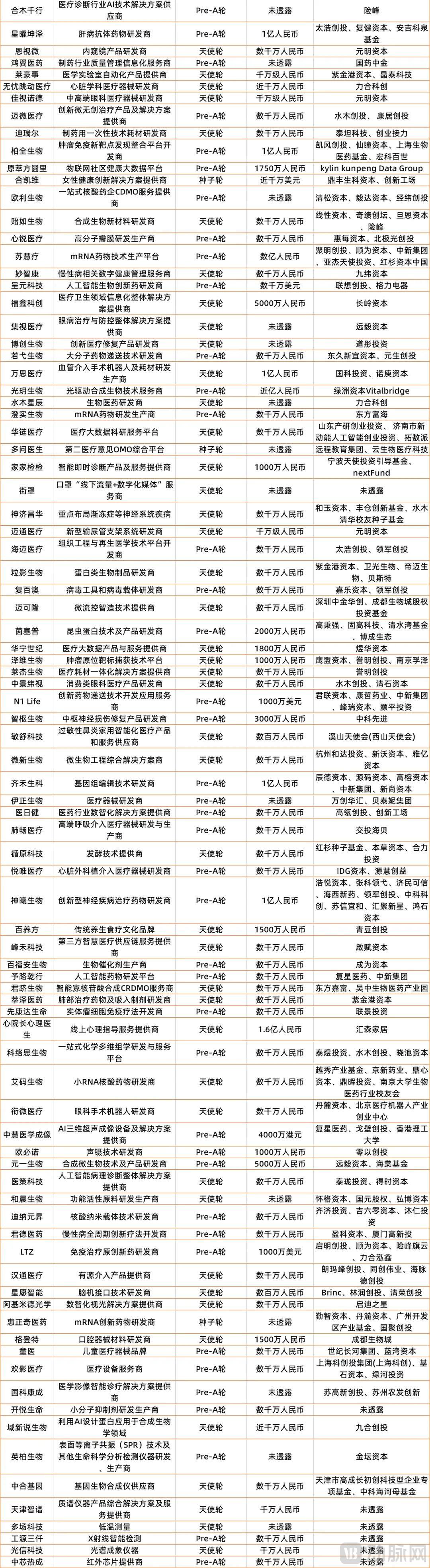

* Appendix: Early-Stage Financing in H1 2023