China's 'Weight Management Leader' Yi Health Files for Hong Kong IPO After Turning Profitable in 2022 with Over RMB 2 Billion Revenue

Looking back at the first half of the year just passed, the heat in the medical field was roughly divided into two stages: the former stage was driven byChatGPTthe resulting rethinking of “AI + healthcare” and large language models; the latter stage is driven bySemaglutide, a Quarterly Blockbuster with $4.2 Billion in Salessparked a “weight-loss fever,” and, single-handedly, it has driven a “reconciliation” between the entire capital market and consumer healthcare.

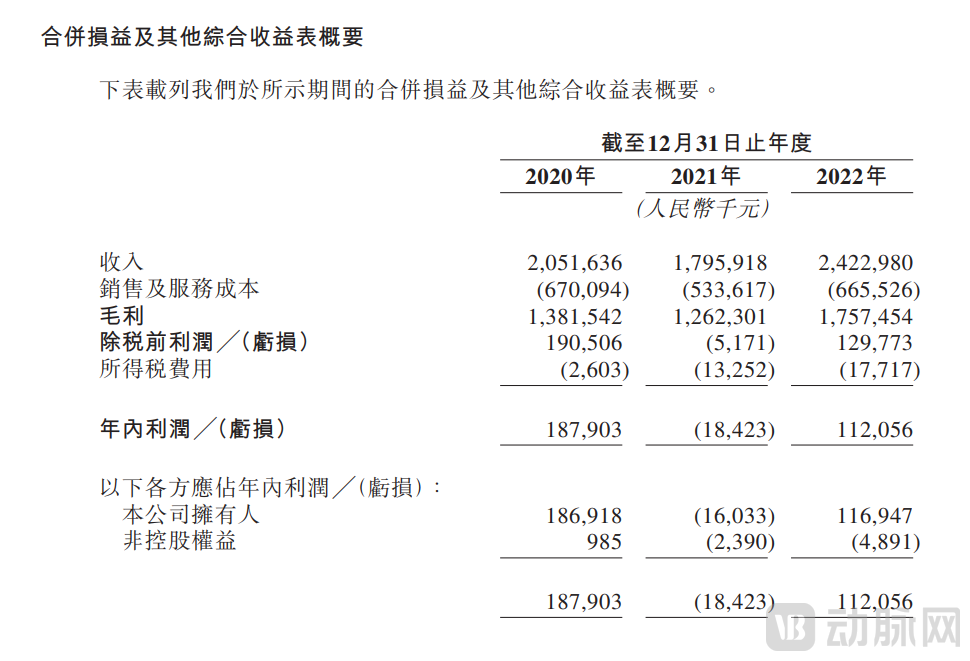

Or perhaps it was precisely to capitalize on such market enthusiasm that, in 2022, it generated nearly RMB 2 billion in revenue from “weight management” and just achieved a turnaround from loss to profit.Guangdong One Health Industry Group Co., Ltd. (hereinafter referred to as “One Health”)Recently, the prospectus was formally submitted to the Hong Kong Stock Exchange.

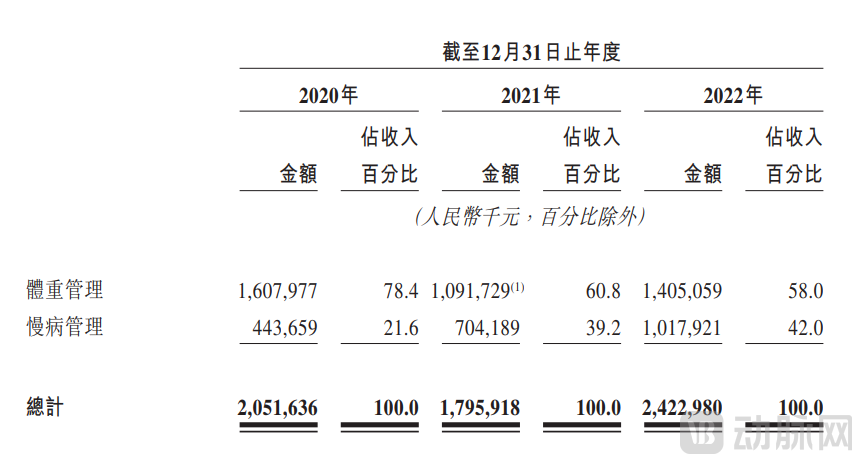

According to the prospectus, One Health was founded in 2009 and is a leading enterprise in China's digital health management sector. Its business primarily consists ofWeight ManagementandChronic Disease ManagementComposed of two major segments, weight management serves as the starting point for Yi Health’s business development and is also the company’s most lucrative segment, generating RMB 1.405 billion in revenue in 2022, accounting for nearly 60% of total income. Chronic disease management, on the other hand, was launched in 2017, primarily focusing onMen's Health、Female Qi and BloodandDiabetesThree Major Segments: In recent years, this business has experienced rapid growth, with revenue increasing from RMB 443 million in 2022 to RMB 1.018 billion in 2022.CAGR as high as 51%。

Figure 1. One Health’s Revenue Performance, 2020–2022 (Source: Prospectus)

Figure 1. One Health’s Revenue Performance, 2020–2022 (Source: Prospectus)

In addition, there are some hidden key figures in the prospectus. For example, Yi Health’s gross profits for 2021 and 2022 were RMB 1.262 billion and RMB 1.758 billion, respectively,Gross Margin Exceeds 70% for Two Consecutive Years; in terms of net profit, Yi Health incurred a loss of nearly RMB 20 million in 2021, but immediately turned profitable in 2022,Net profit of RMB 112 million。

What exactly happened in the interim? And how much leverage does Yi Health, in its rush to go public, actually hold?

“Small” Business, “Big” Impact: How Does One Health Actually Make Money?

According to the prospectus, One Health initially focused on selling traditional weight-loss products. However, as internet healthcare gained momentum, the company found its sales in the weight-loss market increasingly challenging. In 2014, One Health embarked on a digital transformation journey by establishing a Data Intelligence Center, accelerating its business transition and moving offline service scenarios online.

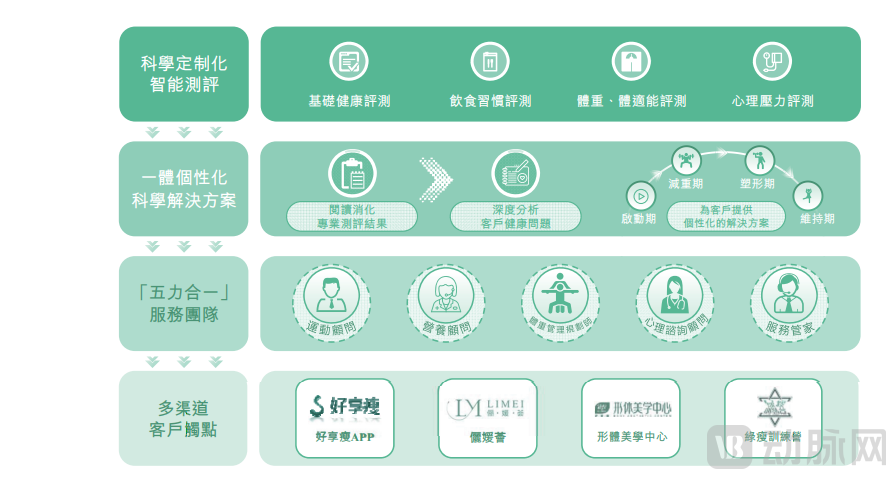

Figure 2. Yi Health's Digital Service System for Health Management

Even so, Yi Jiankang’s weight management service remains relatively simple and rather traditional, with its online component relying primarily on its self-developed“Hao Xiang Shou” APP, facilitating user traffic redirection and establishing deep connections with core customers; offline, it leverages weight-loss boot camps, body aesthetics centers, and other facilities to provide clients with diverse and highly targeted services.

Although its business model is straightforward, One Health, which has accumulated extensive experience in the weight-loss market over many years, still retains certain advantages. These include a complete industrial supply chain and a degree of market pricing power. Furthermore, it boasts a substantial sales team; as of the end of 2022,Yi Jiankang has nearly 3,000 sales personnel, accounting for nearly half of the parent company's total. Additionally, according to insiders, Yi Health has a well-established knowledge system and extensive experience in sales, resulting in a high initial conversion rate and a repurchase rate significantly above the industry average.The average repurchase rate for the weight management business in 2022 was 48.2%.。

It is precisely for this reason that Yi Jiankang’s revenue from its weight management business amounted to RMB 1.608 billion, RMB 1.092 billion, and RMB 1.405 billion in 2020, 2021, and 2022, respectively, accounting for 78.4%, 60.8%, and 58.0% of its total revenue. Furthermore, based on the 2022 revenue,Yi Jiankang Ranks First in China’s Weight Management and Digital Weight Management Industries with Market Shares of Approximately 4.2% and 7.1%, Respectively。

In addition to its “core business” of weight management, Yi Health expanded into a new area in 2017: chronic disease management. Although this is a new venture, it largely leverages Yi Health’s extensive operational experience and professional expertise from the weight management sector, resulting in a relatively straightforward business model. Online, the company primarily relies on“Yibang” AppAchieve in-depth service follow-up and real-time interaction with customers, while offline customized services are supported by physical examination centers and the internet hospital currently under construction.

Figure 3. Revenue and Proportion of Yi Health’s Two Core Business Segments (Source: Prospectus)

According to the prospectus, the chronic disease management business has experienced rapid growth in recent years, with revenue increasing from RMB 443 million in 2020 to RMB 1.018 billion in 2022, representing a compound annual growth rate (CAGR) of 51%. Additionally, its share of total revenue rose from 20% in 2020 to 42% in 2022, essentially on par with the weight management business.

Turning Losses into Profits: What Has Digitalization Truly Brought to Yi Health?

Since embarking on its digital transformation journey in 2014, Yi Health has consistently emphasized the critical importance of digitization to its operations. Zhang Baoku, General Manager of the Enterprise System Data Center, previously stated in an interview that Yi Health’s digital infrastructure development primarily focuses on three key areas, namelyServices, OfficeandManagement。

The primary focus here is on services. It is reported that Yi Health leverages AI and big data to provide users withApplied the corresponding “labels” and created precise “profiles”, thereby enabling Yi Health to more scientifically and efficiently match users with appropriate service providers through intelligent algorithms, and deliver the most suitable weight management and chronic disease management plans. Furthermore, built upon this digital foundation, service efficacy is continuously amplified, and customer experience is rapidly improving.

Extending from this point,The deepening of digitalization has actually driven the rapid expansion of Yi Health's business, while also effectively controlling customer acquisition costs.It is reported that Yi Health acquired a total of 3.9 million new customers from 2020 to 2022, while its sales and service costs decreased by 20.4%, from RMB 670 million in 2020 to RMB 530 million in 2021.

Further breaking it down, Yi Health's customer growth is primarily driven bySelf-operated ChannelsandExternal Traffic Entry PointsTwo approaches. The self-operated channel relies primarily on telemarketing. Digital intervention and empowerment not only enhance the productivity of frontline sales personnel but, more importantly, enable rapid and precise customer analysis, thereby fostering closer customer engagement and facilitating transactions. As a result, Yi Jiankang’s sales team has been gradually streamlined in recent years, leading to a significant reduction in labor costs.

External traffic sources primarily consist of public traffic pools such as Douyin, Kuaishou, Tmall, JD.com, and Xiaohongshu. However, unlike other healthcare companies, Yi Health leverages digitalization to make advertising more precise. Pi Taotao, Chairman of Yi Health, once stated that the company’s exploration of digital transformation began with the marketing department, requiring it to leverage data insights to“For every dollar invested, how much in sales revenue is generated”, even having to predict daily how much money to invest in Baidu, Tencent, or NetEase and what the conversion rate will be,“If it can’t be predicted, it means the ads are being placed haphazardly.”。

In addition to leveraging digitalization to make marketing more precise and cost-effective,Yi Jiankang also demonstrates a high degree of “market self-sufficiency,” with low reliance on external factors.。

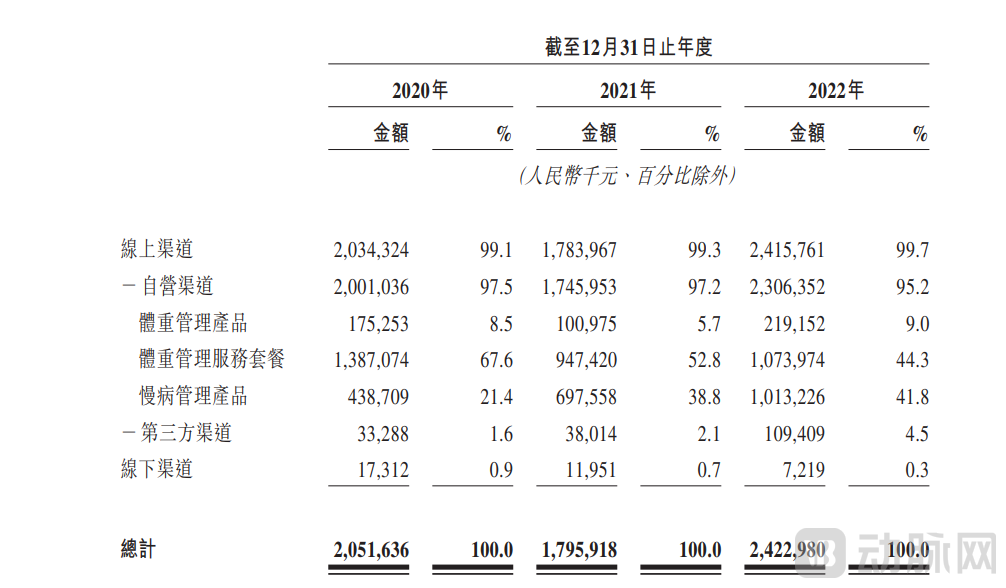

Figure 4. Revenue of One Health by Market Channel, 2020–2022 (Source: Prospectus)

According to the prospectus, Yi Health generated only RMB 100 million in transactions through third-party channels in 2022, accounting for merely 4.5% of its total. The majority of its revenue came from self-operated channels, primarily WeCom, the “Yibang” app, and the “Haoxiangshou” app, which together facilitated RMB 2.3 billion in transactions in 2022, representing 95.2% of the total. As of 2022, the “Yibang” and “Haoxiangshou” apps had accumulated a combined total of 5.4 million registered users.

In fact, customer acquisition cost has always been a common challenge for consumer healthcare companies. In past real-world cases, many listed companies have relied heavily on external marketing to drive revenue, with year-over-year increases in spending on market expansion. However, conversion rates have not risen accordingly; instead, they have declined to varying degrees. As a result, many healthcare companies remain trapped in a vicious cycle of high customer acquisition costs, leading to prolonged operational losses.

andYi Jiankang has leveraged digitalization to strengthen its “self-sustaining” capabilities in market expansion., breaking free from reliance on external traffic and gradually gaining the initiative in the market. It is precisely for this reason that Yi Jiankang has been able to ensure a certain net profit margin amidst its aggressive market expansion, avoiding futile efforts.

Opportunities Come with Hidden Risks: Will Yi Health Successfully Ring the Bell?

Every coin has two sides, and Yi Health is no exception in its IPO process.

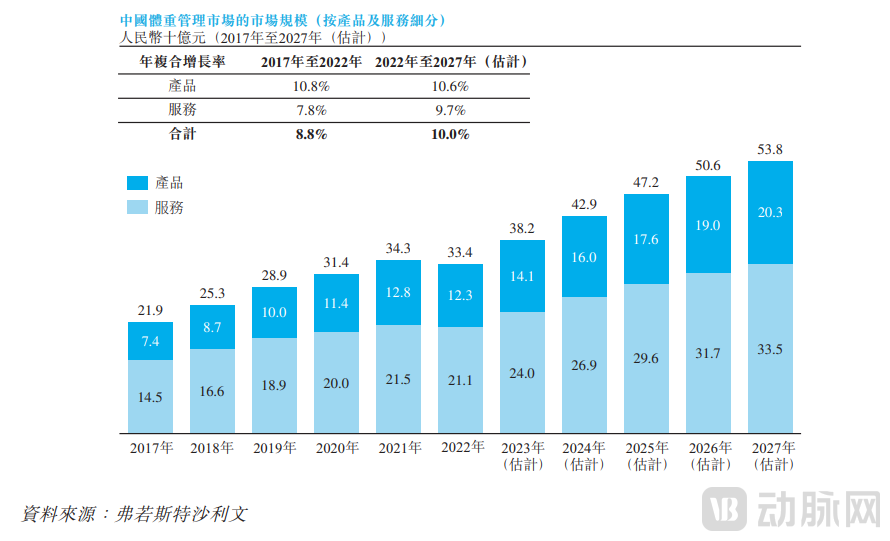

Let’s start with the positive aspects.First, the weight management and men's health management markets in which Yi Health operates are both blue oceans.. According to Frost & Sullivan, the market size of China’s physical constitution management industry reached RMB 33.4 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 10% from 2022 to 2027, expanding to RMB 53.8 billion by 2023. Meanwhile, the market size of China’s men’s health management industry is growing even faster, with a five-year CAGR of 37.3%, and is projected to reach RMB 96.0 billion by 2027, approaching the RMB 100 billion mark.

Figure 5. Market Size of China's Weight Management Industry and Proportion of Segmented Services

Secondly, beneath the blue ocean lies Yi Health’s digital-driven service offerings and market expansion capabilities.. According to the prospectus,Yi Health generated RMB 6.271 billion in revenue over the past three years, yet its total R&D investment remained below RMB 100 million., which indirectly indicates that Yi Health’s primary focus remains on concrete service upgrades and market expansion.

For One Health, breaking through in the market hinges on three key factors:1. It has demonstrated a certain level of service effectiveness., which is reflected in two data dimensions. First, the refund rate has remained below 2.5% over the past three years for both weight management and chronic disease management services. Second, the repurchase rate for these two core businesses stood at approximately 50% in 2022, significantly higher than the industry average;Second, it offers a superior user experience., which is also supported by key data: nearly 4 million new core users have been added in the past three years. Third, it has established a certain level of brand reputation, thereby reducing marketing expenses and expanding profit margins. While we will not delve into the specifics of its reputation at this moment, as previously mentioned, Yi Health has already accumulated a substantial customer base and achieved self-sufficiency, with its annual marketing costs gradually declining.

Finally, there are the ever-expanding business reach and the core customer value-added capabilities with infinite potential.. According to the prospectus, in addition to expanding its offline service bases and internet hospitals, Yi Health will alsoExpand into chronic disease management sectors such as gastroenterology and orthopedics, while strengthening psychological counseling service capabilities., gradually fulfilling its promise to become a "whole-process health management" company based on big data.

Furthermore, in its prospectus, One Health also mentioned actively exploring cooperation opportunities with mainstream companies upstream in the industry chain. Coupled with One Health’s existing large customer base, it is not unlikely that the company will expand into other value-added services beyond the medical field in the future, given that there are already many mature cases in the market.

Having Discussed the Positive Aspects, Let Us Now Examine the Challenges Yi Health May Face in the Future. In fact, the health management sector in which One Health currently operates suffers from serious homogenization due to low entry barriers. As more companies enter the weight management space in the future, competition in this sector is likely to intensify further. This means that One Health must continuously enhance its product competitiveness through innovation, a strategy that inevitably entails significant costs and exposes the company to certain market risks.

Another aspect not previously mentioned is brand effect. As a consumer healthcare enterprise, market reputation is particularly important for Yi Jiankang. However, due to a certain degree of false advertising or excessive promises by sales personnel, its market perception remains relatively negative. According to the prospectus,In 2022, Yi Health received a total of 3,011 complaints on the 12315 and Heimao platforms.。

However, at this point, virtually every consumer healthcare company faces such reputation-related challenges. This is because their products can be rapidly validated in the market, and due to individual user differences, their actual outcomes may vary significantly. In fact,A considerable number of consumer healthcare products in China adopt the “controversial yet popular” strategy.。

The final uncontrollable factor is the potential for expansion into the national and even global markets.. Judging from its current market layout, One Health remains primarily focused on Guangdong Province. Although it has expanded into Beijing, Shanghai, Wuhan, Chengdu, Xi’an, Tianjin, and Foshan in recent years, its transaction volume in these regions remains relatively small. It remains uncertain whether the company can successfully replicate its existing business model across China or even in the global market.

However, one thing is clearly visible. At the headquarters of Yi Health, there is a large digital dashboard featuring a metric that displays the cumulative number of users served by Yi Health. It is reported that by the end of 2022, Yi Health had served a cumulative total of 19 million users. By the end of May 2023, this key figure had risen to 24 million, representing an increase of 5 million users in less than six months—surpassing the total user growth achieved over the previous three years.

Consumer Healthcare Still Holds Great Promise

Entering 2023, amid intensifying competition in the healthcare industry and a cyclical downturn in the innovative drug market,Many investors are reigniting their enthusiasm for consumer healthcare.。

The underlying reason is that consumer healthcare is a sector prone to producing industry blockbusters. On one hand, it boasts a mature market, eliminating the need to wait for prolonged periods of explosive growth; on the other hand, its products can be rapidly validated in the marketplace, leading to exceptionally swift commercial realization. Recent high-profile examples include semaglutide, HPV vaccines that sold out over the past one to two years, and hyaluronic acid fillers from an earlier period.

However, this sector also faces certain limitations due to its low barriers to entry. This requires market participants to continuously enhance their product competitiveness and establish core advantages in the field; otherwise, they risk becoming merely a “flash in the pan,” quickly exiting the market once the initial hype subsides after two or three years.

Even so, many investors remain bullish on the long-term prospects of consumer healthcare. On one hand, the sector benefits from a massive population base, and as market education progressively deepens, the pool of paying customers continues to expand. On the other hand, underpinned by digital infrastructure, services are becoming more diversified, personalized, and transparent, leading to growing user acceptance.