MIT PhD Quietly Sells 'Viruses' to Power Tens of Thousands of Experiments Annually, Propelling Nearly $10B IPO

Legend Capital

Early-stage venture capital and growth-stage private equity investment institutions

VectorBuilder

Gene Delivery Technology Developer

In late June, VectorBuilder’s application for listing on the STAR Market was accepted. Dr. Lan Tian, the founder, had outlined an IPO plan a year ago, which is now being fulfilled as scheduled.

In 2022, when CGT CDMOs were highly sought after, VectorBuilder was in high demand. In September 2022, just months after the first CGT CDMO company went public on the STAR Market, VectorBuilder announced its Series C financing round led by top-tier funds such as Legend Capital and Yuexiu Industrial Fund, raising RMB 410 million and setting a new fundraising record for similar projects. At that time, VectorBuilder’s CDMO business line had been established only a year earlier, generating less than RMB 2 million in additional revenue.

In the C+ funding round one month ago, VectorBuilder’s valuation approached RMB 7 billion. Many people fail to grasp the rationale behind such a high valuation.

In fact, VectorBuilder has been deeply engaged in the field of gene vectors for nearly a decade, pioneering a business model for the commercialization of research-grade gene vectors from the ground up and serving nearly 20,000 top-tier life science researchers worldwide. In recent years, its strategic expansion into gene therapy CRO and gene vector CDMO services represents a bold initiative to extend its service chain toward clinical translation and clinical trials, thereby building comprehensive, full-cycle gene vector service capabilities.

But this time, whether luck will be on VectorBuilder’s side remains an open question. In 2022, VectorBuilder made a significant push into the gene vector CDMO business, only to see marginal revenue growth and a negative gross profit exceeding RMB 10 million. However, amid the intensely competitive CDMO landscape, even CDMO companies serving the high-potential cell and gene therapy (CGT) industry are struggling. VectorBuilder’s announcement of a confirmed CDMO contract worth RMB 35 million may signal brighter prospects ahead.

Even so, over the past three years, VectorBuilder has succeeded in maintaining rapid revenue growth and withstanding the pressure of investing heavily in asset-intensive new businesses during a downturn, thereby gaining some breathing room. Can VectorBuilder remain competitive in the CDMO market, where only the fittest survive? How can its strong capabilities in research-grade gene vector services bolster its clinical-grade gene therapy business? We attempt to find answers by examining VectorBuilder’s history and strategic vision.

Lan Tian likes to describe himself as an atypical scientist. Having engaged in scientific research for over two decades and shifted across several fields to satisfy his curiosity, he is inevitably out of contention for the Nobel Prize. VectorBuilder marks Lan Tian’s second entrepreneurial venture, spurred by the recognition that the value of gene vectors has become increasingly prominent under the impetus of the life sciences technology wave.

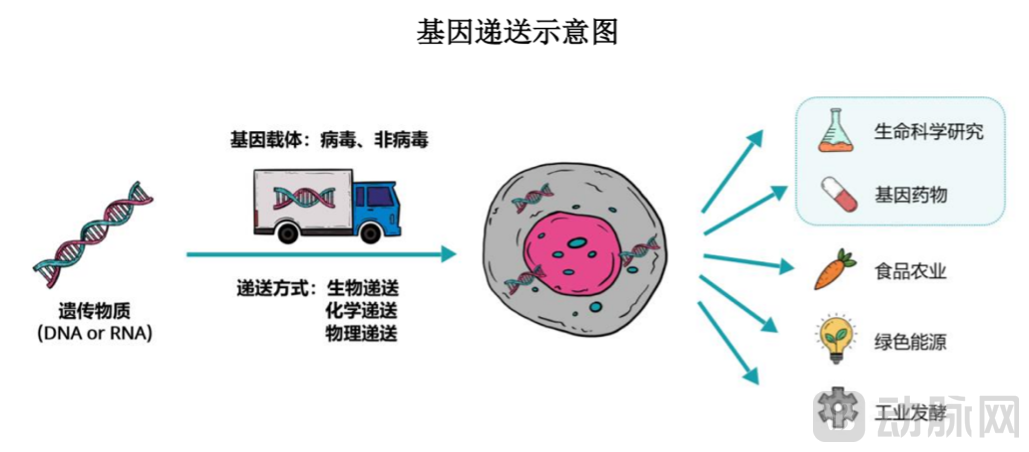

Gene delivery is a technique that uses biological, chemical, or physical methods to package exogenous genetic material (typically recombinant DNA or RNA) into gene vectors for introduction into target cells. For many researchers, this was an entirely unfamiliar technology. At the time, numerous experiments were forced to be delayed by months, or even failed.

There is a wide variety of gene delivery vectors, with different cell types and application areas corresponding to distinct gene delivery methods. Broadly speaking, gene delivery vectors are categorized into two major classes: viral vectors and non-viral vectors. Common viral vectors include lentivirus (LV), adeno-associated virus (AAV), adenovirus (AdV), and retrovirus (RV). Leveraging the inherent biological properties of natural viruses, viral vectors offer high gene delivery efficiency and are the vector type most commonly used in cell and gene therapy projects. Non-viral vectors include plasmids and lipid-based non-viral vectors, such as cationic lipids and lipid nanoparticles, which are widely applied in small nucleic acid therapeutics.

In practice, the technical barriers to gene vector construction are substantial. It is necessary to design a gene delivery system tailored to experimental objectives, taking into account factors such as target cell type and the characteristics of the gene of interest. This requires designers to possess advanced theoretical knowledge in vector construction and gene delivery. During the design process, researchers must consult extensive literature and search databases to identify and compare vector backbones, elemental sequences, and other relevant information, thereby enabling the selection of an appropriate gene delivery system.

It can be said that each step in the construction process of gene delivery vectors faces distinct technical challenges.

On one hand, in the selection and design of gene delivery vector systems, different vector systems are suitable for different cell types. Researchers must accurately grasp key performance metrics such as cargo capacity, target cell growth cycle, delivery efficiency, and immunogenicity. This process rigorously tests researchers’ accumulation of microbiological knowledge and their practical laboratory skills. For instance, adeno-associated virus (AAV) vectors offer high delivery efficiency but have limited cargo capacity for large gene fragments. Retroviral (RV) vectors also exhibit high delivery efficiency; however, a significant drawback is the difficulty in precisely controlling the timing of host cell infection. Non-viral vectors provide greater flexibility in terms of cargo capacity and compatibility with cell growth cycles, but they suffer from lower delivery efficiency in vivo.

Furthermore, enhancing the tissue-targeting specificity and safety of vector systems represents one of the technical challenges in the selection and design of gene delivery vectors. Inappropriate selection of gene vector systems may lead to gene delivery failure, resulting in off-target gene expression, which can induce cytotoxicity or trigger unnecessary immune responses.

On the other hand, in the process of target gene screening for constructing gene delivery vectors, quality control of the target gene has become a new technical challenge. During this process, if the molecular weight and purity of the obtained genes are low, such as containing small amounts of salt ions, proteins, metabolites, and other contaminants, it can affect the effective formation of vector-nucleic acid complexes during gene delivery and reduce gene delivery efficiency, ultimately undermining experimental outcomes.

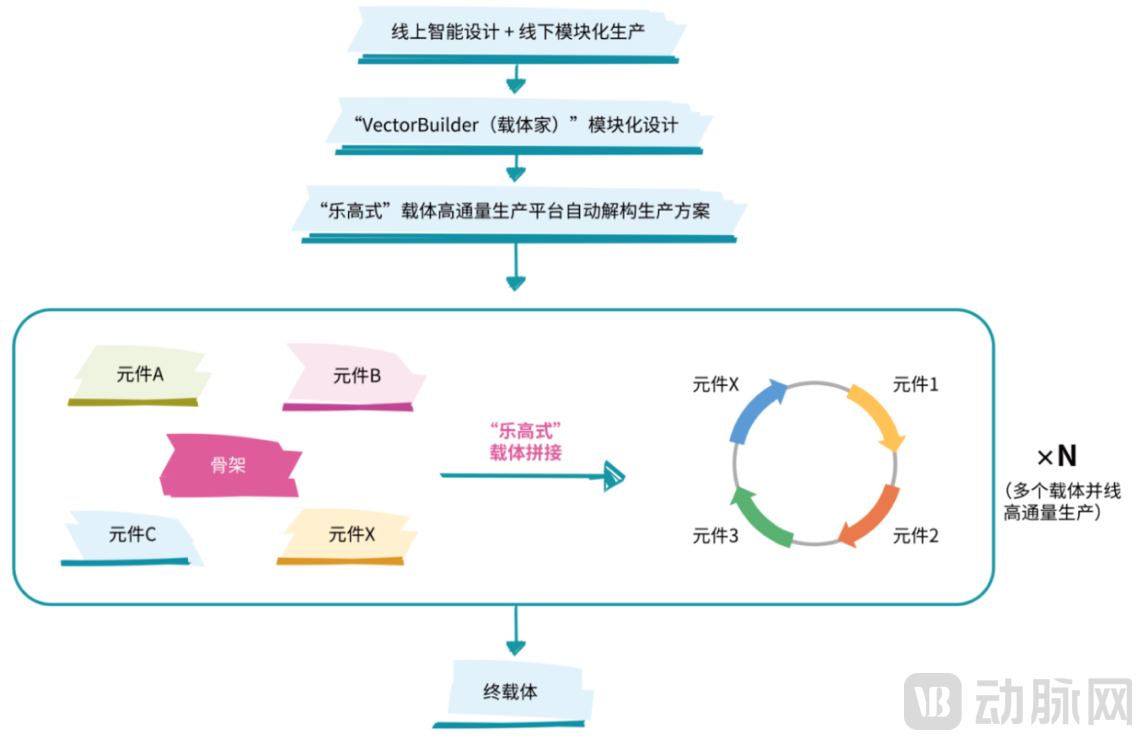

VectorBuilder hosts the complex gene vector design workflow on the cloud, enabling users to complete vector design online through a minimalist graphical interface that leverages database resources. Designed gene vectors are added to the shopping cart on the VectorBuilder website, offering an experience akin to shopping on Taobao. After completing the gene vector design, users can choose to check out directly or further purchase downstream services such as plasmid extraction, with final products typically delivered within a few business days.

VectorBuilder’s Process for Scientific Research Gene Delivery Vector Services Data Source: Prospectus

Previously, no one had considered commercializing research-grade gene vectors as an outsourced product. Today, however, this business has achieved a 5% global penetration rate, representing a new market scenario valued at hundreds of millions of U.S. dollars. According to the prospectus, VectorBuilder’s research gene delivery services primarily cater to researchers’ customized needs, offering hundreds of vector systems that span a wide range of species, including mammals, zebrafish, Drosophila, Caenorhabditis elegans, plants, fungi, and bacteria.

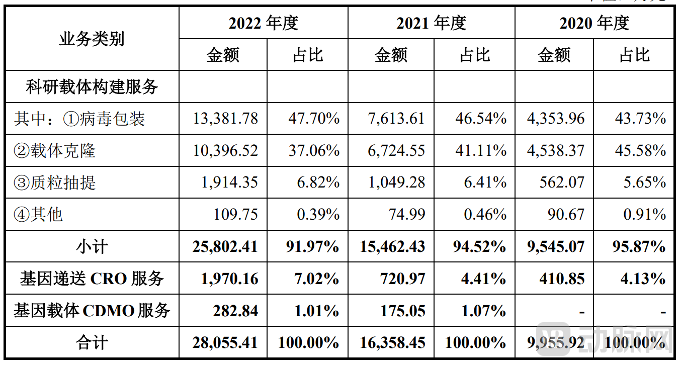

From 2020 to 2022, the research-grade gene vector business remained the primary revenue source for VectorBuilder. According to the prospectus, over the past three years, VectorBuilder’s research vector construction services generated revenues of RMB 95.4507 million, RMB 154 million, and RMB 258 million, respectively, representing a compound annual growth rate (CAGR) of 64.4% and accounting for 91.97%, 94.52%, and 95.87% of total revenue, respectively.

Composition of VectorBuilder’s Main Business Revenue from 2020 to 2022 Data Source: Prospectus

To date, VectorBuilder has cumulatively served over 4,000 research and industrial clients, with nearly 20,000 end users. The prospectus reveals that VectorBuilder’s corporate clients include multinational pharmaceutical giants such as Johnson & Johnson, Roche, Novartis, Bayer, Evotec, Takeda Pharmaceutical, and Otsuka Pharmaceutical. Its research clients hail from top-tier international life sciences institutions, including the U.S. National Institutes of Health (NIH), the French National Institute of Health and Medical Research (INSERM), The University of Texas MD Anderson Cancer Center, Harvard University, Stanford University, the University of California, Columbia University, the University of Cambridge, the University of Tokyo, and Osaka University. Notably, Johnson & Johnson and Roche have consistently ranked among VectorBuilder’s top five customers, contributing cumulative annual orders approaching RMB 10 million.

According to Lantian’s vision, as life science research advances in depth, the global demand for gene delivery vectors will continue to expand, with the current 5% conversion rate serving merely as a baseline. After all, the pursuit of an ideal gene delivery system characterized by high delivery efficiency and low cytotoxicity remains an ever-evolving endeavor.

The business of providing research-grade gene delivery vectors is exciting, yet it faces challenges in scaling up, with relatively low value per order. As a company, VectorBuilder must move up the value chain. Unsurprisingly, Lan Tian has set its sights on the clinical market.

Average Revenue from VectorBuilder’s Research Gene Delivery Vector Services, 2020–2022Source: Prospectus

In recent years, gene and cell therapies have rapidly unlocked their potential for clinical application. Data show that nearly 50 gene-based drugs have been approved for market launch worldwide. Given the highly advanced nature of product technologies and manufacturing processes, manufacturers of gene and cell therapy products often engage professional contract organizations from the outset of research and development.

According to statistics, by the end of 2020, 79.1% of the approximately 500 gene therapy companies worldwide were startups. By the end of 2021, among the eight gene therapy drugs approved by the FDA (including CAR-T therapies, stem cell therapies, oncolytic virus therapies, and gene therapies), five were manufactured using CDMO services, resulting in an outsourcing rate for commercialized products exceeding 55%.

Under normal circumstances, due to the numerous challenges associated with establishing in-house manufacturing capacity for gene and cell therapy products, R&D collaborations typically extend through to the commercialization phase, with only a small number of pharmaceutical companies internalizing production capabilities.

First, large-scale production poses significant challenges. Typically, the mass production process for gene vectors in gene therapies encounters numerous technical hurdles. For instance, in the commercial manufacturing of viral vectors, companies often face a dilemma. During cell culture and expansion, conventional cell culture processes require substantial amounts of culture media and serum, which increases the risk of cellular contamination. This necessitates striking an extremely difficult balance in the manufacturing process: reducing the consumption of culture media and serum while maintaining high yields.

Second, downstream purification is challenging. In the commercial manufacturing process of gene delivery vectors, different types of vectors require the development of distinct production technologies and processes for preparation, packaging, purification, formulation and filling, as well as quality control. Each stage necessitates various equipment and reagents/consumables, including bioreactors, centrifuges, chromatography columns, culture media, and cell lines. Consequently, the production of diverse gene delivery vectors imposes extremely high requirements on manufacturers’ processes, technologies, and equipment. Establishing clinical-grade manufacturing facilities capable of producing multiple vector types significantly increases the technical complexity of commercial production and leads to a sharp rise in associated costs.

Third, the maintenance of manufacturing systems is intricate. The delivery vectors required for gene therapies are highly personalized, necessitating that manufacturers develop specific gene delivery vectors and production protocols based on their own preclinical and clinical experimental data for particular products and pipelines. At each stage, the vector system must be optimized, and related vector production processes and capabilities adjusted, resulting in high learning costs and considerably complex routine maintenance tasks.

Since 2021, VectorBuilder has been progressively expanding its efforts into gene delivery CRO services and even gene vector CDMO services.

Specifically, VectorBuilder’s gene delivery CRO services are primarily targeted at clients translating research into clinical applications, providing tailored solutions to address gene delivery bottlenecks encountered during gene therapy development. These services include AAV capsid directed evolution, tissue distribution profiling of gene vectors, mRNA gene delivery solutions, library construction, promoter evolution and screening, stable cell line generation, BAC modification, and YAC modification.

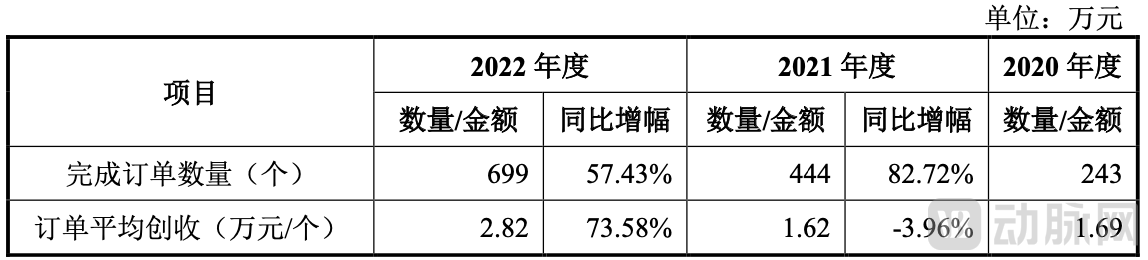

Compared with research vector construction services, gene delivery CRO services offer a higher degree of customization and greater added value. According to the prospectus, from 2020 to 2022, as the number of executed projects in gene delivery CRO services increased, VectorBuilder’s revenue from this segment grew from RMB 4.1085 million to RMB 19.7016 million, reflecting a rapid expansion in revenue scale. Furthermore, the average revenue per order for this business segment significantly improved, driven by an increased proportion of high-value projects such as AAV capsid directed evolution and library construction.

Average Revenue Generated by VectorBuilder’s Gene Delivery CRO Services from 2020 to 2022 Data Source: Prospectus

In 2022, VectorBuilder adopted an ambitious strategy, deciding to invest RMB 3.2 billion to construct a gene delivery R&D and production base with a total area of 100,000 square meters, thereby scaling up its gene vector CDMO business. This milestone was featured as the headline in the company’s annual chronicle of major events, underscoring its strong commitment to expanding into the CDMO sector.

Specifically, VectorBuilder’s gene vector CDMO services primarily target clients in the preclinical research and clinical trial stages, providing clinical-grade gene vectors. The product portfolio covers plasmids, viral vectors, and mRNA. Services include process development and analytical method development for large-scale vector production, manufacturing of clinical-grade vectors, quality control, filling, technology transfer, as well as supporting documentation and regulatory submission support.

However, VectorBuilder’s gene vector CDMO service scale remains very small, having only started generating revenue in 2021. Even in 2022, when the company vigorously promoted this segment, it secured orders worth merely RMB 2.8284 million—far insufficient to cover the nearly RMB 15 million in costs incurred during the period—making it the only business segment with a negative gross profit. VectorBuilder’s path in the CDMO market is fraught with challenges and stretches long ahead.

Despite its small scale and high barriers to entry, the CDMO business is a key driver for VectorBuilder to unlock greater commercial value, and even one of the few significant opportunities. After all, within the gene delivery vector industry chain, the market potential for research and translational services remains debatable, whereas CDMO for gene and cell therapy drugs is widely recognized as a blue ocean market.

Data shows that between 2017 and 2021, global investment in research-grade gene vectors grew from $6.46 billion to $8.56 billion. Even assuming a penetration rate of 10%, the market size for research-grade gene vector services remains below $1 billion. During the same period, the global market size for gene delivery CROs increased from $870 million to $1.57 billion; if growth continues at the current pace, it is difficult to characterize this as a particularly attractive market. In contrast, the market size for gene and cell therapy CDMOs is projected to reach $7.86 billion by 2025.

However, after a brief period of rapid growth, the CDMO sector is entering a bottleneck phase. Many frontline business personnel have openly stated that the CDMO industry in 2023 was excessively competitive; often, a single R&D project would attract fierce bidding from more than ten CDMOs, driving prices down significantly. VectorBuilder, having just entered the market, effectively faced “hard mode” from the outset. Nevertheless, given the clear growth expectations in gene and cell therapy, CDMO services remain an essential need. The current lull in orders provides an opportune time to strengthen internal capabilities.

First is core technical capability. CDMOs for gene and cell therapies differ from traditional R&D and manufacturing outsourcing companies in that their services are not limited to delivering only the final product; instead, they need to engage early in the client’s R&D process, focusing on leveraging experience and vertical technological advantages to enhance R&D efficiency. This requires CDMOs to build comprehensive technology platforms. However, the development of these technology platforms and core technologies demands not only long-term investment in R&D but also the accumulation of technical know-how and process expertise through extensive project practice.

At this juncture, VectorBuilder holds a distinct advantage. Over the past decade of providing customized gene delivery vector services, VectorBuilder has accumulated extensive expertise across various dimensions, including gene delivery vectors, plasmid construction, and cell culture, thereby establishing its primary capability as a CDMO specializing in gene delivery vectors.

Next is the capability for large-scale production and purification. This serves as the foundation for order fulfillment, yet it remains a scarcity for VectorBuilder and constitutes a process challenge that similar service providers worldwide are striving to overcome. Data shows that fewer than 10 companies globally possess cGMP commercial-scale production capabilities. Furthermore, in terms of viral vector scale-up manufacturing processes, only 20% of global CGT CDMO companies have suspension culture capacities exceeding 2,000 liters.

However, as a critical step in the manufacturing process, the large-scale production and purification of gene delivery vectors primarily test developers’ practical experience. At a time when core bioprocessing technologies are being rapidly localized in China, breaking through process bottlenecks is merely a matter of time for VectorBuilder and other CDMO providers alike, provided they remain dedicated to their work.

Finally, there is the matter of service orientation and quality. At its core, CDMO is a service industry; securing an order is merely the beginning, and cutting-edge technology platforms are just tools. Only high-quality delivery on schedule can sustain ongoing operational capability. For VectorBuilder, strengthening its services is not difficult. After all, in its traditional business, providing researchers with personalized gene delivery vectors has always been a highly customized activity. Extending this capability to other areas may simply be a matter of shifting contexts.

In June, the IPO application of another large-molecule CDMO finally passed the regulatory review after numerous twists and turns. During this period of tight capital markets, more CDMO companies successfully secured financing. The historical trend has pushed CDMO enterprises to a critical juncture where they must either go public or face decline. Nevertheless, we remain hopeful that this industry, essential to the broader biopharmaceutical sector, will give rise to great companies.