2023 Pharma R&D Annual Review: China Emerges as Global #2 Drug R&D Powerhouse with 5,402 Pipelines

CSPC

Innovative Drug Research and Development, Manufacturer

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

Fosun Pharmaceutical

Healthcare Industry Group

Recently, Citeline, a Norstella company and the global leading intelligence provider for pharmaceuticals, medical devices, biopharma companies, clinical trials, and markets, released the 31st edition of the “2023 Pharma R&D Annual Review.” Through a comprehensive assessment of dimensions such as pipeline scale, pharmaceutical companies’ R&D size and progress, therapeutic areas, and drug types, the report provides an in-depth analysis of global and Asia-Pacific pharmaceutical R&D trends and insights in 2023, while offering prospects for the future global R&D landscape.

Since its inception in 1993, this report has released a total of 31 issues (with relevant data primarily sourced from Pharmaprojects, part of the Citeline product suite). According to the latest insights, global pharmaceutical R&D has demonstrated greater robustness compared to the previous three years and is poised for sustainable growth. In China, pharmaceutical companies led by Hengrui Pharma, Fosun Pharmaceutical, and CSPC are thriving, distinguishing themselves and showcasing their strengths in the international pharmaceutical R&D market.

Ian Lloyd, Senior Director at Pharmaprojects, stated in the report: “The global pharmaceutical industry is emerging from the impact of the COVID-19 pandemic, becoming stronger and more confident. Notably, domestic pharmaceutical companies, led by Hengrui Pharma, are gradually gaining prominence in the global market, and the explosive growth in the number of Chinese pharmaceutical companies is beginning to normalize. It is foreseeable that as various stakeholders focus more on their respective areas of expertise, R&D activities in the global pharmaceutical industry will continue to increase comprehensively, and the scale of R&D pipelines is expected to achieve sustainable growth.”

Over the past three years, the turmoil in the pharmaceutical industry under the impact of the COVID-19 pandemic has gradually subsided, and global R&D has begun to enter a phase of stable growth.

Last year, Roche acquired Good Therapeutics, Novartis acquired Gyroscope Therapeutics, and Bristol Myers Squibb acquired Turning Point Therapeutics; Pfizer acquired Biohaven Pharmaceuticals, ReViral, and Arena Pharmaceuticals; AstraZeneca acquired TeneoTwo; Sanofi acquired Amunix Pharmaceuticals; Eli Lilly acquired Akouos; while Takeda, Johnson & Johnson, and Merck & Co. did not report any related acquisition transactions.

Pharmaprojects reported only 81 mergers and acquisitions in 2022, down from 116 in 2021, continuing a downward trend. Over the past year, significant declines in company valuations, waning ambitions, and the need to navigate a challenging macroeconomic environment have led to fewer large-scale expansions within the industry, with companies placing greater emphasis on strengthening their own drug pipelines.

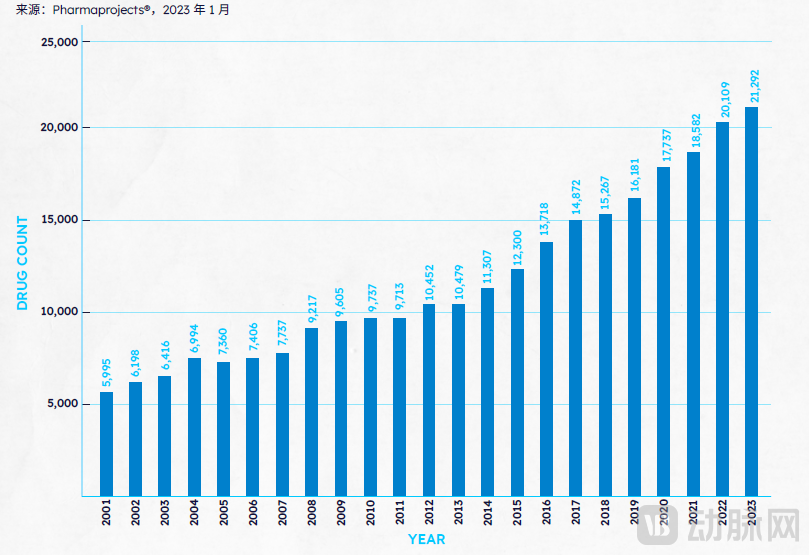

According to Pharmaprojects data from January 2023, the global drug development pipeline reached a new high in 2023, with a total of 21,292 drugs and vaccines worldwide, representing a 5.9% increase from the previous year. This means that the number of drugs under development increased by 1,183 compared to the same period last year; the increase in the prior year was 1,527, while the year before that saw an increase of 845.

Total Pipeline Scale by Year, 2001–2023

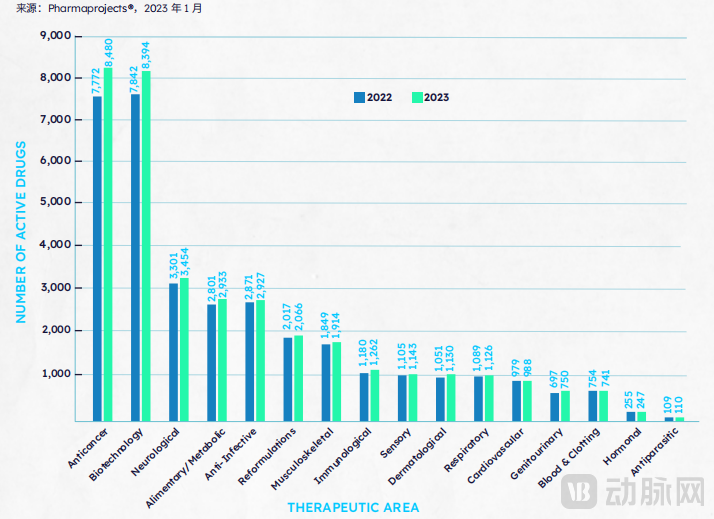

Compared with previous years, the composition of the global drug pipeline in 2023 remained largely unchanged. Oncology drugs continued to be the top priority in global drug development, surpassing biotechnological therapies, neurology, gastroenterology/metabolism, and anti-infectives.

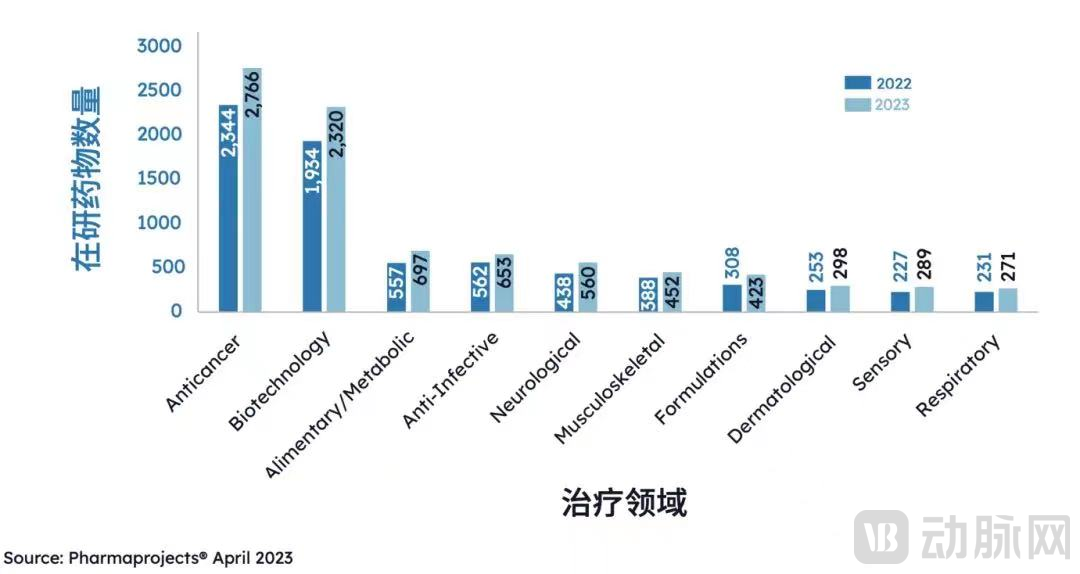

Comparison of Pipelines in Individual Therapeutic Areas Between 2022 and 2023

The report indicates that the number of anti-tumor drugs under development globally continues to rise, reaching a total of 8,480, which accounts for 39.8% of all drugs in global development pipelines, representing a 9.1% increase from the previous year. Among newly identified candidate drugs, more than 40% target at least one type of cancer, a figure higher than the 38.8% recorded in the preceding year and far surpassing the second-ranked therapeutic area, neurological disorders, at 13.5%. In China’s pharmaceutical R&D market, nine of the top ten diseases targeted by domestically developed drugs are cancers. Anti-tumor agents and biotechnological therapies remain the two most prevalent areas of drug research, aligning with global R&D trends. Non-small cell lung cancer is the primary target disease in China’s pharmaceutical R&D sector, whereas breast cancer ranks as the top target disease globally.

The report highlights that immuno-oncology has gained global favor, with related therapies accounting for nearly 16% of the total number of drugs worldwide. However, it is worth noting that as of early 2023, only 2.2% of R&D projects had advanced to the registration and marketing approval stage, with the vast majority of pipelines still in early phases. Although the failure rate for such drug development is high, the pharmaceutical industry remains enthusiastic and confident. In the coming years, companies in this sector, including biotech firms and CROs, are poised for significant opportunities.

From the perspective of pharmaceutical mechanisms of action, the pipeline scale for T-cell stimulators, natural killer (NK) cell stimulators, and immune checkpoint inhibitors and stimulators has all expanded. Furthermore, specific immuno-oncology (IO) technologies have emerged, such as CD3 agonists, PD-L1 antagonists, and PD-1 antagonists. In terms of targets, the well-known PD-L1 has become the most targeted protein in drug development, while the CD3ε molecule and CD19 have also entered the top three ranked targets.

Consistent with the steady growth in global R&D scale, the number of drug pipelines across various development stages worldwide also showed uniform growth in 2023. According to data from Pharmaprojects, the number of pipelines in Phase I and Phase II clinical trials continued to grow significantly in 2023, with increases of 10.7% and 7.2%, respectively. The growth rate for pipelines in Phase III clinical trials rebounded, rising by approximately 9.8%. In contrast, the growth rate of pipelines in the preclinical drug development stage slowed slightly compared to the previous year, increasing by 4.3%.

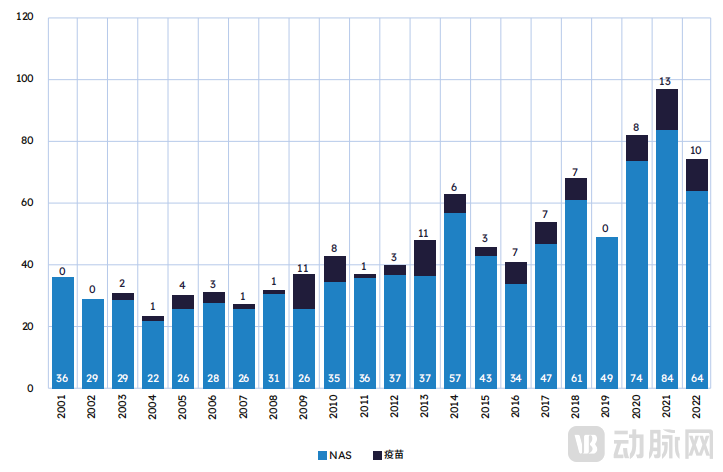

Building on the "Annual Review of Pharmaceutical R&D 2023," the supplementary report "New Active Substances Launched in 2022" provides an in-depth analysis of the global market launch of R&D achievements. Over the past five years, the number of New Active Substances (NAS) introduced globally has been on a steady rise, highlighting the vibrant momentum of global pharmaceutical innovation. The report notes that a total of 73 new drugs, comprising 74 new active substances, were launched worldwide in 2022, ranking among the top three years in the history of the global pharmaceutical industry.

Number of NAS Products Launched Globally Per Year, 2001–2021

According to statistics, oncology once again emerged as the therapeutic area with the highest number of New Active Substances (NAS) launched in 2022, with a total of 21 NAS introduced, accounting for 28.4% of all NAS launches. In terms of the share of total NAS by country, the United States continues to maintain its leading position. Notably, as of March 2022, China’s share of NAS has been steadily increasing, with 16 NAS launched, representing 21.6% of new drugs. The combined total of NAS launched in China and Japan has now reached parity with that of the United States. This demonstrates the burgeoning R&D and innovation capabilities in the Asia-Pacific region, indicating a global shift of innovative strength toward this region.

Among the new molecular entities (NMEs) launched in 2022, 20 met the criteria for first-in-class drugs. The oncology sector led with six novel NMEs, followed by the gastroenterology/metabolism sector (five), and then the dermatology, respiratory, cardiovascular, anti-infective, neurological, musculoskeletal, and ophthalmology sectors. The United States and Japan tied for the lead in innovative drug introductions, each accounting for eight agents.

The supplementary report also boldly predicts the drugs expected to gain approval in 2023. In addition to the two RSV preventive vaccines already launched this May, other promising candidates include aprocitentan, developed by Johnson & Johnson and Idorsia Pharmaceuticals for resistant systemic hypertension; Beyfortus (nirsevimab), an RSV vaccine developed by AstraZeneca and Sanofi; and Zavzpret (zavegepant), a migraine medication developed by Pfizer. These pipeline products are all anticipated to receive marketing approval this year.

Based on a comprehensive review, global drug development is progressing steadily from source innovation to clinical studies. Significant clinical therapeutic achievements are expected in the fields of hematologic oncology and immunobiology, while the application of CAR-T therapy is expanding into the treatment of solid tumors. Global basic financing in neuroscience has returned to second place, trailing only oncology. With the FDA’s updated approval standards for Alzheimer’s disease drugs and deepening insights into the fundamental biology of neurodegenerative diseases, optimism surrounding R&D in this field will intensify further in 2023.

Over the past year, the global R&D market has remained generally stable while undergoing certain changes. Although the lineup of the top ten pharmaceutical companies in global R&D rankings has seen little change, their share of the total number of global R&D pipelines has declined for two consecutive years. In contrast, smaller pharmaceutical companies have demonstrated stronger performance, driving the global R&D market to new heights.

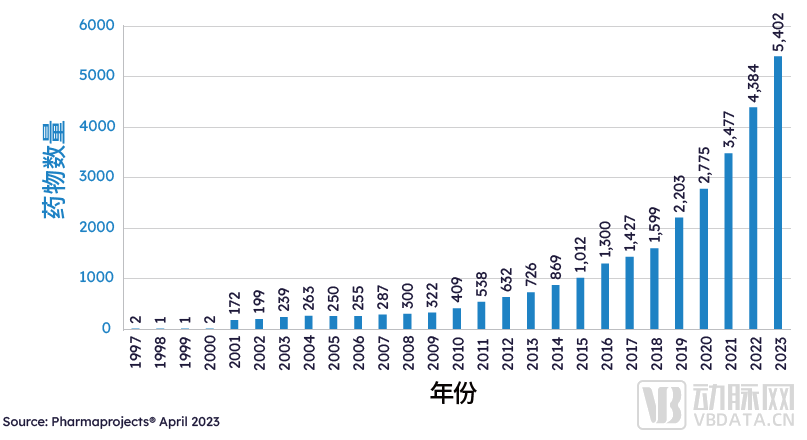

China’s pharmaceutical R&D market has emerged as a dark horse in the otherwise stable global landscape, not only retaining its position as the world’s second-largest country for drug R&D but also demonstrating robust growth momentum. According to Pharmaprojects data from April 2023, China currently has 5,402 drug pipelines, representing a 23.22% increase from 2022 and accounting for 23.6% of the global total—far exceeding the global pipeline growth rate of 5.89%. Meanwhile, China is rapidly catching up in the development of innovative candidate drugs, with 1,457 candidates in 2022, ranking second globally.

China's Pipeline Scale by Year, 1997–2023

China's Pipeline by Year and Therapeutic Area in 2022 and 2023

In recent years, Chinese pharmaceutical companies have actively explored multi-party collaborations to continuously drive innovative development. According to data from Pharmaprojects, as of January 2023, Hengrui Pharma and Fosun Pharmaceutical remained on the list of the top 25 companies globally by pipeline size, while CSPC made its debut on the list. Over the past year, Hengrui Pharma achieved rapid growth, not only increasing its R&D investment by 19.1% but also standing out among the top 25 pharmaceutical companies with significant pipeline expansion, propelling its global ranking from 16th in 2022 to 13th. Notably, in 2022, Hengrui Pharma launched four New Active Substances (NAS), securing the top position in the global pharmaceutical R&D market.

Consistent with global trends, oncology and biotechnology therapies are also the most prominent research areas in Greater China. Among the top ten indications by pipeline volume, nine are cancer-related diseases, with type 2 diabetes being the only exception. Unlike breast cancer, which is the primary target disease globally, non-small cell lung cancer (NSCLC) is the leading focus in China, with 404 drug pipelines recorded as of the statistical cutoff date. Breast cancer ranks second, with 333 pipelines under development.

The report states that the impact of the COVID-19 pandemic is gradually receding worldwide. Against the backdrop of an increase in the number of clinical trials across nearly all therapeutic areas, ongoing anti-infective trials have decreased by 1.2% compared to the previous year. The number of ongoing trials for treatments, vaccines, or supportive therapies targeting SARS-CoV-2 has declined from over 2,500 to 2,384 this year, while the global ranking of drugs targeting the SARS-CoV-2 spike protein has dropped from 12th to 20th place. Nevertheless, it is undeniable that the pandemic has accelerated vaccine research globally and permanently transformed clinical trial practices, leading to remarkable advances in the management of severe diseases.

Over the past three years, although the overall structure of the pharmaceutical industry has remained relatively stable, it is encouraging to note that with the receding threat of the pandemic, industry practitioners have shifted their focus to developing drugs for a broader range of diseases and rare disorders. According to data from TrialTrove in January 2023, there were 6,682 drugs under development globally for 718 rare diseases, with the number of rare disease trials initiated in 2022 surging by 25.4%. Among these, 1,452 drugs were developed for single indications, representing an increase from 1,408 a year earlier.

Biotechnology-based drugs have consistently garnered significant attention. Antibodies remain the most popular class of biologics this year, followed closely by recombinant proteins, while categories such as allogeneic cell therapies, synthetic nucleic acids, and viral vectors have demonstrated the highest growth rates. Amid the biotechnology boom, it is easy to assume that the pharmaceutical industry is gradually leaving small-molecule drugs behind. Although this trend has largely held true over the past 30 years, it does not apply this year: traditional chemical small-molecule drugs grew by 7.8%, indicating that conventional molecular manufacturing methods remain highly vibrant. Meanwhile, this year marks the first time since 2004 that the proportion of biotechnology-derived drugs in the pipeline has slightly decreased compared to the previous year, currently standing at 44.0%, down from 44.7%.

Looking ahead, the report points out that R&D activities in the pharmaceutical industry will continue to increase comprehensively. In terms of pipeline composition and its characteristics, the annual structural changes are relatively small and remain in a state of steady growth, thus promising sustainable growth.

The full versions of “2023 Annual Review of Pharmaceutical R&D” and “New Active Substances Launched in 2022” are now available. Scan the exclusive QR code below from VCBeat New Pharma to download the reports for free:

About Citeline

Citeline, a Norstella company, offers a comprehensive suite of complementary commercial intelligence products that work in concert to meet the evolving needs of health science professionals, accelerating the bidirectional connection between treatments and patients. These patient-centric solutions and services deliver and analyze data to drive clinical, commercial, and regulatory decision-making while creating real-world growth opportunities.

Citeline’s global team, composed of analysts, journalists, and consultants, closely monitors trends in the pharmaceutical, biomedical, and medical technology industries, providing expert insights across key areas such as major diseases, clinical trials, drug development and approval, and market forecasting.