From Lab to Market: Oncotica Files IPO Prospectus Led by University Professor’s Cancer Therapy Breakthrough

This excerpt is taken from Research to Revenue, authored by Cam Patterson and Don Rose, with a foreword by Herbert Boyer, co-founder of Genentech. In his foreword, Boyer emphasizes the concept of the “university ecosystem” proposed by the two authors and underscores the proactive role universities should play in technology transfer. The book aims to help universities incubate and develop startups from research projects, translating scientific achievements into tangible commercial value. Drawing on extensive experience and case studies, the authors provide a systematic set of methods and strategies to help entrepreneurs effectively advance university-based startup initiatives.

This case study chronicles the entire journey of an innovative cancer therapy, from its initial conceptualization in the laboratory through patent registration, company formation, team recruitment, fundraising, and clinical trials, as it gradually makes its way to market. While the company and characters depicted are fictional, every twist and turn described draws upon real-world examples. It is hoped that this comprehensive overview of the end-to-end process—taking a university professor’s entrepreneurial venture from 0 to 99—will offer scientists who are preparing for or already engaged in entrepreneurship a fresh perspective. For ease of reading, the cases presented in this book have been adapted and refined.

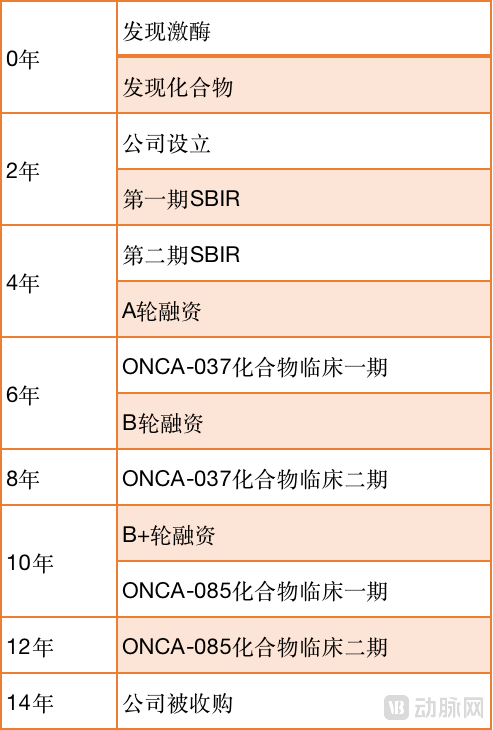

The timeline below lists the major milestones in the company's development history.

1Discovery of New Targets

Dr. Davis said nothing. He rose and walked straight to the vending machine at the end of the corridor outside the laboratory, where he bought a can of ice-cold cola. He downed the entire can in one go, giving no thought to whether it was sweetened with white sugar or aspartame. His mind was elsewhere.

As a professor at the University Cancer Center, Dr. Davis discovered a novel protein kinase in previous experiments. This kinase is activated in patients with cancer and accelerates tumor cell growth by promoting angiogenesis. Through collaborative development with multiple partners, Dr. Davis ultimately identified several compounds capable of inhibiting the activity of this novel kinase. Following medicinal chemistry optimization, these compounds were tested in animal models. One of the compounds demonstrated a significant reduction in tumor growth in preliminary studies using a murine tumor model.

Simply put, he discovered a new pathway for inhibiting tumor growth.

Upon reviewing the preliminary results, Dr. Davis immediately recognized that this kinase held significant promise as a novel therapeutic target for cancer, implying that his discovery could pave the way for new clinical strategies in existing oncology treatments. For this reason alone, he felt justified in celebrating with a can of cola, calories be damned. Of course, it also served to calm his racing heart.

After taking a moment to compose himself, Dr. Davis began to review the existing achievements and outline the next steps. First, he identified a novel target—a kinase—not previously mentioned in the literature, which acts as a “master switch” in tumor growth. Furthermore, several chemical compounds (inhibitors) are also new and fall within the scope of patent protection. The next step is to conduct further testing on the efficacy and toxicity of these compounds. Finally, it is necessary to determine which specific cancer type to focus on. This decision will be primarily driven by unmet clinical needs and therapeutic efficacy.

2Submit an invention disclosure in a timely manner

As a tenured professor at the university, Dr. Davis held the institution’s rules and regulations in high regard. Therefore, once he determined that his research findings held further translational value, Dr. Davis recognized his obligation to report them to the university. Additionally, as he was preparing to deliver a keynote address at the American Association for Cancer Research (AACR), where he would publicly discuss his newly discovered targets and inhibitors, he submitted an invention disclosure to the university’s Technology Transfer Office (TTO) to seek protection for his achievements. After all, if a patent application is not filed within 6–12 months following public disclosure, the ownership of these achievements could become uncertain.

A licensing officer from the Technology Transfer Office interviewed Dr. Davis. The officer was meticulous, and both parties identified and discussed the following facts:

Mason, a graduate student, played a pivotal role in the discovery, cloning, expression, and characterization of this kinase target.

Another graduate student, Thompson, developed antibodies to inhibit this kinase and isolated its natural ligand.

Dr. Davis and Dr. Switzer, a medicinal chemist with expertise in kinase inhibition, jointly designed a series of compounds for testing in xenograft models.

These compounds were synthesized by a contract research laboratory in India.

All work was funded by the National Cancer Institute of the U.S. National Institutes of Health (NIH).

As the discovery of new targets and compounds may involve multiple inventors, the licensing officer engaged a patent counsel from an experienced external intellectual property/patent law firm to address inventorship issues.

3How many patents are being applied for? Whose patents? What kind of patents?

At this stage, it is time to allocate actual financial resources from the school’s budget. As the primary source of funding for public schools, taxpayer money must be spent in accordance with clear and established guidelines.

In assessing the value of intellectual property and determining which patents to file, the Technology Transfer Office considered the kinase target to have limited value, while the compounds were deemed to hold higher value. Given the current lack of evidence supporting the target’s utility as a diagnostic biomarker and the high costs associated with patent maintenance, the Technology Transfer Office decided against filing a patent application for the use of this target in early cancer screening. In contrast, the identified compounds exhibit high-level inhibitory activity (nanomolar potency), demonstrating their efficacy and providing a competitive advantage in out-licensing or collaborative development negotiations.

The question of inventorship ultimately fell to Dr. Davis and Dr. Switzer. Since there was no intention to seek patent protection for the kinase, graduate students Mason and Thompson were excluded from discussions regarding patent registration. Although the two graduate students felt somewhat disappointed, they recognized that the path of scientific research is long, and completing their papers and graduating smoothly were more immediate priorities. The patent consultant conducted interviews with the two doctors. Despite their unequal contributions, both were ultimately deemed co-inventors because each had contributed to the discovery.

The final issue pertains to contract research organizations (CROs) in India. To reduce research expenditures, Dr. Davis requested that the laboratory provide academic rates below market price. In exchange, the laboratory retained the right to commercialize any compounds it synthesized. Naturally, this retained right is limited to India. This arrangement is highly likely to give rise to potential issues in the future; for instance, once these compounds are successfully commercialized, other companies may be precluded from selling the product in India. However, this is not currently a primary concern for the Technology Transfer Office (TTO), as any such issues would not arise for several years. Furthermore, patent counsel has determined that the laboratory is not an inventor of the intellectual property, as it merely synthesized the compounds under the direction of Dr. Switzer.

Based on the above, the TTO decided to file a provisional patent application for these compounds, listing both Dr. Davis and Dr. Switzer as inventors. With this provisional patent application in place, the two researchers will have 12 months to supplement experimental data, refine the invention, secure investors, and strategize their patent portfolio.

4Unsure About the Market? Recruit a Few Advisors First

As Dr. Davis contemplated his next steps, a vague memory surfaced in his mind of an event he had once seen taking place inside a university lecture hall as he passed by. The words “Entrepreneurship,” “Workshop,” and “XX Capital” stood out prominently in that mental image.

The research and innovation capabilities of universities, coupled with robust technology transfer mechanisms, have spurred the emergence of numerous startups from academic and research institutions. Prominent investment firms frequently collaborate with founders of publicly listed companies who are alumni to conduct roadshows and lectures on campus, aiming to identify and incubate new projects. Dr. Davis plans to meet with Dr. Switzer to discuss the feasibility of founding a company focused on these kinase inhibitors.

Dr. Switzer is a rising star in the department, having led his team to publish multiple papers in top-tier journals in a short period, thanks to his unique understanding of molecular structures; one of these manuscripts has even completed the review process at Science. The coffee had barely been served when Dr. Switzer stated that, with his tenure review still a few years away, he did not wish to divert too much energy into entrepreneurship. He was willing to provide ad hoc consulting, as this area falls within his expertise and aligns with his interests. In Dr. Switzer’s view, academic research remains the more conventional path. Dr. Davis was clearly prepared for this response. Having already secured tenure and feeling more passionate about exploring the clinical applications of his work, he decided to take the lead in establishing the company.

Both individuals recognized the need to seek additional input from business professionals with experience in oncology and drug development. Through referrals from the Technology Transfer Office (TTO) and faculty colleagues who had previously been involved in startups, they identified several local candidates to serve as advisors. One advisor had worked for many years at a large pharmaceutical company before joining a biotech startup as Chief Medical Officer (CMO), where he helped advance a compound to Phase IIb clinical trials. The other was an oncologist at the university’s cancer center who had participated in multiple projects in the pharmaceutical and biotechnology sectors.

After some brief business pleasantries, Dr. Davis and Dr. Switzer presented the team with printed copies of the data. Following several minutes of silent review, Andrews, the first advisor—who was more familiar with the market—broke the silence. “The data look impressive, and I have no doubt about their authenticity. But to put it bluntly, so as not to waste anyone’s time: the technical, regulatory, and financial risks involved in taking this product to market are substantial.” The second advisor, who had deeper clinical expertise, said he had only one question. “Which cancer types are these compounds intended to target?”

5Don't rush to write the business plan; try to demonstrate the project's feasibility first.

The conclusion drawn from the first round of discussions was highly pragmatic: before drafting a comprehensive business plan and registering the company, it is essential to conduct a feasibility study to determine whether establishing the company is truly necessary.

Dr. Davis and the aforementioned consultant, Andrews, who has experience in both large pharmaceutical companies and startups, jointly conducted the project feasibility study.

“The primary task is to narrow the therapeutic scope of the product, as these compounds are highly unlikely to exhibit broad-spectrum efficacy.” Andrews’ proposal was highly constructive.

“This kinase is highly expressed in gastrointestinal cancers, and initial testing was conducted in colon cancer models; therefore, these cancer types should be considered first.”

Andrews performed a quick calculation of the current number of patients with gastrointestinal cancers and the annual incidence of new cases, based on the information provided by Dr. Davis. From the slight raise of Andrews’ eyebrows, Dr. Davis was convinced that the market size was substantial.

Based on Andrews’ prior experience, the next task for the two was to conduct preliminary market research to understand the current standard of care for gastrointestinal cancers. Through a series of interviews with gastrointestinal oncologists, they gained insights into the available treatment options, their efficacy, and success rates. Subsequently, the pair began formulating a basic preclinical development plan. In this phase, Andrews drew more heavily on his experience, while Dr. Davis needed to determine which components could be funded through his own research grants and which would require alternative funding sources, such as external grants or investment.

Armed with this information, they reconvened the original advisory team and added additional members (a gastrointestinal oncologist and a preclinical CRO specialist), further elaborating on the project’s rationale and deduction. The team also provided corresponding feedback:

First, there are some obvious questions (e.g., Is this compound more effective than current treatments? Is it safe?) that require future experiments and funding to answer.

Secondly, whether investors will perceive this as a “one-trick pony” project (i.e., whether the drug is effective only against one type of cancer).

Despite its low expression levels, this kinase is indeed prevalent in other cancers. The team believes that if the first drug can be developed in collaboration with partners, and the company subsequently secures additional compounds to treat other cancer types, its growth prospects remain promising.

6Bring all personal identification documents and engage a lawyer to register the company.

After a weekend of mental preparation and strategic review, Dr. Davis announced his decision to lead the establishment of the company to the team on the first workday. He had initially hoped that Andrews would join as a co-founder, but since Andrews could not afford to work solely for equity over the next 6 to 12 months, he opted for another, more stable full-time position.

Like a first-year business school student crafting their first Business Plan, Dr. Davis excitedly began brainstorming names for the company. After conducting thorough uniqueness checks using search engines and specialized software, he ultimately settled on “Oncotica.” He collaborated with a local agent attorney to incorporate the company as a C corporation in Delaware, recognizing that this structure would be advantageous for securing venture capital funding in the future.

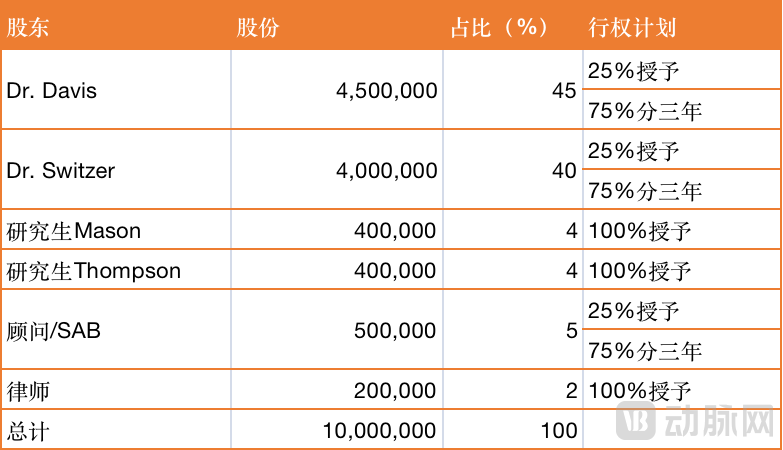

Dr. Davis wished to reward those who had contributed to the project over the years with equity. He therefore compiled a list of 23 individuals—former graduate students, postdoctoral fellows, and other collaborators—and submitted it to his attorney as the complete roster of shareholders. The lawyer’s expression upon seeing the list is something he still finds hard to forget.

The lawyer took a deep breath and began to explain why this was not a good idea. “Except for a few individuals, most people have made only minor contributions. Granting them all equity would make the company’s incorporation highly complex and become an obstacle for future venture capital investments. Merely keeping track of these shareholders or obtaining their consent for document signatures will be a very troublesome task in the future.” Dr. Davis, who was not yet fully familiar with these concepts, asked, “How troublesome could it really be?”

“It’s almost like having a group meeting every week, but everyone has to play the role of both mentor and graduate student.” The nightmarish memories from Dr. Davis’s youth—being challenged by his advisor and subjected to peer pressure from classmates—shot through him like an electric current. He immediately whittled the list down from 23 names to just two.

After completing the necessary paperwork, Dr. Davis specifically chose a Friday afternoon to discuss equity allocation with Dr. Switzer, as both were the primary founders. As the largest shareholder, Davis held a 45% stake, while Switzer came in second with 40%. When the proposal was presented, Switzer, who had been leaning forward over the coffee table listening to the lawyer, instinctively leaned back into his chair and placed his hands on the armrests.

Dr. Davis hurriedly attempted to rephrase his words, but the lawyer was accustomed to such situations. He continued to explain that Dr. Switzer’s equity reflected his past contributions, whereas Dr. Davis’s equity represented both past and future contributions—namely, establishing the company, organizing and leading the Scientific Advisory Board (SAB), participating in the preparation of grant applications, and providing biological insights for drug development. Although Dr. Switzer did not have a business background, he quickly mentally assessed the workload involved in these tasks. “I understand. Where do I need to sign?” The brief tension that had settled over the coffee table dissipated, and the conversation returned to its normal course.

For the time being, Dr. Davis and Andrews (who has agreed to continue providing consulting services to the company) will be the sole members of the Board of Directors, with a lawyer serving as the Corporate Secretary. The equity allocation is as follows:

Under the explanation and guidance of the attorneys, Dr. Davis established distinct vesting schedules for the company’s various founders. Both Dr. Davis and Dr. Switzer are required to become fully engaged at a future point. For Dr. Switzer, this entails contributing through his roles on the Scientific Advisory Board and the Board of Directors; failure to participate will result in the forfeiture of his unvested shares. The same provisions apply to advisors. Members of the Scientific Advisory Board must remain engaged over the long term to receive their full equity allocation. As the students have already made contributions in the past, it is unnecessary to establish vesting schedules for them. The attorneys waived certain legal fees in exchange for equity. Following the advice of corporate counsel, Dr. Davis did not reserve any equity for the future management team; instead, the equity held by the aforementioned individuals will be proportionally diluted to accommodate allocations to the future management team.

7Professional Team, Dedicated Specialists

After the founding of Oncotica, the founders began recruiting a CEO.

Lacking capital, they faced a challenge common to all life sciences startups: how to persuade an experienced biotechnology executive to assume substantial risk with equity compensation as the sole remuneration? Dr. Davis knew he was not up to the task. He admitted that he had once briefly fantasized about donning bespoke three-piece suits and leading his team in intense business negotiations across thick oak conference tables with established European pharmaceutical companies. But this was reality, not a life sciences spin-off of Mad Men. Dr. Davis neither had sufficient training nor should he squander precious energy on corporate management and operations. Scientists prefer working at the bench rather than sitting behind a desk.

As an alternative, they recruited Jan McCallister, a business development executive recently laid off by Big Pharma. They appointed her as Vice President of Business Development, granting her equity and a sales commission based on the value of deals closed over the next 12 months. The founding team was highly impressed by McCallister’s drive and her extensive network within the pharmaceutical industry. By establishing the VP of Business Development role, they could begin exploring partnership opportunities, with plans to recruit a CEO and/or initiate venture capital fundraising once progress was made. Additionally, Dr. Davis organized Oncotica’s inaugural Scientific Advisory Board meeting, which proved highly productive in terms of both scientific direction and industry connections.

8Authorized by the University

To secure a license for the technology from the university’s Technology Transfer Office, Dr. Davis delegated negotiation authority to the company’s corporate counsel and an external board member. Given that the company was still in its very early stages, they decided to first obtain an exclusive option on the technology, which would allow them to secure a license in the future. The option agreement had a term of 12 months and cost $10,000, which was not applicable toward the license agreement. Both Dr. Davis and Dr. Switzer agreed to contribute a portion of the funds to secure the option agreement. The final terms were as follows:

9In-Depth Market Research Beyond Equity Research Reports

After resolving the issue of intellectual property usage rights, Dr. Davis returned to the laboratory bench, where he felt most comfortable and secure. Further research in the laboratory confirmed the compound’s activity in colorectal cancer models. The company decided to focus its market research on this indication. Through individual and multiple channels (Scientific Advisory Board, advisory panels), the team selected and interviewed oncologists specializing in the treatment of colorectal cancer. The interviews explored the challenges of treating colorectal cancer, the advantages and disadvantages of first-line and second-line therapies, as well as pricing and reimbursement situations. Dr. Davis and McCallister also met with executives from a large health insurance company to understand the reimbursement landscape for cancer treatments.

Throughout this process, the company’s VP of Business Development, McCallister, played a pivotal role. A Scottish-American, she is known for her signature freckles and a mane of frizzy red curls. Her hairstyle typically exists in one of two states: either splayed out like a haystack in daily routine, or tied back with a frayed hair tie when meeting clients. McCallister is efficient and direct in communication. Whenever discussions hit key points during meetings, she instinctively clenches her molars, accentuating her already prominent jawline—a sharpness that mirrors the padded shoulders of her suit jackets.

To provide a more intuitive and visual overview, McCallister created a matrix of potential partner companies, including those with products targeting colon cancer. She identified products currently undergoing clinical trials and those already on the market through official government channels, paying particular attention to their patent expiration dates. As Dr. Davis observed the diagram McCallister sketched on the whiteboard with a marker, his confidence grew somewhat. This information provided an overview of the products and companies, helping to determine which partners should be approached.

Of course, these alone were not enough. Leveraging the network he had built through his previous work at big pharma and his attendance at academic conferences, McCallister placed calls to several physicians and retired FDA officials.

““The primary market drivers for colon cancer treatment remain safety and efficacy.”

“Of course. I see at least ten articles every day reiterating these same points. But ours is a novel target and a novel inhibitor—not a dual- or triple-drug combination!”

“We cannot deny that a certain level of toxicity is observed in many current treatments, and the life-saving nature of cancer therapy is also critical.”

“I need you to give me some reassurance.”

“Efficacy must outweigh safety, McCallister.”

“Understood! Thank you very much for your explanation.”

After cordially bidding farewell to the former FDA official, McCallister and Dr. Davis had a clear sense of direction. To determine the level of therapeutic efficacy required to secure FDA approval, the company focused on its current and pipeline treatments. By integrating these insights with information on its product pipeline and upcoming patent expirations, the company gained a realistic outlook on the market landscape over the next 7–10 years, by which time Oncotica’s products are expected to reach the market.

10The Final Piece of the Business Model Puzzle

Like most innovative therapy companies, Oncotica is highly likely to partner with collaborators at some stage of clinical development. The timing of such partnerships will depend on the level of interest from partners (large pharmaceutical or biotechnology companies), which is driven by their strategic priorities and the status of their current product pipelines. Ideally, pharmaceutical companies show the greatest interest after Phase II clinical trials. However, if the drug addresses a clear unmet medical need during preclinical or early clinical stages, or if it aligns exceptionally well with a pharmaceutical company’s strategy, collaborations may also be discussed at the preclinical stage. The biggest challenge for startups like Oncotica is securing sufficient cash to support preclinical and early clinical (Phase I) development, which may require $5 million to $10 million. The most likely source of such substantial funding is venture capital firms specializing in biotechnology investments.

When Oncotica identifies a partner, the nature of the collaboration will depend on Oncotica’s funding needs and the partner company’s expertise. If Oncotica has already raised sufficient capital to achieve meaningful milestones, its pharmaceutical partner may provide only advisory support until larger-scale clinical trials become necessary. Conversely, the partner may assume responsibility for the majority of the research efforts, with the Oncotica team collaborating with the partner to design and execute studies funded by the partner.

11Corporate Website: Showcase of Information and Credibility

After achieving considerable phased progress, Dr. Davis believed it was time for the team to engage in some relatively relaxed tasks. On another Friday afternoon, the founders gathered to discuss the selection of the company logo. After discarding a red design that might evoke associations with blood in patients, they debated at length over two different shades of blue for the same logo. Ultimately, they chose the version available under a free copyright license.

Next, the founders reserved the domain name oncotica.com for the company’s website and created a simple site using a WordPress template. The site included an “About” page, a “Founders and Management Team” page, a “Technology” page, and a “Contact” page. They also provided links to the most relevant publications. The purpose of the website was to serve as a convenient access point for recruiting advisors and executives. It would also become the core foundation for developing a full-fledged website when the company began its fundraising efforts.

12The BP being written now is what a real BP should be.

The initial Oncotica business plan was a 20-slide PowerPoint presentation, including several appendices. The BP focused on several key points:

First, Oncotica’s drug is differentiated from other oncology agents. The discussion of its mechanism of action is sufficiently compelling to persuade both non-experts and scientists. Furthermore, other therapeutic approaches in the field of colorectal cancer are discussed and compared with Oncotica’s product. In making these distinctions and comparisons, the proposal selects content supported by data, such as the novelty of its mechanism, while refraining from comparison in areas lacking validation, such as efficacy and safety.

Secondly, product development. The team has thoroughly completed the preclinical development work required by the FDA prior to IND submission, including animal models, toxicity testing, pharmacodynamics/pharmacokinetics (PD/PK) studies, and Chemistry, Manufacturing, and Controls (CMC). The appendix slides also include detailed quotations from several Contract Research Organizations (CROs) to substantiate the company’s actual funding requirements.

Next, intellectual property. Particular emphasis is placed on completed patent filings, demonstrating the company’s patent landscape for its compounds. The appendix slides include details on application status and Technology Transfer Office (TTO) progress.

Subsequently, an overview is provided of the future strategy for selecting partners, including the names of potential key partners and the rationale for their selection (e.g., whether they have compounds with patents nearing expiration, or developed oncology compounds with limited focus on colorectal cancer).

The business plan concludes with management profiles and financial data, accompanied by a table providing further details. The focus is on the costs required to complete three stages: submitting the Investigational New Drug (IND) application, conducting the first-in-human Phase I trial, and performing the initial efficacy and safety Phase II trial. If the Phase II data appear promising, the plan is to license the compound to a major pharmaceutical company for continued development, thereby securing sufficiently optimistic upfront payments, milestone payments, and licensing revenue.

13Initial Fundraising Amount

The company adopted two approaches to raise capital: applying for SBIR (Small Business Innovation Research) grants and seeking seed-stage venture capital funding. During the preliminary preparation phase, Dr. Davis heard that the so-called “primary market” was experiencing a “winter.” Although he was not particularly sensitive to such terminology, he did not have high expectations for securing venture capital support at this stage.

The team reached out to 20 venture capital firms. Eight of them engaged in preliminary phone discussions, and three invited the team for in-person meetings to present their pitch deck. Although the team’s presentation sparked investor interest and prompted a series of questions, the final response from each firm was identical: “It appears too early at this stage. Let’s reconnect once you have further data. Let’s stay in touch.”

Fortunately, the company secured a Phase I SBIR grant from the National Institutes of Health/National Cancer Institute to achieve two milestones: designing and synthesizing 10 new compounds based on the first identified hit compound, and conducting medium-throughput screening of these compounds in the laboratory of a university incubator. After nine months of effort, the company successfully identified a lead compound with low-nanomolar potency and a backup compound with high-nanomolar potency. The company also obtained a 12-month Phase II SBIR grant to initiate preliminary toxicity, pharmacodynamic, and pharmacokinetic studies.

Although these grants have helped Dr. Davis obtain more comprehensive data, the company still faces unmet funding needs, specifically for engaging regulatory consultants with compliance expertise to assist in preparing for pre-IND meetings with the FDA, and for providing financial support for both prior and new patent applications.

After obtaining the data, the team re-engaged with the original eight venture capital firms and held meetings with two of them. The company sought to raise $2.5 million to complete the studies required for an Investigational New Drug (IND) application, initiate the first-in-human Phase I clinical trial, and provide additional working capital. One of the venture capital firms, Peak Ventures, was highly interested in the company but wished to see the results of the Phase II SBIR study first. The firm agreed to invest $250,000 via a convertible note (seed round) to help cover part of the patent costs and enable the company to hire regulatory consultants to map out the regulatory pathway, particularly to determine the costs associated with the studies required for the IND application.

14A Cost-Effective Office Space

The company had already begun operations within a university incubator, but after the seed funding round, Dr. Davis sought a dedicated space for meetings and data review, and more importantly, to instill a stable “corporate atmosphere” within the team. The team connected with a company that had recently filed for bankruptcy and assumed the remaining two years of its lease through a sublease agreement. Although the space comprised only offices and a single conference room, it was perfectly sized for the Oncotica team.

The experiments are currently being conducted at the university’s incubator. Given the company’s current financial situation, purchasing expensive laboratory equipment and reagents is simply unthinkable, not to mention the series of environmental impact assessment issues that would arise from building an independent laboratory.

15

Raise Growth Fund

After 12 months of effort, the Phase II SBIR data for Oncotica’s lead compound, ONCA-037, appear highly promising. Although the toxicology results are somewhat ambiguous, they can be addressed through alternative compounds. Armed with these data, Dr. Davis and his team headed to Peak Ventures’ office for a more confident negotiation.

Through due diligence and discussions with regulatory advisors, Oncotica has outlined the allocation of the total $3 million required: $1.5 million for completing pre-IND studies, $750,000 for Phase I clinical trials, and $750,000 for working capital (covering salaries, intellectual property fees, rent, consultants, etc.). Peak Ventures has also provided a Term Sheet for this round of financing. The term sheet includes the following key terms:

Investment: The $3 million investment will be disbursed in installments, with an initial tranche of $2 million allocated to support the company’s submission of an Investigational New Drug (IND) application. The remaining funds will be released upon submission of the IND.

Valuation: The company’s pre-money valuation is set at $5 million. With a $3 million investment, Peak will hold approximately one-third of the company’s equity.

Stock Options: To provide incentives for the future management team, a stock option pool of one million shares (approximately 6% of the company's total share capital) will be issued.

Board Seats and Management: As Oncotica does not have a Chief Executive Officer, Dan Rivers, a Managing Partner at Peak, has assumed the roles of Interim CEO and Chairman. The company plans to recruit a full-time CEO as it approaches the submission of its Investigational New Drug (IND) application.

The founders expressed concern over relinquishing one-third of the company’s equity. However, these terms were not entirely one-sided. Dr. Davis highly valued Dan’s industry experience. Many years ago, Dan founded a biotech startup and took it public; after exiting, he established Peak Ventures to continue deepening his engagement in the life sciences sector. Dr. Switzer conducted a cross-sectional analysis of comparable data from other venture capital deals in the biotechnology industry and found that their valuation was not the worst. Meanwhile, advisors believed that securing financing under such adverse market conditions constituted success in itself.

Ultimately, the company signed the agreement.

16The Company's Core: R&D

With the investment secured, the company immediately initiated pre-IND studies. Given the growth of the CRO industry, it was able to outsource the majority of the research work. The company also hired a Vice President of R&D and a project manager to plan and oversee the research efforts. Although some minor issues arose during the study, the data remained reliable. Consequently, the company submitted an Investigational New Drug (IND) application to the FDA, paving the way for first-in-human trials and triggering the release of the second tranche of venture capital funding.

After submitting the Investigational New Drug (IND) application, the company hired a Chief Medical Officer (CMO) to oversee the clinical development of its drug candidates. This CMO was recruited through an executive search firm and had previously guided multiple products into clinical trials, possessing a clear understanding of where regulatory hurdles typically arise throughout the process. However, having come from a large pharmaceutical company, he was entirely unaccustomed to operating under such tight budget constraints. Cost-saving measures as extreme as using pipette tips as medicinal spoons were completely unheard of to him. Coupled with his arrogant personality, this quickly led to numerous heated discussions with the Vice President of R&D and the CEO. As the management team expanded, such conflicts were inevitable. In addition to the CMO, the company had planned to hire several clinical and regulatory affairs professionals, but unfortunately, the current personnel budget was insufficient to support these recruitments.

17The Company's God—Customers

After the company successfully secured financing and brought on a CEO and a VP of R&D, McCallister redirected her focus to her core business development (BD) responsibilities—building relationships with potential pharmaceutical partners. She evaluated a range of potential partners, including small pharmaceutical startups with products complementary to Oncotica’s portfolio, as well as large pharmaceutical and biotechnology companies facing impending patent expirations or seeking to fill gaps in their oncology pipelines.

She is open to various types of partnerships, including joint development and corporate acquisitions. She recognizes that few companies are willing to collaborate with startups in the preclinical stage, but she also understands that building these relationships takes time; therefore, now is an opportune moment to introduce the company and its products to potential partners. McCallister is extremely driven, seemingly constantly on conference calls establishing or maintaining relationships. However, even favorable results from Phase I clinical trials are insufficient to bring Oncotica to the negotiating table with partners.

18Ongoing R&D and Fundraising

After the company exhausted its cash reserves, Dr. Davis had no choice but to seek additional funding from Peak. Following the proposal of an $8 million Series B financing plan, Peak expressed interest in the deal but required other firms to participate as co-investors. Securing sufficient co-investors took time, while the company was in urgent need of capital. To buy time and avoid laying off key employees, the company agreed to accept a bridge loan from Peak to sustain operations. Two other venture capital firms were also willing to participate in the transaction; however, due to a significant downturn in the capital markets, the pre-money valuation stood at a deeply disappointing $8 million—identical to the post-Series A valuation—resulting in a flat round. Despite the substantial equity dilution, the company proceeded with the Series B financing to enable the continuation of Phase II clinical trials.

Unfortunately, the Phase II results for ONCA-037 were inconclusive. The trial failed to meet its primary endpoint but did achieve its secondary endpoints. After consultations with the FDA and key advisors, Oncotica decided to abandon this compound in favor of an alternative candidate, ONCA-085, which had also demonstrated promising performance in preclinical testing. While ONCA-085 exhibited a safety profile comparable to that of ONCA-037, its efficacy (survival rate) appeared to be approximately 40% higher. Of course, no compound is perfect. The synthesis of ONCA-085 is highly complex, involving excessive steps that result in highly variable yields. The team has begun to raise concerns about whether the production of ONCA-085 can be successfully scaled up for clinical trials.

As the company once again faced a cash shortfall, along with the high-risk prospect of scaling up production and conducting costly Phase I and II clinical trials, investors carefully weighed their options and decided to extend a bridge loan. This loan provided the company with the time to engage external experts to review preclinical data and to design an improved clinical protocol based on the failed Phase II trial, thereby increasing the likelihood of success. On the positive side, the team had already accumulated substantial experience and know-how with compound 037, and advisors held a highly favorable view of compound 085. However, on the downside, the new clinical trial would require adding several trial sites, and the resulting scale-up would introduce considerable risk and uncertainty.

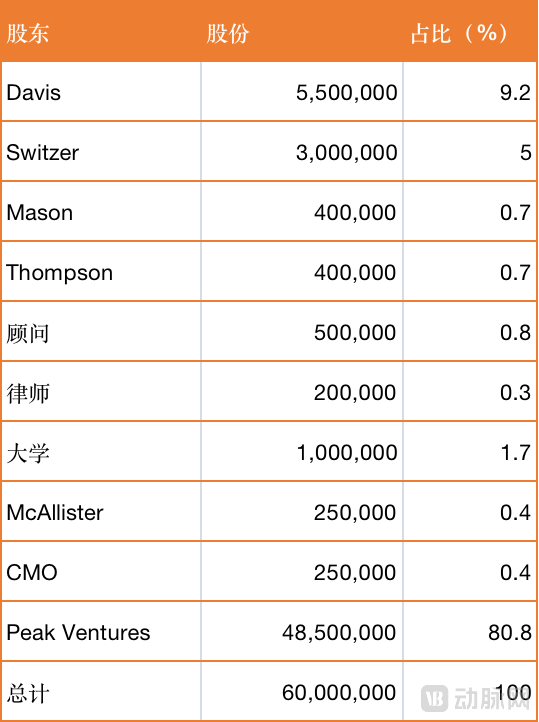

Peak had been involved in this transaction for a full five years and was exhausted from managing the company. Consequently, Peak decided to make a $12 million Series B2 investment to attract partners. While this was good news for the company, it was a bitter pill for the founders, as the investors set the pre-money valuation at a highly disappointing $8 million, marking a typical down round. Although this was extremely difficult for the founders to accept, they ultimately had no choice. Due to multiple rounds of equity dilution from early-stage investments, the founders had long since lost control of the company. Nevertheless, this funding still provided the company with an opportunity to advance its more promising products into clinical trials and even toward patient access.

1999 Startups

Contrary to all expectations, the Phase I and II clinical trial results for 085 were highly favorable. Armed with this data, the management team initiated discussions with several pharmaceutical companies that McAllister had previously contacted. Through engagements with these firms and others—involving nearly 50 site visits and presentations, along with countless phone calls and emails—four companies demonstrated sufficient interest to sign non-disclosure agreements and commence preliminary due diligence. Over the following six months, the number of prospective partners was narrowed down from four to two.

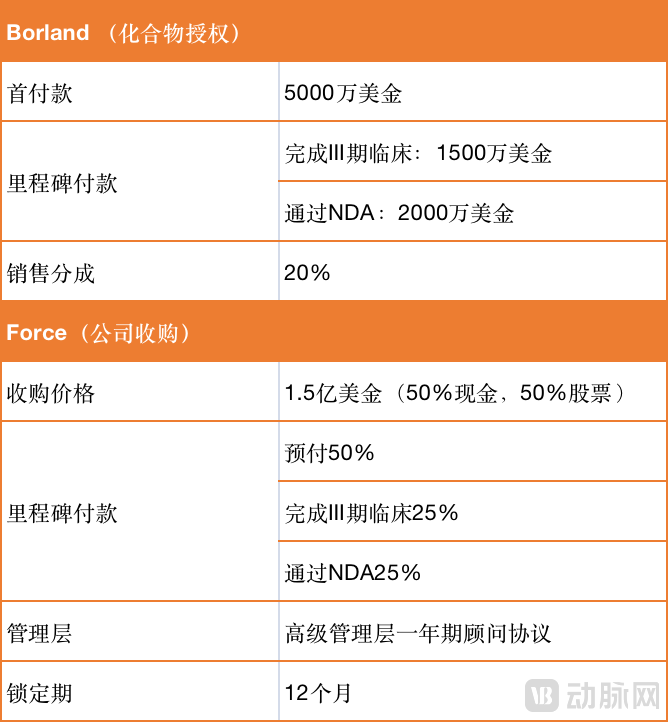

One is Borland Biotech, a small biotechnology company, and the other is Force Pharmaceuticals, a mid-sized publicly listed specialty pharmaceutical company. Borland has just experienced a failure in its Phase III clinical trial for colorectal cancer and urgently needs to formulate a contingency plan. Fortuitously, Borland has secured substantial funding, and it could raise an additional round of financing if a partnership is established. Initial discussions between Oncotica and Borland centered on licensing the development of a colorectal cancer compound. Force faces patent expiration for one of its colorectal cancer treatments in five years and requires a new product to replace it. Preliminary conversations with Force appear to lean toward a direct acquisition of Oncotica.

The team skillfully managed to conduct two negotiations simultaneously, tactfully ensuring that each party was aware of the other’s presence at the negotiating table. The discussions evolved to the point where both companies presented term sheets nearly concurrently, although this required considerable effort (Oncotica delayed Force for six months before finalizing both deals in close succession). Borland sought to license asset 085 from Oncotica, agreeing to pay an upfront fee, milestone payments upon achieving clinical and regulatory milestones, and royalties on sales revenue. In contrast, Force aimed to acquire Oncotica outright. The key terms of each deal are as follows:

It is evident that both deals are highly attractive. The total value of the Borland transaction amounts to $85 million, comprising upfront payments and milestone payments, with annual royalties ranging from $160 million to $200 million based on the patent life of the compound (assuming annual sales of $800 million to $1 billion over an eight-year period). In contrast, the Force transaction is valued at $150 million in cash and stock. Investors clearly favor the Force deal, as it allows them to lock in definite returns earlier, even though restrictions on the sales period and insider trading will delay their liquidity. Although the Borland deal offers higher potential value, the timeframe for returns is too long for investors. The management team and founders, however, prefer the Borland deal, as their earlier efforts have yielded a novel compound for bladder cancer, and they believe that developing a series of compounds can create greater long-term value.

The board engaged in intense discussions over which transaction to pursue. Both sides presented rational arguments from their own and each other’s perspectives, but the company’s governance framework superseded all considerations and had to be respected. Ultimately, investors holding a majority of voting rights steered the outcome of the deal. The company was acquired by Force Pharmaceuticals.

How did things unfold after Force acquired Oncotica? The lead compound failed in Phase III clinical trials due to a series of serious adverse reactions. From the venture capitalists’ perspective, the investment was neither a complete success nor a total loss. After cumulative investments totaling $20 million, they still achieved a return of $65 million despite the compound’s failure. This fell short of the five- or tenfold returns they had originally anticipated had the compound succeeded. Nevertheless, the founders ultimately received cash payouts and were satisfied with the outcome.

Finally, Davis led some of the founders in negotiations with Force Pharmaceuticals to license/acquire previously discovered novel compounds for bladder cancer and established a new company to develop these bladder cancer compounds. This time, they will leverage greater experience and a higher success rate to achieve the translation from research to clinical application.

20Conclusion

In fact, by this point, it is not difficult to see that the tasks required at each stage of the journey from 0 to 99 are hardly mysterious. In a model approximating a perfectly competitive market, every stakeholder engaged at each stage should have established protocols to follow. At the Technology Transfer Office (TTO), there are forms to complete and structured interviews to undergo; when submitting documents to the FDA, there are dedicated officers and corresponding channels; and after cashing out, professional accountants are indispensable for handling tax filings. However, the dilemmas in real-world models often arise from missing links in the chain and participants’ irrational decision-making.