China's $30 Billion Heavy-Ion/Proton Therapy Market: High Barriers to Deployment for the World's Most Expensive Medical Device

APACTRON

Proton Therapy Equipment R&D and Manufacturer

Driven by policy, the Chinese medical device market is undergoing earth-shaking changes: on one front, volume-based procurement has shrunk the multi-billion-yuan coronary stent market down to a scale of billions; on the other,Planning for the Configuration of 41 Heavy Ion and Proton Radiotherapy Systems Creates a New Multi-Billion Market.

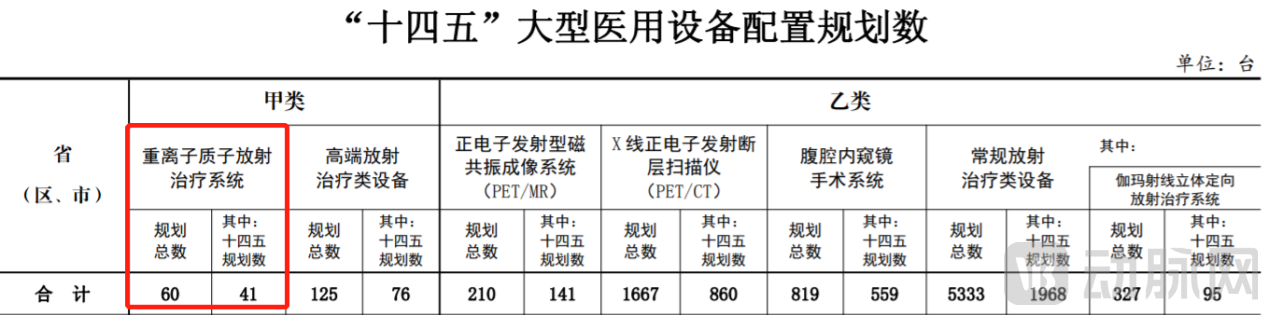

Recently, the "14th Five-Year Plan for the Allocation of Large Medical Equipment" released by the National Health Commission pointed out: During the "14th Five-Year Plan" period, a total of 3,645 large medical equipment units are planned to be allocated nationwide, including 117 Class A and 3,528 Class B units. Among the Class AHeavy Ion and Proton Radiotherapy System41 units are planned. As of now, the total number of planned heavy ion and proton radiotherapy systems stands at 60.

Previously, the National Health Commission planned to allocate 10 proton radiotherapy systems in 2018 and adjusted the plan to 16 units in 2020. The gradual increase in the planned allocation indicates that the state is placing growing emphasis on heavy ion and proton therapy equipment.

It is reported that the price of a proton radiotherapy system amounts to hundreds of millions of yuan, while heavy ion and proton radiotherapy systems are even more expensive. For instance, the total planned investment for the Proton Center at the Shenzhen Hospital of the Cancer Hospital, Chinese Academy of Medical Sciences, is approximately RMB 1.648 billion, of whichInvestment in Proton Therapy Equipment and Associated Medical Devices Amounts to RMB 860 Million; introduced by Shanghai Proton and Heavy Ion Hospital from Siemens, GermanyProton and Heavy Ion Equipment Costs 1.3 Billion Yuan。

Based on a single unit priced at RMB 800 million, the 14th Five-Year Plan'sThe 41 heavy-ion and proton radiotherapy systems can reach a value of RMB 32.8 billion.

In fact, the deployment of heavy ion and proton radiotherapy systems involves numerous aspects, including customized construction, installation and commissioning, personnel training, and operation and maintenance, each of which entails substantial costs. For instance, the annual maintenance cost for the proton therapy system introduced by Shandong Zibo Wanjie Cancer Hospital ranges from RMB 6 million to RMB 10 million.

From an industry perspective, how will this plan affect the market for heavy ion and proton therapy equipment? Which companies will capture shares of this multi-billion yuan market? How long will it take to move from planning to implementation?

Liu Cixin, the author of The Three-Body Problem, might never have imagined that protons traveling at near-light speeds would not lock down Earth’s technological development, but rather help humanity conquer tumors.

To understand heavy ion and proton radiotherapy systems, one must begin with radiotherapy (RT).

Radiotherapy refers to the use of radiation beams with different properties to destroy lesions (typically tumor cells). Currently, radiation beams used in clinical practice are categorized into photon beams and particle beams. Photon beams include X-rays and gamma rays, while particle beams include neutron beams, proton beams, and heavy ion beams.

Among these, proton radiotherapy systems, heavy ion radiotherapy systems, and proton-heavy ion radiotherapy systems are internationally recognized as cutting-edge radiotherapy technologies, offering clinical advantages such as high cure rates, superior precision, broad indications, and minimal side effects.

Proton Radiotherapy System (Proton Therapy): The principle involves accelerating protons to approximately 70% of the speed of light, enabling them to rapidly penetrate the body and destroy tumors. Studies have shown that, compared with conventional X-ray therapy, proton therapy reduces the relative risk of severe side effects within 90 days post-treatment by two-thirds.

During treatment, the proton beam does not release energy before reaching the tumor; it releases energy instantaneously upon reaching the tumor and stops releasing energy after passing through it (i.e., the controlled energy almost exclusively kills tumor cells without damaging other cells). Leveraging this characteristic,Proton radiotherapy can maximize the killing of tumor cells without damaging the normal tissues surrounding the tumor.。

Heavy-ion radiotherapy systems operate on principles similar to proton therapy; however, they deliver higher energy during treatment, theoretically resulting in greater tumoricidal efficacy than proton therapy. Data released by the Shanghai Proton and Heavy Ion Center in May 2023 indicated that for early-stage small cell lung cancer or locally advanced non-small cell lung cancer treated with heavy-ion radiotherapy alone, the five-year survival rates were superior to those achieved with proton radiotherapy in the United States.

Proton and Heavy Ion Therapy SystemThe proton and heavy ion therapy system combines proton radiotherapy and heavy ion radiotherapy, capable of separately delivering proton and heavy ion beams to treat tumors throughout the body. Due to its minimal damage to healthy tissues, this system is suitable for elderly patients, individuals who are not candidates for surgery, and those with compromised cardiopulmonary function.

Currently, constrained by factors such as cost and technology, the majority of heavy ion and proton radiotherapy systems available on the market are proton radiotherapy systems.

From the perspective of patient needs, according to statistics from the International Agency for Research on Cancer (IARC) of the World Health Organization, there were 19.29 million new cancer cases and 9.96 million cancer deaths worldwide in 2020. Among these, China reported 4.57 million new cancer cases and 3 million cancer deaths, ranking first globally in both the number of new cancer cases and cancer-related deaths.

Given the severity of cancer and the large patient population, the market size of tumor radiotherapy in China is expected to grow from RMB 51.7 billion in 2021 to RMB 88.0 billion in 2025. Among them, researchers believe that:If cost were not an issue, proton/heavy ion therapy would be the preferred treatment option for most patients with localized tumors.。

In fact, proton and heavy ion therapy is indeed being increasingly adopted by patients. According to data released by the Particle Therapy Co-Operative Group (PTCOG), by the end of 2022, more than 360,000 patients worldwide had received particle therapy, an increase of 35,000 cases compared to 2021. Among these, 312,000 patients received proton therapy, accounting for 86.6% of the total, representing an increase of 32,000 cases from 2021; 46,800 patients received carbon ion therapy, and approximately 3,500 patients received other types of particle therapy.

From the perspectives of bottleneck technologies, clinical needs, and the high-end medical equipment market, it is imperative for China to secure a strategic foothold in the deployment of heavy ion and proton radiotherapy systems.

To date, only a few countries, including China, Germany, Belgium, the United States, and Japan, have mastered proton and heavy ion technology. Relevant companies include IBA, Varian, Hitachi, Mitsubishi, Siemens, Sumitomo Heavy Industries, and Maisheng. Among them, the three giants—IBA, Varian, and Hitachi—account for nearly 80% of the global market share.

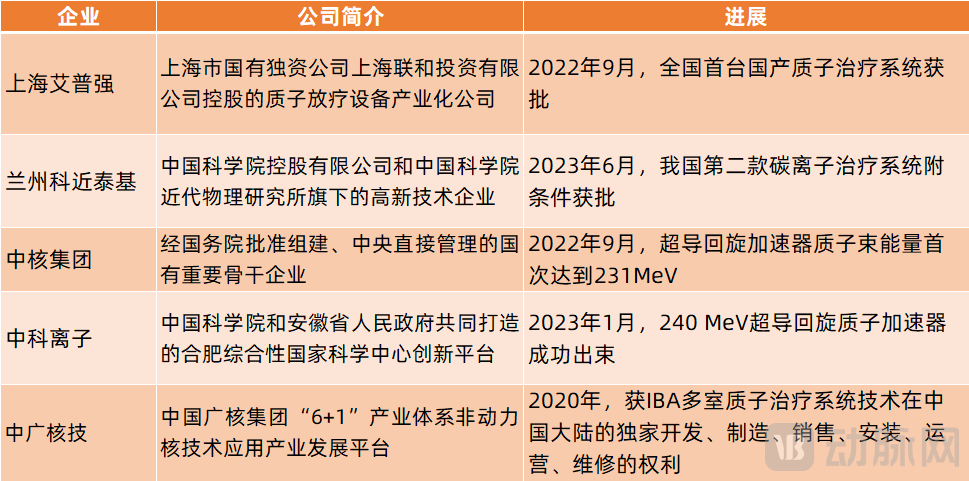

Although the global market is monopolized by three major players, several other manufacturers are gradually making breakthroughs. In particular, Chinese enterprises such as Shanghai APACTRON, Lanzhou Kejin Taiji Co., Ltd., CGN Nuclear Technology Development Co., Ltd., China National Nuclear Corporation (CNNC), and Hefei Branch ion medical technology and equipment Co.,Ltd. have all achieved significant breakthroughs in the past two years.

Notably, the first domestically developed proton therapy system, jointly researched and developed by Shanghai APACTRON, the Shanghai Institute of Applied Physics of the Chinese Academy of Sciences (CAS), the Shanghai Advanced Research Institute of CAS, and Ruijin Hospital, was approved for market launch in September 2022; the carbon ion therapy system independently developed by Lanzhou Kejin Taiji received conditional approval in June 2023; the proton beam energy of the superconducting cyclotron developed by China National Nuclear Corporation (CNNC) first reached 231 MeV in September 2022; the 240 MeV superconducting cyclotron proton accelerator developed by Hefei Branch Ion Medical Technology and Equipment Co., Ltd. successfully achieved beam extraction in January 2023, and its superconducting proton radiotherapy system cyclotron was successfully hoisted into place in May 2023……

In terms of technological breakthroughs, APACTRON’s independently developed proton therapy system has overcome multiple core technical challenges, securing 55 invention patents and 18 utility model patents. The superconducting cyclotron developed by China National Nuclear Corporation (CNNC) is currently the isochronous superconducting cyclotron with the highest proton beam energy in China. Its successful beam extraction signifies that China has mastered the core technologies for miniaturized, high-dose-rate superconducting cyclotrons, entering the global first tier.

In terms of product performance, the proton therapy system developed by APACTRON offers overall functionality and performance comparable to imported counterparts, with stable and reliable operation; its localization is expected to further reduce equipment and healthcare costs. The carbon ion therapy system recently approved for Lanzhou Kejin Taiji Co., Ltd. has performance indicators that meet international standards. The 240 MeV superconducting cyclotron proton accelerator developed by Hefei Branch ion medical technology and equipment Co.,Ltd. achieves overall performance indicators at a leading international level, serving as a domestic alternative to similar imported equipment.

It is reported that mass production of the 240 MeV superconducting cyclotron proton accelerator by CAS Ion has been proceeding in an orderly manner. The second accelerator is about to enter the beam commissioning phase, while the third is currently under manufacturing.

Overall, China's proton/heavy ion equipment has reached or approached the international leading level in terms of products and technology.

Furthermore, compared with the three industry giants—IBA, Varian, and Hitachi—domestic proton/heavy ion equipment manufacturers also benefit from localization advantages and policy support. Previously, the “Guiding Opinions on Promoting the Healthy Development of the Pharmaceutical Industry,” issued by the General Office of the State Council, explicitly stated that where domestically produced drugs and medical devices meet requirements, government procurement projects shall, in principle, procure domestic products, thereby gradually raising the configuration level of domestically produced equipment in public medical institutions.

Against this backdrop, the National Health Commission has planned for 41 heavy ion and proton radiotherapy systems.Domestic enterprises are poised to gain a competitive edge in the Chinese market by leveraging advantages in product quality, pricing, localization, domestic manufacturing, and procurement policies. It is projected that the majority of planned proton/heavy ion therapy systems will be sourced from domestic manufacturers.。

Proton and heavy ion therapies, regarded as "miracle weapons" in tumor treatment, are scarce medical resources worldwide. As of March 2023, there were only 115 proton/heavy ion therapy centers globally.

In China, according to incomplete statistics, there are currently 10 proton/heavy ion therapy centers, with approximately 27 additional proton/heavy ion centers planned or under construction.

(Open for BusinessProton/Heavy Ion Center)

The 41 proton/heavy ion devices configured in this plan are allocated with quotas in various provinces across China, indicating a vast market and broad prospects. However, judging from historical cases,These planned projects are constrained by challenges such as funding, timelines, technology, and personnel, making it difficult to implement them in the short term.。

The construction of a proton/heavy ion center is divided into four phases: administrative approval, construction, equipment installation and commissioning, and clinical operations. Each phase presents exceptionally high levels of difficulty and stringent requirements.

For example, in terms of administrative approval, proton/heavy ion centers are required to obtain a Medical Device Registration Certificate, a License for the Allocation of Large-Scale Medical Equipment, a Radiation Safety License, and a Radioactive Diagnosis and Treatment License. Meanwhile, the Allocation License imposes specific requirements on hospital classification, patient admission volume, talent teams, and equipment conditions. Hospitals must conduct self-assessments in accordance with relevant regulations before initiating the construction of proton and heavy ion facilities, and may only launch the project upon meeting these criteria.

As of now, the total number of planned heavy ion and proton radiotherapy systems in China is only 60, accounting for an extremely low proportion of hospitals. However, some hospitals are constructing (or planning to construct) proton/heavy ion centers without having obtained configuration permits.

In addition, the establishment of proton and heavy ion therapy centers imposes exceptionally high requirements in terms of funding, construction, and talent.

Proton/heavy ion centers require substantial capital investment and are often prioritized as key investment projects promoted by various provinces.

For example, the Proton and Heavy Ion Tumor Treatment Center at Heyou International Hospital has a total investment of nearly RMB 3 billion; the Proton Center at the Shenzhen Hospital of the Cancer Hospital, Chinese Academy of Medical Sciences, has a planned total investment of approximately RMB 1.648 billion; the Proton Center at Shandong Cancer Hospital has a total investment of RMB 1.47 billion; the Hefei Ion Medical Center project is being constructed in two phases, with Phase I covering an area of 70 mu and representing an investment of approximately RMB 1.27 billion; the Proton Center at Xi’an International Medical Center Hospital has a total investment of RMB 1 billion; the Proton Therapy Center project at Tianjin Medical University Cancer Institute and Hospital has a total investment of RMB 980 million; and the Proton Therapy Center at Sichuan Cancer Hospital has a total investment of approximately RMB 820 million.

Due to the enormous capital investment required, some investors may cancel their projects in the later stages after announcing plans to build proton/heavy ion centers. For example, in February 2022, Phoenix Shares announced that Jiangsu Phoenix Cancer Hospital was scheduled for deregistration in the near future. Previously, Phoenix Group, the Nanjing Pukou New City Development and Construction Management Committee, and Jiangsu Province Cancer Hospital had signed a framework agreement to jointly establish the Jiangsu Provincial Proton and Heavy Ion Hospital. In fact, although Jiangsu Phoenix Cancer Hospital announced its launch in 2015, it never entered the construction phase. Currently, this project has been completely deregistered.

Not only are the upfront construction costs enormous, but the subsequent operational and maintenance expenses are also extremely high. For instance, media reports have previously indicated that the annual maintenance cost for the Proton Therapy Center at Shandong Zibo Wanjie Cancer Hospital ranges from RMB 6 million to RMB 10 million.

Given the high upfront capital costs and substantial ongoing operational expenses, the cost of proton/heavy ion therapy is naturally “not to be underestimated.” It is reported that a single course of treatment at the Shanghai Proton and Heavy Ion Center costs approximately RMB 278,000. When hospitalization fees and other diagnostic and therapeutic procedures are included, the total average cost amounts to around RMB 400,000.

The exceptionally high unit price means that the number of patients who can afford the treatment is limited. According to data released by the Shanghai Proton and Heavy Ion Center, as of May 8, 2023, the hospital had been in operation for eight years, with a cumulative total of 5,648 discharged patients treated and an average annual growth rate of 20%. In comparison, similar international institutions in Japan, Germany, and other countries took 9–15 years to reach a treatment volume of 5,000 cases.

High capital costs, operational and maintenance expenses, treatment fees, and limitations on patient volume have led many proton/heavy ion centers to operate at a loss. According to Kaiser Health News, one-third of the 27 proton therapy centers in the United States were losing money in 2018.

The construction period for proton/heavy ion centers is extremely long.

For example, the Shanghai Proton and Heavy Ion Center began its preparatory work in the 1990s, started construction in 2003, and did not commence operations until 2015; the Wuwei Heavy Ion Tumor Treatment Center project initiated preliminary preparations in 2012, broke ground in April 2013, and was not completed and put into operation, officially opening for clinical services, until May 2023.

Based on an analysis of previous construction experience, new proton/heavy ion therapy facility projects require 5–8 years from initiation to formal operation. Specifically, infrastructure construction takes more than 24 months, environmental acceptance takes more than 48 months, and the procurement, installation, and commissioning of proton equipment take 36–72 months, after which clinical operations can commence.

It is worth noting that proton/heavy ion centers differ from conventional hospitals right from the architectural design phase. While conventional hospitals typically follow a process of designing the building first and then procuring medical equipment, proton/heavy ion hospitals must procure the proton/heavy ion equipment first, and then design the layout and structure of the hospital building based on the selected proton/heavy ion therapy system.

Furthermore, proton/heavy ion therapy systems from different manufacturers and of different models vary significantly in structural layout and architectural requirements. Therefore, during the design phase, it is essential to fully consider the equipment parameters and architectural specifications provided by the vendor, and to implement customized designs tailored to the specific equipment.

During the construction phase, proton/heavy ion equipment imposes extremely stringent requirements on the environment and building structure, necessitating “zero overall settlement, zero building vibration, zero structural cracks, zero blockages, and zero deviations.” For instance, due to the strong penetrating power of protons, cracks in the walls of the proton therapy area must not exceed 0.2 millimeters; the thickness of a single wall in the proton therapy area is more than 20 times that of conventional hospitals.

During the installation and commissioning phase, proton/heavy ion equipment poses significant challenges for lifting and installation due to its weight, which can exceed hundreds of tons. It is reported that the proton therapy system at the Hefei Ion Medical Center has a total weight of up to 280 tons, with the rotating gantry component alone weighing 220 tons. Furthermore, the procurement of proton/heavy ion equipment marks the starting point of construction, as the facility must be custom-built according to the specifications of the ordered equipment. The entire process, from equipment procurement to lifting and installation, and finally to beam commissioning, typically takes 36 to 72 months, underscoring the complexity of installation and commissioning.

Proton/heavy ion equipment also features a “one device, one license” requirement; therefore, after installation and commissioning, each unit must undergo clinical trials before it can be commercialized and enter the clinical operation phase. These clinical trials also present challenges such as patient recruitment and prolonged duration.

Furthermore, the complex structure of proton/heavy-ion equipment means that factors such as gravity, temperature, and humidity can affect components and interfere with the delivery of radiation beams. This necessitates routine maintenance by medical physicists to promptly address equipment malfunctions. However, there is a severe shortage of qualified medical physicists in China. According to statistics, in 2020, only approximately 33,000 individuals were engaged in radiotherapy work in mainland China, including 18,966 radiation oncologists, 4,475 medical physicists, and 9,537 radiation therapists. This scarcity of talent has also constrained the rapid expansion of proton/heavy-ion therapy centers.

Based on the above analysis, VCBeat believesAlthough proton/heavy ion equipment has been planned in batches, it will not be rapidly deployed in the short term. The proton/heavy ion equipment under planning is expected to be primarily sourced from domestically produced devices.。