Global Biopharmaceutical Investment and Financing Report H1 2023: Signs of Recovery Amid Ongoing Chill

1. In the first half of 2023, both the number of global financing deals and the total amount raised increased compared to the same period last year, whereas domestic investment and financing activities in China declined in both deal count and total value, reflecting continued caution in the capital market. Globally, early- to mid-stage investments remained dominant.

II. Small molecules, large molecules, and the CXO sector remain the primary arenas for investment and financing; nucleic acid drugs, cell therapy, and gene therapy continue to be hot sectors, while radiopharmaceuticals and microbiome-based therapies have emerged as prominent new fronts.

III. Biopharmaceutical investment and financing in China are primarily concentrated in the Yangtze River Delta and Pearl River Delta regions. The trend of government funding supporting industrial recovery has strengthened, with a significant increase in the number of investments made by government-guided funds and state-owned capital-backed funds in Q2, while market-oriented funds remain cautious in their investment activities.

IV. Two Chinese Companies Strongly Enter the Top 10 in Global Biopharma Financing for Q2 2023; Global Investment and Financing Show a Diversified Distribution, with Stable and Mature Sectors Remaining the Focus of Domestic Capital.

H1 2022–H1 2023: Trends in Global Biopharmaceutical Investment and Financing

1.1 In H1 2023, both the number of global financing events and the total amount of financing increased year-on-year, while the domestic market remained in a "winter."

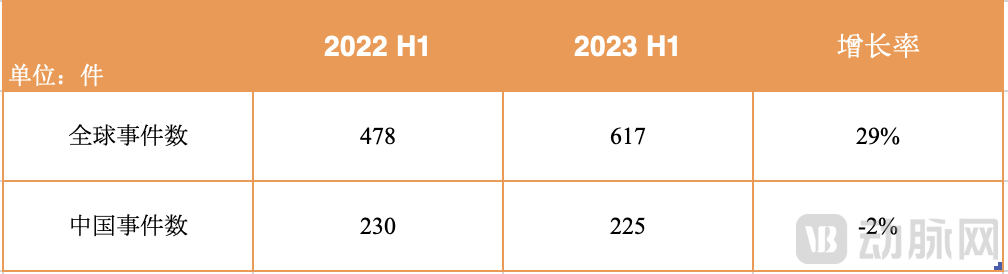

▲ Comparison of the Number of Financing Events in H1 2022 and H1 2023, Data Source: Arterial Orange

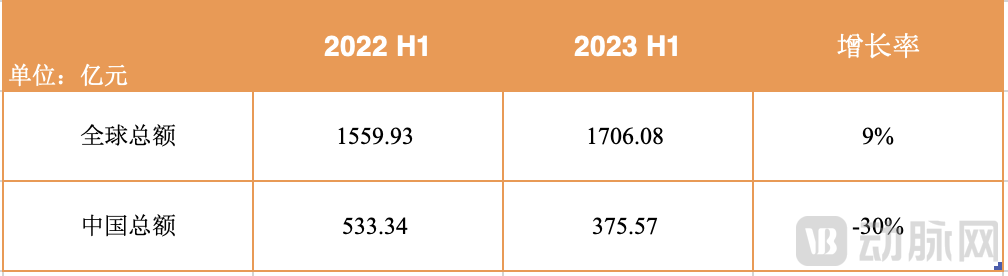

▲ Comparison of Total Financing Amounts in H1 2022 and H1 2023; Data Source: Artery Orange

In the first half of 2023, there were a total of 617 global financing events, with a total amount of RMB 170.608 billion. Among these, China had 225 financing events, totaling RMB 37.557 billion.

Global Financing and Investment Events in H1 2023 Compared to the Same Period Last YearUp 29%, the total global financing compared to the same period last year9% growth, global capital markets have been more active this year than last, with total financing amounts increasing, sending positive signals to the biopharmaceutical industry and indicating a warming trend in capital markets.

China’s investment and financing events in H1 2023 compared with the same period last yearReduced by 5 units,Remained basically flat, but the total investment and financing amount compared to the same period last yearReduce by 30%,Contrary to the global overall trend. It is evident that the fundamentals of China’s capital market remain sluggish, with investment institutions maintaining a cautious approach to deploying capital; the “capital winter” in the biopharmaceutical industry persists.

1.2 Global financing events and total funding amount in Q2 2023 increased significantly compared to Q1, while domestic investment slowly warmed up

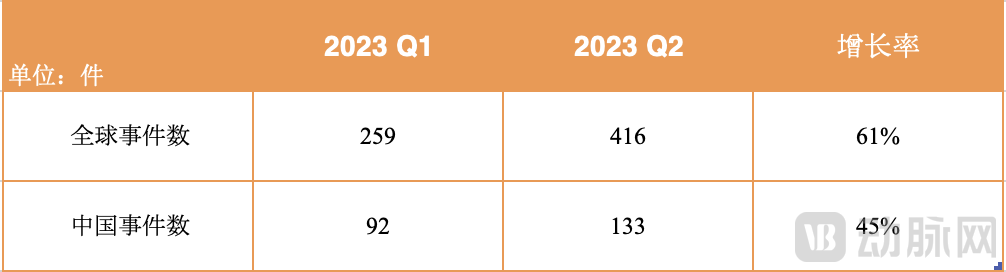

▲ Comparison of the Number of Financing Events in Q1 2023 and Q2 2023, Data Source: VCBeat Orange

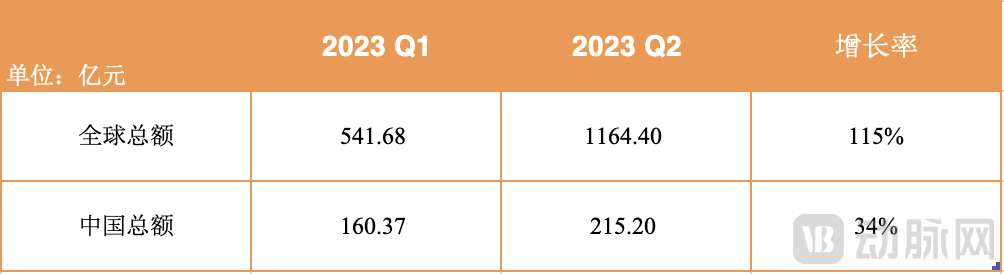

▲ Comparison of Total Financing Amounts in Q1 2023 and Q2 2023, Data Source: Arterial Orange

If only the data for Q2 2023 is considered, there were a total of 133 financing events in China, with a total amount of RMB 21.52 billion. The number of financing events and the total financing amount in ChinaQ2 saw respective increases of 61% and 34% compared to Q1.

From this perspective, compared to Q1,China's Biopharmaceutical Industry Showed Signs of Recovery in Q2 2023, the challenge of “difficult financing” has been somewhat alleviated, but the mindset of domestic investment institutions remainsExercise caution.

1.3 Capital Markets Favor Early-Stage Investment and Diversified Financing Models, as Companies Strive to Break the Ice

▲ Data source: Artery Orange

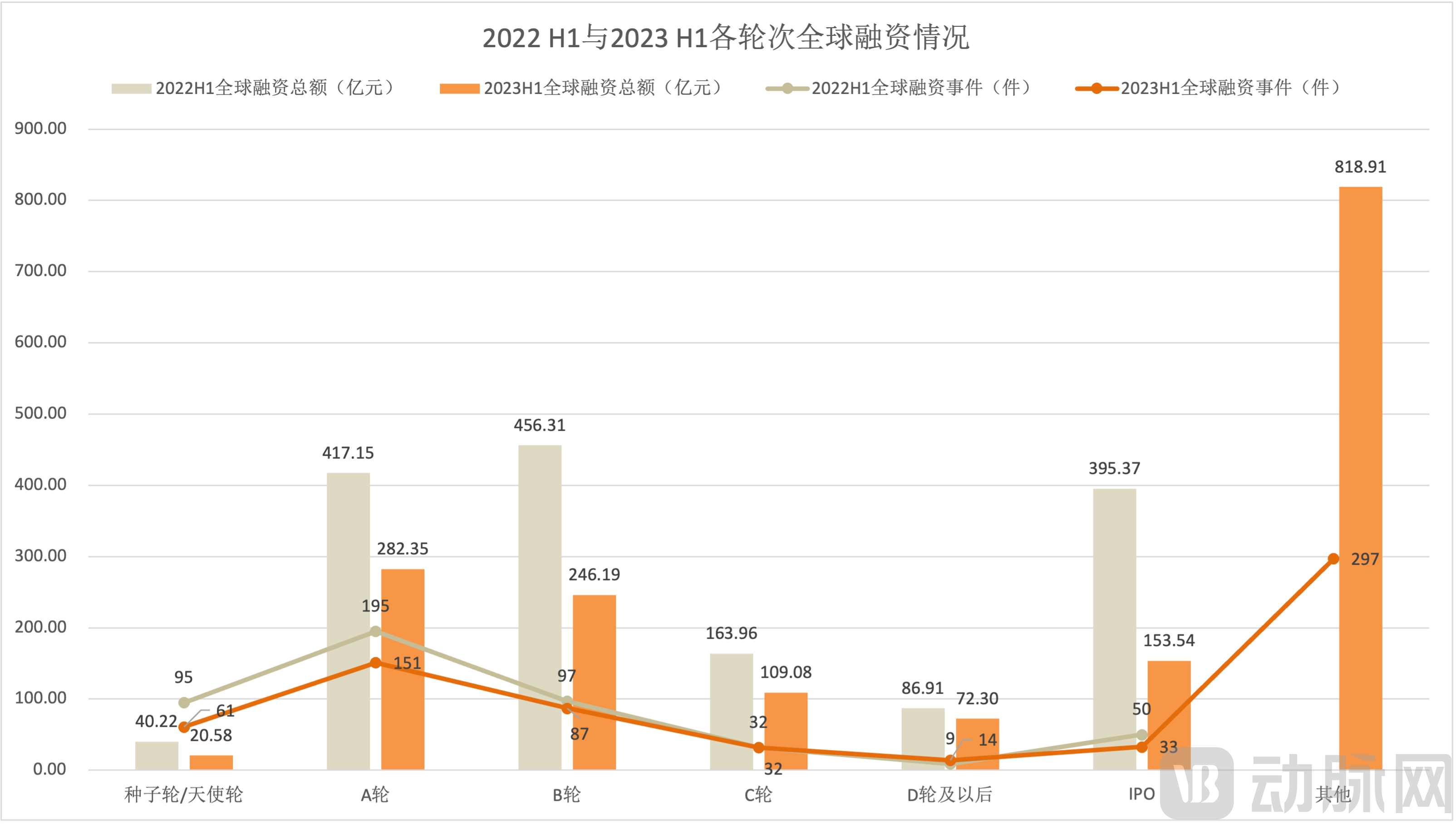

Global financing events in the first half of 2023 were dominated by Series A, Series B, and other rounds. The “other” category includes undisclosed rounds, strategic financing, equity financing, debt financing, and donations/crowdfunding, indicating thatGlobal capital markets show a stronger preference for early-stage investments and more diverse financing and investment models.

In H1 2023, global investment and financing amounts across all rounds were lower than those in H1 2022; however, the total amount for other rounds reached RMB 81.891 billion, accounting for nearly half of the global total.

▲ Data source: VCBeat Orange

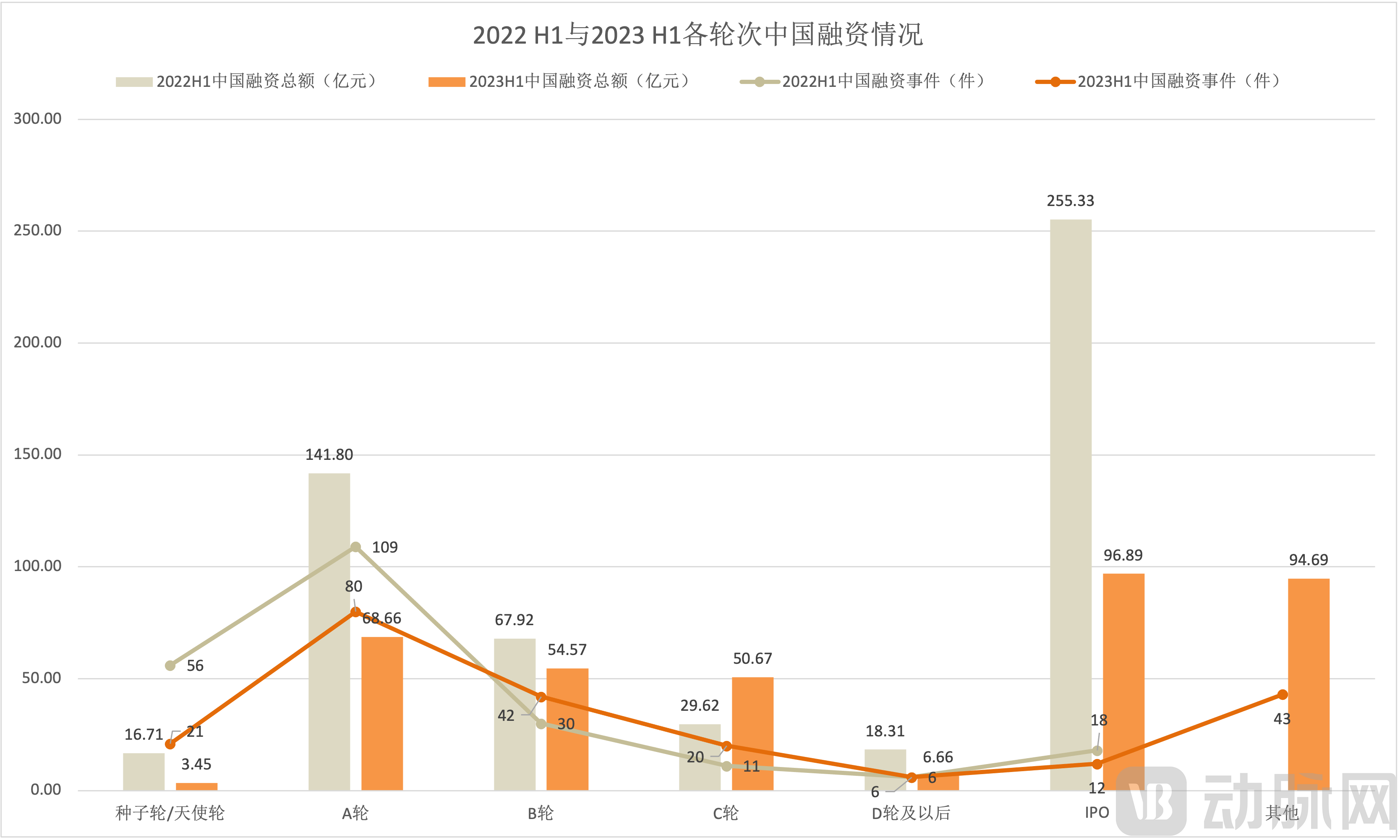

In China, financing rounds are predominantly Series A, Series B, and other stages, a trend that aligns with the global overall trend.

Notably,Total IPO financing in the first half of 2023 amounted to only 38% of that in the first half of 2022., this precipitous decline is a direct reflection of the cooling Chinese biopharmaceutical market.

However, in the first half of 2023, the total financing amount from other rounds—including undisclosed rounds, strategic financing, equity financing, debt financing, and donations/crowdfunding—reached RMB 9.469 billion. Companies began to adopt more diverse financing methods to address funding difficulties, which has become a trend in China’s biopharmaceutical industry.A Portrait of Striving to Break the Ice Amidst the Capital Winter。

Hot Investment and Financing Sectors in the Global Biopharmaceutical Industry, H1 2023

2.1 Small Molecules and Macromolecules Remain the Primary Focus, with Radiopharmaceuticals and Microbiome Therapies Showing Strong Performance

▲ Data source: Artery Orange

▲ Data source: VCBeat Orange

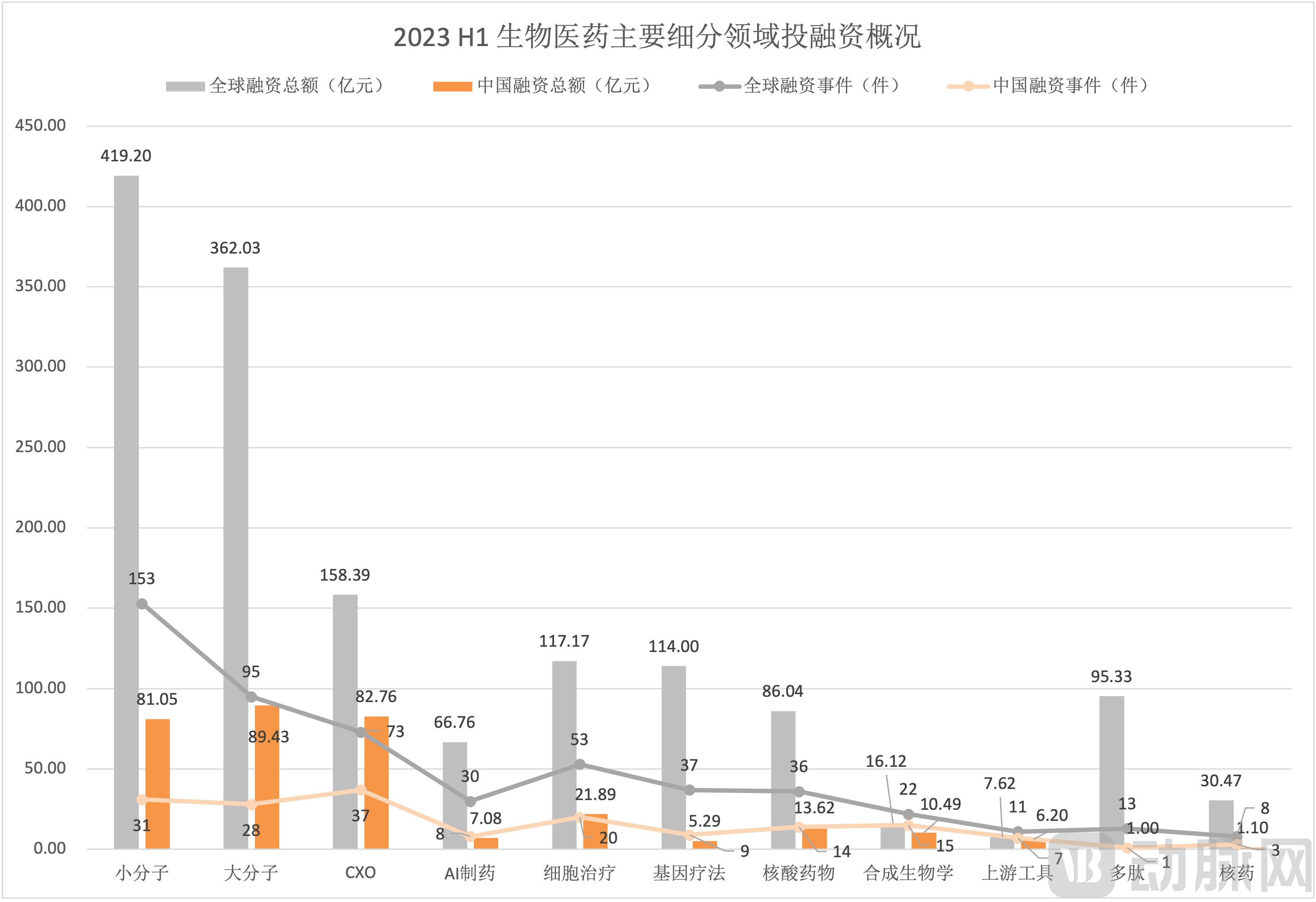

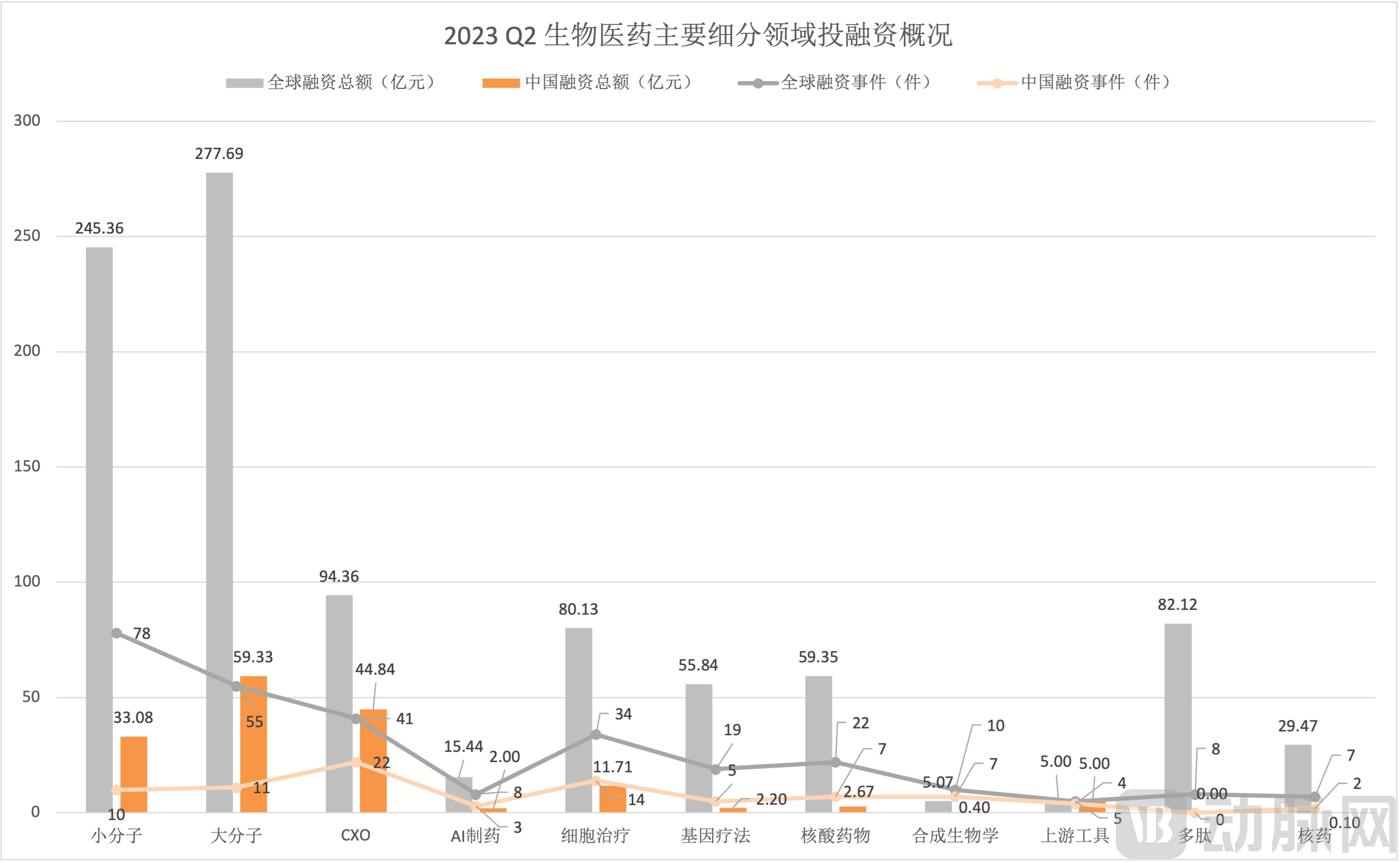

Whether examining the data for Q2 2023 alone or the overall data for H1 2023, small molecules and large molecules remain the primary focus of global and domestic investment and financing.

From a global perspective, financing amounts in the CXO, cell therapy, gene therapy, nucleic acid drug, and peptide sectors closely follow, while AI-driven drug discovery continues to maintain strong investor interest.

In China, CXO is the most sought-after investment sector after small-molecule and large-molecule therapeutics.

In addition, niche segments have demonstrated outstanding performance.Total Financing in the Nuclear Medicine Sector Reached RMB 3.047 Billion in the First Half of 2023, with seven financing events in Q2 alone, totaling RMB 2.947 billion. In contrast to the lull in Q1, the radiopharmaceutical sector ushered in a springtime in Q2. In China, Nuoyu Pharmaceutical and Zhongke Shuaitian Pharmaceutical were the only two radiopharmaceutical companies that secured investments in the first half of 2023.

Apart from the radiopharmaceutical sector,Microbiome Therapies Are Gaining Momentum. Following the FDA’s approval of REBYOTA, the first microbiome-based therapy, on February 14 this year, the momentum behind microbiome therapies was significantly evident in Q2,A total of 9 investment and financing events occurred, with a total amount reaching RMB 3.005 billion.However, no domestic companies have yet emerged as leaders in this sector, making its future prospects worth anticipating.

2.2 In the CXO sector, Series C and IPO financing events are on the rise

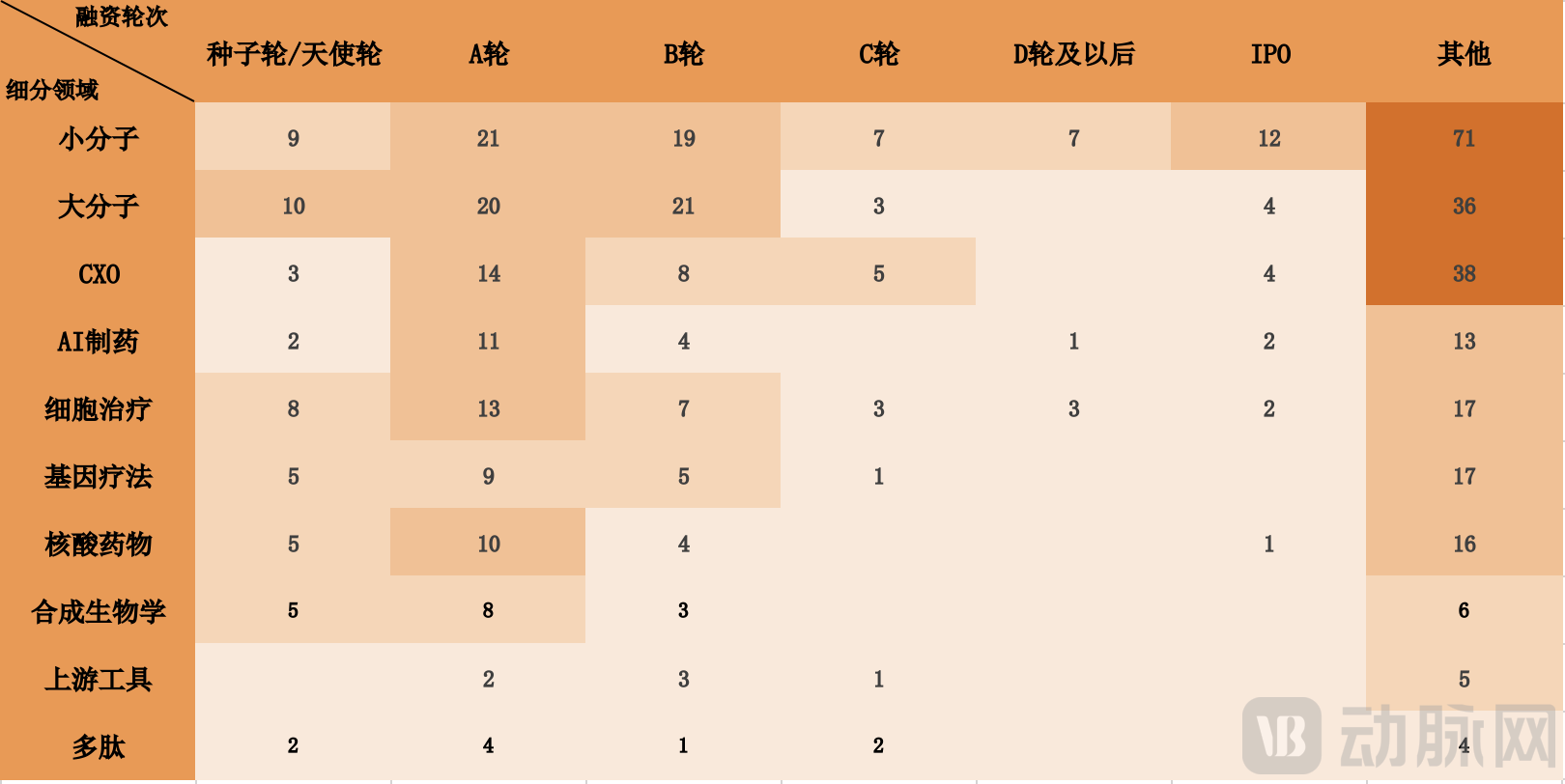

▲ Distribution of Financing Rounds in Major Global Sub-sectors, H1 2023. Data source: VCBeat Orange

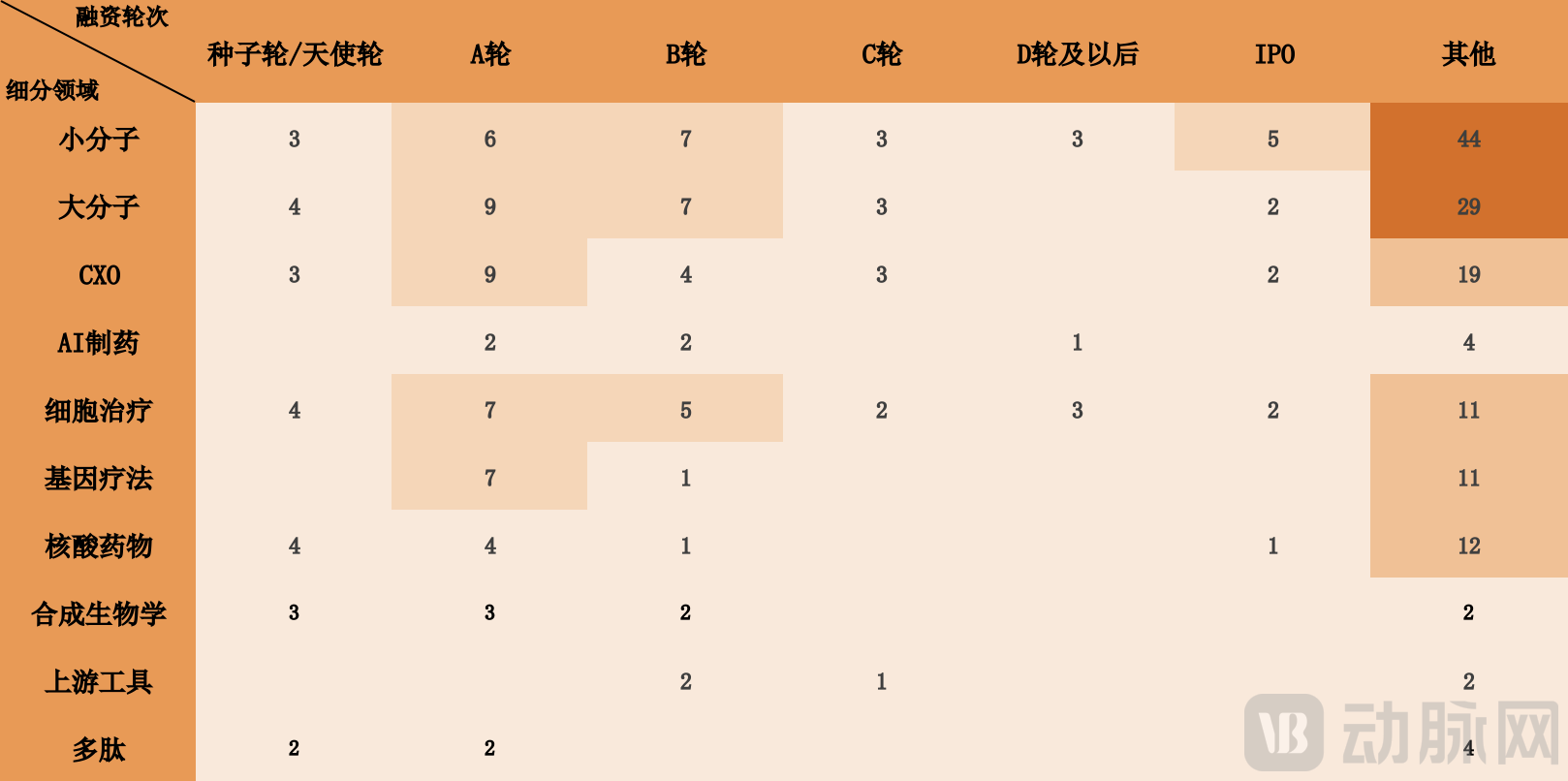

▲ Distribution of Global Major Sub-sector Financing Rounds in Q2 2023, Data Source: VCBeat

From the perspective of financing rounds, combining data from Q1 and Q2 of 2023, the small molecule sector demonstrated outstanding performance across all investment and financing stages. In contrast, large molecules, cell therapy, gene therapy, and nucleic acid drugs were predominantly focused on early-stage investments. In the fields of AI drug discovery and synthetic biology, investment rounds were concentrated mainly in Series A, while financing activities in the CXO sector began to shift toward later stages, with an increasing number of events occurring in Series C and IPO rounds.

Top Chinese Cities for Biopharma Investment and Financing in H1 2023

3.1 The Yangtze River Delta and the Pearl River Delta Remain Hotspots, with Government-Guided Funds Emerging as a Highlight

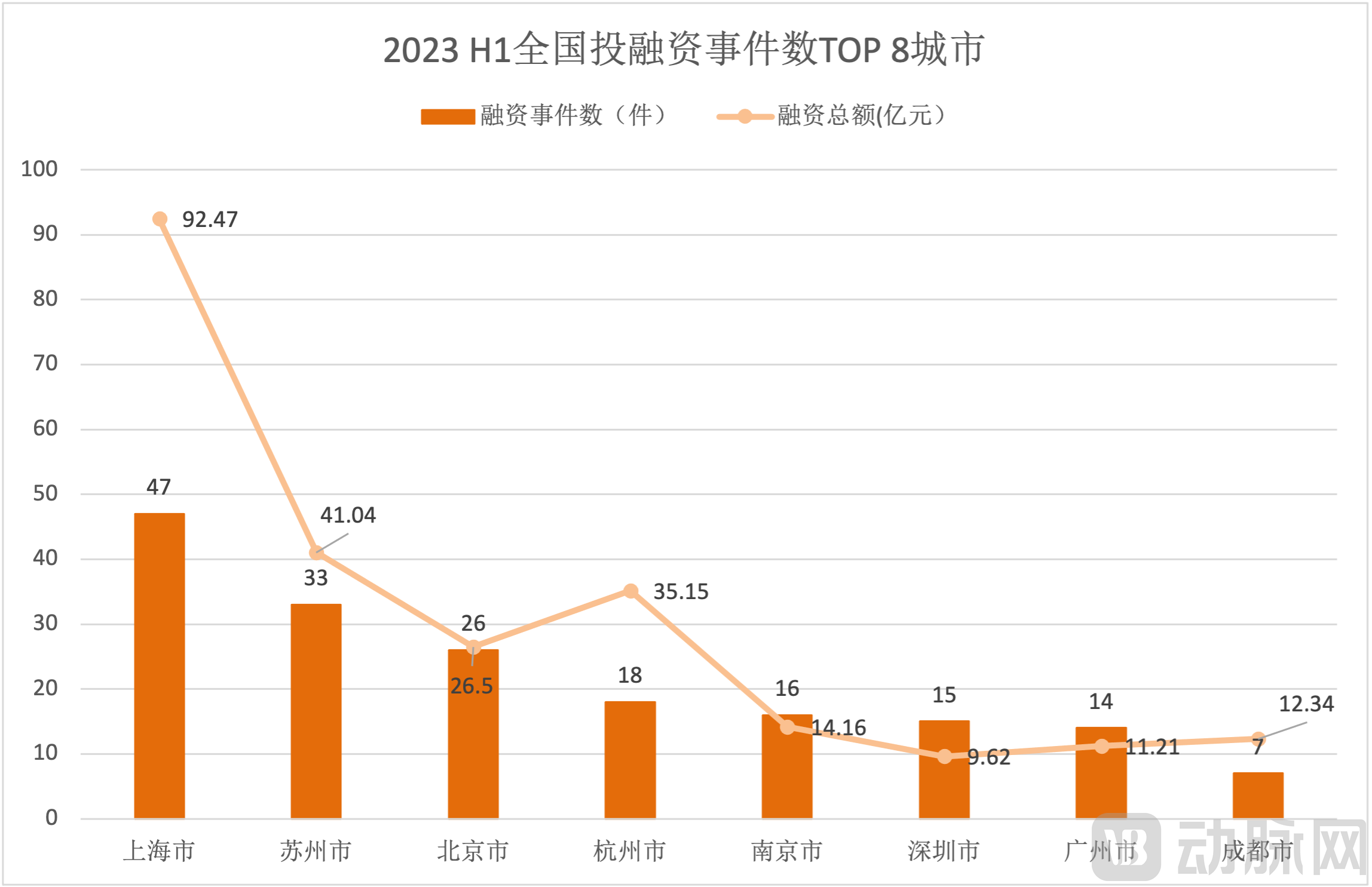

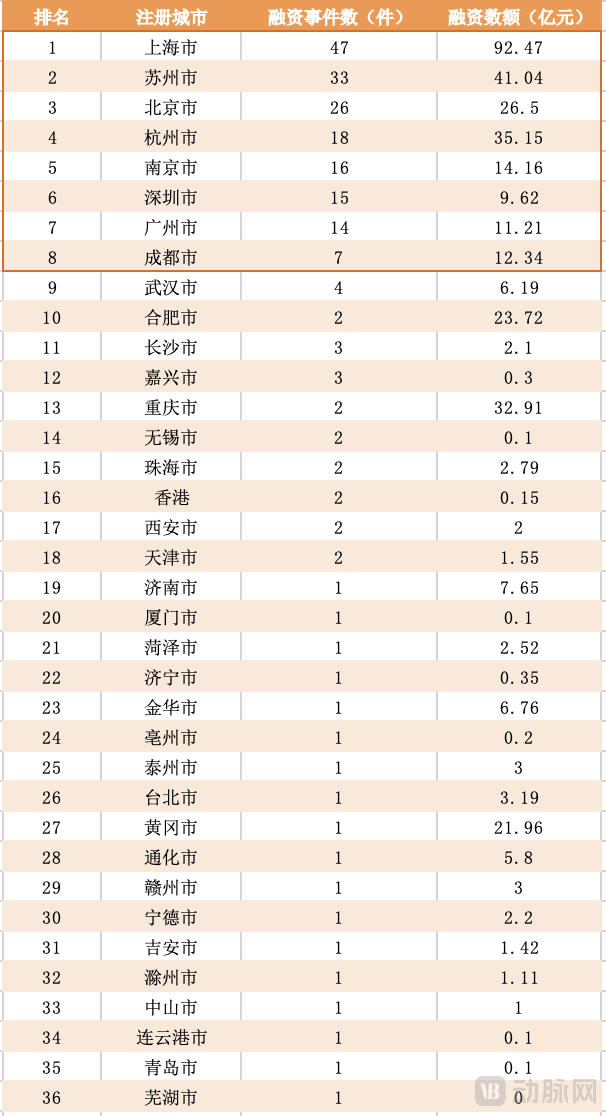

▲ Distribution of Financing Across Chinese Cities in H1 2023, Data Source: Artery Orange

In terms of geographic distribution, financing and investment activities in the first half of 2023 (H1 2023) were primarily concentrated in the Yangtze River Delta region. Shanghai led with a total of 47 financing and investment deals, amounting to RMB 9.247 billion. WuXi Biologics emerged as the company securing the largest single financing round in Shanghai, raising RMB 1.581 billion.Suzhou surpassed Beijing in the first half of the year, ranking second., with both the number of financing events and the total investment amount exceeding those in Beijing; investments are primarily concentrated in the CXO and macromolecule sectors.

Guangzhou and Shenzhen, the core cities of the Pearl River Delta, have comparable numbers of investment and financing events. Guangzhou’s financing rounds tend to be at later stages, with a total of five Series C and Series D deals. In contrast, Shenzhen’s financing activities are skewed toward early stages, with Angel and Series A rounds accounting for 60% of the total, primarily concentrated in the fields of synthetic biology and cell therapy.

Compared with Q1,In Q2, there was a greater presence of government-guided funds and state-owned capital-backed funds among investment and financing institutions.There were only 10 such funds in Q1, but the number grew to nearly 50 in Q2.Local Governments Inject Breakthrough Momentum into Investment and Financing for the Biopharmaceutical Industry, and even played a leading role in driving the industry’s recovery. Taking Guangzhou as an example, government-guided funds such as the Guangzhou Development District Industrial Fund, Guangzhou Yuexiu Industrial Fund, Guangzhou Industry Investment Group, and Guoju Venture Capital have essentially covered investment and financing activities across all major sectors in Guangzhou. Notably, the largest financing deal in Guangzhou during the second quarter was secured by Laigen Biologics, an innovator in TCR-T therapy development, whose Series B round received dual support from Guoju Venture Capital and Guangzhou Industry Investment Group.

Moreover, state-owned or government-guided funds such as SDIC Venture Capital, Zhongke Kechuang, Chengdu Tianfu International Bio-town Investment, and Zhejiang University Venture Capital are not limited to investing in local industries and enterprises; they are also highly active in other regions.

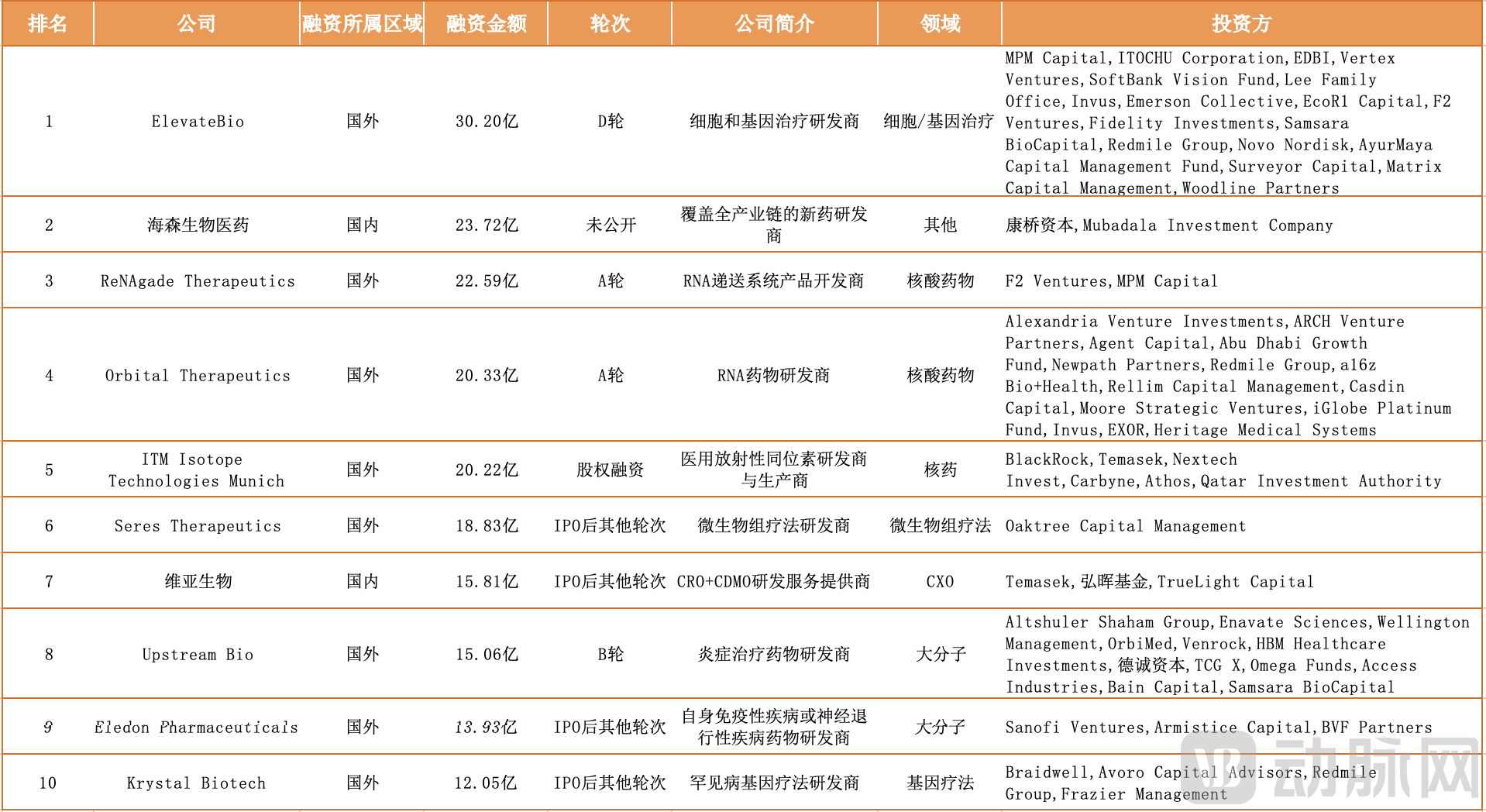

Top 10 Global Biopharma Companies by Q2 2023 Funding (Excluding IPOs))

4.1 Global Investment and Financing Exhibit a Diversified Distribution, with Domestic Enterprises Moving Toward Interdisciplinary Integration

▲ Overview of the Top 10 Companies by Global Biopharmaceutical Financing in Q2 2023; Data Source: VCBeat

Among the top 10 global companies in financing and investment, two are from China: Haisen Biopharma, with a total financing amount of RMB 2.372 billion, and Viva Biotech, with RMB 1.581 billion.

Furthermore, the ten companies operate in a diverse range of fields. Large-molecule and nucleic acid drug companies each account for two spots, while the remaining six companies operate in non-overlapping sectors. This indicates that capital is increasingly focusing on more specialized niches. Nuclear medicine and microbiome therapy have emerged as highly favored emerging sectors, distinguished by significant financing rounds.

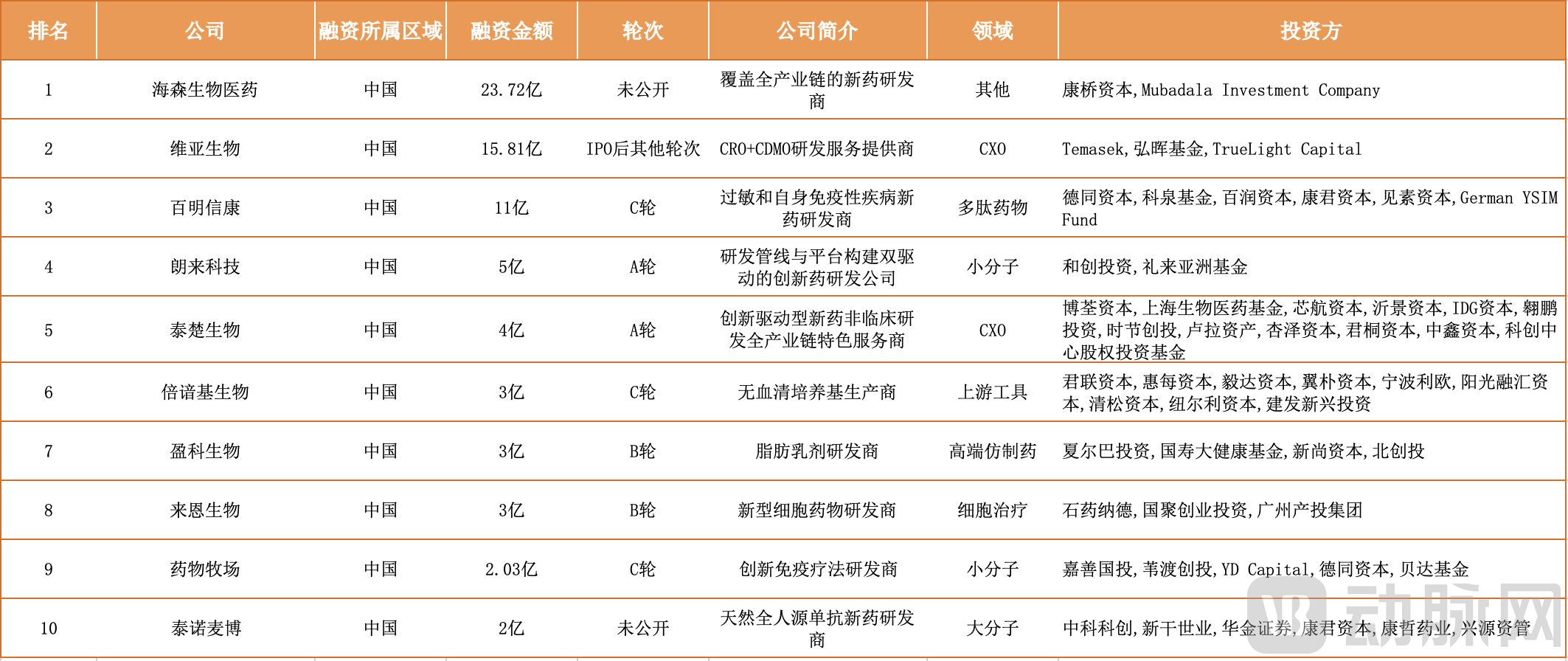

▲ Overview of the Top 10 Companies by Financing Amount in China’s Biopharmaceutical Sector in Q2 2023; Data Source: Artery Orange

An analysis of China’s top 10 companies in investment and financing reveals that, similar to global trends, the sectors in which these companies operate are beginning to show a diversified distribution. However, whether in CXO, large-molecule drugs, small-molecule drugs, peptides, upstream tools, generic drugs, or active pharmaceutical ingredients (APIs), these are all relatively mature sectors, and capital continues to prioritize stability.

Meanwhile, many domestic pharmaceutical companies can no longer be defined by a single therapeutic area; instead, an increasing number of enterprises are moving toward interdisciplinary integration.

Data Definition Rules:

To facilitate statistical analysis, we adhere to the following principles when processing investment and financing data:

1. The financing events covered in this report include those from the angel round to IPO, excluding private placements, mergers and acquisitions, and other similar transactions;

2. In this report, seed rounds, angel rounds, and seed-stage VC investments are consolidated into the “Seed/Angel Round” category; all Series A rounds are consolidated into “Series A”; all Series B rounds into “Series B”; all Series C rounds into “Series C”; and all Series D rounds together with Pre-IPO rounds are consolidated into “Series D and Beyond.” Other financing types include undisclosed rounds, strategic financing, equity financing, debt financing, and donations/crowdfunding.

2. All financing amounts are converted into RMB using the following unified exchange rates: 1 USD = 6.85 RMB, 1 HKD = 0.87 RMB, 1 EUR = 7.40 RMB, 1 CHF = 7.45 RMB, 1 GBP = 8.4 RMB, and 1 SEK = 0.66 RMB;

3. Standardize financing amounts in the millions, tens of millions, or hundreds of millions to 1 million, 10 million, or 100 million, respectively;

4. The data in this report is current as of June 30, 2023. Any data released after June 30, 2023, falls outside the scope of this report’s statistics and will be dynamically updated on the VCBeat Investment & Financing channel.