H1 2023 Global Healthcare Industry Capital Report: Deepening Divergence Across Sub-sectors and Increasingly Cautious Investment Decisions

# Core Viewpoints

I. Influenced by cautious investment trends and shrinking valuations, the number of companies voluntarily disclosing new financing amounts in the first half of 2023 decreased, with average financing falling short of previous periods, which to some extent impacted the total financing volume; more companies, driven by strategic considerations, prioritized stabilizing their operations or completing their business loops to ensure their competitiveness.

II. Intensified Divergence Across Sub-sectors in H1 2023: In the medical device and biopharmaceutical industries, capital continued to concentrate on high-valuation segments such as surgical robotics and cell and gene therapy (CGT), while most other sub-sectors experienced significant declines. The digital therapeutics sector remained sluggish due to unproven business models and the impact of bankruptcies among leading companies, whereas AIGC-powered healthcare emerged as a disruptive force driven by technological innovation, demonstrating strong short-term growth momentum.

III. The reform of the stock issuance registration-based system and price reductions from centralized procurement have raised the listing threshold for A-shares. The Beijing Stock Exchange’s introduction of equity incentives, differentiated voting rights structures, and a direct connection mechanism better aligns with the needs of small and medium-sized enterprises (SMEs). Meanwhile, policies such as the listing mechanism for “Specialized and Sophisticated Technology” enterprises and the “Dual Counter Model” have further boosted activity in the Hong Kong stock market.

IV. Star investment institutions are becoming increasingly cautious in their investment decisions, doubling down on mature projects while delving deeper into the early stages of healthcare.

V. China Surpasses the United States in Number of Financing Deals to Lead Globally, with Jiangsu Ranking First Domestically in Financing Activity.

VI. Top 10 Most-Funded Companies in H1 2022: U.S. Healthcare Service Providers Dominate the List, with Heisen Biopharmaceuticals as the Only Chinese Company Ranked.

I. Trends in Global Healthcare Industry Financing from 2012 to H1 2023

1.1 Market remains on the sidelines, with fewer companies willing to proactively disclose new funding rounds

In H1 2023, the global healthcare industry witnessed a total of 1,570 financing events, a year-on-year decrease of 18; the total financing amount reached USD 30.2 billion (approximately RMB 218.65 billion),Ranked third in history, with only a slight increase in the first half of 2020 (the impact of the black swan event of the COVID-19 pandemic hardly affected investment enthusiasm in the overseas primary healthcare market during the first half of 2020); however, compared to 2020, capital in H1 2023 was no longer concentrated.

In addition to the increasingly cautious investment trends, compared with the same period in previous years, the global healthcare industry enteredMature StageThe number of companies raising funds in later stages (Series D and beyond) has increased; however, due to cautious investment sentiment and shrinking valuations, fewer companies are willing to proactively disclose the amounts raised in new funding rounds, with average financing volumes falling below previous levels. This also indirectly indicates that for companies that have already established competitive barriers, their financing plans continue to proceed steadily.

1.2 Slower Financing Pace, Companies’ Next-Round Valuations in a “Sideways” State

In H1 2023, the total investment and financing in China's healthcare industry exceeded US$5.6 billion (approximately RMB 41.051 billion), a year-on-year decline of over 43%; the number of financing transactions reached 650, an increase of 27 compared to H1 2022.

It is worth noting that corporate financing slowed in the first half of 2023 (H1 2023): represented by growth-stage companies, most of which had already secured funding in previous years. In 2023, given that company valuations could not be lowered and the next round of financing failed to meet expectations, these companies chose to decelerate their fundraising pace.

In contrast, mature-stage companies in China, out of prudence, have mostly opted to quietly complete their new rounds of financing as planned while maintaining promotional efforts, and have chosen not to disclose specific funding amounts. Although the survival rate of companies significantly improves by Series C and subsequent rounds, due to pessimistic expectations, they prioritize strategies such as stabilizing operations and completing their business loops.

1.3 Cooling Rates Across Sectors Remain Unsynchronized; Industrial Demand Continues to Drive Investment

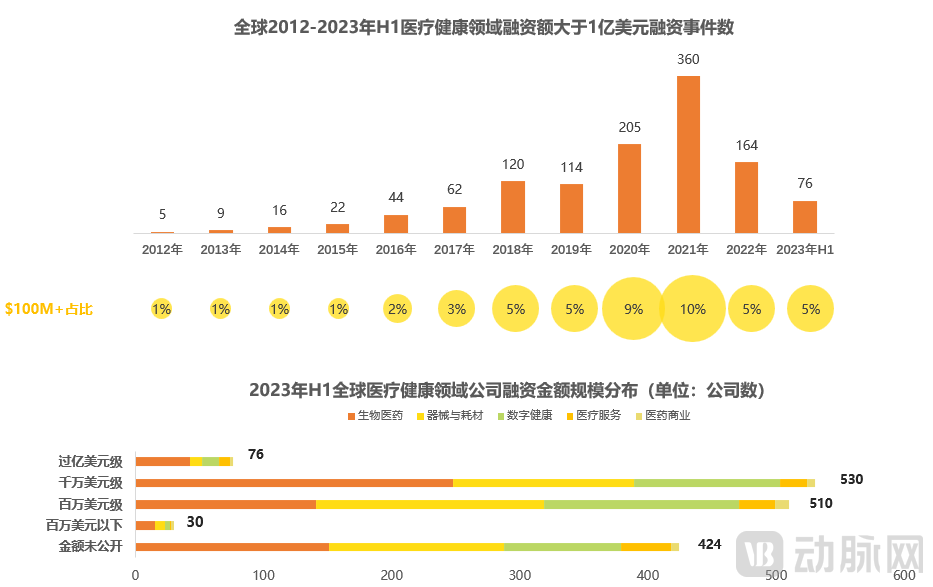

In H1 2023, there were 76 individual financing deals worldwide exceeding $100 million, accounting for approximately 5% of the total financing amount in H1, comparable to the same period in 2022; more than half of these deals originated from the biopharmaceutical sector.

Among the most numerous financing rounds in the tens of millions of dollars, biopharmaceutical companies continue to maintain their leading advantage. In contrast, medical device and digital health sectors hold only a slight edge in the million-dollar range, reflecting more restrained investment activity compared to the biopharmaceutical sector.

Furthermore, it is worth noting that although there was no advantage in the number of financing events, companies in the healthcare services sector attracted several funding rounds exceeding $100 million in H1 2023. The demand market for basic healthcare and the capital market remained in sync.

II. Hot Sectors in Global Healthcare Investment and Financing in H1 2023

2.1 Biopharma Remains Stable Despite Decline in Single-Deal Financing; Global Digital Health Sector Drops 49% Quarter-on-Quarter

In H1 2023, the global biopharmaceutical sector led all sub-sectors with 598 transactions totaling $14.8 billion. The digital health and medical device sectors followed closely behind, with 474 and 473 transactions, respectively. Compared to H1 2022, both the total financing amount and the number of financing events across all global sectors declined to varying degrees in the current period, with the digital health sector experiencing the most pronounced drop—a 49% quarter-on-quarter decrease in total financing value.

In China, the biopharmaceutical sector continues to hold the top position, but total financing has declined significantly, dropping 38% quarter-on-quarter. Specifically, the number of financing deals is comparable to that in the first half of 2022, indicating a decrease in the average amount per deal.

Digital health and medical devices also saw significant declines in domestic financing, with total amounts dropping 40% and 48% month-over-month, respectively.

Compared with H1 2022 and H1 2021, financing activity across various healthcare subsectors has remained sluggish, underscoring the growing uncertainty within the broader medical industry.

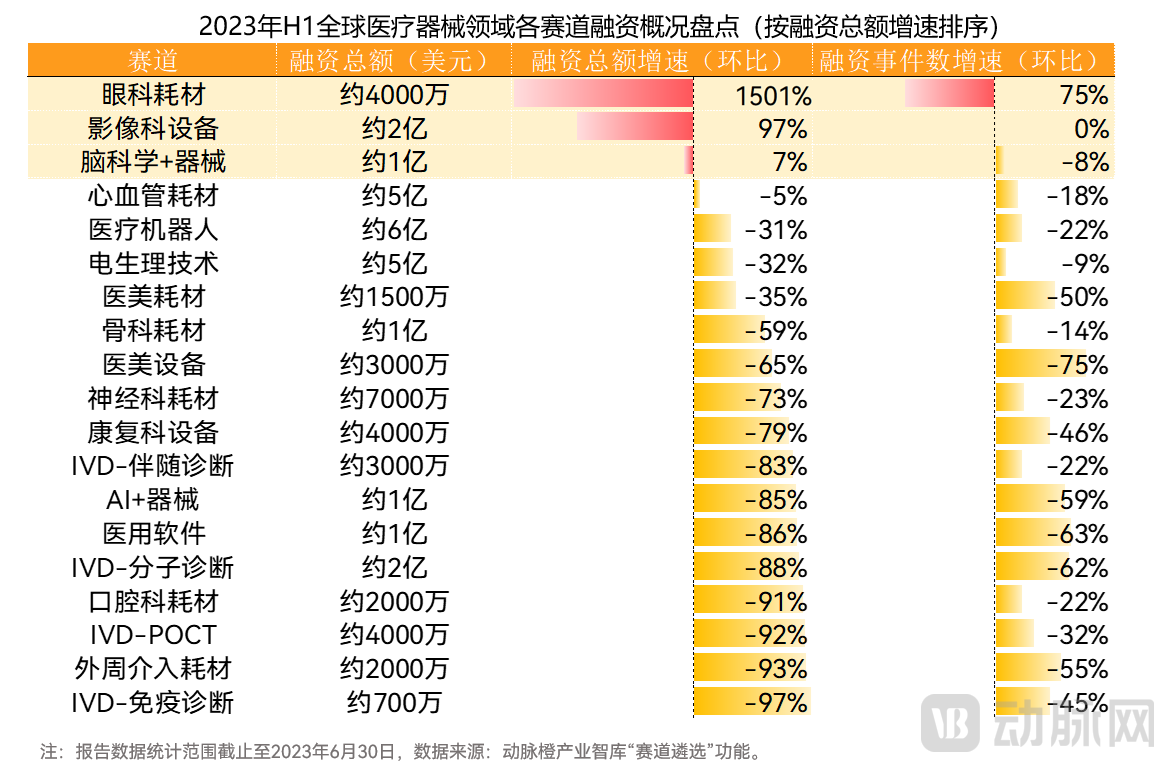

2.2 Financing Heat in the Primary Market for Medical Devices Declines Broadly, with Only 3 Sub-sectors Maintaining Positive Growth

In H1 2023, there were a total of 473 financing deals in the global medical device sector, amounting to approximately USD 5.271 billion, indicating a decline in financing activity compared to H1 2022.

According to the “Track Selection” feature of VBInsight, all sub-sectors of the medical device industry exhibited varying degrees of decline in the first half of 2023, particularlySub-segments of the IVD Industry, since the end of 2022, as domestic prevention and control policies were gradually relaxed, financing enthusiasm in the IVD sector has significantly cooled. In H1 2023, there were 88 financing deals totaling approximately $483 million, a 84% quarter-on-quarter decrease, and even lower than the $1.419 billion recorded in H1 2019. Meanwhile, individual deal sizes were relatively small, with 28 deals concentrated at the million-dollar level.

Ophthalmic Consumables SectorIt is one of the few segments in the medical device sector where both total financing amount and number of financing events have shown positive growth. Notably, the year-over-year growth rate of total financing reached 1501% in the first half of 2023, driven by RMB 100 million in major financing rounds completed in Q1 2023 by Meimu Meijia, a colored contact lens manufacturer, and Ruitai Biology, a developer of regenerative repair materials, which significantly boosted the segment’s overall financing volume.

Financing in the primary market for medical devices remains sluggish, while the secondary market shows little promise. The industry landscape is undergoing rapid consolidation, with increasing market concentration compelling companies to intensify innovation and accelerate their global expansion. According to data from the General Administration of Customs of China, the total value of China’s medical device exports reached RMB 444.179 billion from January to November 2022, with the full-year export value projected to reach RMB 478.5 billion.

2.3 Strong Policy Support for Surgical Robots Sustains High Financing Momentum

In H1 2023, the global surgical robotics sector maintained its momentum, with 26 financing deals totaling $611 million.

In China, 15 surgical robot companies have completed financing rounds, including the one that secured RMB 800 million in funding.ConustechHaving reached Series B, the overall funding stages remain relatively early, with all companies having secured at least Series A financing. Meanwhile, half of these enterprises were founded in 2020 or later. According to data from the National Medical Products Administration (NMPA), at least 15 surgical robots were approved in China in 2022, indicating that the Chinese surgical robot market is poised for significant transformation.

Meanwhile, policy initiatives are also accelerating the adoption of surgical robots. In March 2023, the National Health Commission releasedCatalogue for the Administration of Configuration Licenses for Large Medical Equipment (2023)notice, laparoscopic surgical robots remain in the Category B list, but the price cap has been adjusted from the previous range of RMB 10–30 million to RMB 30–50 million. In April, the National Health Commission announcedDraft for Comments on the Standards for Configuring Large-Scale Medical Equipment (New Edition), which means that in the future, laparoscopic surgical robots will no longer be exclusive to large tertiary Grade A hospitals; medical institutions at the prefecture-level city and county levels will also have the opportunity to acquire them during this expansion.

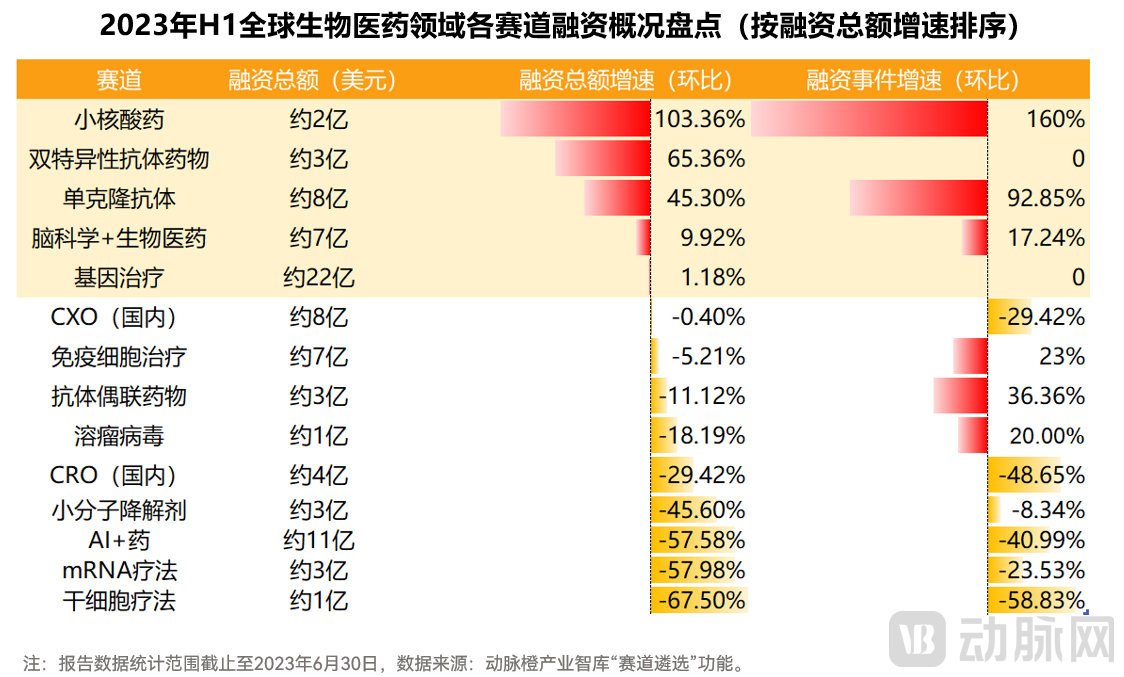

2.4 Financing Heat in the Innovative Drug Sector Cools Slightly, with Small Nucleic Acid Drugs Standing Out

According to the “Track Selection” feature of VBInsight, financing trends across various sub-sectors in the biomedical industry have shown mixed fluctuations. Among them, the gene therapy sector remained largely flat year-over-year in both total financing amount and number of financing deals; whereas with theSmall Nucleic Acid DrugsThe application and technical domains continue to achieve breakthroughs and innovations, the market size is gradually expanding, and market interest in small nucleic acid drugs is steadily growing.

Driven by the pandemic, interest in mRNA COVID-19 vaccines surged rapidly, leading to increasing crowding in the mRNA sector. Since the relaxation of pandemic control measures, market demand for COVID-19 vaccines has gradually declined, resulting in a cooling of overall financing activity in the mRNA field compared to previous levels.

It is worth mentioning that in recent years, with the development of the field of artificial intelligence,Brain Science and BiopharmaceuticalsOnce again becoming a topic of industry focus, coupled with the forward-looking layout and resource allocation towards basic research in biomedicine, including brain science, under the “14th Five-Year Plan,” the heat in the fields of brain science and biomedicine continues to rise.

2.5 Indication Expansion and Surge in R&D Pipelines Propel CGT Sector into a Phase of Rapid Growth

In H1 2023, the global cell and gene therapy sector witnessed 128 transactions, with cumulative financing amounting to $4.119 billion.

Specifically, in the field of cell and gene therapy in China during the first half of 2023, domestic companies completed 57 transactions, raising a total of $641 million. In comparison, while the number of transactions increased compared to the previous year, both the total transaction value and the average deal size showed a downward trend.

As the application of CAR-T therapy expands into the field of solid tumor treatment,CGT Accounts for an Increasing Share of Oncology Clinical Trials, Becoming a Global Trend, the number of new R&D pipelines and related clinical projects for CGT has increased significantly both domestically and internationally. In addition, the therapeutic indications for CGT are gradually expanding to other diseases, such as cardiovascular diseases and neurodegenerative disorders. Particularly after the FDA updated its drug approval criteria for Alzheimer’s disease, interest in this field has markedly intensified.

2.6 Payment Models Challenge Sector Maturity, Digital Therapeutics Field Faces Overall Setbacks

In H1 2023, the global digital health sector saw a total of 374 financing deals, amounting to approximately USD 5.833 billion, marking a decline in investment activity compared to H1 2022.

According to the "Track Selection" function of VBInsight, the digital health sector saw significant divergence across its various sub-sectors in the first half of 2023.Digital Therapeutics SectorBuffeted by multiple headwinds—including valuation contractions, unproven business models, and bankruptcies among industry leaders—overall funding amounts and deal counts have declined. This has prompted investors to exercise greater caution when increasing their stakes in companies that have entered the maturity stage, such as those in the digital therapeutics sector for stroke. On the other hand, the current market correction has enabled some companies to carve out new paths by delving into niche areas like gastrointestinal diseases, successfully attracting attention from the capital markets.

Moreover, in addition to the virtual care sector, which has been consistently generating substantial revenue,Internet Marketing ServicesIn the first half of 2023, a surge of new projects emerged. This trend was closely related to the growing demand among major healthcare enterprises and institutions for cost reduction and efficiency improvement. Additionally, unlike digital therapeutics, particularly in the realm of domestic internet marketing services, the payment process has been refined under the support of internet-based medical insurance reimbursement policies, thereby indirectly boosting industry development.

2.7 AIGC+Healthcare Emerges as a Dark Horse, with Tech Giants Vying for Strategic Positioning

Since the advent of natural language processing tools driven by artificial intelligence technologies such as ChatGPT, interest in AIGC technology within the healthcare sector has continued to rise, with its significant application potential drawing considerable attention from the medical industry. Currently,AIGC Has Penetrated the Entire Clinical Workflow from Pre-Consultation to Post-Consultation. AIGC can also help optimize clinical pathways by analyzing large volumes of clinical data to identify best practices and treatment patterns.

Behind the rapid rise of the AIGC industry, in addition to the accumulation and integration of numerous AI innovative technologies, factors such as the introduction of relevant policies and the influence of the market environment are also involved. In July 2023, the Cyberspace Administration of China issued《Interim Measures for the Administration of Generative Artificial Intelligence Services》, to promote the healthy development and standardized application of generative AI technologies. As domestic and international tech giants represented by Microsoft, Google, Baidu, Alibaba, and Tencent have entered the AIGC sector, this field has garnered significant attention from the investment community and is being vigorously pursued by both the technological and industrial sectors.

2.8 Trending Tags: Biopharmaceuticals, Healthcare Informatics, Other Consumables, and R&D and Manufacturing Outsourcing Are Highly Popular

In H1 2023, tags such as biopharmaceuticals, healthcare informatics, other consumables, and R&D and manufacturing outsourcing garnered significant attention.

In terms of funding rounds, public financing in the first half of 2023 was concentrated primarily in the early stages, especially Series A. Fewer companies reached Series D and beyond, with these being mainly in the biopharmaceutical sector. Notably, three companies advanced to the Pre-IPO stage, all of which were biopharmaceutical firms, including a developer of novel fully human monoclonal antibody therapeutics derived from natural sources.Tainuomab, Developer of New Drugs for the Treatment of Metabolic DiseasesYinuo Medicine、An integrated pharmaceutical R&D company with a full industry chain spanning large-scale API and formulation manufacturingDisano。

It is worth noting that in previous years, the sectors with a higher number of financing eventsIVD Sector, in H1 2023,Fall to Seventh Place. Financing enthusiasm in the IVD sector has significantly waned, with the total financing amount in H1 2023 dropping by 84% quarter-on-quarter, marking a substantial decline.

III. Analysis of Active Healthcare Investment Institutions in H1 2023

3.1 Qiming Venture Partners Made 16 Investments in Total, Becoming the Most Active Investment Firm in the First Half of the Year

In H1 2023, the most active institutions in global healthcare wereQiming Venture Partners, with a total of 16 investments made in the first half of the year, showing a preference for the medical device and biopharmaceutical sectors. Its investment targets are primarily medical device companies, such as innovative surgical robot developers.ConustarProvider of Catheter and Membrane Material SolutionsShanghai Yike. Meanwhile, Qiming Venture Partners served as the lead investor seven times in the first half of 2023.

Compared with the first half of 2022, star investment firms such as Sequoia Capital China, Hillhouse Capital, and Yuansheng Ventures exercised considerable caution in making investment decisions during the first half of 2023. This indicates that the entire healthcare industry’sUncertainty Becomes Increasingly Evident。

3.2 Domestic investment institutions significantly reduced their deal activity, with early-stage and small-ticket investments becoming the norm

In H1 2023, the most active institutions in China's healthcare sector wereQiming Venture Partners, having made a total of 16 investments, primarily targeting medical device companies.

Notably, among the financing rounds participated in by Qiming Venture Partners in the first half of 2023, there were7 financing rounds are secondary injections, and3 rounds of capital injectionWushuang Medical, a developer of cardiac rhythm management products, and Dingke Medical, a developer of vascular interventional balloon products,4 rounds of capital injectionTumor Immune Cell Product Developer: Yuanqi Bio.

In recent years, guided by industry trends and policies from various local governments, investment institutions have increasingly focused on early-stage and small-scale investments, delving deeper into the early stages of the healthcare sector. Data from the first half of 2023 shows that investment firms still favor early-stage projects.

IV. Review of Healthcare IPOs Listed in H1 2023

4.1 U.S. IPO Market Shows Signs of Recovery, with Reduced Fundraising Scale

According to the VCBeat database, in H1 2023, a total of 93 healthcare companies listed on the A-share, U.S. stock, Hong Kong stock, and Canadian stock markets raised over $7.631 billion. Compared with H1 2022, although the number of fundraisings increased, the total amount raised declined. Notably, in H1 2023U.S. StocksThe number of listed companies has risen sharply year-on-year, amounting to approximately the sum of IPOs in all other stock markets.Twofold。

Since the beginning of 2023, global capital markets have underperformed amid multiple factors, including the banking crisis in Europe and the United States, the implementation of the Federal Reserve’s interest rate hike plans, and intensifying inflation in many countries. Corporate valuations have remained at low levels, and IPO fundraising has been dominated by small- to mid-sized offerings. With the exception of Kenvue, a consumer health product developer, which raised $3.8 billion to become the largest IPO since 2021 by a wide margin, no other IPOs have raised more than $1 billion.

Among the three major stock exchanges in China’s A-share market,SZSEThe largest number of healthcare companies applying for listing are in the medical and health sector. Although the number of listed companies is on par with the Shanghai Stock Exchange, the Beijing Stock Exchange, influenced by its own positioning, generally accepts smaller-scale companies.

4.2 Multi-party policy incentives drive steady increase in activity of China's IPO market

Under the dual impact of the registration-based IPO system reform and price reductions from centralized procurement, listing thresholds have gradually risen, while companies and investment institutions have become increasingly cautious. As a result, the number of A-share listed companies in the first half of 2023 declined compared to the same period last year.

BSEThe introduction of equity incentives, differentiated voting rights structures, and the direct listing mechanism has better aligned with the needs of small and medium-sized enterprises (SMEs), stimulating greater innovation vitality among them. As a result, the number of companies listed on the Beijing Stock Exchange in the first half of 2023 increased significantly compared to the same period last year.

With the implementation of policies such as the listing mechanism for “Specialized and Sophisticated Technology” enterprises and the “Dual Counter Model,”HK Stocksliquidity and trading activity have further increased, with June alone seeing5 companiesChinese-funded enterprise successfully listed on the Hong Kong Stock Exchange.

Furthermore, the proper resolution of the audit dispute between China and the United States, coupled with the release of new regulations on overseas listings, has further smoothed the path for Chinese enterprises to pursue initial public offerings (IPOs) in the U.S.

V. Distribution of Global Healthcare Investment and Financing Hotspots in H1 2023

5.1 China Surpasses the US in Number of Financing Deals, with China and the US Accounting for 81% of Global Financing Amount

In H1 2023, the five countries with the highest number of global healthcare financing events were China, the United States, the United Kingdom, France, and Canada.

H1 2023,China, with 649 financing events and $5.676 billion (approximately RMB 40.8 billion)Global Financing Leads the Way. China and the US Account for 81% of Total Global Financing and 78% of Financing Deals.

Although the number of financing events in the United States this quarter was lower than that in China, it surpassed China with a total amount of $18.654 billion (approximately RMB 134.1 billion), a phenomenon closely related to the distribution of large-scale financings.

From the perspective of hot investment sectors,BiopharmaceuticalsandMedical DevicesIt was a hot topic of global concern in the first half of 2023.

5.2 Jiangsu Tops the List, with the Jiangsu-Zhejiang-Shanghai Region Becoming a Hotspot for Investment and Financing

The five regions with the most concentrated healthcare and medical investment and financing activities in China in H1 2023 were, in order:Jiangsu, Guangdong, Shanghai, Beijing, Zhejiang。

Jiangsu has witnessed a cumulative total of 141 financing events, raising $831 million (approximately RMB 6 billion).the city with the highest number of financing events in the first half of the year. Guangdong, ranking second, has recorded a cumulative total of 116 financing events, raising $874 million (RMB 6.3 billion).

The Jiangsu-Zhejiang-Shanghai region remains a fertile ground for investment and entrepreneurship. With robust economic development, strong policy support, an optimized industrial structure, and powerful innovation capabilities, this region has attracted significant attention from investors.

VI. Top Financing Records of Healthcare Companies in H1 2023

6.1 U.S. Health Service Providers Lead the Global Rankings, with Heisen Biopharma as the Only Chinese Company on the List

6.2 Chinese biopharmaceutical companies dominate the rankings with an absolute advantage, while only two companies from the medical device sector made the list