Subtle Signals in Biotech Investment Midway Through 2023

2023 was a year when the biotech sector was expected to rebound. Early in the year, investors were the first to spring into action, engaging in frequent business trips and intensive project evaluations. However, after some time, the prevailing feedback was that “no suitable investment opportunities had been identified.” Coupled with the Silicon Valley Bank incident at the end of the first quarter, the biotech venture capital ecosystem appeared to be on shaky ground.

The first quarter was disappointing, as the nascent market enthusiasm was quickly dampened. However, good news soon followed: biotech stock prices stopped their decline and began to recover, with some even doubling in value; large-scale financings re-emerged in the market, with certain IPOs raising amounts unseen throughout all of 2022; the ADC boom and the vigorous competition in the GLP-1 sector have repeatedly bolstered the pharmaceutical segment.

However, some previously popular platform-based companies have fallen out of favor, with capital flowing toward those with promising pipeline progress or the ability to fill market gaps. Biotech firms specializing in technology are also increasingly emphasizing their “keen insight into real clinical needs.”

Major catalysts or technological breakthroughs remain absent, yet subtle signals and shifts are propelling the biotech market forward. As RA Capital recently summarized this year’s investment tone: more cautious than in 2020, but more confident than in 2022.

Silicon Valley Bank Collapses, Biotech Survives

This March, many biotech companies were shaken by the collapse of Silicon Valley Bank. At the time, there were widespread concerns about the future of the entire innovation ecosystem—particularly in the biotech sector—and about investor confidence in biotech firms.

Already impacted by the Federal Reserve’s interest rate hikes, the collapse of Silicon Valley Bank has further exacerbated the challenges facing the biotech sector. In the first quarter of this year, total financing in the biotech industry—including venture capital (VC), initial public offerings (IPOs), secondary market follow-on offerings, and debt—declined by 31% year-over-year and 18% quarter-over-quarter. Notably, VC financing dropped by 45% year-over-year, hitting its lowest level since the third quarter of 2019.

In the U.S. stock market, many biotech stocks did indeed decline more than the broader market in the first quarter, but since then, the share prices of most publicly listed biotech companies have been on a path to recovery: either continuing to rise or declining less than they did a year ago.

The S&P Biotechnology Select Industry Index shows a 9.6% increase from its low of 6,004 on March 31 to 6,582 by June 30. The SPDR S&P Biotech ETF (ticker: XBI) tracks this index. Most of the biotech companies included in the index have immature business operations and exhibit high volatility. It is widely regarded in the industry as representative of the performance of typical small- and mid-cap biotech stocks.

An ETF linked to the S&P Biotech Index: Direxion Daily S&P Biotech Bull 3X Shares (LABU), which previously experienced a significant decline, has seen its price rise from $4.91 to $5.59 in the second quarter, representing a 13.8% increase.

Another Biotech ETF: First Trust NYSE Arca Biotechnology Index Fund (FBT), which rose 10.1% year-over-year as of May 2, climbing from $138.38 to $152.29. FBT is the fourth-largest biotech ETF, with total assets under management reaching $1.46 billion. Its top holdings include Acadia Pharmaceuticals, a company focused on innovative CNS therapies; Agios Pharmaceuticals, specializing in cellular metabolism therapeutics; and Ionis Pharmaceuticals, a leader in antisense oligonucleotide drugs.

More Good News on IPOs as Large-Scale Fundraising Continues

It is not only publicly listed biotech companies that are recovering from the bottom; there is also good news regarding IPO financing and large-scale funding rounds.

On May 5, biotech company Acelyrin (NASDAQ: SLRN) listed on the Nasdaq Stock Market, pricing its shares at the top of the range at $18 per share. The company also expanded its offering size from 8.95 million shares to 10.74 million shares, raising $540 million. This marks the largest IPO proceeds for a U.S.-listed biotech firm since February 2021. Less than three years have passed since Acelyrin’s founding to its public listing. Established during the pandemic, Acelyrin focuses on treating refractory autoimmune diseases, with its core product, izokibep, currently undergoing three Phase IIb/III clinical trials.

Chinese Biotech Companies Begin Returning to Nasdaq: In March this year, Yisheng Biopharma completed its business combination with Summit Healthcare to list on Nasdaq, while Crown Bioscience completed its business combination with Maxpro to go public on Nasdaq.

Turning to the Hong Kong stock market, Kelun-Biotech listed on the Hong Kong Stock Exchange (HKEX) on July 11, achieving a market capitalization exceeding RMB 10 billion. Having submitted its prospectus in March and completed its listing by July, it became the first biotech company since 2022 to pass the HKEX hearing after a single submission. Leveraging over a decade of accumulated expertise in transformation, Kelun-Biotech has capitalized on the rapid growth of the antibody-drug conjugate (ADC) sector. From May to December last year, Kelun-Biotech entered into three collaborative agreements with Merck & Co., covering nine novel ADC drugs, with a total transaction value reaching $11.8 billion. The listing of Kelun-Biotech has served as a significant boost to the long-dormant Hong Kong stock market.

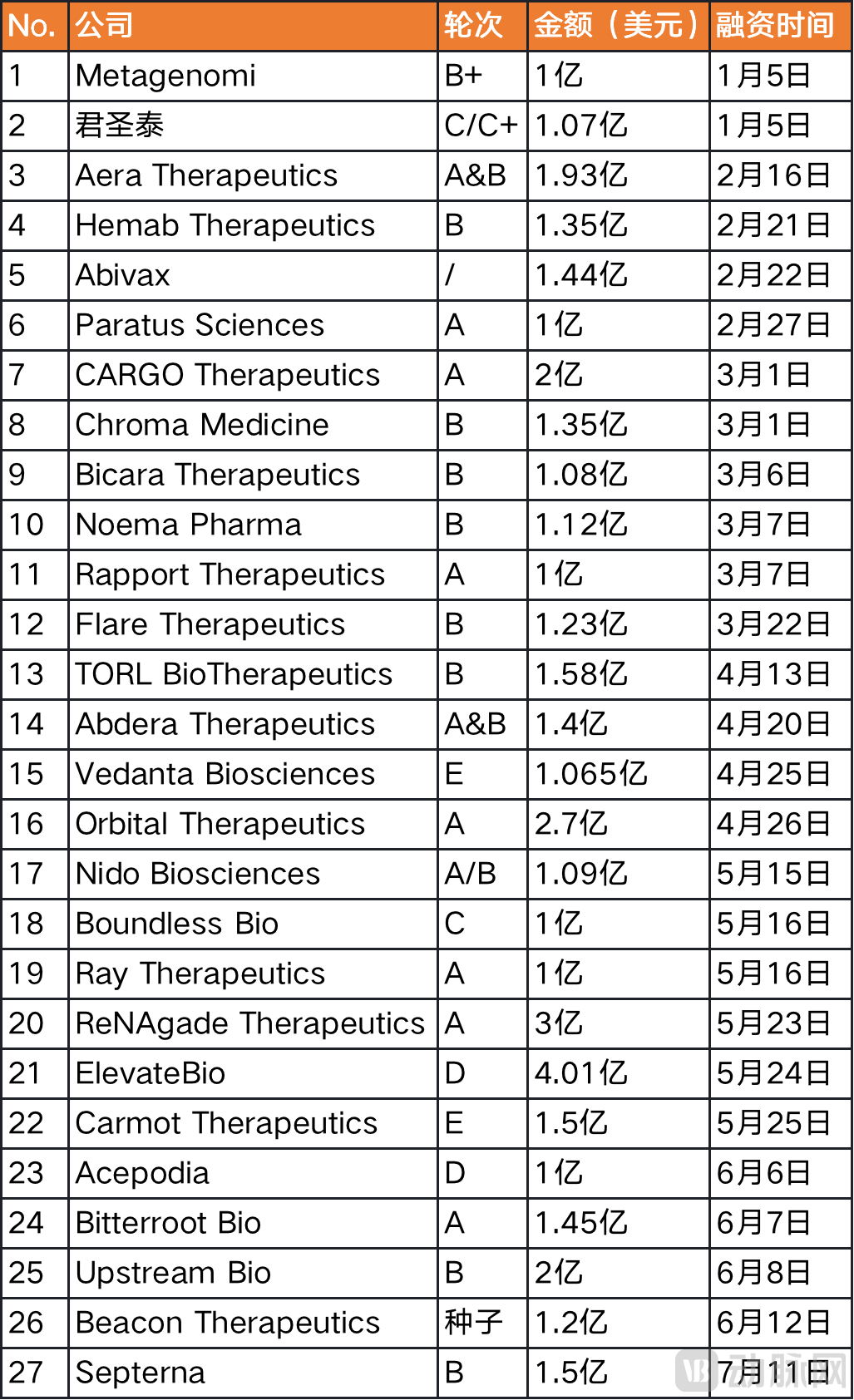

In the primary market, the number of large-scale financings for global biotech companies is also gradually increasing.In the first quarter of this year, the only deals that could be considered large-scale were Cargo Therapeutics’ $200 million Series A financing and Aera Therapeutics’ combined $193 million in Series A and B financing. In the second quarter, the market began to heat up, with a succession of major financings, including Orbital Therapeutics’ $270 million Series A, Hasten Biopharmaceutic’s $315 million Series A, ReNAgade Therapeutics’ $300 million Series A, and ElevateBio’s $400 million Series D.

Biotech Financing Deals Exceeding $100 Million in 2023; Data Source: Fierce Biotech; Chart by VCBeat New Medicine

Compared with the large-scale financing rounds seen in 2020–2021, this year’s figures are less striking—for instance, Sana Biotechnology raised $700 million in its Series A round in 2020, and Eqrx secured $470 million in its Series B round in 2021—but at least the momentum continues.

However, analysts have pointed out that despite the abundance of capital in the market, investor confidence in biotech remains lacking. Biotech companies are beginning to address potential future cash shortages as early as the seed and Series A financing rounds, striving to use cash more efficiently and focusing on the most promising projects.

Chinese Biotech: Shining Gold

Biotech stocks are never short of two-baggers or even multi-baggers. Even when the broader market is lukewarm, biotech companies with encouraging clinical progress can still buck the trend and rise. Among the companies that have surprised the market this year, Chinese biotechs are well represented.

For instance, several Chinese biotech companies that made appearances at ASCO demonstrated strong stock performance. Gracell Biotechnologies, for example, surged to $6 following ASCO, having hit a low of $1.46 on April 25. The company later released positive data on its CAR-T therapy GC012F for the treatment of relapsed/refractory B-cell non-Hodgkin lymphoma at the 28th Congress of the European Hematology Association (EHA), driving its share price to a new high of $6.99—the highest level in nearly one and a half years—and marking an increase of nearly 400% over 35 trading days.

In 2022, Gracell Biotechnologies was once included on the U.S. SEC’s “Pre-Delisting” list for Chinese issuers, but has since made a remarkable comeback. Setting aside changes in the external environment, its products’ profound and durable efficacy, coupled with differentiated advantages in CAR-T manufacturing capacity, have positioned it as a Chinese biotech company drawing dual attention from both the industry and investment communities.

Legend Biotech is also experiencing a return to value. In the first quarter of 2023, overseas sales of Carvykti reached $72 million, marking a significant quarter-on-quarter increase. The company has entered into an industrialization cooperation agreement with Novartis to boost production capacity. With market expectations continuing to rise, Legend Biotech’s stock price has increased by 41.46% year-to-date.

One of the most impressive performers in the Hong Kong stock market is 3D Medicines, which listed late last year. Thanks to the successful commercialization of its first product, Envafolimab (®), 3D Medicines successfully removed the “-B” marker from its stock name just half a year after its listing, becoming the eleventh company to achieve this milestone among those listed under Chapter 18A of the Hong Kong Stock Exchange since the channel opened five years ago. In the first half of this year, the gross profit from sales of 3D Medicines is expected to range between RMB 319 million and RMB 335 million, representing a year-on-year increase of 66.1% to 74.6%. The company, which had an IPO price of HK$24.98, has seen its share price nearly quintuple, with its market capitalization approaching HK$30 billion.

Investing in Clinical Needs

Looking at the overall performance of pharmaceutical stocks this year, Eli Lilly has emerged as the clear winner, with strong results in both the glucose-lowering and weight-loss segments and the central nervous system (CNS) therapeutic area. Its market capitalization has surpassed $400 billion, making it the world’s most valuable healthcare company, with an increase of over $94 billion this year alone. Eli Lilly’s closing price in June hit a record high. The market’s high growth expectations are largely driven by the company’s portfolio of high-demand drug candidates and its proven ability to successfully commercialize and launch them.

Nowadays, the wind of pragmatism has also blown into the Biotech sector. Roger, an investor who has long tracked the secondary market for biopharmaceuticals, believes that since the beginning of this year, most Biotech companies with successful IPO fundraisings or strong stock performance share a common trait: their businesses aim to address unmet clinical needs, and their pipeline progress or clinical data are optimistic.

Biotech companies that focus on cutting-edge technologies but lack successful commercialization of their achievements are currently out of favor in the market. For instance, Ginkgo Bioworks, a leader in synthetic biology, has seen its stock price drop by 33% compared to a year ago, and its current market capitalization is only one-sixth of its peak value at the end of 2021. Due to the absence of flagship products, Ginkgo has been actively engaging in external collaborations or acquisitions in platform and technology development since the second half of last year. Its ventures span from biocatalysts and gene therapy to bio-based materials, yet these efforts have failed to alleviate market skepticism.

Several AI-driven biotech companies are also struggling. Recursion Pharmaceuticals, Exscientia, BenevolentAI, and Absci have all seen their stock prices decline over the past year (until NVIDIA’s investment in Recursion suddenly injected new momentum into the sector). Although “AI for Science” has been frequently highlighted in recent years, the integration of AI and drug development has not proceeded smoothly in the industrial arena. Schrödinger stands out as one of the more successful companies in this space. Revenue from its computer-aided drug design (CADD) and AI-driven drug discovery (AIDD) software constitutes its primary income source, while revenue from collaborative drug development projects has been accounting for an increasing proportion of its total revenue year by year. Its stock price surged by more than 172% in the first half of this year. Nevertheless, the company recently asserted that it is “a pharmaceutical company with proprietary software,” rather than an “AI drug discovery company.”

This also underscores the scientific essence of biotech: while cutting-edge technologies may be glamorous, it is the emergence of new billion-dollar molecules that truly ignites excitement in the field.

The Pace of Biotech Has Changed

The massive liquidity injection and capital influx from 2020 to 2021 significantly accelerated the development of this industry. The technological advancements in R&D driven by this capital have paved the way for more innovative therapies, expanding the horizons of this field. This year, the surge in interest in GLP-1s and ADCs, coupled with the FDA’s historic approvals of new drugs for ALS, Alzheimer’s disease, and ophthalmic complement inhibitors, has further boosted the overall prosperity of the pharmaceutical industry.

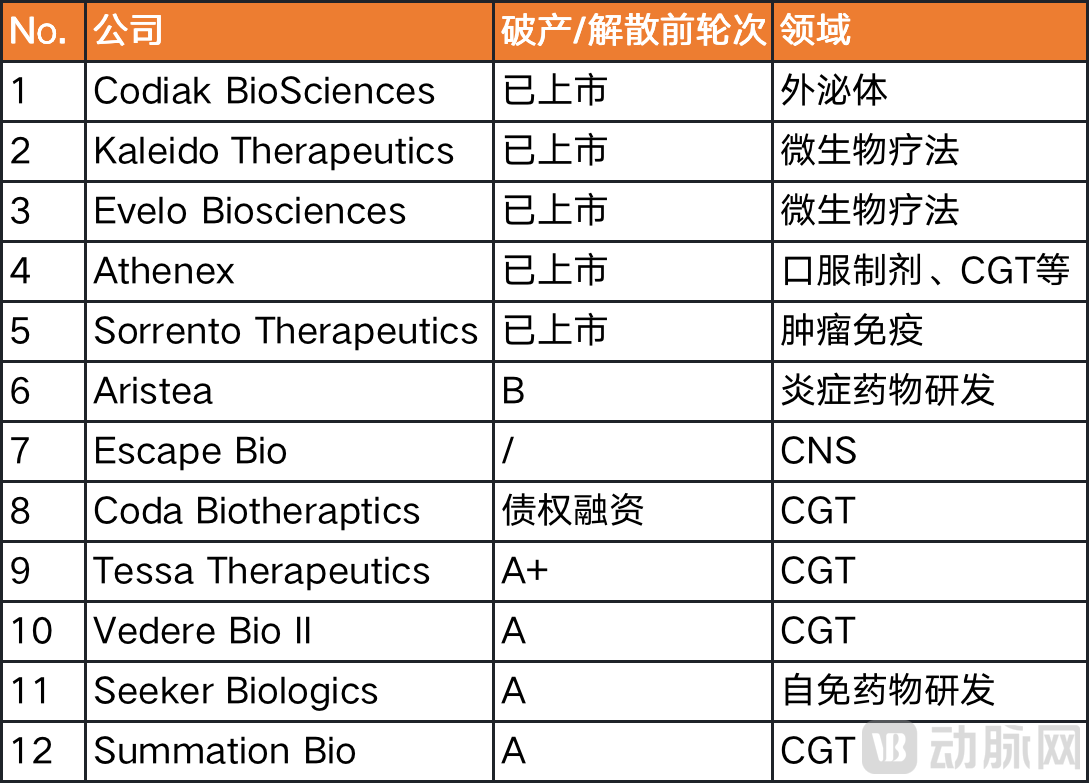

Yet the market’s frenzy lies in the belief that everyone can become the next Moderna, such that every instance of one or a few biotech firms going bankrupt, some innovative therapies failing, or cutting-edge technologies losing their way triggers lamentation over the entire biotech sector’s prospects. Admittedly, no small number of biotech companies have gone bankrupt in the past two years, with even star companies under the Flagship Pioneering model filing for bankruptcy one after another. However, we should not overlook the technological nature of biotech. This sector, much like tech stocks, adheres to the 80/20 rule: the demise of the majority of companies like bubbles and the collapse of batches of once-glamorous unicorns are normal phenomena of industry consolidation, just as it is normal for high-quality companies to remain in high demand.

Biotech Companies That Filed for Bankruptcy or Dissolved in 2023

Dr. Xia Yukun, a biopharmaceutical investor, believes that investors are increasingly focusing on metrics such as company revenue and production capacity, with their risk appetite gradually declining. Therefore, startups that prioritize only the novelty of their technology without addressing specific market demands and indications will find it difficult to secure financing.

Just like tech companies, if they lack practical and scalable application scenarios, they cannot generate actual revenue.

However, this does not mean that new technologies should be neglected by capital. Large pharmaceutical companies are acting like private equity firms, continuously identifying valuable biotech companies and their technology platforms, and striving to explore practical applications for various emerging technologies. Meanwhile, major tech giants are also entering the biotech sector, leveraging their substantial cash reserves to simultaneously support multiple cell and gene therapy (CGT) or regenerative medicine startups in exploring uncharted territories of human knowledge.

Biotech is still moving forward, only the pace has changed; everyone in this market must adapt to it.