Golden Membrane Material at the Heart of a Trillion-Yuan Market Attracts Investments from Legend Capital and Matrix Partners

Cobetter

Developer of Microporous Filter Membranes, Nanofibers, and Ultrafiltration Membranes

In 2023, investors in biopharmaceuticals and medical devices simultaneously turned their attention to a specific sector: membrane materials.

You can envision membrane materials in the medical industry as sieves that filter out unnecessary impurities, viruses, and toxins in pharmaceutical manufacturing and hemodialysis, with a filtration precision at the 1-nanometer level.

Investors are queuing up to approach membrane material companies, but some have been turned away. Domestic enterprises in the membrane material sector, which started development earlier and have larger production capacities, have refused to meet with investors. Shutting out investors indirectly demonstrates the confidence and strength of the membrane material industry.

The membrane materials industry is indispensable in biopharmaceuticals, occupying a critical position in the industrial chain. It directly determines product performance in devices such as hemodialyzers and ECMO systems.

The technical barriers for membrane materials are also difficult to overcome, especially in achieving large-scale mass production.Domestic high-end filter membranes rely on imports, with membrane filter cartridges once priced as high as $300 per unit. Due to the lack of domestic suppliers, many products have experienced annual price increases of 3%-5%.

In terms of supply chain security, hollow fiber membranes have previously triggered a supply chain crisis. In February 2022, WuXi Biologics was placed on the U.S. Department of Commerce’s Unverified List (UVL), with the restricted export products being hollow fiber filters and single-use bioreactors.

In fact, as China’s biopharmaceutical and medical device industries reach their current stage, the challenges remaining for breakthroughs are becoming increasingly thorny. The path back is arduous and long, and filter membrane materials serve as a microcosm of this industrial challenge.

Amid growing supply chain anxieties surrounding high-end filtration membrane products, domestic companies have begun to make substantial investments.Recently, multiple domestic high-end membrane material companies have secured hundreds of millions in financing.

On July 12, Shanshan Hemodialysis (688410) announced its plan to establish a wholly-owned subsidiary, Chongqing Yuanzhongyuan Biomaterials Co., Ltd., with self-owned funds not exceeding RMB 270 million. Shanshan stated that the establishment of this subsidiary is primarily intended to provide membrane materials for the company’s consumable products and to handle the processing of plastic and rubber components for these consumables. This move will facilitate the registration and filing of the relevant consumables, reduce their production costs, and enhance the company’s competitiveness in centralized procurement bids.

Financing in China's Biopharmaceutical Filter Membrane Industry

Financing in China's Biopharmaceutical Filter Membrane Industry

In reality, as China’s biopharmaceutical and medical device industries have progressed to their current stage, the challenges impeding breakthroughs have become increasingly intractable. The path forward is arduous and long, and filtration membrane materials serve as a microcosm of these industrial challenges.

In 1784, A. Nelkt discovered that water could spontaneously diffuse into a pig bladder containing alcohol, pioneering the study of membrane permeation. In the 1860s, membrane separation technology was applied to industrial processes.

Today, membrane separation technology is widely used in various industries such as chips, water treatment, pharmaceuticals, and food. In biopharmaceuticals and hemodialysis, how do filter membranes become a bottleneck in these niche sectors?

Membranes and filters for biopharmaceutical applications are essential consumables in the separation and purification process. Separation and purification constitute a core production step for biologics such as monoclonal antibodies, fusion proteins, vaccines, insulin, and peptides, directly determining drug purity and quality, and representing a major component of production costs.

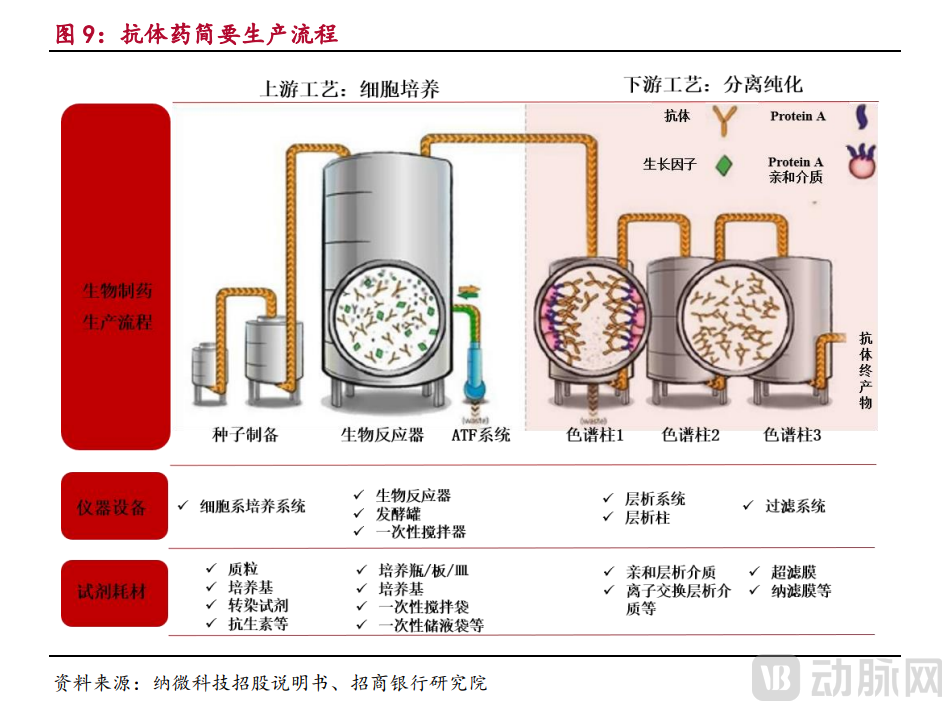

Taking the production of antibody drugs as an example, the entire manufacturing process primarily consists of upstream cell culture and downstream separation and purification. Upon completion of antibody fermentation, the broth proceeds directly to the downstream separation and purification stage, where it undergoes steps such as clarification, chromatographic separation, and virus removal filtration to yield the final antibody bulk drug substance. This process mainly consumes chromatography resins—such as affinity and ion-exchange media—and various filter membranes as consumables, while utilizing equipment including chromatography columns and filtration systems.

Antibody Drug Manufacturing Process and Associated Equipment, Reagents, and Consumables

As shown in the figure above, membrane filtration products are positioned as a category of upstream consumables within the life sciences industry chain. Similar to most upstream life sciences consumables, membrane filters used in the biopharmaceutical sector also rely on supply from import-dependent enterprises.

As is well known, the upstream sector of the life sciences industry has become a focal point for capital markets. Over the past year, substantial funds have flowed into sectors such as single-use bioreactors, cell culture media, chromatography resins, and equipment for the cell and gene therapy (CGT) industry.

However, the highlight moment for filter membranes came later.

Investors seeking membrane filtration companies are not limited to those focused on upstream life sciences; others are also targeting domestic membrane filtration enterprises based on the logic of sourcing core components for upstream medical devices. This is because hollow fiber membranes are the lifeline of two critical products: hemodialysis machines and ECMO systems.

In hemodialysis, the performance of hollow fiber membranes influences the "transport" between blood and dialysate, determining the transmembrane transport efficiency of substances with different molecular weights. As the core component of the hemodialyzer, hollow fiber membranes retain proteins and cellular components in the blood while removing low-molecular-weight waste or harmful substances, such as urea.

Most domestic hemodialysis machine manufacturers rely on imported membrane products. As a high-tech consumable in blood purification, dialyzers face significant technical barriers in hollow fiber dialysis membrane spinning, preparation processes, and dialyzer encapsulation. Due to the lagging technical capabilities of local enterprises, domestically produced dialyzers suffer from low clearance rates and poor biocompatibility. Only a few companies, such as Jiangsu Langsheng and Shandong Weigao, can independently produce dialysis membranes; other manufacturers assemble dialyzers using imported membranes, which compresses the profit margins for domestically produced dialyzers.

In hemodialyzers, the import cost of a “tow” consisting of 10,000 hollow fiber membranes is $2–$2.5.

In ECMO systems, hollow fiber membranes enable blood to "breathe" outside the body. The centrifugal pump and membrane oxygenator are the two core components of ECMO. The oxygenator consists of hollow fiber membranes; during operation, oxygen flows through the lumen of the fibers, while blood circulates around their exterior. Carbon dioxide in the blood exchanges with oxygen in the fibers via a pressure gradient, thereby achieving blood oxygenation.

Hollow fiber membranes account for over 70% of the cost of ECMO products.LeadLeo Research Institute points out that the primary cost of raw materials for ECMO devices stems from core components such as solid silicone membranes, microporous hollow fiber membranes, and solid hollow fiber membranes. Notably, third-generation solid hollow fiber membranes are exclusively manufactured by Membrana, a subsidiary of 3M Company, with prices ranging from hundreds of thousands to millions of yuan. These core materials account for approximately 78% of the total production cost of ECMO devices, while other components necessary for the normal operation of ECMO equipment, such as electrical and electronic parts, constitute about 20% of the cost.

Filtration membranes are not only core components in biopharmaceuticals, ECMO, and hemodialysis products but also account for a significant proportion of costs; therefore, the domestic substitution of filtration membrane products is of great significance.

Among the diverse product categories in upstream life science tools, what is the market size for individual membrane material products?

An investor stated, “Currently, the market ceiling for filtration membranes is not particularly high. The hemodialysis sector relies almost exclusively on hollow fiber membranes, with the current annual market size for hollow fiber membranes in China’s hemodialysis field standing at approximately RMB 1.5 billion. In the biopharmaceutical industry, two main types of products are used: flat-sheet membrane cassettes (microfiltration and ultrafiltration cassettes) and hollow fiber membranes. The market size for filtration membranes in the biopharmaceutical sector is around RMB 2 billion, with an annual growth rate of approximately 30%; however, the filtration membrane industry holds significant future potential.”

In the future, the growth momentum of hollow fiber membranes will be driven by market expansion fueled by the development of the cell and gene therapy (CGT) industry.

Dr. Yin Zehua from Guanhuai Medical stated, “The CGT industry will drive the expansion of the hollow fiber membrane market. Macromolecular products such as CGT products, insulin, and mRNA have complex protein structures. These proteins are subjected to significant external forces during clarification and purification, which may lead to protein inactivation or reduced efficacy. Hollow fiber membranes are more suitable for protein-based drugs that are sensitive to shear stress.”

Currently, the market size for hollow fiber membranes in the biopharmaceutical sector is less than $1 billion, but it is poised for rapid growth alongside the development of the cell and gene therapy (CGT) industry. China has become a fertile ground for the global CGT sector, with more than 500 R&D enterprises and a clinical pipeline that has surpassed that of the United States for the first time, as new drugs gradually transition from research and development to commercialization. The rapid development of the domestic pharmaceutical industry has boosted market demand for critical filtration consumables used in drug manufacturing.

The use of disposable products will promote the growth of the flat-sheet membrane market.Flat-sheet membrane cassettes are primarily used in traditional vaccine and pharmaceutical applications. Historically, flat-sheet membranes were predominantly reused in biopharmaceutical processes; however, international companies are now widely promoting the shift toward single-use filtration membrane products, which is expected to expand the market size for flat-sheet membrane cassettes.

For domestic companies, a major opportunity for market growth lies in the import substitution driven by cost-control efforts among downstream CDMO enterprises.Whether flat-sheet membranes or hollow-fiber membranes, foreign enterprises still hold a significant market share in the pharmaceutical filtration consumables industry. Hollow-fiber membrane products used in the CGT sector are virtually absent from domestic production, relying entirely on imports.

Filtration membrane consumables account for a certain proportion of costs in pharmaceutical production. According to cost breakdown data for monoclonal antibody (mAb) production from Soochow Securities, equipment accounts for 48% of mAb production costs, consumables (such as filtration membranes and chromatography resins) account for 30%, and raw materials (such as culture media) account for 15%. Cost pressures from centralized procurement will drive domestic pharmaceutical companies and CDMOs to pursue cost-effective filtration process solutions.

International trade disputes have created an urgent need for stable supply chains among domestic biopharmaceutical companies, factors that will also drive biopharma and CDMO enterprises to increasingly opt for domestically produced products.

In terms of product quality and market recognition, multiple domestic enterprises have completed validation with key clients and accumulated industrialization experience, while downstream companies are actively promoting the substitution of imported filtration membrane products with domestically produced alternatives.

Overall, the future development of the CGT industry, the single-use trend for filter membranes and consumables, and domestic substitution will all serve as drivers sustaining high growth in the biopharmaceutical filtration membrane sector.

Chinese hemodialysis companies are driving stronger momentum for the domestic substitution of hollow fiber membranes.Hemodialyzers were included in a joint centralized procurement program across 18 provinces in 2022. This centralized procurement is expected to further compress corporate profit margins, imposing stricter requirements on cost control for hemodialysis machines. In response, domestic hemodialysis companies are increasingly establishing their own membrane material production lines.

However, hollow fiber membrane products have high technical barriers, making independent breakthroughs extremely challenging. Currently, the market share of domestically produced hemodialysis machines is increasing year by year and has approached 50%, leaving substantial room for the replacement with domestically produced membrane materials.

What gaps exist between domestic and imported enterprises in the critical market of membrane materials?

Let us first examine the major import participants in the filter membrane industry. The primary suppliers of filter membranes for China's biopharmaceutical industry include Cytiva, Merck, Danaher Pall, Sartorius, Asahi Kasei, and Repligen.

Dr. Yin Zehua introduced the characteristics of several major global players. Merck and Cytiva have integrated the entire biopharmaceutical value chain, spanning upstream processes such as cell culture and fermentation to downstream operations including clarification, purification, and filling. Large-scale domestic pharmaceutical manufacturers rely heavily on them. In the field of membrane materials, Repligen stands out as a leader in its niche. Repligen holds exclusive patents that are particularly advantageous for preventing cell clogging in membrane pores during perfusion culture, resulting in the highest market share for Repligen in the cell perfusion segment of the cell and gene therapy (CGT) sector. Another company, Asahi Kasei, holds over 50% of the market share in the final stage of biopharmaceutical manufacturing: virus removal filtration.

The domestic market has also evolved from a blank slate to nurturing multiple membrane material companies, including Hangzhou Cobetter, Guanhuai Medical, Shanghai Yike, Ailios, and Saipu Filtration.

Cobetter is dedicated to the research and development of various microporous filtration membranes, nanofibers, and ultrafiltration membranes, providing innovative filtration and purification solutions for global customers. Its products and technologies are widely applied in multiple industries, including biopharmaceuticals, chemical pharmaceuticals, medical devices, and semiconductor integrated circuits.

Cobetter is dedicated to creating comprehensive membrane-based solutions for all scenarios. Its membrane products serve high-end biomedical sectors such as gene therapy, vaccine production, and antibody drugs; address the mature blood purification market and the highly promising ECMO market; and also cover the water treatment market as well as the filtration consumables market for food and medical applications.

Shanghai Yike possesses two major technology platforms: catheters and hollow fiber membranes. In the field of biomedical membrane materials, Shanghai Yike has passed downstream customer testing for both high-flux and low-flux hemodialysis membranes.

Aelios, founded in 2021 and backed by Matrix Partners China and Legend Capital, specializes in the development and application of process-supporting technologies for pharmaceutical manufacturing. The company is committed to providing high-quality separation and purification solutions that comply with domestic and international regulatory requirements.

What gaps still exist between domestic enterprises and importers?

Dr. Yin Zehua candidly stated, “Chinese enterprises have achieved breakthroughs from scratch, starting with the foundational technologies of membrane materials. Currently, they are focusing more on the membrane materials themselves, and our membrane products are already comparable to imported ones. However, in the biopharmaceutical industry, it is not enough to simply produce high-quality membrane products; we also need to assist customers in process exploration and ensure seamless integration between upstream and downstream operations. Overseas companies such as Danaher and Merck cover the entire upstream and downstream industry chain and enjoy stronger brand recognition. This is their advantage, and also an area where Chinese enterprises need to improve.”

Gaps certainly exist, but hope is far from dim. It is foreseeable that domestic enterprises will continuously expand their capability boundaries and unlock new avenues for development.

To break free from constraints and secure autonomy over the industrial chain, China’s membrane material industry needs to achieve breakthroughs from the ground up. Domestic enterprises are tracing the supply chain to tackle key products; some are expanding upstream from downstream segments, while others are deeply engaged in R&D of critical membrane materials. Several companies have already obtained validation from key customers. Chinese firms are carving out opportunities in the industry and are poised for robust growth in the future.

References:

Prospectus of Chongqing Sunwawa Blood Purification Technology Co., Ltd.

Upstream Life Sciences in Biopharma: Industry Development Accelerates, Seizing New Opportunities for Domestic Substitution — China Merchants Bank

Deepening Domestic Substitution of Hemodialysis Equipment, Vaccine Syringes Contribute to Incremental Growth - Huaan Securities

Critical Care Treatment Sparks Surge in ECMO Demand, but Key Membrane Materials Relied on Sole Global Supplier — Yicai