Hospital SPD Model: Amid Industry Controversies, 91-Fold Growth in 6 Years Attracts Major Players

"Distributors have long suffered under SPD."

“Charging a 20% service fee is simply outrageous!”

Recently, we have heard mixed reviews about the SPD market.

SPD is aIntegrated Management Model for Hospital-Wide Medical Supplies, namely Supply, Processing, and Distribution, can help hospitals reduce costs and improve efficiency in supply chain management.

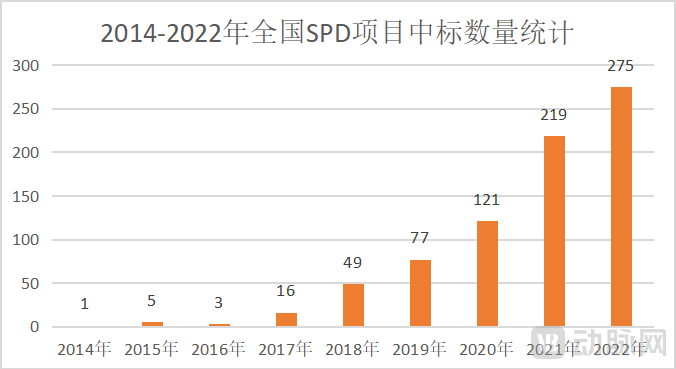

Despite considerable controversy, SPD has demonstrated a trend of rapid growth. According to data from Zhongcheng Medical Devices, there were only three SPD projects awarded in China in 2016, whereas by 2022, the number of awarded SPD projects had surged to 275.6-Year Surge Exceeds 91-Fold。

(Number of SPD Project Bids Won Nationwide in China, 2014–2022; Data Source: Zhongcheng Medical Devices)

According to estimates by the Medical Device Supply Chain Branch of the China Federation of Logistics & Purchasing: Given the rapid growth trend observed in the past two years, the number of medical institutions in China implementing medical device SPD (Supply, Processing, and Distribution) projects is expected to exceed 1,200 by the end of 2023.

Behind the Rapid Growth: Why Is SPD Highly Favored by Hospitals, Yet Mired in Controversy? Can This Industry Achieve More Orderly Development in the Future? VCBeat Provides an Overview.

Prior to 2019, medical consumables constituted a significant source of revenue for hospitals, which were permitted to charge a markup over the procurement cost of these supplies.

However, with the implementation of the “Zero Markup on Consumables” policy and the “Two-Invoice System,” medical consumables have gradually shifted from being profit centers to cost centers. The “Zero Markup on Consumables” policy requires hospitals to sell consumables to patients at their purchase price, without adding any fees; meanwhile, the “Two-Invoice System” eliminates intermediate distribution links and reduces profit margins.

When consumables management becomes a cost center, issues previously masked by high profit margins gradually come to light. According to Zhang Wei, General Manager of Haiyu Medical, “The traditional model for managing medical supplies is relatively extensive and inefficient, which not only increases hospital expenditures and burdens healthcare staff but also impairs the operational efficiency of supply logistics.”

In this context, the SPD model, which can enhance the refined management of medical supplies, reduce labor costs, and improve supply chain management efficiency, has emerged as the trend dictates and rapidly become a “favorite” among hospitals.

According to VCBeat, SPD (Supply, Processing, and Distribution) involves the integrated planning of procurement management, inventory management, distribution management, and consumption management. It aims to “let logistics handle logistics, and let clinical staff focus on clinical care,” while leveraging information technology and the Internet of Things (IoT) to enhance logistical efficiency and reduce management costs. Specifically,Through SPD, hospitals can achieve refined supply chain management, full-process traceability of high-value consumables, significant reduction in logistics management costs, and improved efficiency in medical supplies management.。

It can be seen that, based on the advantages of the SPD model and the trend toward smart hospitals,Some Regions Have Incorporated SPD into the Accreditation of Tertiary Hospitals, as stipulated in the "Anhui Province Implementation Rules for the Tertiary Hospital Accreditation Standards (2020 Edition)" issued by the Anhui Provincial Health Commission in 2021, which recognizes "the implementation of full-process standardized management of medical consumables using SPD" as the highest-level Grade A standard;Some Regions Are Accelerating the Adoption of SPD in Hospitals, such as the Guizhou Provincial Health Commission’s issuance of the “Implementation Plan for the Three-Year Improvement Program for Smart Hospitals in Guizhou Province (2021–2023),” which proposes advancing intensive hospital operational services through technologies such as Supply, Processing, and Distribution (SPD).

Bolstered by supportive policies, the SPD industry has experienced rapid growth. Meanwhile, industry insiders predict that,The SPD Model Will Become the Mainstream Approach for Hospital Supply Chain Management in the FutureHowever, at present, based on the existing market stock of public hospitals, the penetration rate of SPD projects in public hospitals across China is only about 5%, indicating significant room for future growth. Data released by Probe Capital shows that the SPD services market will reach RMB 35.22 billion per year.

Amid the promising prospects of the SPD industry, THALYS MEDICAL TECHNOLOGY GROUP CORPORATION upgraded its RMB 108 million business to the SPD model, while Liuzhou Pharmaceutical Co., Ltd. also spent RMB 1.17 billion to secure its entry into the SPD market.

Meanwhile, the four major medical device distribution giants—China Resources Pharmaceutical, Sinopharm Holding, Shanghai Pharmaceuticals, and Jointown Pharmaceutical Group—as well as the recently listed Guoke Hengtai, are all positioning themselves in this market; while innovative enterprises such as Fenghe Technology, Guoyi Technology, Haiyu Medical, Derong Medical, Wanxu Health, Yibei, Weimeng, Tute, Aihui, and Lianzhong Wisdom are entering the market as third-party providers.

As more enterprises enter the market, the SPD industry will become increasingly vibrant.

From three successful bids in 2016 to 275 in 2022, the rapid growth of SPD projects has relied not only on policy support but also on the value they deliver, which is key to gaining hospital recognition.

Under the SPD model, SPD enterprises will deploy a professional operations management team within the hospital to handle the procurement, inventory management (inbound and outbound), distribution, and overall management of medical consumables, thereby alleviating the workload of hospital staff.

Meanwhile, SPD providers also supply hospitals with both software and hardware solutions to enhance management efficiency. On the software front, SPD providers customize and deploy in-hospital consumables logistics management systems tailored to each hospital’s specific needs.

In terms of hardware, SPD enterprises are required to establish a central warehouse within the hospital or upgrade existing warehouses into smart central warehouses. Upon acceptance, consumable distributors or suppliers deliver medical consumables directly to the central warehouse, where an SPD professional team manages inventory through activities such as coding, RFID chip installation, distribution, stocktaking, and maintenance.

Additionally, at points of consumption for medical supplies such as operating rooms, laboratories, and anesthesiology departments, SPD providers customize the deployment of smart devices and auxiliary hardware—including RFID-enabled supply cabinets, intelligent sensing cabinets, smart shelves, logistics robots, and barcode scanners—based on the specific needs of each department. Staff can directly retrieve supplies from the intelligent sensing cabinets or smart shelves when needed.

During use, hospital staff can set upper and lower usage limits for consumable products in advance. When replenishment conditions are triggered, the SPD service team will proactively deliver supplies; no delivery is required when inventory is sufficient. Meanwhile, when using consumables, hospital staff can either scan the QR code or place the RFID electronic chip of the corresponding consumable into the return cabinet, allowing the SPD in-hospital consumable logistics management system to record that the product has been consumed. Unused excess consumables can be returned to smart shelves or smart sensing cabinets for future use, and the system will update the records accordingly.

(SPD Business Service Model, sourced from Thalys Medical's 2022 Annual Report)

By leveraging information technology and Internet of Things (IoT) applications, the central warehouse can proactively acquire consumption data for medical supplies at point-of-use locations. Based on pre-defined upper and lower threshold standards, it can automatically perform picking, processing, and replenishment. Compared to the traditional model of “requisition submission, departmental procurement, supplier delivery, inspection and warehousing, and warehouse dispatch to point-of-use,” the proactive distribution of consumables enabled by SPD (Supply, Processing, and Distribution) undoubtedly offers higher efficiency.

Statistics show that after implementing the SPD model, the inventory turnover days for consumables in relevant hospital departments decreased from 15 days per cycle to an average of 2 days per cycle, significantly reducing the time spent on cleaning, inventory counting, and organization. After Lingwu People's Hospital implemented the SPD system, the average consumable cost ratio in key departments such as the Clinical Laboratory, Operating Room, Orthopedics, and General Surgery decreased by 4.28% year-on-year, while the hospital’s average consumable cost per 100 yuan of medical revenue dropped by 9.82% over the same period.

Notably, in June 2020, the National Health Commission issued the "Operational Manual for Performance Assessment of National Tertiary Public Hospitals (2020 Edition)," adding the indicator "proportion of revenue from high-value medical consumables." Consequently, reducing the proportion of consumable costs has become one of the quantifiable monitoring and assessment indicators for public hospitals across China. The application of SPD can help hospitals reduce this proportion.

As the SPD model delivers high-value returns to hospitals, their recognition of it has correspondingly increased, with the number of successful bids surging 91-fold over six years.

Currently, in the SPD market, medical device distribution giants such as China Resources and Sinopharm hold the majority share.

According to statistics from the Medical Device Supply Chain Branch of the China Federation of Logistics & Purchasing, 87% of SPD projects are currently operated by medical device commercial enterprises (such as China Resources and Sinopharm), predominantly by national-level distributors and leading regional players. However, in the SPD software market, Haiyu Medical and Wanxu Health have secured significant shares, accounting for 28% and 25%, respectively.

Although all parties provide SPD services, their objectives differ. Third-party SPD service providers aim to help hospitals reduce supply chain management costs and enhance the precision of medical supplies management, thereby securing corresponding commercial returns based on the value delivered.

Unlike third-party SPD operations service providers, which focus more on the delivery of services themselves, medical device commercial enterprises have a stronger demand for leveraging SPD to enhance commercial value and market share.。

According to the annual report released by Sinopharm Group Co., Ltd., 72 new SPD (Supply, Processing, and Distribution) projects were added during the year. This has helped the Group achieve steady growth in project revenue while gradually expanding the scope of in-hospital consignment management and service offerings. Looking ahead, the Company will vigorously expand green and smart supply chain services, such as SPD and centralized distribution, strengthen its professional service capabilities, continuously broaden value-added services, and drive an increase in market share.

The prospectus of Guoke Hengtai reveals that the company has achieved rapid growth in its number of end-user medical institution clients through self-developed solutions, collaborations with local resource providers, and winning bids for SPD (Supply, Processing, and Distribution) operational management. Driven by the increase in end-user hospital clients, the company’s direct sales revenue has grown rapidly, thereby propelling a high-speed expansion of its overall operating revenue.

Thalys Medical also pointed out in its annual report: Within the existing intensive customer system, the company strives to introduce its self-produced products as well as distributed equipment and reagents, thereby strengthening customer stickiness and enhancing the sustainability of business volume and profits. Meanwhile, Thalys Medical stated that regarding the selection of SPD (Supply, Processing, and Distribution) service models, its third-party service model does not involve operational business activities, resulting in greater transparency in its operational status and reducing management pressure and risks for hospitals.

This shift in strategic orientation has led many industry insiders to worry that medical device commercial enterprises are “acting as both referee and player,”Major suppliers serve as SPD operators while also having access to service data from other vendors,Impact on Internal Control Risks in Hospitals,Resulting in unfair business competition.

In response to this issue, some large tertiary hospitals have begun to restrict the eligibility of SPD service providers. For instance, The First Affiliated Hospital of Sun Yat-sen University explicitly stated in its tender documents for medical consumable SPD services that bidders must not have any sales business relationship with the tenderee regarding medical consumables. Similarly, Xi’an No. 1 Hospital also required in its tender for the smart supply chain project for SPD pharmaceuticals that bidders must not have any business relationship with the tenderee.

“Third-party SPD providers that return to the essence of service are more compliant, better able to deliver professional and reliable SPD services, and more aligned with hospitals’ development needs; they will become the major players in the SPD market in the future.” This interpretation was also offered by a relevant executive at Fenghe (Beijing) Technology Co., Ltd.

Previously, an SPD service provider at a hospital in Sichuan charged a 20% service fee, triggering strong backlash from its partners. In fact, this issue is rooted in the business model of SPD enterprises.

Currently, there are three primary business models in China's SPD industry:

1. Single centralized distribution share model, the SPD operator is the sole distributor;

2. Service Fee Collection Model, SPD companies charge service fees based on a certain percentage of the total purchase price of medical consumables supplied to hospitals. For instance, if a hospital procures RMB 3 billion worth of consumables annually and the service fee rate is set at 5%, the SPD company would generate RMB 150 million in revenue;

Third, the model combining centralized distribution share with platform service fees, the SPD operator distributes its market share among multiple centralized distribution providers, who in turn pay a certain percentage of service fees to this operator.

Currently, the predominant business model in the SPD industry is the service fee-based model. According to incomplete statistics, medical device SPD service fees primarily range from 1% to 3%, varying by region and project scale.

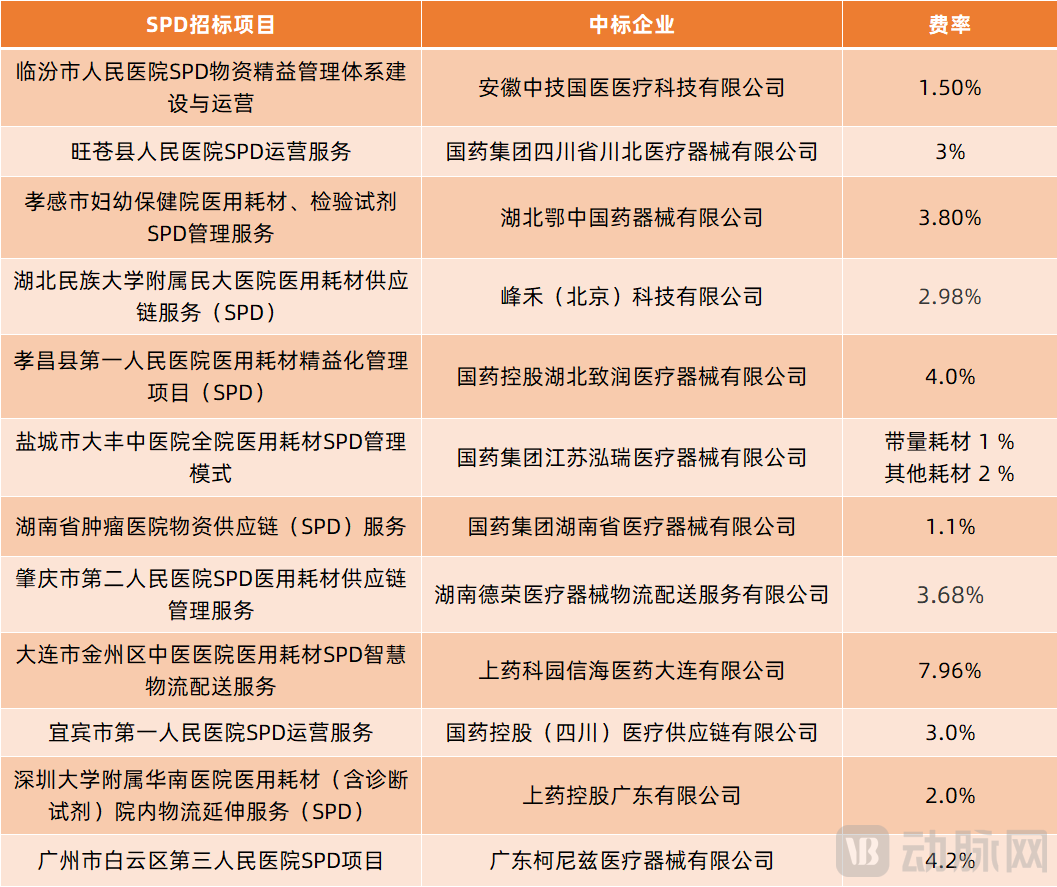

(Partial SPD Project Bid Winning Status from 2022 to 2023)

However, behind the rapid growth of the SPD industry, there has also been a mix of reputable and questionable players. Some engage in low-price competition to capture market share, while others rely on regional monopolies to charge exorbitant service fees. For instance, certain SPD companies that previously sparked controversy by charging a 20% service fee fall into this latter category.

For hospitals, if the management fee rate is set unreasonably or lacks a regulatory coordination mechanism, it may have a negative impact on the supply of medical consumables. For example, if the service fee rate is too high, suppliers/agents may refuse to supply goods or increase the supply price; if the service fee rate is too low, SPD companies may operate at a loss, affecting their supply chain management effectiveness and impacting the stability of the hospital's supply chain.

Due to the relatively short development history of the SPD industry, there are currently no established standards for setting service fee rates. In practice, SPD service providers charging service fees of 1%–3% are generally well accepted by their partners. Regarding the issue of service fee rates, Haiyu Medical has also provided us with a directional recommendation: determine service fee rates based on cost composition.

Zhang Wei, General Manager of Haiyu Medical, stated: “The total investment in SPD projects includes software, intelligent hardware, warehouse renovation, operational staff, and equipment depreciation. Some projects also incur additional costs such as rent for off-site warehouses and vehicle purchases.”Reasonable service fee rates must be calculated based on the total investment costs and the contract term signed with the SPD service provider; otherwise, it is difficult to achieve a win-win outcome for hospitals, suppliers, and SPD enterprises.”

Currently, the SPD industry is still in its early stages of development, with many avenues yet to be explored.

For example, in the pharmaceutical distribution sector, hospitals typically have payment terms ranging from one to six months, or even longer. This imposes significant financial pressure on suppliers. If SPD providers introduce supply chain finance solutions to address challenges related to payment cycles and capital constraints, SPD will deliver greater value and potentially generate higher commercial returns.

For another example, some SPD enterprises have begun to explore the transition from serving a single hospital to serving multiple hospitals within a region. This shift involves more than just an increase in the number of hospitals served; it also requires corresponding adjustments to the SPD enterprises’ operational models, warehouse configurations, and staffing arrangements.

Not only is the service area expanding, but the scope of SPD services is also continuously growing. Previously, SPD management primarily focused on medical consumables; in the future, SPD will also be applied to pharmaceuticals, in vitro diagnostics, and other fields.

Furthermore, the information technology and Internet of Things (IoT) technology underpinning SPD systems require continuous iteration. Smart hardware, such as intelligent logistics robots, smart cabinets, and intelligent chips, will see broader application, ultimately enabling refined management down to the level of “a single pack of cotton swabs.”

Even though some irrationalities persist at present, it is believed that the SPD market will gradually become more standardized as the industry develops.