2023 Microfluidics Industry Report: Global M&A Exceeds $140 Billion, with POCT, Single-Cell Sequencing, and Digital PCR Driving Rapid Adoption

Following the rise of point-of-care testing (POCT), emerging fields such as single-cell sequencing and digital PCR are becoming new hotspots for microfluidic technology applications. Areas that have long utilized microfluidics, such as circulating tumor cell (CTC) enrichment and sorting, are currently undergoing rapid technological iteration. Organ-on-a-chip systems, which have seen vigorous development in the past two years, rely on microfluidic chips as their core component. Novel approaches to high-performance microsphere fabrication based on microfluidic chips have achieved industrial-scale production breakthroughs in recent years, propelling microfluidic technology from an era focused on reactions into one centered on manufacturing. The integration of emerging technologies such as electrochemistry and CRISPR with microfluidics is demonstrating significant development potential...

Microfluidics technology is bringing about transformative changes to our era and is currently on the cusp of a technological explosion.Which track will see the first “killer app” emerge? How will the “rising tide” of microfluidics technology activate the “pool of spring water” comprising both traditional and emerging technologies?

VCBeat.Over 100 Leading Microfluidics Companies WorldwideConducted in-depth research, and withMultiple domestic microfluidics experts, investors, and core executives from nearly 30 companiesThrough in-depth discussions, we aim to present the latest industry development landscape of the microfluidics sector to industry readers, and uncover hidden opportunities and future trends by examining the current challenges faced by the industry and the solutions contributed by industrial stakeholders.

Below are the core insights and table of contents of the report:

Non-disruptive technologies, creating disruptive applications; killer apps are rapidly emerging.Whether leveraging microfluidic chips to achieve miniaturization and integration of laboratory processes (e.g., in the fields of IVD and new drug development), employing them as micro-generators for applications such as CTC enrichment and sorting, or utilizing them as production equipment for tasks like microsphere fabrication, microfluidics itself is not a disruptive technology. However, as an enabling technological tool, it has created potentially disruptive applications. While a killer application for microfluidics has yet to emerge, it is rapidly taking shape.

POCT has become the most widely applied field for microfluidics technology, with multiple products successfully commercialized.Microfluidics is the foundational core technology enabling the integration and miniaturization of point-of-care testing (POCT) devices. Its high alignment with the development trends of POCT products has made POCT the most widely applied and mature field for microfluidics at present. Among the 81 companies in China applying microfluidic technology, nearly half (36 companies) have positioned their business scenarios in POCT. Furthermore, eight of the target companies in the top ten global M&A transactions were primarily engaged in the development of microfluidic POCT products. Currently, multiple microfluidic products have been successfully commercialized worldwide and have received favorable market responses.

Unearthing New Blue Oceans: The Commercial Potential of Emerging Sectors Begins to Emerge.Following the rise of POCT, the application of microfluidics in single-cell sequencing and digital PCR has become a new hotspot for capital investment. The field of molecular diagnostics, characterized by relatively low levels of automation and high profit margins, is emerging as the primary battleground for microfluidic applications. Areas such as molecular POCT, digital PCR, and cell enrichment and sorting are seeing vigorous adoption, with 24 companies actively positioning themselves in these sectors. Emerging markets like organ-on-a-chip, microsphere fabrication, and assisted reproductive technologies are beginning to demonstrate commercial potential, offering opportunities for disruptive, killer applications to emerge. Looking ahead, the integration of microfluidics with emerging technologies such as CRISPR, electrochemistry, and super-resolution microscopy holds significant promise.

![]ONO]](AY@XC`OMH)US6(IR.png](http://cdn.vcbeat.top/upload/image/00/07/27/47/1690418856740322.png/dmw)

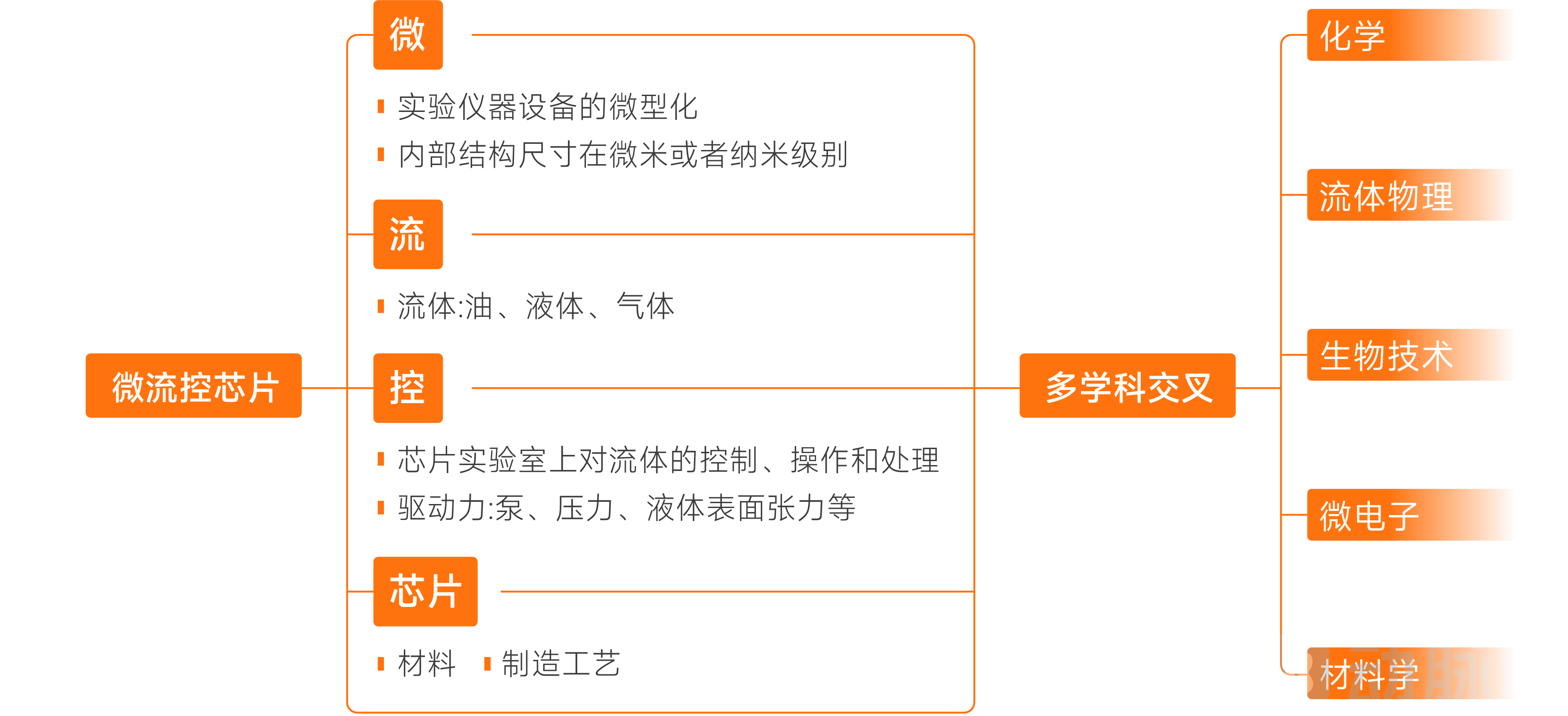

Microfluidics(Microfluidics) refers to the science and technology involved in systems that process or manipulate minute fluid volumes (ranging from microliters, nanoliters, down to attoliters) using microchannels (with dimensions of tens to hundreds of micrometers). It is an emerging interdisciplinary field encompassing chemistry, fluid physics, microelectronics, new materials, biology, and biomedical engineering. At this scale, fluid motion is typically dominated by surface forces (such as surface tension and viscous drag) rather than body forces (such as gravity and inertia).

Research Foundation of Microfluidic Chips

Source: Public information; chart by VCBeat.

Due to their miniaturization and integration, microfluidic devices are often referred to as microfluidic chips or lab-on-a-chip systems.

It involves constructing a miniature laboratory analysis platform on a chip measuring just a few square centimeters or even smaller. This technology integrates fundamental operational units from the fields of biology and chemistry—such as sample preparation, reaction, separation, detection, cell culture, sorting, and lysis—onto a single compact chip. A network of microchannels facilitates controlled fluid flow throughout the system, enabling it to perform various functions typical of conventional chemical or biological laboratories. These functions include the rapid and accurate processing, detection, and analysis of proteins, nucleic acids, cells, and other specific targets.

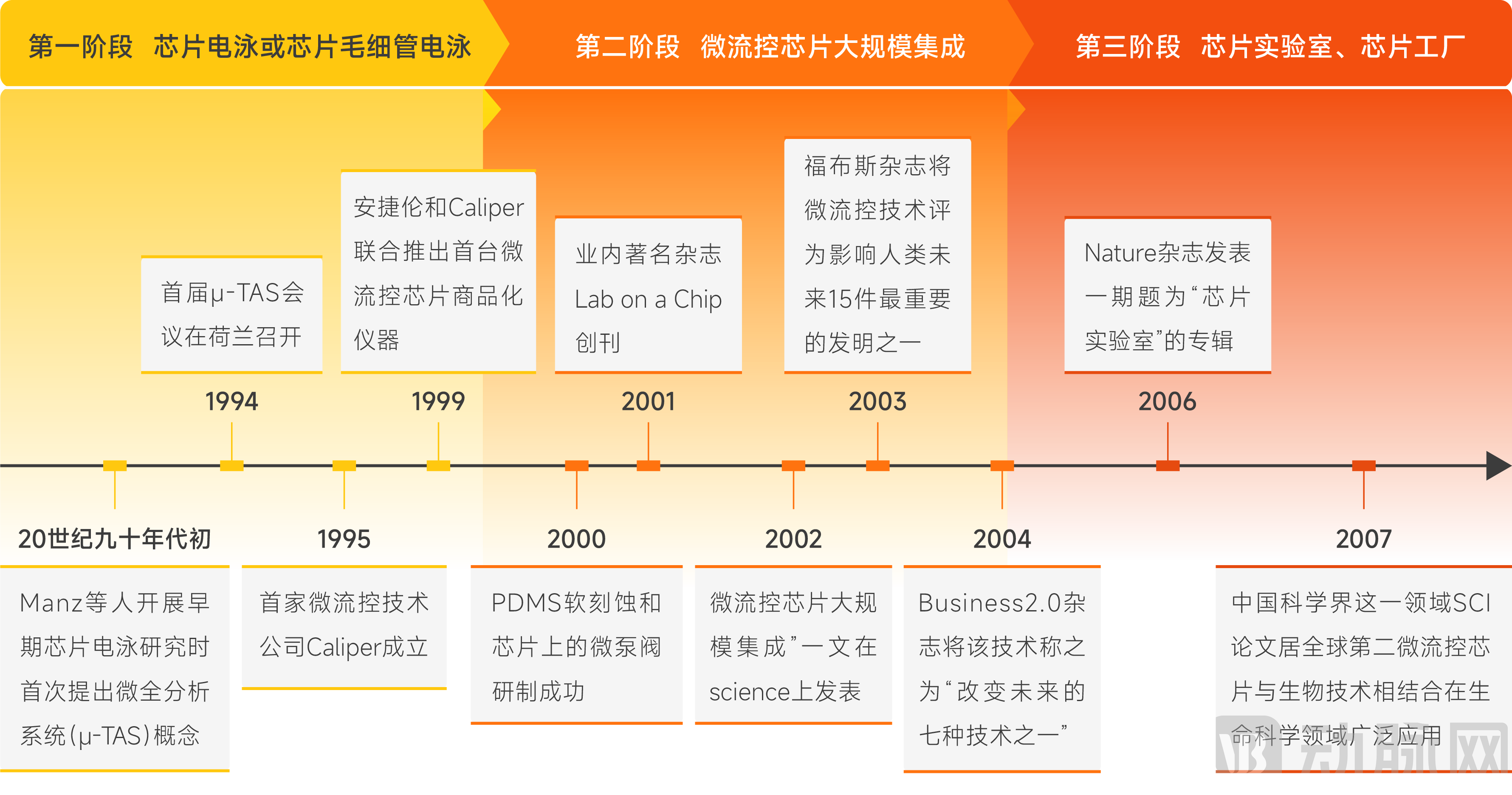

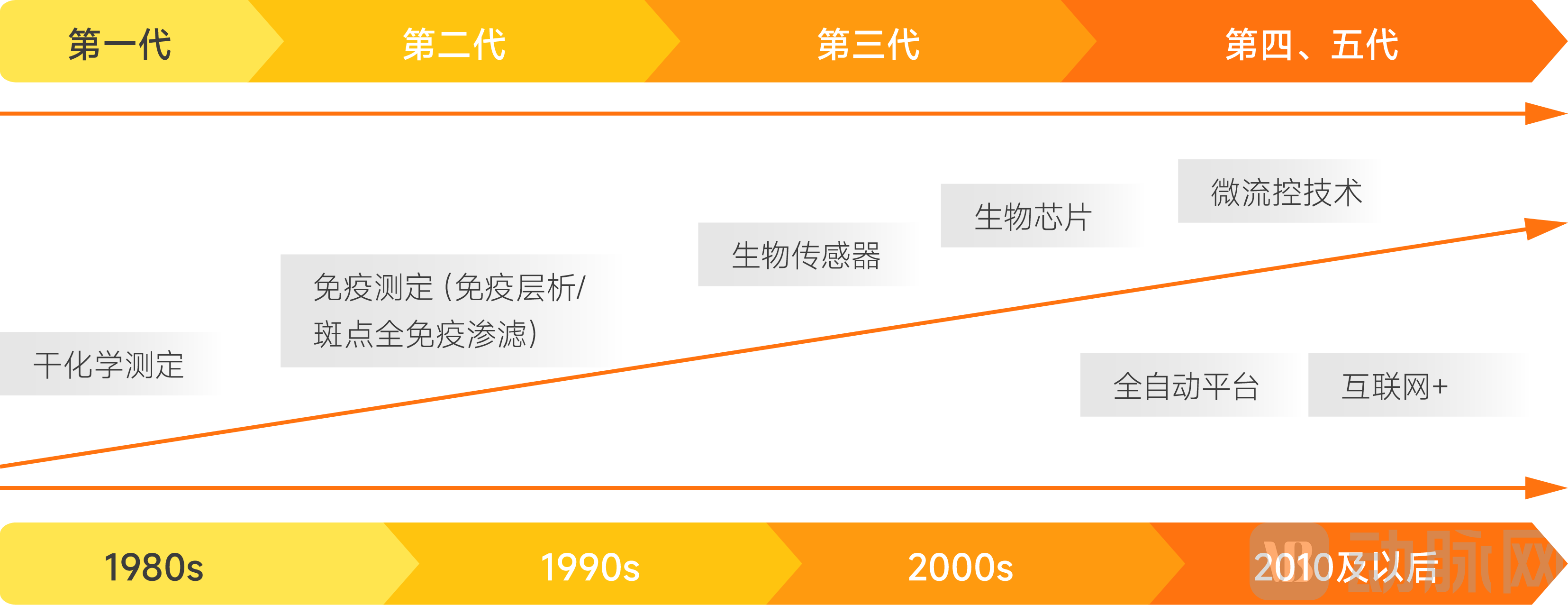

Development History of Microfluidics Technology

The concept of microfluidic chips was proposed in the early 1990s by A. Manz et al. Worldwide research began in the mid-to-late 1990s, and its development has generally undergone three stages.

The Development History of Microfluidic Chips

Source: Public information and research interviews; chart by VCBeat.

Phase I (1990–2000): Microfluidic chips were regarded as chemical analysis platforms and were often used interchangeably with the concept of “Micro Total Analysis Systems.” Subsequent practice has demonstrated thatMicro total analysis systems are merely one category within microfluidic chips, far from representing the entirety of the field.

Phase II (2000–2006): Academia and industry increasingly recognized that microfluidic chips far transcended the concept of “Micro Total Analysis Systems,” representing a critically important platform with the potential to evolve into a major scientific and technological discipline.

For example,By leveraging microfluidic chips as micro-reactors, combinatorial chemical reactions can be conducted on-chip for analytical diagnostics. Alternatively, when integrated with droplet technology, these systems facilitate drug synthesis and screening, as well as the high-throughput, large-scale production of nanoparticles, microspheres, crystals, and other materials, thereby creating a “chemical or pharmaceutical plant on a chip.”

Phase III (2006–Present): Microfluidics has been widely applied in analytical and detection processes within the biological and chemical fields, achieving commercialization in areas such as in vitro diagnostics (IVD), cell sorting, and organ-on-a-chip technologies.

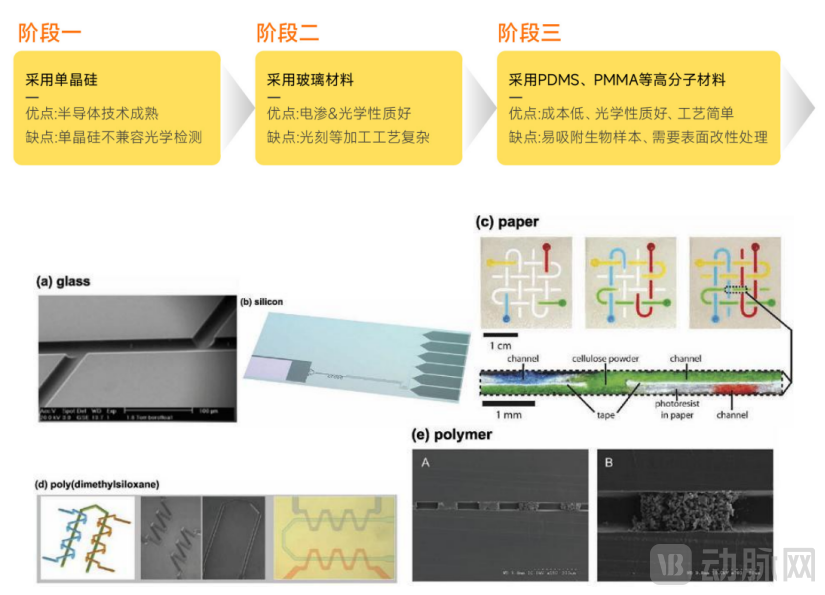

From semiconductors to polymer materials, and from photolithography to molding, the exploration of microfluidic materials and process technologies is progressively deepening.Organic polymer materials, represented by polydimethylsiloxane (PDMS), are currently popular materials for the fabrication of microfluidic chips. In terms of fabrication processes, techniques widely used in microfluidic chip manufacturing include photolithography, etching, molding, hot embossing, LIGA technology, laser ablation, and soft lithography.

Evolution of Microfluidic Chip Materials and Microfluidic Chips of Different Material Types

Source: Public information; chart by VCBeat.

Comparison of the Advantages and Disadvantages of Microfluidic Chips with Different Material Types

Data Source: Public information; chart prepared by VCBeat.

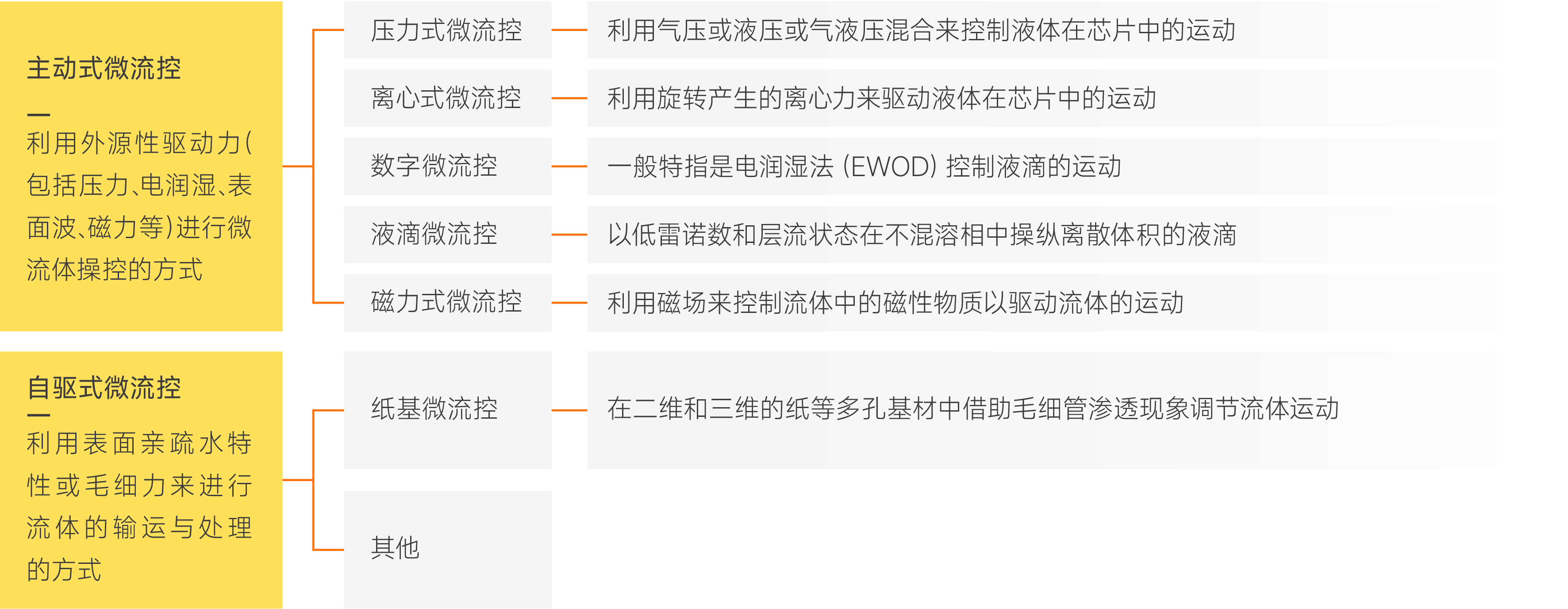

Different Fluid Control Strategies, Classified as Passive and ActiveCurrently, commercialized products primarily rely on active driving forces such as aerodynamic and centrifugal forces, with some incorporating passive driving mechanisms.

Microfluidic Technology Under Different Fluid Control Strategies

Data source: Public information; chart by VCBeat.

Advantages of Microfluidics Technology and Its Industry Value

Microfluidic chips are composed of components such as micron-scale fluidic channels and reactors. Compared with macroscopic analytical devices, their structure significantly increases the surface-area-to-volume ratio of the fluidic environment, thereby maximizing the utilization of special properties associated with liquid–solid interfaces, including laminar flow effects, capillary effects, rapid heat transfer, and diffusion effects. This enables a series of experimental processes—such as sample introduction, pretreatment, molecular biology reactions, and detection—to be completed on a single chip.

Specifically, microfluidic chips offer four major advantages: (as detailed in the original report, not elaborated here)

Four Major Advantages of Microfluidic Chip Technology

Source: Survey interviews; chart by VCBeat.

As an enabling technology, it drives the emergence of disruptive applications.Whether leveraging microfluidic technology to achieve miniaturization and integration of laboratory processes (such as applying microfluidics in the fields of IVD and new drug development), utilizing microfluidic chips as micro-generators (for instance, for the enrichment and sorting of CTCs), or employing microfluidic chips as production equipment (such as for the fabrication of microspheres)... Microfluidics itself is not a disruptive technology, but as an enabling tool, it has created potentially disruptive applications.

A Rapidly Growing $10 Billion Market: China Is Poised for Takeoff

2021-2027 Market Forecast for the Microfluidic Chip Sector

![X[C_WQ`]~(H[9Y(((5P$Q}U.png](http://cdn.vcbeat.top/upload/image/07/07/26/28/1690356509473149.png/dmw)

Data source: Yole Développement

According to the research report “Status of the Microfluidics Industry 2022” published in July 2022 by Yole Développement, an international MEMS-focused consulting firm,The global microfluidic chip industry was valued at $18.1 billion in 2021, and the market share is projected to reach $32.3 billion by 2027, representing a compound annual growth rate (CAGR) of 10.1% from 2021 to 2027.

Among these, the microfluidic device market grew from $2.5 billion in 2017 to $5.8 billion in 2022, with a compound annual growth rate (CAGR) of 18%; the microfluidic product market expanded from $9 billion in 2017 to $23 billion in 2022, at a CAGR of 21%.

In terms of market segments, the top three areas by microfluidics market share are projected to be as follows by 2027:Point-of-Care Testing(Point-of-Care Diagnosis, POC Dx)、Pharmaceutical and Life Sciences ResearchandClinical Laboratory Testing, with market shares of $11.3 billion (CAGR 9.1%), $9.4 billion (CAGR 13.1%), and $8.6 billion (CAGR 10.3%), respectively.

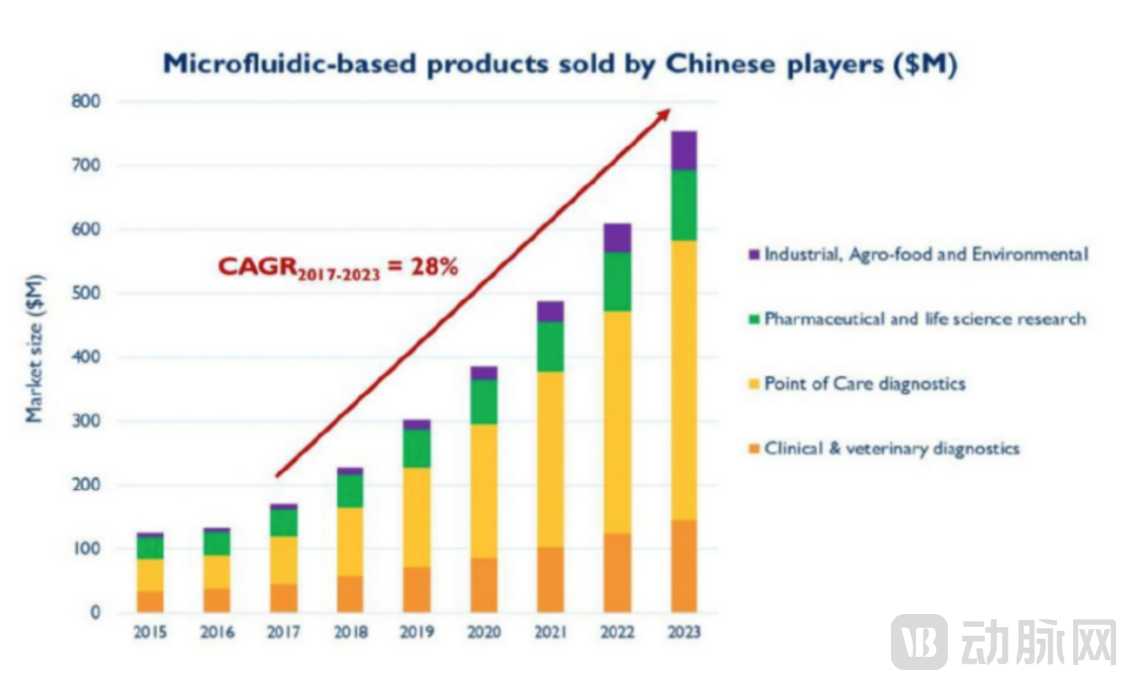

Sales of Microfluidic Chip-Related Products in the Chinese Market

Data source: Yole Développement

The development of China's microfluidics market is still in its early stages but is growing rapidly.According to Yole’s statistics, the size of China’s microfluidics market in 2017 was approximately USD 552 million. Among this, international brands achieved sales of USD 368 million for their microfluidics products in China, accounting for 67% of the market share. Sales of domestically produced microfluidics products reached approximately USD 171 million, representing a 33% share.

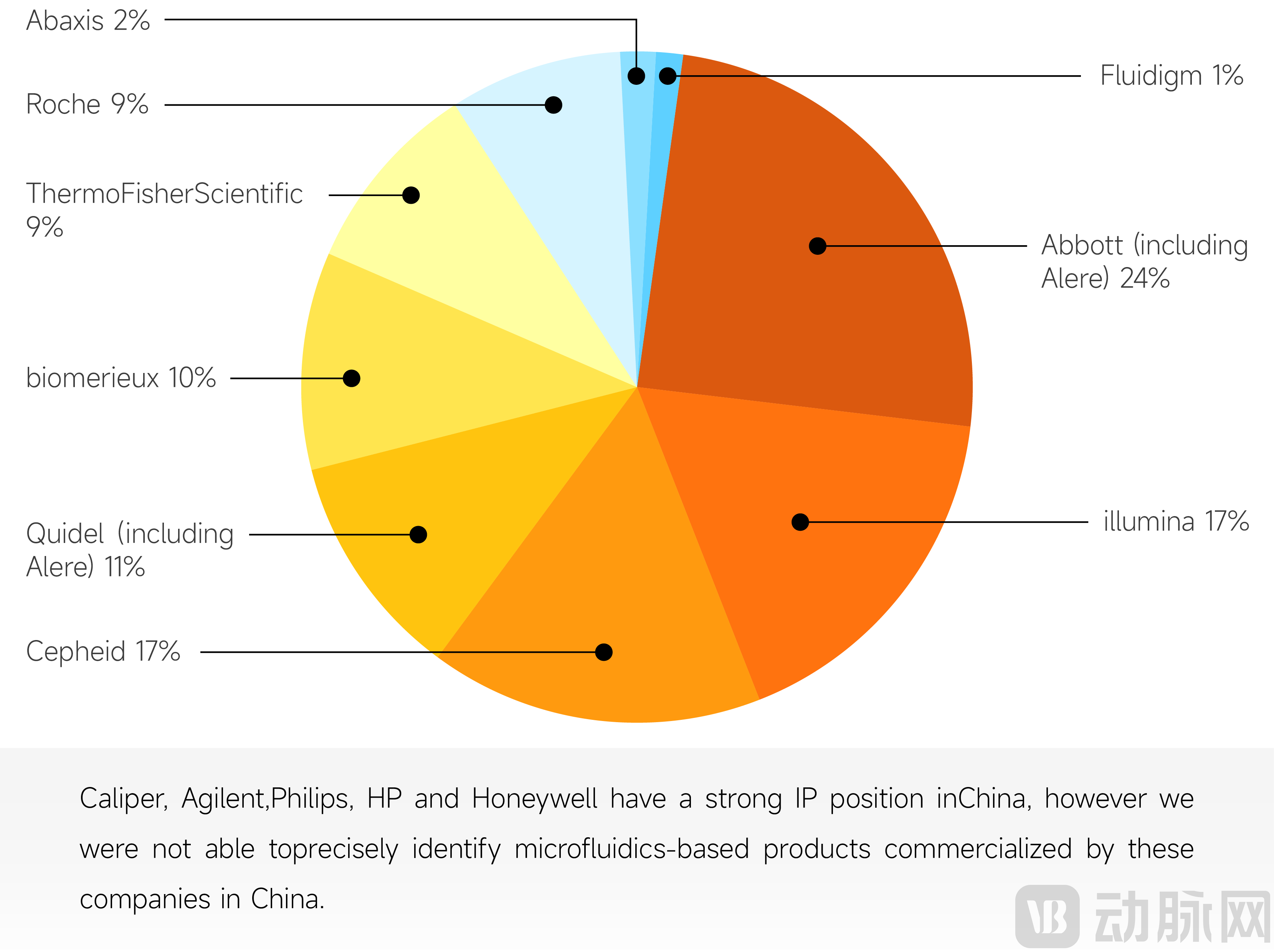

Companies Holding the Majority Market Share in China's Microfluidics Market

Source: Public information; chart by VCBeat.

The rapid development of POCT and other fields has generated strong demand for microfluidics technology

Currently, the primary application scenarios for microfluidics technology are Point of Care Testing (POCT), pharmaceuticals, and life sciences research. The robust growth in these sectors, coupled with strong demand for microfluidic solutions, constitutes a major driver behind the advancement of the microfluidics field.

Factors such as China’s entry into an aging society, rising per capita consumption, heightened health awareness among residents, and government promotion of tiered diagnosis and treatment have driven the rapid development of the POCT industry, with most POCT products relying on microfluidics technology for support.

The development of POCT technology has undergone four evolutionary stages: qualitative, semi-automated quantitative, semi-quantitative, and fully automated quantitative products. With gradual improvements in precision and automation, the ultimate trend is toward miniaturization, user-friendly “foolproof” designs that require no specialized personnel, and simple operation where bodily fluid samples can be directly input to rapidly obtain diagnostic results. This information is then uploaded to a remote monitoring center for physician-guided healthcare management. The characteristics of microfluidics technology align closely with the development trends of POCT, making it increasingly the core technology for building POCT systems.

The Development History of POCT Technology

Data source: Public information; chart by VCBeat.

In the pharmaceutical and life sciences research sectors, the development of organ-on-a-chip technologies, centered on microfluidic chips, is advancing rapidly.Driven by the pharmaceutical industry’s demand to overcome the Eroom’s Law dilemma, regulatory support from the FDA, the global trend toward animal-free testing, and phased technological breakthroughs, multiple factors are accelerating the rapid development of the Organ-on-a-chip (OOC) field, making it an emerging area of intense interest within the industry.

Furthermore, some companies leverage microfluidics technology for drug delivery to achieve superior administration methods, or utilize microfluidic chips for high-performance microsphere preparation to provide purification resins and controlled-release drug formulations for the downstream biomedical sector. Others employ microfluidics-based manipulation at the single-cell, microbial, and molecular levels to empower antibody drug development, CAR-T cell screening, optimization of cell therapy targets, gene editing, nucleic acid isolation and quantification in cell biology, DNA sequencing, and DNA synthesis.

Microfluidics technology is unleashing significant application potential in the pharmaceutical and life sciences research fields.

Multiple Policies Introduced: Nearly RMB 6 Billion Injected into China’s Market Over the Past Five Years to Drive Rapid Industry Growth

Given the immense application prospects of microfluidics, the Chinese government has continuously strengthened policy support for microfluidics-related fields in recent years.

Relevant Policies in China Supporting the Development of the Microfluidics Industry

Data Source: VBInsight; Chart by VCBeat

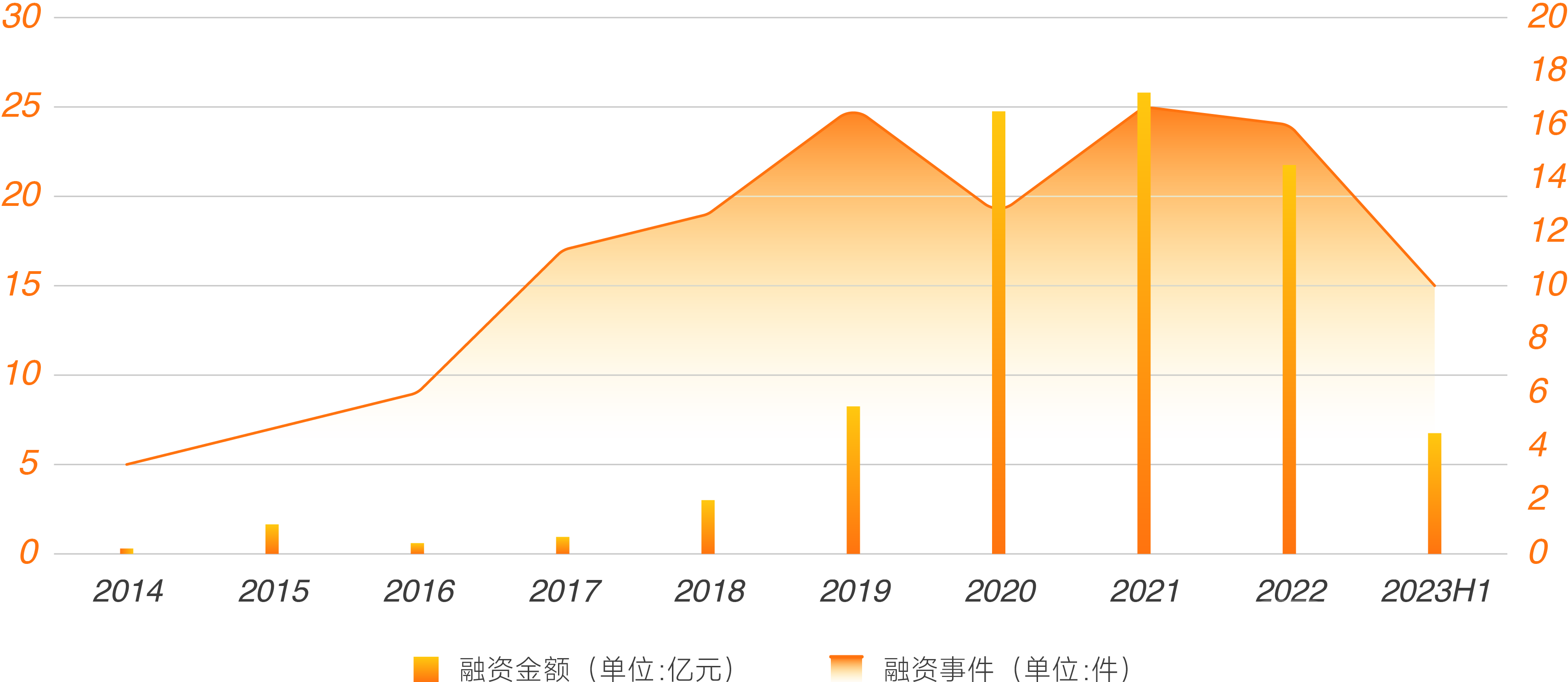

Over the past decade, both the total funding amount and the number of financing events in the microfluidics sector have maintained an overall upward trend.

Overview of Investment and Financing in China’s Microfluidics Sector Over the Past Decade

Data Source: VBInsight; Chart by VCBeat

The capital winter that has prevailed since the second half of 2021 has had some impact on the microfluidics field, but not significantly. It can be seen that the financing performance in the microfluidics sector remained relatively strong in 2021, even reaching a historical peak, with the total annual financing amount reaching 1.804 billion yuan and a total of 26 financing events.Over the past five years (2019–2023), a total of 108 investment and financing transactions occurred in China’s microfluidics sector, with cumulative capital inflows reaching RMB 5.82 billion, thereby rapidly driving industry development.

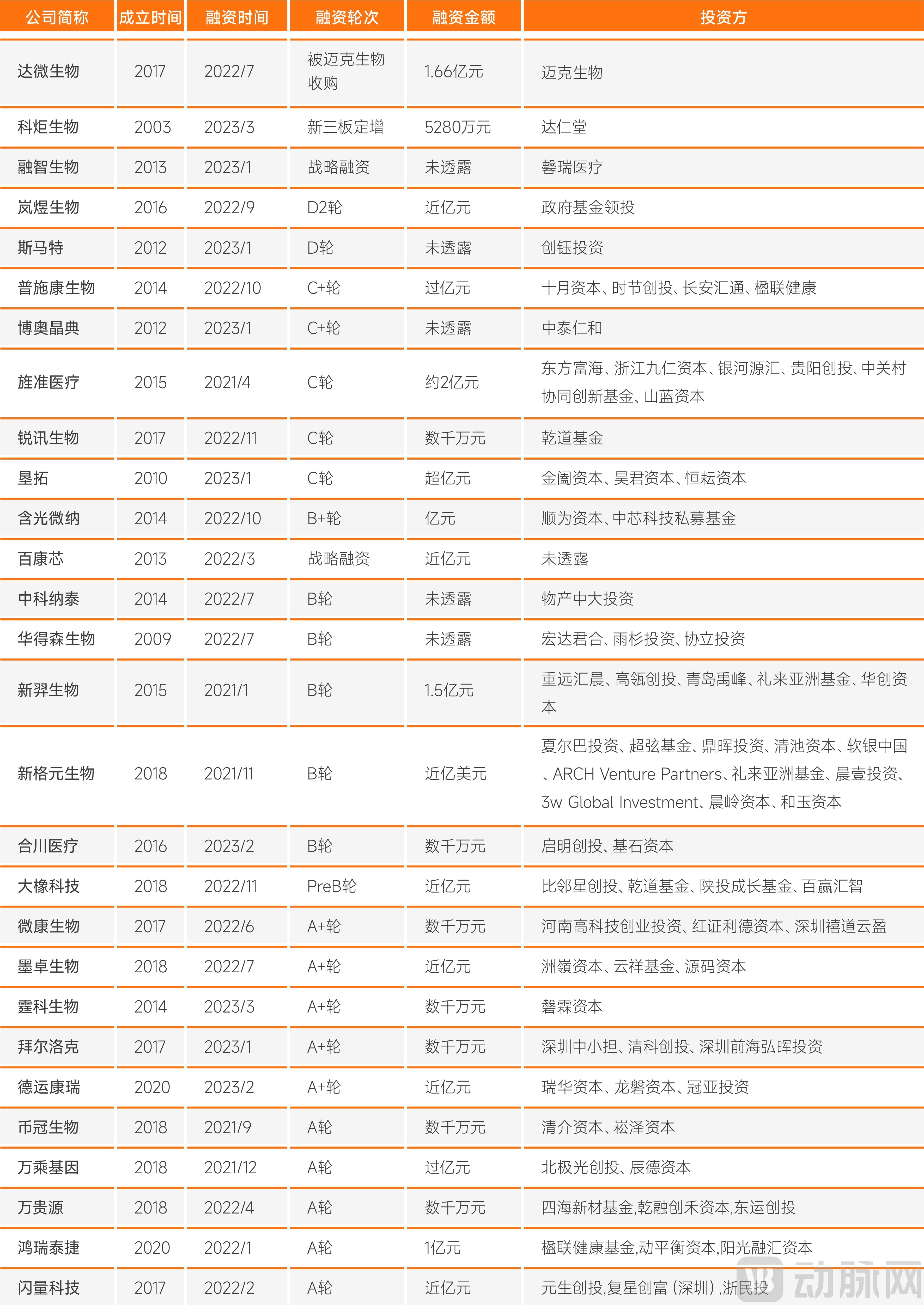

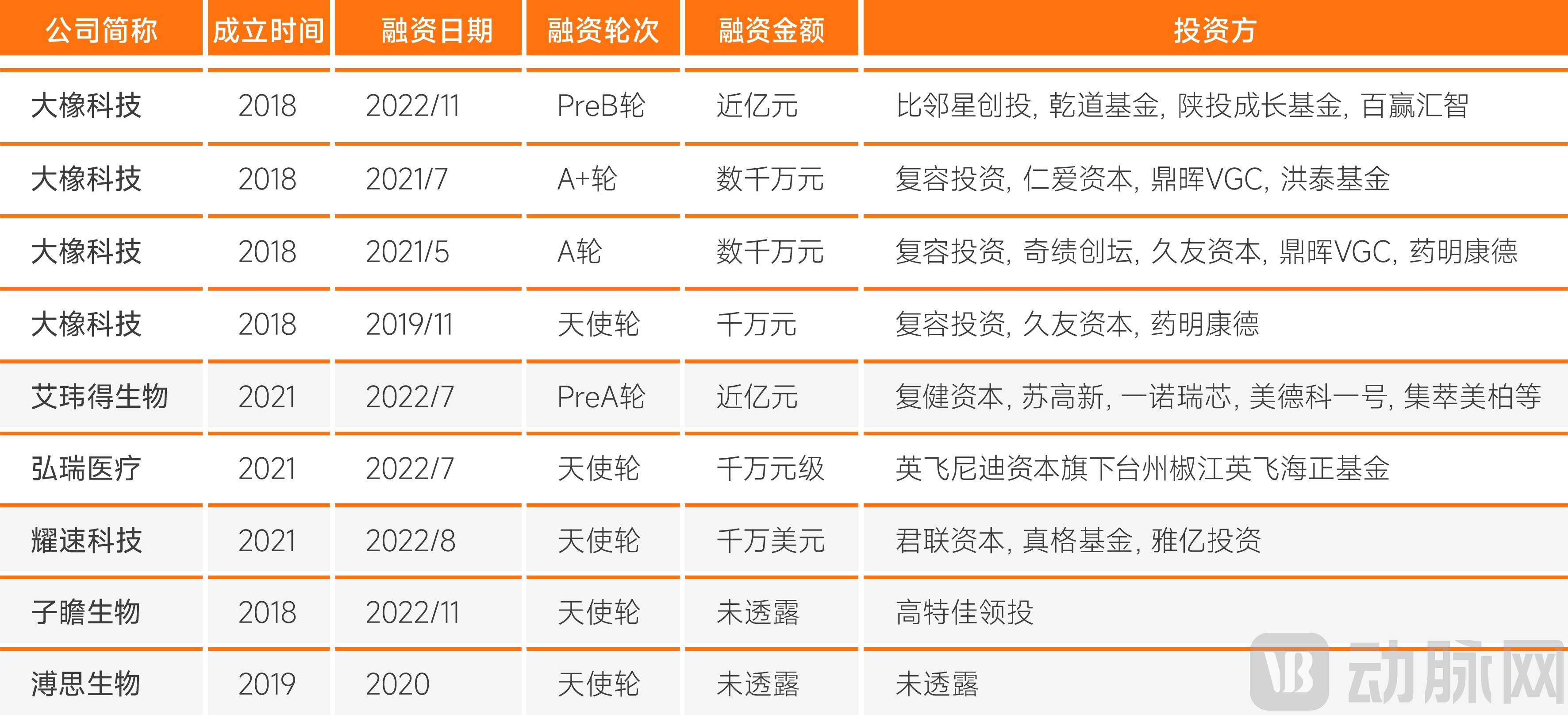

Latest Round of Financing for Domestic Microfluidics Companies

Source: VBInsight; Chart by VCBeat

IVD applications are the most mature, while emerging fields such as organ-on-a-chip and microsphere fabrication are also beginning to attract capital attention. VCBeat has compiled the latest round of financing data for companies in China’s microfluidics sector, as shown in the table above, revealing that:

Companies Applying Microfluidics Technology to the IVD Sector Are Currently Advancing Most Rapidly in Fundraising—Companies such as Keju Bio, Rongzhi Bio, Lanyu Bio, and Smart Biotech have advanced to Series D financing or later stages, with some even proceeding toward an initial public offering (IPO).Reflecting that microfluidics technology has been explored most deeply and is the most mature in this field.

Furthermore,Emerging microfluidics application scenarios, including organ-on-a-chip, microsphere preparation, and assisted reproductive technology, may not stand out in terms of total funding volume and financing progress, but a significant amount of capital has already begun to actively position itself in these areas.

For instance, Daxiang Technology, a rapidly growing organ-on-a-chip company, has advanced to its pre-Series B financing round, having secured nearly RMB 200 million in cumulative funding from the capital market. Other intelligent manufacturing enterprises that have pioneered microsphere preparation using microfluidics technology—such as Arcasso Biotech, Haoli Technology, and Microlong Biotech—have also successively completed angel financing rounds worth tens of millions of yuan.

Commercialized Products Gain Market Recognition, with Global M&A Transactions Reaching Nearly $20 Billion

In more cutting-edge niche sectors, the most promising companies are often prioritized for acquisition by larger corporations. The field of microfluidics is no exception.

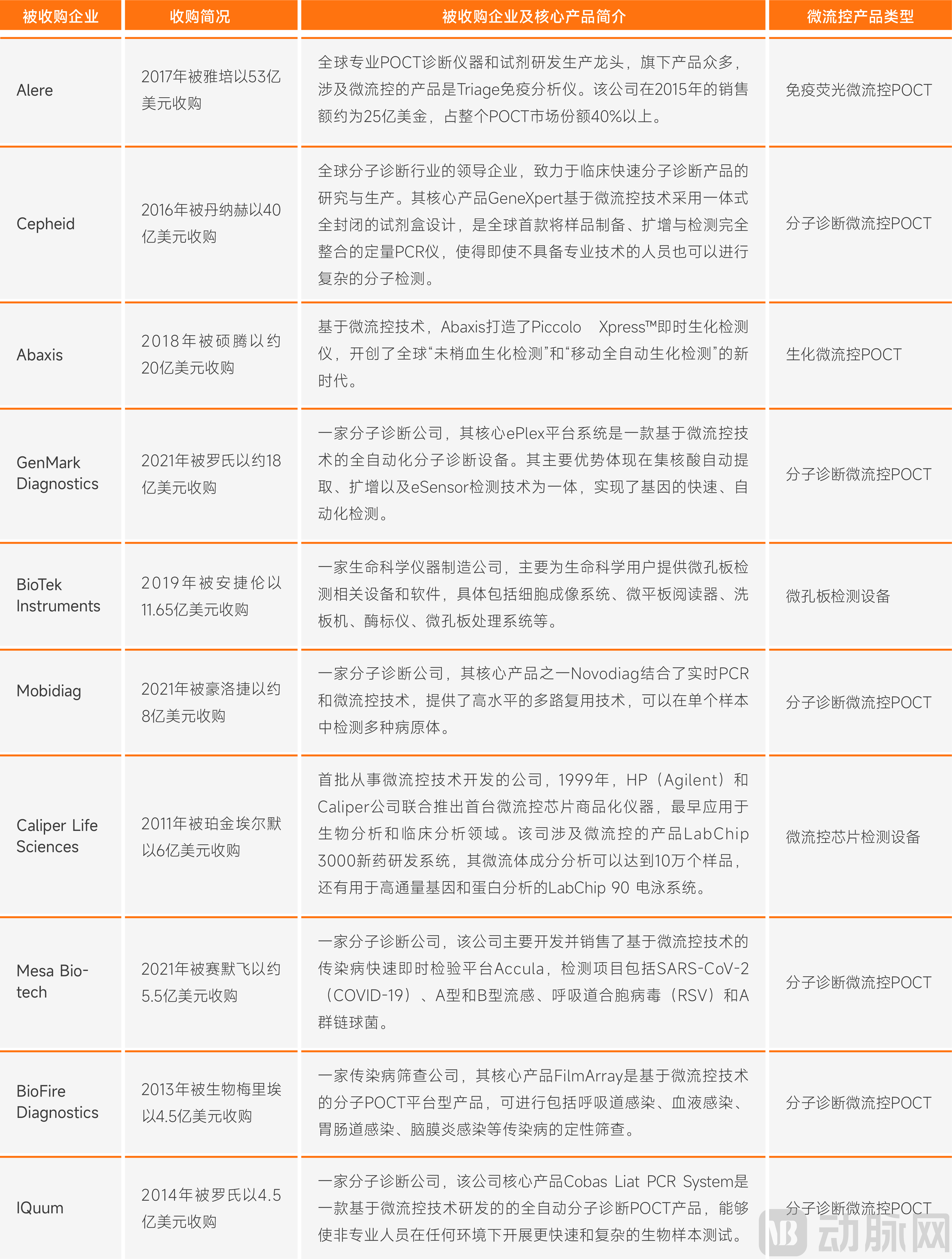

Overview of Mergers and Acquisitions in the Global Microfluidics Sector

Data source: VBInsight; chart by VCBeat

Leading companies that have developed outstanding products based on microfluidics technology include Cepheid, the leader in microfluidic molecular diagnostics known for its GeneXpert system, which was acquired by Danaher for $4 billion in 2016; Alere (which included the Triage microfluidic immunodiagnostic platform, later sold to Quidel Corporation), which was acquired by Abbott for $5.3 billion in 2017; Abaxis, a microfluidic clinical chemistry diagnostics company, which was acquired by Zoetis (formerly Pfizer’s animal health division) for $2 billion in 2018; and BioTek, a microfluidic immunofluorescence company, which was acquired by Agilent Technologies for $1.165 billion in 2019.

According to incomplete statistics from VCBeat,To date, there have been more than 16 global mergers and acquisitions in the microfluidics sector, with a total transaction value approaching $20 billion (over RMB 140 billion).The consecutive acquisitions of numerous star enterprises by large multinational corporations demonstrate that both the technological value and the timing value of microfluidics have gained market recognition.

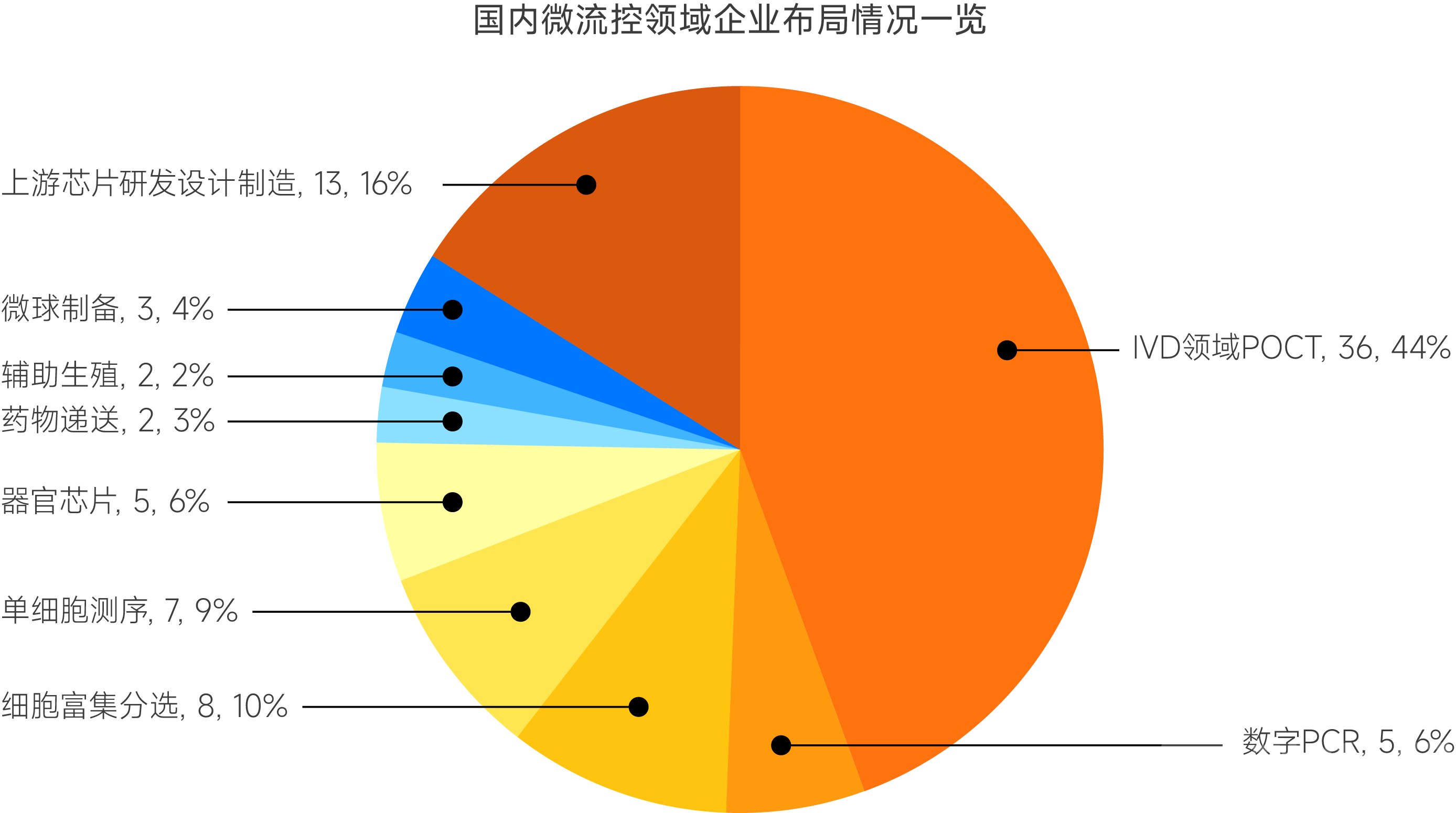

Companies Race to Position Themselves: POCT in the IVD Sector Becomes the Most Widely Applied Field for Microfluidics Technology

Source: VBInsight; Chart by VCBeat

VCBeat has conducted a categorized statistical analysis of 81 domestic companies applying microfluidics technology. From the perspective of corporate business layout,Nearly half (36 companies) of the enterprises applying microfluidics technology have positioned their business scenarios in the field of IVD POCT. Among the top 10 M&A transactions in the microfluidics sector, eight were primarily focused on developing microfluidic POCT products.

8 of the Top 10 M&A Deals in the Microfluidics Sector Involved Companies Primarily Developing Microfluidic POCT Products

Source: VBInsight; Chart by VCBeat.

The race among companies to apply microfluidics technology to the point-of-care testing (POCT) sector, coupled with the fact that most acquired microfluidics firms specialize in POCT products within the in vitro diagnostics (IVD) field, underscores that POCT represents the most mature application scenario for microfluidics commercialization and reflects market recognition of its use in this domain.

Multiple Microfluidic Products Have Been Successfully Commercialized Worldwide, While Disruptive Applications Remain to Be Uncovered and Explored

As the most mature application scenario for the commercialization of microfluidics technology, POCT has already seen the successful launch of multiple commercial products with strong market performance. It is fair to say that the vast majority of commercially available molecular POCT products on the market are currently implemented based on microfluidic chip platform technology.

POCT, as a testing platform and application scenario platform, encompasses multiple methodologies across various subfields of IVD.

Data source: Public information; chart by VCBeat.

VCBeat has selected and provided detailed introductions and analyses of representative microfluidic products across various fields, including biochemistry (Piccolo Xpress Point-of-Care Biochemistry Analyzer), immunology (Triage Fluorescence Immunoassay Analyzer), molecular diagnostics (GeneXpert PCR Analyzer and FilmArray Multiplex PCR System), and blood gas analysis (i-STAT). (Due to space constraints, further details are omitted here; interested readers may download the original report for more information.)

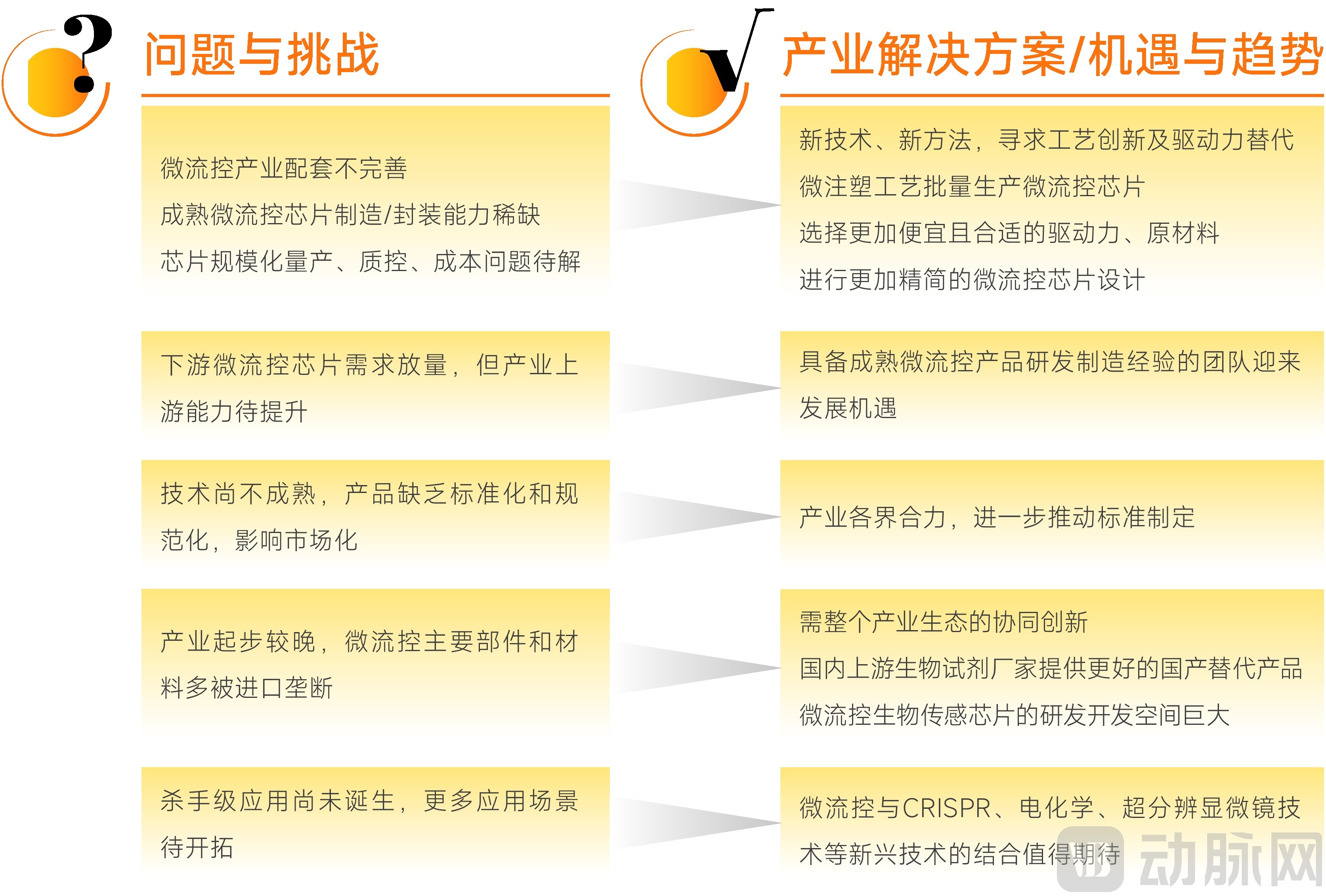

Microfluidics has yet to fully realize its commercial potential, and its disruptive applications require further exploration.The microfluidic POCT products mentioned in the report above are all excellent representatives in the POCT field and have demonstrated strong market performance. However, microfluidic technology has yet to fully realize its commercial potential. This is because microfluidic technology is still in its early stages of development, and while products built around this core technology can deliver superior performance, cost-related challenges remain to be addressed.

Chen Tao, Chairman of LaboRise, pointed out that in fields such as clinical chemistry and immunoassay, which have already reached a stage of high automation and low cost, although the adoption of microfluidics technology can reduce sample volume and shorten testing time, its competitive advantage is not significant due to cost constraints. Consequently, there is weak momentum for substitution within the industry, making it difficult for microfluidic products to gain substantial traction.

However, it is worth noting thatThe level of automation in the field of molecular diagnostics remains relatively low. High-end automated systems are typically bulky and expensive. The application of microfluidics technology can confer significant competitive advantages to products, making it a key focus for industry players in recent years.Meanwhile, the significant boost that the COVID-19 pandemic provided to molecular diagnostics has also led more companies to adopt microfluidics technology for product upgrades.

Furthermore, numerous industry experts believe thatThe microfluidics industry is currently experiencing rapid growth but remains in its early stages. Overall, the industry’s grasp of microfluidic technology, as well as its understanding and insights into the technology itself, remain superficial. The application scenarios identified so far represent only the tip of the iceberg., and many application scenarios have yet to fully harness the potential of microfluidics; the disruptive applications enabled by this technology warrant further exploration and development.

In the future, with the state’s sustained investment in and development of interdisciplinary fields, more application scenarios will be uncovered, thereby revealing the greater development potential of microfluidics technology. Meanwhile, as the cost of microfluidic chips continues to decline and the design and manufacturing capabilities for high-end chips further improve, the industry is poised for explosive growth.

Two Directions for Domestic Substitution: Ensuring Performance While Reducing Costs, and Differentiated Layout and Innovation

Multiple industry experts have pointed out that the future development of microfluidic products in the IVD field will mainly follow two directions.

First, by substituting domestically produced alternatives to reduce costs while ensuring product performance, thereby penetrating the primary healthcare market.

For instance, domestic enterprises have carried out innovative design and optimization improvements based on some of the world’s leading microfluidic POCT products, and have already launched multiple microfluidic POCT products that have been well received in the market.

In the field of clinical chemistry, companies such as Tianjin Micro-Nano Core, Wondfo, Jinrui Biology, Smart Technology, Puscan Biology, and HanGuang Micro-Nano have all developed series of microfluidic POCT products for clinical chemistry. In the field of immunodiagnostics, Shenzhen Weidian Biology and Chengdu Weikang Biology have established their presence. In molecular diagnostics, enterprises including Bohui Innovation, Wondfo, and Diqi Biology are vying to enter the market. In blood gas analysis, Edan’s i15 from Shenzhen follows the technical route of i-STAT and has received positive market feedback. In coagulation testing, Puscan Biology has created a series of microfluidic coagulation products. (Due to space constraints, this introduction will not be expanded further; interested readers may download the original report for more details.)

However, overall, due to the incomplete development of upstream and downstream supporting industries for China's microfluidics sector, many domestic products still struggle to match imported counterparts in terms of performance across various metrics, leaving room for further cost optimization.As domestic products continue to mature and incorporate more features, leveraging China’s inherent advantages in talent costs and industrial manufacturing to further reduce product costs—while ensuring performance—will enable these products to reach a broader base of primary healthcare institutions, undoubtedly unlocking a larger market.

For instance, in the field of molecular diagnostics, Cepheid’s GeneXpert PCR analyzer and BioFire’s FilmArray multiplex PCR system have arguably established the two major developmental directions for molecular point-of-care testing (POCT) products. However, the prices of these two systems remain high, making them inaccessible to primary care markets where POCT solutions are most needed. If domestic manufacturers in China can catch up by reducing costs while ensuring performance, they will undoubtedly unlock a significant market opportunity.

Second, pursue differentiated strategic layout and independent innovation, exploring the integration of microfluidics with emerging technologies and their application and implementation in new scenarios.

For instance, companies such as Huamai Xingwei, Pushikang Biology, and Keruida Biology are exploring the integration of microfluidics with chemiluminescence, aiming to leverage the high sensitivity of chemiluminescence while utilizing microfluidic technology to achieve miniaturization and full automation. Boshi Diagnostics’ microfluidic magnetoresistive immunoassay product, m16, employs microfluidic technology and the giant magnetoresistance (GMR) effect to enable fully automated multiplex immunoassays, representing another breakthrough innovation.

Kexun Bio leverages the advantages of microfluidic chips to develop microbarcode array chips based on inorganic nanomaterial substrates for rapid, highly sensitive, and precise detection of protein molecules. Yuanjing Taike has pioneered the integration of electrochemistry and microfluidics, focusing on high sensitivity, speed, and portability. Its research-grade handheld electrochemical detector, Taiji Mini, is already on the market, while a commercial instrument for IVD applications is imminent. Digifluidic’s latest commercial POCT fully automated nucleic acid analyzer, Virus Hunter S, adopts an open collaboration model to serve fields such as medical disease diagnosis, pet/animal and plant pathogen detection, agricultural disease testing, and food safety inspection.

Pet healthcare is on the rise, and the veterinary market deserves attention.According to statistics, the market size of pet disease diagnosis and treatment in China was estimated at RMB 11 billion in 2022, and is expected to exceed RMB 18 billion in the future. Among them, the market size of pet in vitro diagnostics (IVD) was approximately RMB 6.1 billion, with a compound annual growth rate (CAGR) of over 20%, and is projected to reach RMB 9 billion by 2025.

Amid the surging demand for pet diagnosis and treatment, immense development opportunities lie hidden. Currently, there are few domestic suppliers of pet diagnostic equipment, with the majority relying on imports. Veteran players and new entrants in China’s IVD market are rapidly moving in to establish their presence. Many companies developing microfluidic products, such as Shenzhen Edan, Micropoint Biotechnology, Tianjin MicroNano Chip, Smart Technology, and Diqi Biotechnology, have all entered the veterinary market.

Compared to the human healthcare market, the veterinary market has lower requirements. To maintain equipment stability, devices are typically replaced every three years. High-priced pet diagnostic equipment offers a certain market space for relatively high-cost microfluidic products, allowing manufacturers, distributors, and end-users to retain a profit margin without incurring losses. With the rise of pet healthcare, the veterinary market presents greater opportunities.

Applying Microfluidics to Single-Cell Sequencing and Digital PCR Becomes a New Market Hotspot

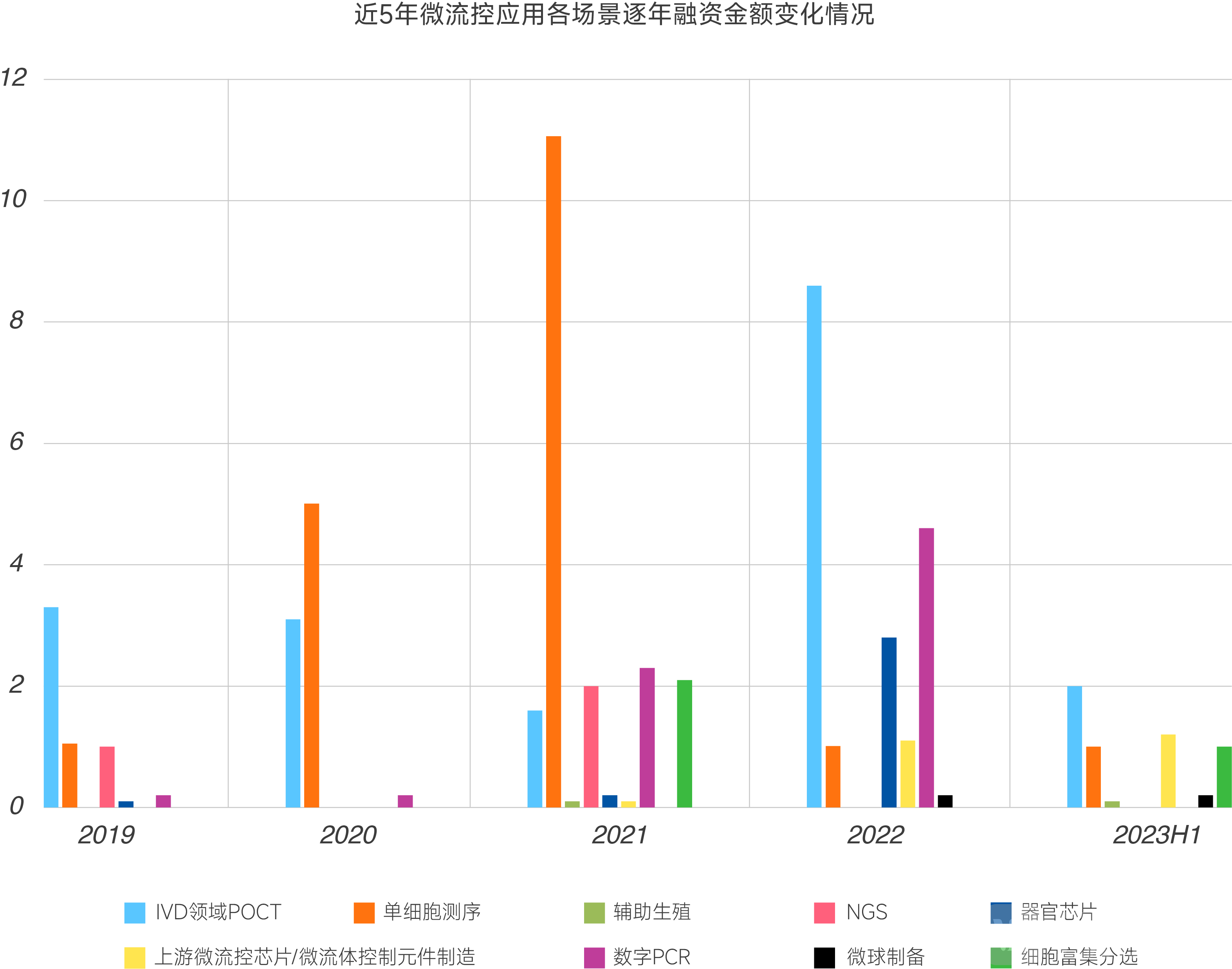

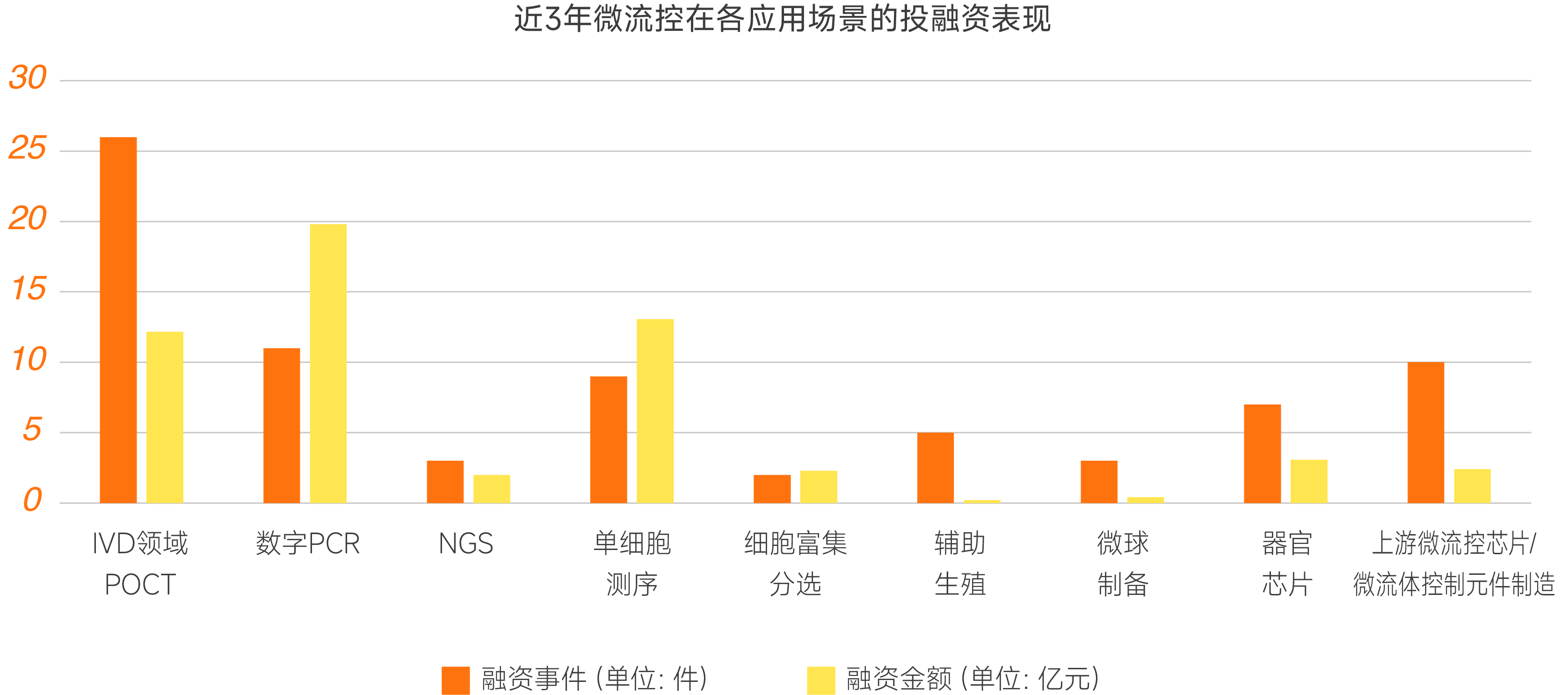

VCBeat has reviewed the year-by-year investment and financing trends across various microfluidics application scenarios over the past five years, revealing shifts in capital interest in the primary market for microfluidics.

Based on the comprehensive performance of financing events and amounts, the application of microfluidics technology to point-of-care testing (POCT) in the in vitro diagnostics (IVD) sector has consistently been a field favored by investors. However, in recent years,The application of microfluidics in single-cell sequencing and digital PCR is gaining significant market traction, emerging as a new hotspot following its adoption in the POCT sector.

Source: VBInsight; Chart by VCBeat

A summary of investment amounts and financing events in the microfluidics sector over the past five years shows that,Single-cell sequencing stands out with its exceptional and unique performance, securing the highest single-round financing amount.——Accounting for 16% of financing events but 33% of the total financing amount, which is comparable to the financing amount in the IVD sector’s POCT segment, where financing events account for 35%.

Overview of Total Financing Amount (Unit: 100 Million Yuan) and Number of Financing Events (Unit: Cases) Across Various Microfluidics Application Scenarios in the Past Five Years

![[[18LJBTZA_U]}8}{2~NJ9V.png](http://cdn.vcbeat.top/upload/image/08/07/26/00/1690358443899837.png/dmw)

Data source: VBInsight; chart by VCBeat.

Zooming in on the timeline, an examination of investment and financing trends for microfluidics across various application scenarios over the past three years similarly reveals that, apart from point-of-care testing (POCT), applications of microfluidic technology in single-cell sequencing and digital PCR have attracted greater capital interest.

Data source: VBInsight; Chart by VCBeat.

The report provides a detailed overview of the advantages of microfluidics technology in single-cell sequencing and digital PCR, along with representative case studies from both domestic and international markets. (Due to space constraints, this section is not elaborated further; interested readers are encouraged to download the full report for more details.)

Applications in POCT, digital PCR, and cell enrichment/sorting are booming, making molecular diagnostics the primary battlefield for microfluidics applications.

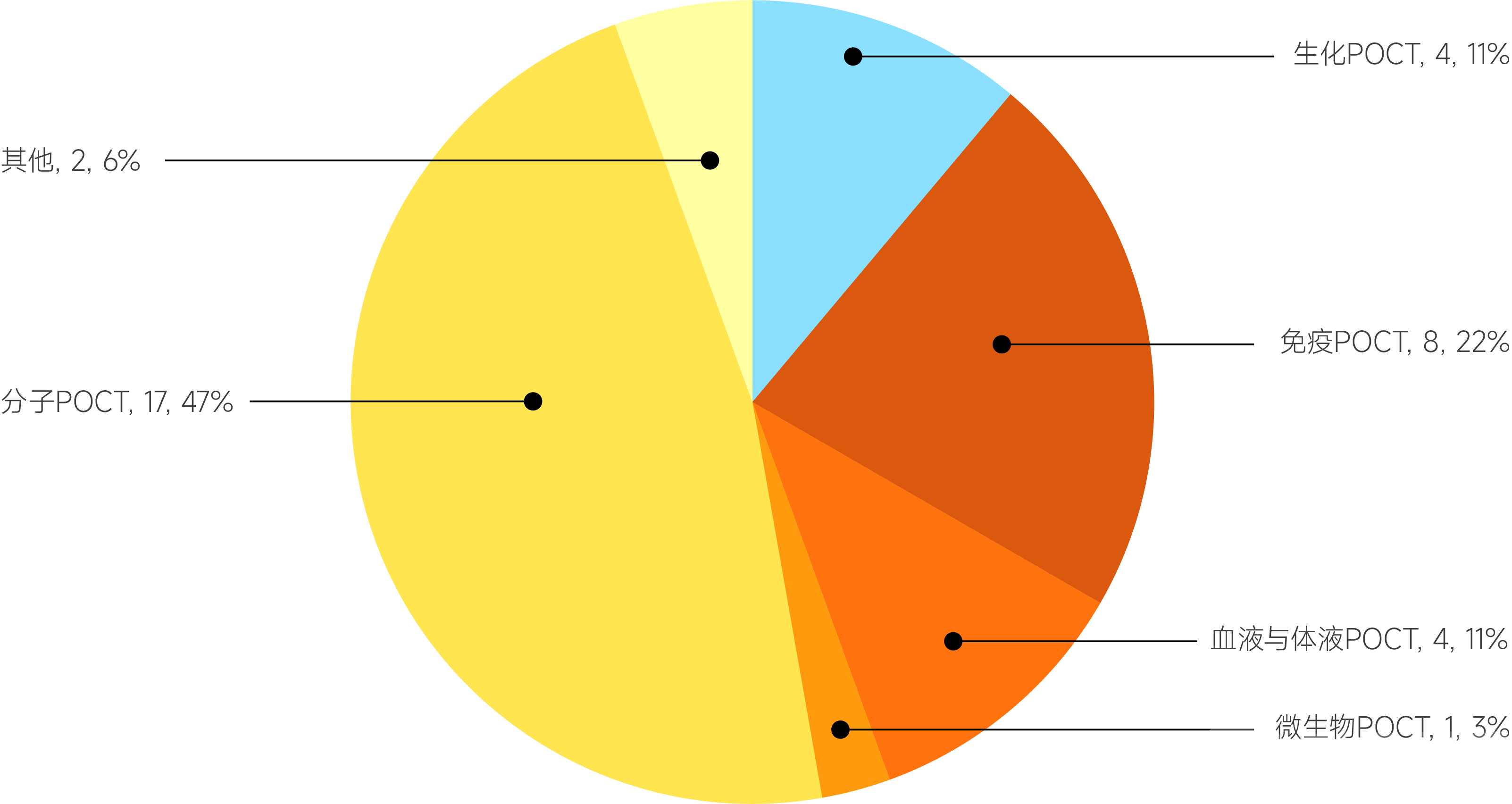

Currently, the most widespread and mature application of microfluidics lies in point-of-care testing (POCT), where several products have already achieved commercial success; however, a killer app has yet to emerge. In contrast to the high automation and low costs characteristic of clinical chemistry and immunodiagnostics, molecular diagnostics—despite its relatively lower level of automation—offers higher profit margins, thereby attracting significant attention from many teams developing microfluidic technologies.

As shown in the figure, VCBeat has compiled statistics on the layout of domestic applications of microfluidics technology in the POCT field. It can be seen thatThe largest number of companies applying microfluidics technology are in the field of molecular POCT, accounting for nearly half. Furthermore, an analysis of the top M&A deals involving microfluidics globally reveals that among the eight acquired companies primarily focused on developing microfluidic POCT products, five were engaged in the development of molecular POCT products.

Domestic Landscape of Microfluidics Technology Application in the POCT Field

Data Source: VBInsight; Chart by VCBeat.

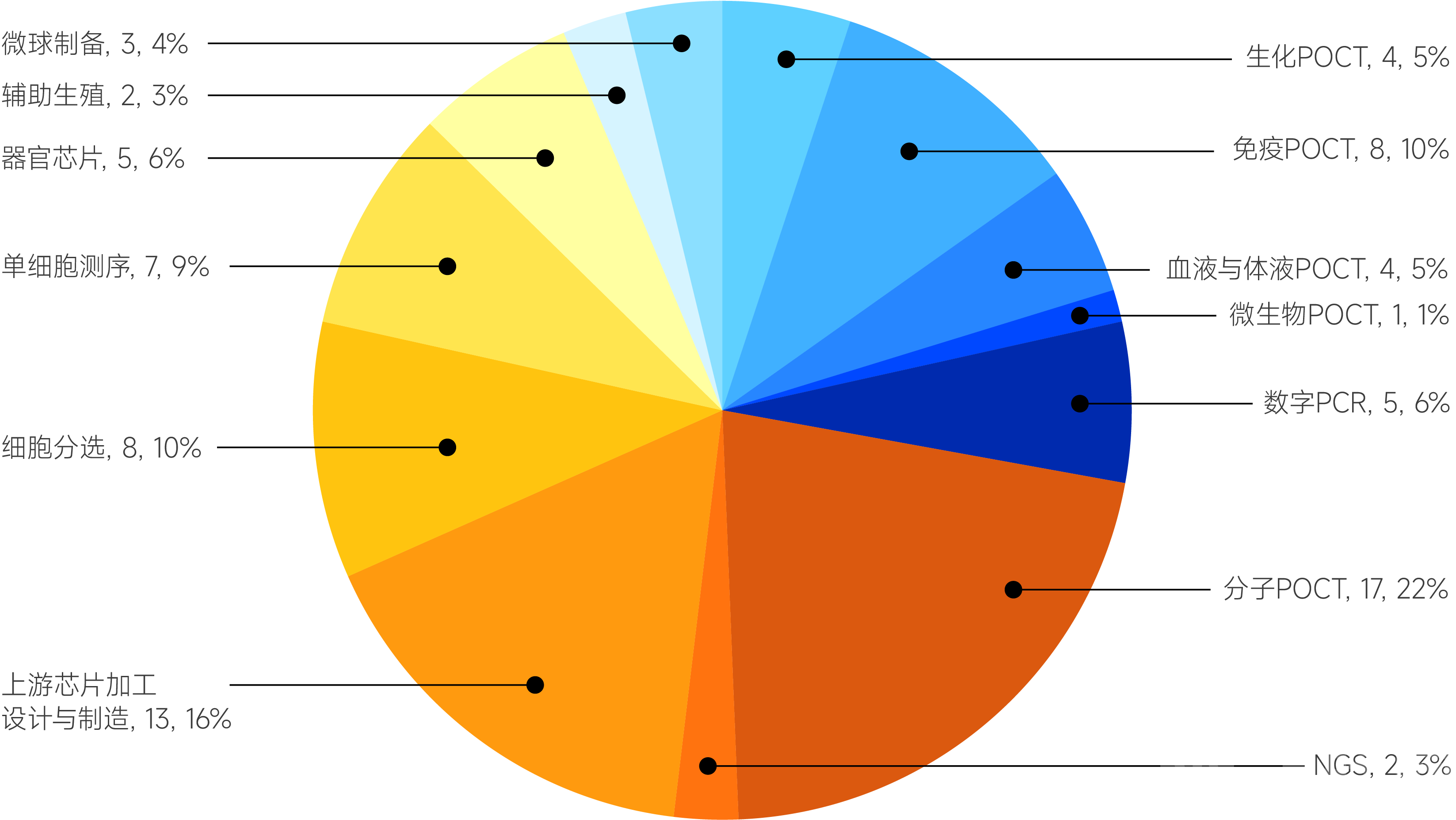

From the perspective of the layout of domestic microfluidics companies in various application scenarios, molecular diagnostics is currently the most widely adopted field for microfluidics technology. As shown in the figure below,In China, a total of 24 companies apply microfluidics technology to digital PCR, molecular diagnostics POCT, and NGS.Accounting for over 30% of domestic microfluidics companies.

Overview of the Layout of Domestic Microfluidics Companies

Data Source: VBInsight; Chart by VCBeat.

Furthermore, companies leveraging microfluidics for single-cell sequencing often apply this technology to molecular diagnostics, while the ultimate application of microfluidic-based cell enrichment and sorting (primarily for circulating tumor cells, or CTCs) also predominantly lies in molecular testing.The field of molecular diagnostics is becoming the main battleground for microfluidics technology applications.The report provides a detailed introduction to the application advantages of microfluidics in scenarios such as enrichment and sorting of cells (e.g., CTCs, CTBs) and cell counting, as well as representative domestic enterprises; due to space limitations, these details are not further elaborated here.

Investment and Financing Performance of Microfluidics-Based Companies in the Field of Cell Enrichment and Sorting Over the Past Three Years

Source: Public information; graphic by VCBeat.

Emerging markets such as organ-on-a-chip and microsphere fabrication are beginning to demonstrate commercial potential, with the prospect of giving rise to killer applications.

Entrepreneurs are boldly venturing in, and investors are placing their bets. Microfluidics, still in its early stages of development, holds limitless possibilities. Beyond popular application areas such as POCT, single-cell sequencing, digital PCR, and cell enrichment and sorting, microfluidics is also demonstrating significant commercialization potential in earlier-stage emerging fields. The quiet rise of these sectors has already attracted considerable attention from investors.

Latest Funding Performance of Domestic Microfluidics Companies

Source: VBInsight; Chart by VCBeat.

An analysis of the latest round of financing distribution in China reveals that organ-on-a-chip, microsphere preparation, and assisted reproduction are emerging application scenarios for microfluidics technology. These sectors account for the highest proportion of early-stage financing, with most companies being newly established and having just completed their angel rounds.

Although exploration in these fields is still in its early stages, it cannot be overlooked. For instance, organ-on-a-chip technology, centered on microfluidic chips, may become a powerful tool to break the pharmaceutical industry’s Eroom’s Law, while microsphere fabrication marks the advent of the 3.0 era for microfluidic chips, transitioning them from analytical reactions to manufacturing production.The industry has high hopes for these emerging fields, believing that exploration in these areas could enable a leapfrog advantage and lead to the first killer application based on microfluidics technology.

Organ-on-a-chip technology originates from microfluidic chip technology, which serves as the core of organ-on-a-chip systems.The organ-on-a-chip field has witnessed rapid development over the past two years. Previously, VCBeat had just released“White Paper on the Organoid and Organ-on-a-Chip Industry”, this microfluidics report provides a detailed introduction to the core status and application advantages of microfluidic chips in organ-on-a-chip systems, which will not be further elaborated here due to space constraints.

Currently, the core members of companies or teams in China engaged in the development of organ-on-a-chip or organoid-on-a-chip products all have years of prior experience in microfluidic chip R&D. Professor Luo Guoan, one of the pioneers in the field of microfluidics in China, has also entered the entrepreneurial arena by founding Hongrui Medical, which has now established two major product matrices of microphysiological systems: organ-on-a-chip (including liver, kidney, and barrier function models) and organoid-on-a-chip (such as those for culturing tumor organoids).

Bullish on the development of microfluidic chip technology in the organ-on-a-chip field, more than 20 investment institutions have already entered this space, with cumulative investments exceeding RMB 300 million.

Investment and Financing Performance of Domestic Organ-on-a-Chip Companies

Data source: VBInsight; chart by VCBeat

Furthermore, it is worth noting thatCurrent Applications of Microfluidics in Microsphere Preparation。

Microspheres, measured in micrometers or nanometers, are indispensable core foundational materials in fields such as biopharmaceuticals and in vitro diagnostics. Their preparation and application present significant challenges, and they were once listed by Science and Technology Daily as one of the 35 key core technologies subject to “chokehold” constraints. In the Guidelines for the Development Planning of the Pharmaceutical Industry, jointly issued by multiple national departments, it is explicitly stated that priority should be given to the development of high-end formulations, including microspheres, and to the industrialization technologies for such high-end formulations.

Unlike in the detection field, where microfluidic chips are used as consumables, microsphere preparation employs microfluidic chips as production tools, enabling a role transition from “Lab-on-Chip” to “Factory-on-Chip” and ushering in a new era of microfluidic technology development.

Previously, the use of microfluidic technology for microsphere preparation was largely confined to academic research and had not yet been commercialized; the primary challenge lies inProduction Capacity(A single-channel microfluidic chip generates no more than 500 μL of microspheres per hour; while this throughput meets research needs, it falls short of industrial-scale scenarios that often require thousands to tens of thousands of liters). However, with further accumulation of research findings and technological breakthroughs achieved in industrialization, several companies in China have now reached significant milestones.

For instance, Acasobio in China successfully launched the world’s first microfluidic chip with thousands of channels in August 2022, thereby enabling the mass production of highly uniform microspheres. The monthly microsphere output per chip can reach nearly 1,000 liters. Haoli Technology, a recently established company, has successfully developed a production-grade silicon-based microfluidic chip for agarose chromatography resin microspheres, increasing the total throughput of a single chip to the million-microsphere level.

Moreover, traditional microsphere preparation methods, such as batch reactor-based processes, cannot achieve precise control and are limited by materials and processing techniques, failing to meet the increasingly complex and diverse market demands for microspheres. However,In addition to enabling the efficient production of high-performance microspheres with uniform particle size and narrow size distribution, microfluidic chip technology offers rapid customization capabilities for microspheres of varying sizes, materials, and structures. It also facilitates the fabrication of complex core-shell or multi-layered microspheres, thereby addressing the limitations of traditional microsphere preparation methods and breaking the import monopoly on mid-to-high-end microspheres.

In terms of production efficiency, traditional methods for achieving microsphere particle size control, sieving, modification, and encapsulation require a long-chain, complex manufacturing process with extremely low yields. In contrast, microsphere production using microfluidic chips (taking agarose microspheres as an example, where industry players can currently achieve a particle size variance of <5% and yields approaching 100%) enables exponential capacity expansion or significant cost reduction with each technological iteration.

In the assisted reproductive technology sector, which boasts a blue-ocean market worth hundreds of billions, microfluidics is also demonstrating its substantial market potential.According to projections based on information released by the official website of China’s National Medical Products Administration (NMPA) at the end of 2020, the infertility rate in China is expected to rise to 18.2% by 2023. According to a Frost & Sullivan report, driven by the continuously rising infertility rate in China, the increasing penetration of assisted reproductive technology (ART) services, and the implementation of the national three-child policy, the ART sector is projected to maintain a compound annual growth rate (CAGR) of 14.5% from 2023 to 2027. The market size for ART services is estimated to reach approximately RMB 85.2 billion by 2027.

Although assisted reproductive technology has developed rapidly, it still faces challenges such as tedious and repetitive procedures, difficulty in controlling operational quality, and human operational errors.The characteristics of microfluidic technology align with the detection and manipulation requirements in assisted reproductive practice, effectively enhancing the operational efficiency of assisted reproduction platforms.(The report provides a detailed overview of the advantages of microfluidic technology in the field of assisted reproduction; interested readers may download the original report for further information.)

For instance, Baylock leverages microfluidics technology to replace all the cumbersome, inefficient, and costly manual steps in the cryopreservation process, significantly improving the success rates of egg and embryo freezing. Mochang Technology has achieved automated operations in gamete selection, embryo testing, oocyte cryopreservation, and embryo cryopreservation within embryology laboratories based on microfluidics technology, thereby helping to increase IVF (in vitro fertilization) pregnancy success rates and substantially reduce the cost of consumables and reagents.

Investment and Financing Performance of Microfluidics-Based Companies in the Assisted Reproductive Technology Sector Over the Past Three Years

Data Source: VBInsight, Chart by VCBeat

With further research and optimization of microfluidic chips, it is believed that microfluidic-assisted reproductive technology products more suitable for clinical applications can be developed.

The above is an excerpt from the main content of the report. IfGet Full ReportPlease scan the QR code to add our assistant, and initiate your inquiry after adding.

Special Acknowledgments (in order of interviews and research):

Jiang Tao, Co-founder & General Manager of Acasso Bio; Bao Xiaofan, Co-founder of Acasso Bio; Chen Tao, Founder & Chairman of Labores; Zhao Yan, Technical Director of Labores; Zhang Jichao, Product R&D Manager of Labores; Han Lin, CTO of Kexun Bio; Zhu Kun, Founder & General Manager of Yuanjing Taike; Han Linchen, Co-founder & CEO of Haoli Tech; Guo Ziyuan, Business Director of Haoli Tech; Luo Guoan, Founder, Chairman & Chief Scientist of Hongrui Medical; Zhong Ming, General Manager of Hongrui Medical; Chen Tianlan, Founder, Chairman & General Manager of Diqi Bio; and other unnamed corporate and venture capital representatives.

References:

1. Dr. Tang Minghui's Column. Zhihu

2. Chenghui Medical Technology Official Account Content

3. Microfluidics Learning Official Account

4. Content from the IVD Sharer Official Account

5. Lin Bingcheng. Illustrated Guide to Microfluidic Chip Laboratories [M]. Beijing: Science Press, 2008.

6. Tian Changmin, Yang Xiangliang, Yang Hai. Development and Applications of Digital PCR Based on Microfluidic Technology[J/OL]. Micronanoelectronic Technology:1-12[2023-04-24].

7. [Kaitai Industry Research] Research on the Microfluidic Molecular Diagnostics Industry and Investment Recommendations

8. The "Dog-Beating Stick" in the POCT Arsenal: Abaxis Piccolo Biochemical Analyzer – Mindray Medical

9. The POCT Arsenal’s Heaven-Reliant Sword – Alere Triage Immunoassay Analyzer. Mindray Medical

10. Integration of Microfluidics into Digital PCR: All-in-One Systems Are Just the Starting Point

11. Applications of Microfluidics in the IVD Sector: Analysis of Representative Product Technology Pathways – Heyi Guangye Innovation Platform