U.S. Internet-Enabled Home Care Sector Surges with Over $12.5 Billion in Funding in First Half of 2023 as Investors Target Three Key Trends

The Era of Hot Money Pauses; The World Shares the Same Chill.

In the U.S. digital health sector, there were 244 financing deals totaling $6.1 billion in the first half of 2023. According to Rock Health, “if this pace continues in the second half, 2023 will see the lowest funding volume since 2019.”

But we believe that even in the most cautious markets, there remain hotbeds of capital activity; indeed, investors in the digital health sector are still eager to back the next star company.

First, there was no shortage of large-scale financings (exceeding $100 million) in the digital health sector during the first half of the year, with a total of 12 deals recorded. The average financing amount per deal reached $185 million, comparable to the robust levels seen in the same period of 2021, when the average for large-scale financings stood at $188 million.

Figure: Compiled based on “H1 2023 digital health funding: A Brave New (lower funding) World” and publicly available information

However, half of these 12 large financing rounds went to companies post-Series D, with four occurring in pre-IPO stages. This indicates that despite increasing market uncertainties, investors remain fully committed to backing the companies they deem exceptional.

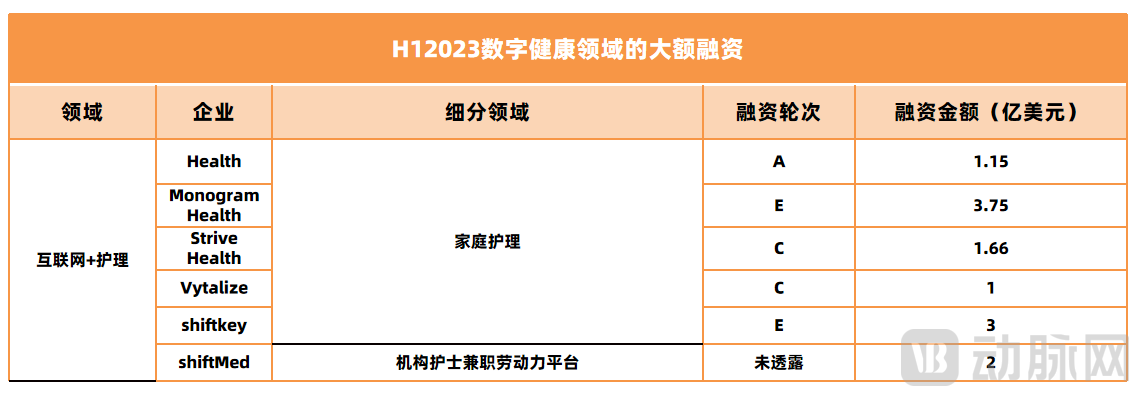

From a project-specific perspective, investors collectively went into a frenzy over “Internet + Nursing Services” in the first half of the year—6 out of 12 financing deals were related to this sector, with a total funding amount of $1.256 billion (approximately RMB 9 billion).Among them, Monogram Health, which focuses on home-based care for kidney disease, topped the funding list with $375 million.

Ultimately, this situation reflects capital’s return to the principle that “demand is king.”The healthcare industry is one of the largest and fastest-growing sectors in the United States.

Similar to the United States, China boasts a vast market potential for healthcare. This is particularly evident in the elderly care sector: by the end of 2021, China’s population aged 60 and above had reached 267 million, including approximately 40 million seniors with partial disabilities who have strong demands for medical nursing care.

However, the concept of “family health” in China started relatively late, and the home care market has been gradually activated since the rise of the “Internet + Nursing” model. According to previous statistics by Analysys, the size of China’s Internet nursing market was approximately RMB 2.96 billion in 2019, accounting for only 5.7% of the overall Internet healthcare market, but its compound annual growth rate reached 94% compared with 2015.

In recent years, the state has repeatedly issued policy documents to promote the development of “Internet Plus Nursing,” encouraging hospitals to provide transitional care services (post-discharge home nursing).

From the National Health Commission’s issuance of the Notice on Launching Pilot Programs for “Internet + Nursing Services” in January 2019, to its release of the National Nursing Development Plan (2021–2025) in May 2022, and further to the joint publication by the National Health Commission and the National Administration of Traditional Chinese Medicine of the Action Plan for Further Improving Nursing Services (2023–2025) on June 20 this year, these documents have consistently emphasized this topic. They also explicitly encourage non-governmental entities to actively participate in innovating nursing service models.

Currently, China’s “Internet + Nursing” sector has also entered a fast lane of development—the market is rapidly “awakening,” and more practitioners are “crossing the river by feeling the stones.”

At this point, we examine the seven major financing deals in the U.S. digital health sector during the first half of the year that are related to “Internet + Nursing,” and analyze their business models and development trends.

“Perhaps, stones from other hills may serve to polish the jade.”

The incremental growth in the healthcare market always lies “beyond the hospital ward.” Among these opportunities, home-based care—characterized by lower costs and higher efficiency—is of paramount importance.

Among the six financing rounds related to “Internet + Nursing” mentioned above, one focused on human resource management for hospital nursing staff, while the other five were concentrated in the field of home health care.

Figure:Compiled from “H1 2023 digital health funding: A Brave New (lower funding) World” and publicly available information

The U.S. home health market is highly fragmented, with more than 11,000 Medicare-certified home health agencies in operation, based on 2020 Medicare claims data; the top 10 operators account for 26.6% of the national market share.

For example, Amedisys, a leading home healthcare provider in the United States, reported annual revenue of $2.223 billion in its 2022 annual report, with home health care accounting for 60%, hospice care for 35%, and other care services for 5%. However, according to a 2020 study by Grand View Research, Inc., the U.S. home health market was valued at approximately $300 billion and is projected to grow at a compound annual growth rate (CAGR) of 7.88% from 2021 to 2028.

Nevertheless, despite the vast market size, investors are not acting blindly.They place greater emphasis on “rigid demand,” “high-frequency use,” and “long-term needs.”

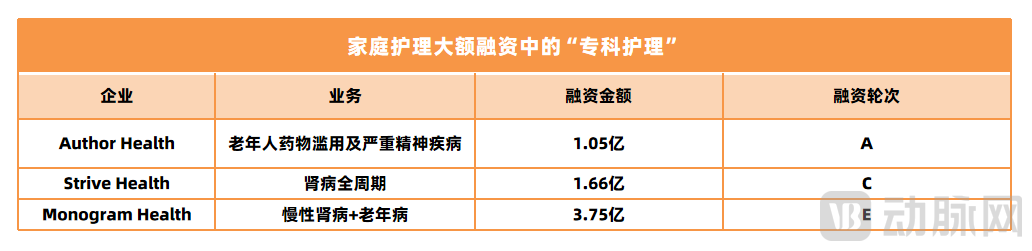

Among the seven financing deals in the first half of the year, we noted that three projects—Author Health, Monogram Health, and Strive Health—focusing on chronic disease management within home care, are essentially explorations in the “specialized nursing” segment of the “Internet + Nursing” track, tailored to national conditions.

Figure:Compiled from “H1 2023 digital health funding: A Brave New (lower funding) World” and publicly available information

Poor Kidney Health Among Americans Is a Major Problem. According to data, more than 37 million American adults (approximately 14% of the population) currently suffer from chronic kidney disease, and kidney disease–related expenditures account for about one-quarter of annual Medicare spending.

In the realm of kidney care, Monogram Health and Strive Health have pursued two distinct development paths.

Monogram Health focuses on telemedicine and health education, extending nephrology care resources to communities and homes via the internet at “affordable costs,” including through partnerships with numerous chronic disease management benefit plans.

In terms of telemedicine, the platform integrates nephrologists, cardiologists, geriatricians, endocrinologists, internists, pharmacists, nurses, and social workers to deliver evidence-based medical services with a primary focus on kidney disease and secondary attention to geriatric conditions. In the nursing sector, once a patient is diagnosed, the system generates a care plan. Monogram Health’s nurses then manage the course of the disease through video consultations, phone calls, or home visits, including providing home dialysis services.

Strive Health focuses on integrating hospitals with community and home-based care.

On one hand, Strive Health provides a big data- and artificial intelligence-powered diagnosis and treatment platform (CareMultiplier™) for nephrologists and kidney specialists. On the other hand, it builds or integrates community care teams (Kidney Heroes™) to extend nephrology “physician offices” into communities and deliver personalized care services. This home-based care is led by one nephrologist, with the community care team assisting in disease course management. This model aligns with China’s advocacy for “public hospitals providing transitional care services,” extending in-hospital resources to out-of-hospital settings.

Furthermore, as the kidneys are “silent” organs, kidney diseases are difficult to detect in their early stages and often exhibit irreversible characteristics. Therefore, the management of chronic kidney disease (CKD) requires early detection and timely intervention. In its specific care workflows, Strive Health emphasizes the use of the “predictive analytics” feature within its big data platform, CareMultiplier™. Following predictive risk stratification on the technological platform, if intervention is deemed necessary, the care team notifies partner healthcare institutions to intervene, thereby achieving comprehensive, end-to-end disease management.

Thus, it is evident that Monogram Health leans more toward "inclusive care," while Strive Health places greater emphasis on "the cost and effectiveness of care."

It should be noted that these two directions are not mutually independent but are increasingly “integrating with each other.”In fact, leveraging the “Internet + Nursing” model to shift patient care toward more cost-effective solutions is an ongoing trend in the development of nursing platforms, while “value-based care” represents their next major direction.

In 2008, spurred by the Obama administration, the curtain rose on value-based healthcare reforms in the primary care system.

Home health care is a vital component of the U.S. primary healthcare system. In 2016, the Centers for Medicare & Medicaid Services (CMS) introduced the Home Health Value-Based Purchasing (HHVBP) model and launched pilot programs in nine states. Unlike the previous fee-for-service model based on volume, HHVBP ties reimbursement to quality and efficiency of care, implementing financial incentives and penalties for providers (with maximum payment adjustments of 3% in 2016, increasing annually to reach 8% by 2020). This performance-based model helps improve patient health outcomes and reduces federal Medicare expenditures.

In early 2021, CMS announced that the Home Health Value-Based Purchasing (HHVBP) model would be expanded nationwide to all 50 states after 2022, with payment adjustments of up to 5% upward or downward.

Medicare is the largest payer in the home care market.Therefore, starting in 2022, U.S. home healthcare providers entered a new round of market competition.

Among the seven financing deals in the first half of the year, two were for care programs grounded in medical value: one was Strive Health, mentioned above, and the other was Vytalize Health, which provides remote care for seniors and supports the primary healthcare system.

Value-Based Care Model,The core objective is to delay or reduce the likelihood of high-cost events (such as hospitalization and emergency care) through daily care, slow the progression of the disease to its terminal stage, and improve patients’ quality of life.Therefore, “trend prediction” and “timely intervention” have become critical links, enabling medical big data and large model platforms to “fully leverage their capabilities.”

Secondly, the ultimate goal of implementing value-based nursing is to “reduce costs and increase efficiency” in the healthcare system.. In addition to the nursing decision-making process itself, such platforms have two key “levers”: first, driving down operational costs for healthcare and nursing providers through digital tools or extended on-the-ground services; second, actively participating in payment model innovation by collaborating with insurers and healthcare organizations to establish “special funds” that assume medical risks and provide incentives to healthcare professionals.

Vytalize Health is a typical example.

According to the company’s official website, Vytalize Health was founded in New York in 2014. Initially, the company built its own clinical and technical teams to primarily provide telemedicine, virtual care, and home-based care services, with its business model being entirely B2C at that stage.

In 2016, Vytalize Health recognized that a more competitive growth strategy lay in serving the U.S. primary care system, as they believed “there is sufficient waste within the healthcare system.”

Based on this core shift, the team immediately changed course.

They have begun collaborating with relevant practitioners to deploy a data-driven, health insurance-focused healthcare service model.

At this stage, Vytalize Health focuses on digitizing home care service workflows within the primary healthcare system—providing institutions with “Internet + Nursing” solutions.By integrating big data from patient clinical records, health metrics, and insurance claims, this solution provides digital tools for healthcare providers and downstream care networks to facilitate more efficient care coordination among hospitals, specialists, and ancillary service providers.

After optimizing process efficiency, Vytalize Health turned its attention to improving the quality of medical care.

In this step, Vytalize Health primarily activates internal efficiency within healthcare through innovative payment models, proposing risk-bearing solutions for primary care practices.For example, in 2018, they transformed their clinical care model into a “contracting system.” In brief, Vvtalize Health establishes entities known as KECs in collaboration with professional medical groups. Vvtalize Health is responsible for managing these KECs, assuming accountability for patients’ total costs and quality of care. It also provides partners with access to its data capabilities and pool of clinical experts to help develop personalized care plans, while sharing both risks and savings generated from Medicare.

By examining the development trajectory of Vytalize Health, we can clearly observe its transformation from a standalone “Internet + Nursing” service provider into an integrated industry service provider. Ultimately, by leveraging its self-built ecosystem capabilities, it has gradually assumed responsibility for nursing outcomes and undertaken corresponding risks, thereby entering the deep-water zone of “Internet + Nursing” development.

According to the official website, Vytalize Health is currently positioned as “a new type of ACO (‘Accountable Care Organization’).” This “Accountable Care Organization” is a healthcare consortium centered on primary care physicians, encompassing hospitals at all levels, insurance institutions, and other entities.

Among these, Vytalize Health plays a role in empowering through internet technology, integrating medical care resources, and assuming nursing risks.

Vytalize Health’s development model shares similarities with the domestic “medical consortium + internet technology service provider” model; however, as a platform, Vytalize Health plays a more dominant role in resource integration and payment innovation.

More perspectives suggest that 2023 was the year when “value-based care” became a more mainstream approach in home care in the United States, with an increasing number of U.S. home health service providers shifting toward this model.As mentioned earlier, Author Health and Monogram Health have both stated in news reports that they have begun efforts to pivot in this direction.

Meanwhile, industry giants are also rapidly “staking their claims.”

For instance, healthcare giant CVS spent $8 billion last year to acquire Signify Health, positioning itself in the home care market. CVS stated that it needed a company capable of enhancing its home care capabilities and driving value-based care. Among the seven financing deals completed in the first half of this year, both Strive Health and Monogram Health have CVS as their backer, underscoring the systemic opportunities within this sector.

In the first half of the year, there were two large-scale financing deals in the “Internet + Nursing” sector, both focused on human resources.

No matter how technology advances, the “last link” in home-based care always remains human. Therefore, “human resource management” for nursing services often tests a company’s core competencies.

Not applicable to the ride-hailing or food delivery industries; nursing services are highly specialized and carry certain medical risks.

On one hand, from the perspective of total supply, the “nurse shortage” is a widespread phenomenon across countries worldwide, reflecting a structural issue in human resources within healthcare systems. On the other hand, from an operational standpoint, the ability to balance labor costs with service scale represents a critical bottleneck constraining corporate development.

Taking Amedisys, the leading company in the home health care sector mentioned earlier, as an example, its 2022 annual report reveals that the company’s nursing team currently exceeds 13,000 members, with labor costs accounting for more than 60% of its operating expenses.

Consequently, sectors that revitalize social resources and enhance workforce utilization will inevitably give rise to high-quality projects, attracting capital eager to “add the finishing touches.”

Benefiting from the openness of multi-site practice for nurses and the improvement of the tiered system in the United States, these two “people-centric” initiatives have made attempts in two different directions within the “shared nursing” sector—ShiftMd focuses on “part-time nurses” for medical institutions, emphasizing human resource optimization for healthcare facilities, while Shiftkey concentrates on “home-based services,” prioritizing the staffing and standardized management of community home-care personnel.

Figure:Compiled based on “H1 2023 digital health funding: A Brave New (lower funding) World” and publicly available information

In terms of business model, both platforms connect licensed nurses or nursing resources with institutions, functioning as on-demand workforce technology management platforms rather than direct-to-consumer (DTC) nursing service platforms.

The key distinction lies in the fact that ShiftMed’s service scenarios demand greater stability. Since hospital nursing staff typically work for periods ranging from 4 to 26 months, a primary focus is on extending employee-level benefits to contingent workers and enhancing employers’ management of their part-time workforce. For instance, ShiftMed’s part-time model is structured around W-2 tax reporting (indicating an employer-employee relationship). Once licensed nurses and caregivers register with ShiftMed, they are subject to payroll taxes, accrue retirement benefits, and become eligible for unemployment insurance. According to its official website, ShiftMed is currently the most-downloaded nurse scheduling app in the U.S. Apple App Store.

In the context of in-home nursing care, Shiftkey must address the challenge of “randomness,” making workflow management for home visits critical. Therefore, unlike other “shared nurse” platforms, Shiftkey’s innovation primarily centers on “visualized worksheets” powered by big data.

This form serves as both the “electronic medical record” for community patients and the “operational manual” for home-visit nurses, guiding visiting personnel on necessary preparations, procedural workflows and standards, as well as emergency response protocols. This approach aims to standardize home-based nursing care as much as possible, mitigate medical risks, and enable shift-based scheduling for home-visit nurses.

Figure: Shiftkey Official Website

For healthcare institutions, Shiftkey’s “Internet + Nursing” solution effectively enables them to manage both patients and home-visit nursing services, while providing telemedicine support. Currently, the Shiftkey platform has reached its Series E financing round, aggregated hundreds of thousands of nurses and nursing care resources, and is moving toward an initial public offering (IPO).

Before writing this article, the author happened to chat with a former classmate who works as a nurse at a public county-level hospital in southwest China, and inquired about the implementation of “Internet + Nursing” services at her hospital.

“Many institutions are currently promoting their services in a manner akin to marketing. Our hospital is also preparing to offer internet-based medical services, including home nursing care for patients with paralysis or limited mobility. However, we are still in the preparatory phase and have not yet determined the final operational model; we may collaborate with other hospitals in the county.”

Despite her already demanding hospital workload, she remains enthusiastic about “home-based services.” However, she believes that “training, safety, and reasonable performance incentives are essential,” with her greatest concern being the potential for emergencies.

In China, “Internet + Nursing” has expanded from pilot programs in a few cities to widespread implementation, fundamentally driven by the public’s surging demand for health. At the end of last month, Tianjin announced that by 2025, all secondary-level and above public hospitals in the city will provide transitional care services, with the number of “Internet + Nursing Services” items reaching 60.

As the window of opportunity opens, how can China’s internet nursing professionals find the “magic bullet” for rapid growth? The verdict may still be some time coming.