2023 Cancer Early Screening Industry Report: Breakthroughs in Proprietary Technologies, Initial Validation of Business Models, and Untapped Potential in C-end and Overseas Markets

In 2020, the early cancer screening sector made a significant impact in the capital markets, with the year often hailed as its “Year One.” By 2023, the industry had formally entered the commercialization phase. Currently, market concentration remains low, mainstream technologies have been validated, and business models are largely still in an exploratory stage.

Technologically, the development pathways for single-cancer and pan-cancer products have become increasingly clear, with ctDNA methylation emerging as the mainstream approach, multi-omics gaining momentum, and original innovations rising. In 2023, four Chinese companies received FDA Breakthrough Device Designation.

In terms of business model, hospital-side operations serve as the foundation, health checkup services are essential, public welfare projects are being gradually rolled out, while direct-to-consumer (C-end) initiatives remain rare. Meanwhile, overseas expansion is gaining momentum, whereas penetration into grassroots markets remains challenging to implement in the near term.

What innovative technologies have emerged during this period? What are the development paths of domestic enterprises? What is the logic behind their business model choices? What will be the future development trends?

This report is the third “Industry Research Report on Early Cancer Screening” released by VCBeat. Going forward, we will continue to track the early cancer screening sector and analyze industry changes and trends.

This article analyzes the technologies and commercialization of early cancer screening based on surveys of 12 companies and nearly 20 experts, drawing the following conclusions:

1. The pace of financing has slowed, with a greater overall emphasis on practical implementation; regulatory approval capability is a key consideration, while innovative technologies and solutions still present opportunities;

2. Through expert interviews, biomarkers for early cancer screening can be evaluated across five dimensions: accuracy, applicability, convenience, technical cost, and accessibility;

3. In terms of industrial maturity, ctDNA methylation is the tumor early screening biomarker with the highest expected value in the mature stage, while multi-omics is the one with the highest expected value in the growth stage;

4. Most domestic companies have followed the strategic roadmap of “single-cancer screening → combination screening for multiple high-incidence cancers → pan-cancer screening.” To create differentiation, some companies have recently adopted a “cancer early screening+” strategy, particularly the integrated model of “cancer early screening + screening for other chronic diseases + health management.”

5. The comparison of reimbursement prices for endoscopy and early screening products is a key factor in international expansion; Southeast Asian countries along the “Belt and Road” initiative, such as Malaysia and Indonesia, as well as the Middle East, exhibit high recognition of Chinese-made products and are currently preferred markets for overseas expansion;

6. As global expansion gains momentum, early-stage tumor screening companies are primarily entering overseas markets through distributor partnerships. Regarding grassroots penetration, the completion of PCR infrastructure serves as a foundation; however, implementation remains challenging at this stage. In contrast, AI-assisted diagnosis offers high accessibility and represents a viable alternative.

7. In terms of products, single-cancer and pan-cancer offerings have distinct positioning and will achieve co-development across different scenarios. Regarding scenarios, home-based testing can drive significant incremental growth, while the implementation of Laboratory Developed Tests (LDT) policies within hospitals may face a tortuous path.

8. In terms of payment, early cancer screening products have not yet played a role in cost containment within insurance coverage, primarily due to a lack of accumulated real-world data. In the future, they will play a role throughout the pre-insurance, underwriting, and post-insurance phases.

Overview: Financing is more focused on practical implementation, with frequent industrial dynamic collaborations.

Overall, cancer screening in developed countries has entered a phase of gradual standardization. Taking the United States as an example, large-scale screening was conducted from the 1970s to the 1980s, built upon technological compliance and heightened public awareness. This led to significant improvements in five-year survival rates, incidence, and mortality. Subsequently, risk-benefit assessments for early screening of various cancer types were carried out based on robust evidence-based medical data.

Development Stages of Cancer Screening in Developed Countries

Image source: VCBeat

In China, large-scale screening has not yet been implemented for most cancer types, and development remains in its early stages. Apart from cervical cancer and breast cancer, which have undergone large-scale screening, most other cancers have not yet been subjected to such programs.

As incidence and mortality rates improve, early cancer screening is poised for further explosive growth. Currently, while the five-year survival rate in China has increased, the overall incidence and mortality rates have not yet begun to decline.

Evidence from evidence-based medicine for early screening of most cancer types remains insufficient, requiring further data validation; currently, the tumor early screening industry, which is in its initial commercialization stage, is experiencing rapid development.

We believe that with further practice, we will see improvements in incidence and mortality rates, followed by a potential explosion in commercialization.

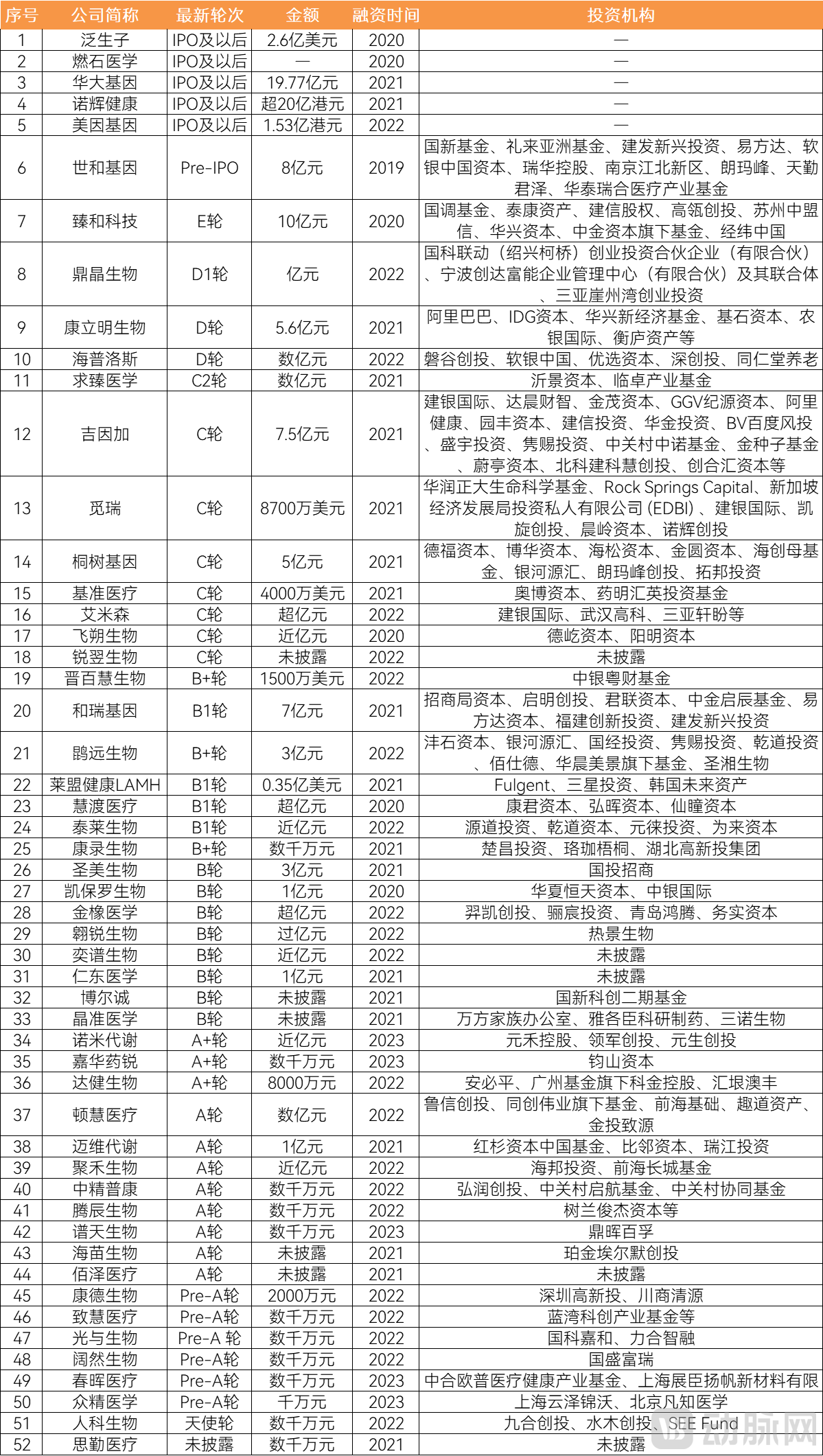

Overall, funding for early cancer screening over the past three years has been more focused on practical implementation. While overall enthusiasm for financing in early cancer screening projects has declined in the last three years, the number of deals remains substantial.

According to incomplete statistics, a total of 52 companies were involved, with the majority being post-Series A projects, accounting for approximately 69%. Projects at Series A and earlier stages were primarily focused on new technologies and novel solutions.

The decline in market interest is primarily driven by two factors. First, 2020 and 2021 marked a peak period for initial public offerings (IPOs) among cancer early screening companies, meaning that well-capitalized players have already taken a leading position, leading to a more cautious approach from investors.

On the other hand, successful business models have already been validated in the current market. Investors are increasingly focusing on projects with rapid translation capabilities, favoring those with lower risk, later-stage funding rounds, and the ability to achieve commercialization quickly. Greater emphasis is placed on project implementability, making regulatory approval capability a key consideration. The specific projects that have secured financing are summarized below:

Review of Financing in the Early Cancer Screening Industry Over the Past Three Years

Image source: VCBeat.

Current market concentration remains low, and early screening presents significant opportunities, particularly in the realm of new technologies and solutions. Among projects that have secured Series A or earlier financing, the focus is primarily on novel technologies—such as proteomics and metabolomics—and innovative solutions. For instance, Zhongjing Pukang is dedicated to analyzing serum metabolites of gut microbiota, while Guangyu Shengwu has developed single-molecule detection technology based on new rare-earth materials for protein detection.

ZJ Medicine focuses on “urinary health,” with strategic initiatives in urothelial carcinoma and chronic disease health management. It has not only developed an epigenetics-based multi-gene methylation assay for assessing the risk of urothelial carcinoma, but is also committed to creating precision diagnostic testing and health management solutions based on multi-omics analysis of urine samples from the Chinese population.

Technology: Synergistic Development of Mainstream and Innovative Omics, Rise of Original Research

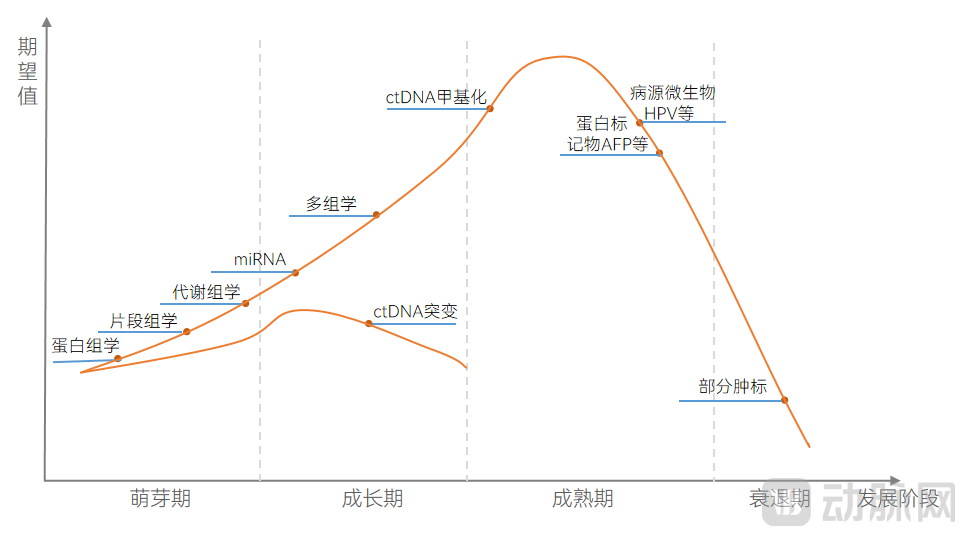

The industrial maturity of various biomarkers used for early cancer screening varies. The figure below analyzes the development stages and expectations of these biomarkers. The development stages include the embryonic, growth, maturity, and decline phases. As shown in the figure, ctDNA methylation has the highest expectations during the maturity phase, while multi-omics has the highest expectations during the growth phase, as detailed below:

Maturity of Industrialization of Biomarkers for Early Cancer Screening

Image source: VCBeat.

ctDNA methylation is one of the most well-established biomarkers used in early cancer screening. Aberrant ctDNA methylation, an important epigenetic modification driving cancer initiation and progression, often occurs at the early stages of the disease.

The ctDNA methylation patterns of normal cells and cancer cells differ significantly, making them a stable and viable screening biomarker. ctDNA methylation is one of the most mature features utilized in early tumor screening and represents a mainstream technical approach.

ctDNA mutations are mostly analyzed in conjunction with other features through multi-omics testing; ctDNA levels in the blood during early-stage cancer are low.

Among these, tumor-derived ctDNA yields fewer fragments, and the mutation burden within these fragments often fails to meet the abundance requirements for detection in early-stage patients using NGS or digital PCR. Consequently, most early screening products currently under development employ multi-omics approaches that combine mutations with other biomarkers.

Fragmentomics is an emerging field with broad biological and clinical implications. Relying on next-generation sequencing (NGS) technology, fragmentomics is primarily characterized by copy number variations, nucleosome footprints, fragment size distributions, and fragment end sequence motifs.

Copy number variations (CNVs) encompass copy number changes and rearrangements caused by translocations, amplifications, or deletions, which typically lead to alterations in gene expression and affect normal gene function. For example, the fragmentation patterns of cell-free DNA (cfDNA) can reflect gene expression status, and cfDNA fragmentomics features can be used to monitor DNase activity, providing biomarkers for autoimmune diseases.

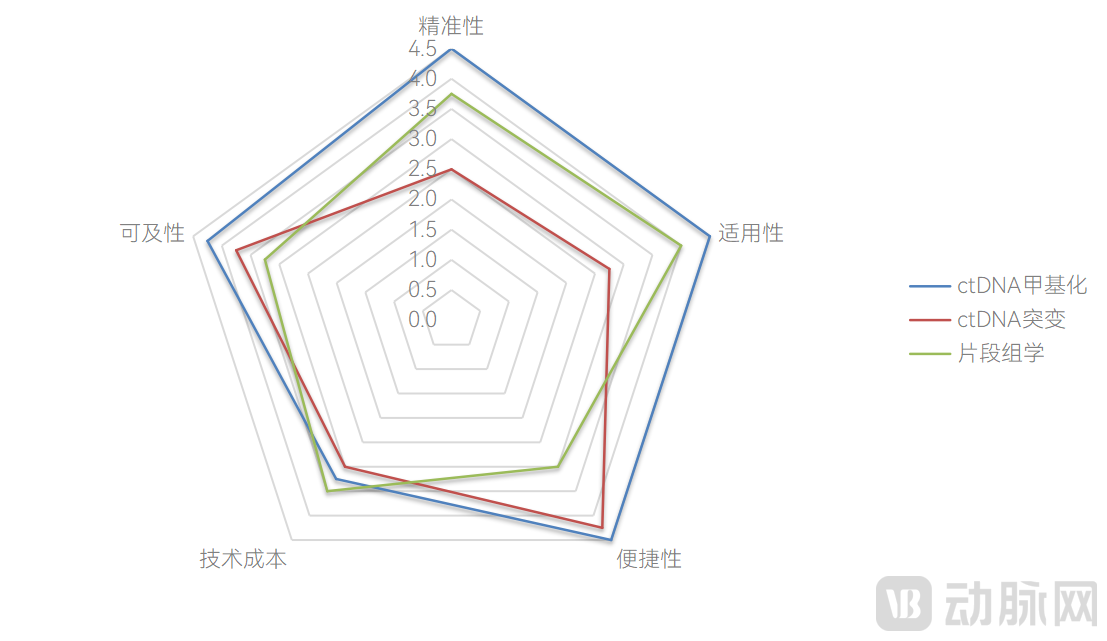

We evaluated the aforementioned biomarkers for early cancer screening, selecting five dimensions through expert interviews: accuracy, applicability, convenience, technical cost, and accessibility.

Among these, “precision” refers to the correlation with early-stage tumors, as reflected in sensitivity and specificity; “applicability” refers to the scalability of the same technical pathway and detection platform across different types of cancer; “convenience” refers to the ease of sampling, whether samples are easy to store and transport, and whether the detection process is automated and user-friendly; “technical cost” refers to the costs associated with enrichment, signal amplification, and detection platforms; “accessibility” is primarily determined by costs such as labor and resources, where higher costs result in lower accessibility.

Based on the above five dimensions, we conducted a comprehensive evaluation of ctDNA methylation, ctDNA mutations, and fragmentomics, as shown in the figure below. Among these, ctDNA methylation demonstrates advantages across all five dimensions.

Evaluation Chart of Tumor Early Screening Biomarkers in Genomics

Image source: VCBeat

miRNAs can participate in the regulation of post-transcriptional gene expression. Currently, the most widely used circulating tumor RNAs in clinical practice are microRNAs (miRNAs). miRNAs are a class of small non-coding RNAs (22–25 nucleotides in length) that participate in the regulation of post-transcriptional gene expression.

To date, more than 2,500 distinct miRNAs have been identified, each of which can directly or indirectly regulate multiple target genes, thereby modulating key cellular processes such as proliferation, differentiation, DNA repair, and apoptosis, and exerting oncogenic or tumor-suppressive functions.

Proteomics is more complex and directly reflects the immediate state of life. As downstream products of the central dogma, proteins are the ultimate executors of biological activities. They are closely associated with the development of major diseases such as cancer. Furthermore, protein detection utilizes samples from body fluids like plasma, which are non-invasive and easily accessible, making proteomics highly suitable for early disease screening.

In recent years, with the rapid advancement of mass spectrometry technology, proteomics research has entered a new era. For instance, high-throughput proteomics technologies can reveal the mechanisms underlying tumor initiation and progression, identify specific biomarkers, elucidate the mechanisms of drug resistance, and discover novel therapeutic targets.

Metabolomics technology can directly and promptly reflect an individual's disease status. By performing qualitative and quantitative analyses of small-molecule metabolites with a relative molecular mass below 1,000 in a given organism or cell, metabolomics identifies disease biomarkers, thereby enabling early screening and diagnosis of metabolic disorders and cancer.

Researchers generally agree that metabolomics analysis more directly and promptly reflects an individual's disease status. Metabolomic testing and analysis can be applied to early disease diagnosis, drug target discovery, and the study of disease mechanisms.

Microbiome research can be categorized from the perspectives of genomics, transcriptomics, proteomics, and metabolomics. In recent years, an increasing number of researchers have begun to integrate microbiomics with metabolomics, jointly addressing scientific questions at the levels of species, genes, and metabolites. This approach facilitates a better understanding of disease processes and metabolic pathways within the body, aids in the discovery of disease biomarkers, and thereby supports clinical auxiliary diagnosis.

The gut microbiota is a crucial metabolic “organ” that influences the host’s overall metabolism. With in-depth exploration of basic research, the key role of the gut microbiota in the pathogenesis or signaling pathways of various diseases has become increasingly clear.

However, the pathogenesis of diseases is complex. Compared with genomics, transcriptomics, and proteomics, metabolomic changes are most closely associated with diseases and can promptly reflect the functional status of the body.

For example, Zhongjing Pukang launched its first blood test product for the early detection of colorectal cancer, Zaochangjing.®, from advanced adenomas to stage I and II colorectal cancer, its sensitivity and specificity are on par with the contemporaneous data released by international benchmark companies Freenome and Guardant Health. The product received FDA Breakthrough Device Designation in June 2023.

Integrated multi-omics analysis is the mainstream developmental trend. Numerous companies are strategically positioning themselves in the multi-omics field, combining multidimensional biological data analysis to investigate changes in cancer cells across multiple molecular levels, including the genome, transcriptome, proteome, epigenome, and metabolome. The combined application of multi-omics is not limited by quantity; its core focus remains on addressing specific research questions. Practical applications include cross-omics assays and combined intra-omics testing.

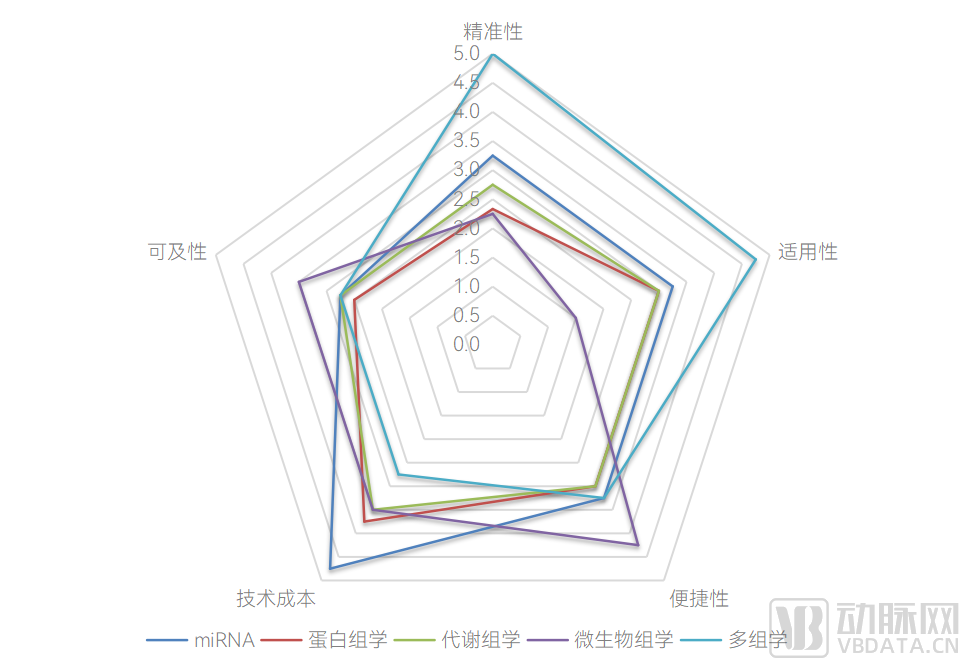

Here, we similarly evaluate miRNA, proteomics, metabolomics, microbiomics, and multi-omics within the realm of innovative omics across five dimensions: “precision, applicability, convenience, technical cost, and accessibility.”

Among these, multi-omics demonstrates the highest precision and applicability, microbiomics offers the greatest convenience and accessibility, and miRNA analysis incurs the highest technical costs, as illustrated in the figure below:

Evaluation Landscape of Tumor Early Screening Biomarkers Under Innovative Omics

Image source: VCBeat

In terms of detection technologies, we have already analyzed PCR, NGS, single-cell sequencing, nucleic acid mass spectrometry, and mass spectrometry in the “2022 Companion Diagnostics Industry Research Report,” so they will not be reiterated here. This section focuses on introducing single-molecule detection technology for proteomics under innovative omics and elaborates on the enabling role of AI.

Single-Molecule Detection Technology Enables Ultra-High Sensitivity in Protein AssaysThe advancement of protein detection technologies has facilitated the development of precision medicine. As an ultra-sensitive biomolecular detection technique, single-molecule detection technology achieves a sensitivity at the femtogram-per-milliliter (fg/mL) level by manipulating, resolving, and monitoring individual molecules in real time. It is anticipated that this technology will enable the development of diagnostic products for more than 1,000 trace biomarkers.

Meanwhile, single-molecule technologies exhibit strong adaptability, enabling the development of high-throughput or low-throughput detection devices tailored to diverse application scenarios.

Single-molecule detection technology can be used for the screening and diagnosis of major diseases such as cancer. The application value of single-molecule detection technology is mainly reflected in two aspects.

First, scientific instruments in the life sciences sector, such as those for marker screening; for example, developing customized diagnostic products based on different testing objectives, discovering novel biomarkers through clinical research and diagnosis/treatment in oncology, and assisting clinicians in making more accurate prognostic assessments for tumor patients. Second, ultra-low-concentration protein detection applied to Alzheimer’s disease, cardiomyopathy, and cardiovascular diseases.

Guangyu Biology primarily relies on novel rare-earth fluorescent materials for quantitative immunofluorescence assays, developing a variety of detection platforms tailored for proteomic quantification. These include single-molecule detection platforms that leverage the high brightness of fluorescent materials to achieve ultra-high sensitivity and trace protein detection, as well as POCT products that capitalize on the high stability and brightness of these materials.

AI-Assisted Diagnosis Plays a Crucial Role in Early Screening and Diagnostic Processes. AI technology excels in image recognition, pattern recognition, and data analysis, enabling physicians to rapidly and accurately identify signs of pathology, thereby enhancing the accuracy and efficiency of early diagnosis.

By providing rapid and reliable screening results, AI-assisted diagnostic software can help physicians initiate interventions earlier, thereby improving treatment outcomes, particularly in primary care settings with limited medical resources.

AI-assisted diagnosis and molecular diagnostics are complementary. Molecular testing can provide quantitative biological and chemical information, which is crucial for the diagnosis and monitoring of certain diseases. Therefore, in medical diagnostics, AI-assisted imaging diagnosis and molecular testing should complement each other to jointly provide more accurate and comprehensive diagnostic results for patients.

AI-Driven Bioinformatics Analysis: A Future Direction for Early Cancer Screening Product DevelopmentWith technological advancements, the discovery of biomarkers may require multidimensional analysis. Pathologists are largely unable to perform comprehensive analysis and quantification, whereas AI can facilitate multi-layered analyses and predictive modeling to address complex challenges, thereby supporting the development of early cancer screening products.

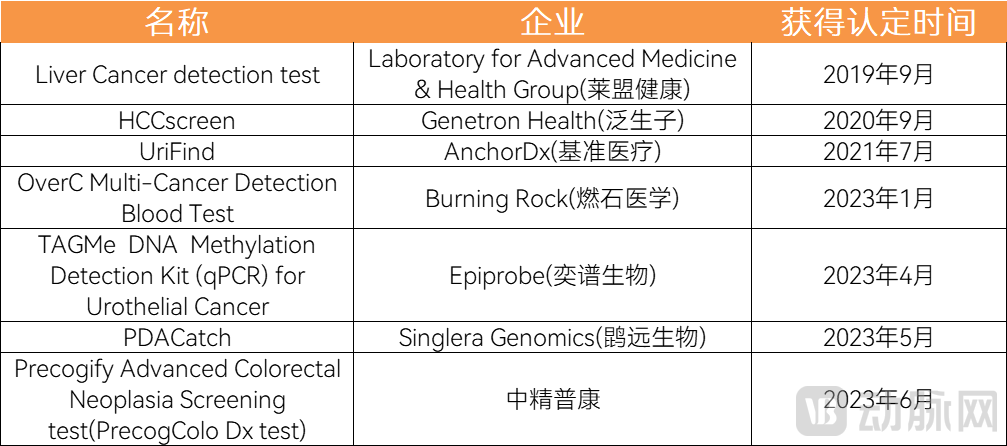

From replication to localized innovation, and further to original R&D-driven innovation, domestic technologies are gradually achieving breakthroughs. According to incomplete statistics, as of June 10, 2023, a total of 34 products had received the FDA’s Breakthrough Device Designation in the field of cancer screening/diagnosis, including seven from China.

It is evident that from the first domestic company receiving certification in 2019 to four companies achieving this status by 2023, overall breakthrough progress has been made.

Overview of Chinese Companies with FDA Breakthrough Device Designations

Image source: VCBeat.

In 2019, LAMH Health’s product Ganbeikang received the U.S. FDA Breakthrough Device Designation, and related research findings were published in top-tier global life sciences journals, including Nature, Science, PNAS, and Cell. In June 2023, Ganbeikang obtained approval from the National Medical Products Administration (NMPA), marking the issuance of the first certificate for early screening and detection of liver cancer, achieving a breakthrough with a sensitivity of 95.42% and a specificity of 96.02%.

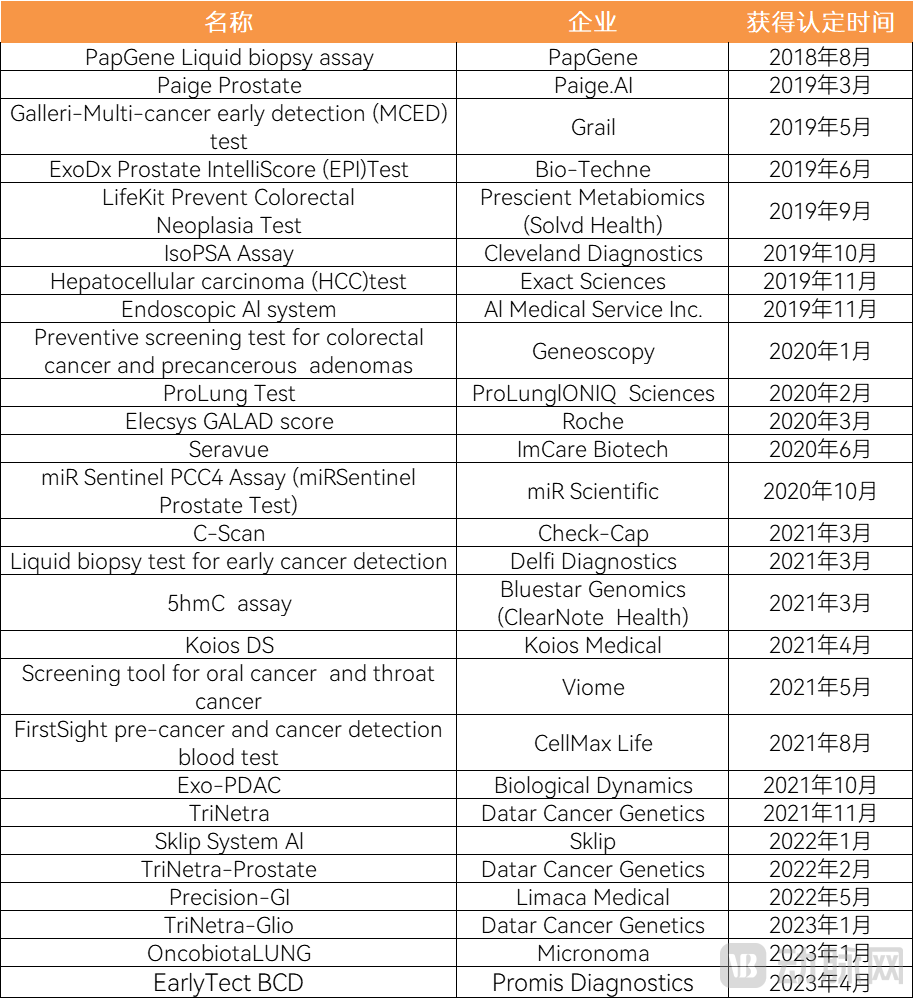

The table below summarizes foreign companies that have received FDA Breakthrough Device Designation for tumor screening/diagnostics. A total of 27 designations have been approved since 2018, as detailed below:

A Review of Overseas Companies with FDA Breakthrough Device Designations

Image source: VCBeat.

Large-scale prospective clinical trials constitute one of the primary barriers to the development of early screening products. It is essential to design phased clinical validation studies for early screening, particularly through multi-center, large-scale prospective research. The patient cohorts and resources required at each stage of this process typically increase progressively.

Generally, the prospective validation clinical trials for early screening products are costly. To achieve statistical significance, enrollment requires thousands to tens of thousands of participants, taking 3–5 years or longer, representing a substantial investment.

In addition to conducting large-scale prospective studies, building international influence also constitutes a significant barrier to entry. In this regard, collaborating with leading global enterprises to jointly undertake research projects is particularly critical. This not only demonstrates the company’s international strength but also enhances its brand influence.

For instance, Burning Rock Biotech collaborates with Academician Zhong Nanshan on the “Zhong Sheng Project,” a large-scale global prospective clinical study for the early diagnosis of lung cancer, which is conducted in partnership with the National Clinical Research Center for Respiratory Diseases and 23 other hospitals. In terms of internationalization, the company has partnered with the multinational pharmaceutical giant Johnson & Johnson on a lung cancer early diagnosis project, and jointly launched pan-cancer product development and industrialization initiatives with Twist Bioscience.

Commercialization: Mainstream Models Initially Validated, Innovative Models Emerging

At this stage, companies in the early cancer screening sector face a multitude of choices and diverse paths to commercialization. Beyond technological selection, there are various options regarding cancer types, business layout, and business models. Different choices entail differences in resource allocation, and distinct combinations may unleash varying levels of potential; therefore, achieving balance is critical. The figure below illustrates the choices facing early cancer screening companies.

The Choices Facing Early Cancer Screening Companies

Image source: VCBeat

Low Market Concentration; Mainstream Technologies Dominate the Landscape. Currently, the market concentration in the early cancer screening industry is low, primarily due to insufficient product differentiation among existing offerings.

Although domestic technologies have progressively achieved breakthroughs, evolving from imitation to localized innovation and ultimately to original research and development (R&D), most products based on original R&D are currently in the development stage and have not yet been launched on a large scale. The main products currently available on the market are based on ctDNA methylation, which constitute the dominant segment.

Resource Integration and Ecosystem Building Are the Themes of This Stage. At this stage, focusing on commercial implementation, channel integration and ecosystem building are the main themes. Not only have strategic alliances been formed with domestic enterprises, but some companies have also reached strategic cooperation agreements with leading international firms to achieve complementary resource advantages.

From the initial divergence in PCR and NGS strategies to their current synergistic development. Based on the business layouts of domestic early screening companies, they can be categorized into two main types: one type enters through the precision medicine track, leveraging NGS technology to integrate production and marketing, and establishing a comprehensive oncology portfolio covering companion diagnostics, early cancer screening, and minimal residual disease (MRD) detection across the entire cancer care continuum; the other type enters through the early screening track, relying on PCR technology, and focuses specifically on early screening solutions.

Certainly, from a practical perspective, PCR is more suitable for single-cancer applications and offers a faster pathway to regulatory approval, whereas NGS is better suited for pan-cancer applications and is the preferred choice for companies developing pan-cancer solutions. Consequently, we have observed that many enterprises are pursuing a dual strategy, simultaneously deploying both PCR and NGS technologies to achieve synergistic development across single-cancer and pan-cancer indications.

In terms of cancer type portfolio, domestic companies mostly adopt a strategy of “single cancer – combination of high-incidence single cancers – pan-cancer.”

Among single-cancer indications, colorectal cancer has the most mature industrialization both domestically and internationally. Although its incidence and mortality rates are not the highest, colorectal cancer demonstrates the greatest health economic benefits.

In terms of product offerings, colorectal cancer-related products are the most numerous and diverse. Meanwhile, an increasing number of companies are expanding their portfolios to include high-incidence cancers such as liver cancer, lung cancer, and gastric cancer.

Currently, early screening is expanding its portfolio across a wider range of cancer types. In addition to these high-incidence cancers, early screening initiatives now also cover urothelial carcinoma, pancreatic cancer, and esophageal cancer, resulting in an increasingly diverse product lineup.

For instance, Ameson has established 15 pipelines targeting the digestive system, gynecology, urology, high-incidence cancers, and pan-cancer indications. These include colorectal cancer, esophageal cancer, liver cancer, gastric cancer, and pancreatic cancer; cervical cancer, endometrial cancer, and combined testing for two major gynecological cancers; bladder cancer, ureteral cancer, renal pelvic cancer, and prostate cancer; lung cancer; combined testing for five major digestive cancers; and pan-cancer screening for twelve high-incidence cancers.

In addition, to create differentiation, there has been a strategic push in recent years toward the “early screening+” model, particularly the “early screening + other chronic disease screening + health management” approach.

In terms of business models, the current focus is primarily on four directions: hospital-side, checkup-side, public welfare projects, and consumer-side (C-end). From a practical perspective, the largest number of companies are deployed in the hospital-side and health checkup center sectors, with companies gradually entering the public welfare project space, while deployment on the consumer side remains relatively limited. The underlying reason lies in the distinct characteristics of each scenario, which result in varying returns on investment and differing levels of difficulty in market entry. Specifically:

Characteristics of Various Business Models

Image source: VCBeat

For consumer-facing (C-end) marketing, shifting mindsets and enhancing perceived value are key. Unlike hospital-facing channels and other scenarios, C-end marketing directly targets consumers, requiring distinct strategies. The critical challenge lies in building consumer trust in the product and ensuring recognition of its value.

First, a shift in mindset is required: approach the field from the perspective of consumer healthcare rather than serious medical care. Provide consumers with professionalism they can understand and value they can perceive. This value encompasses external value, internal value, and additional value.

For instance, external value encompasses aspects such as product appearance and naming, which should align with the needs and aesthetic preferences of consumer-end (C-end) users, avoiding an overly professional or serious tone. Intrinsic value refers to product performance, where credibility is demonstrated through expert endorsements, inclusion in clinical guidelines, and regulatory approvals, allowing consumers to intuitively perceive the product’s professionalism. Added value comprises supplementary benefits bundled with the purchase, such as related insurance coverage and access to specialist consultations, thereby enhancing the customer’s sense of getting more than their money’s worth.

In summary, regarding early screening products, it is essential to first adhere to regulatory compliance and clinical validation, establishing rigorous medical standards as the foundation for consumer healthcare. Secondly, emphasis should be placed on multi-channel collaborations, such as partnerships with insurance providers and health examination centers. Finally, innovation in user service and experience is crucial; based on accurate product performance, this should encompass the convenience of at-home testing, interpretation of results, and integrated insurance coverage.

For instance, Changweiqing has launched a compliant home-based testing and self-testing service model, wherein users collect samples at home, ship them free of charge to a central laboratory, and receive their reports within five working days. The service includes insurance coverage for negative results and reimbursement for colonoscopy in case of positive results. Additionally, the Youyou Tube home self-test delivers results in just 10 minutes.

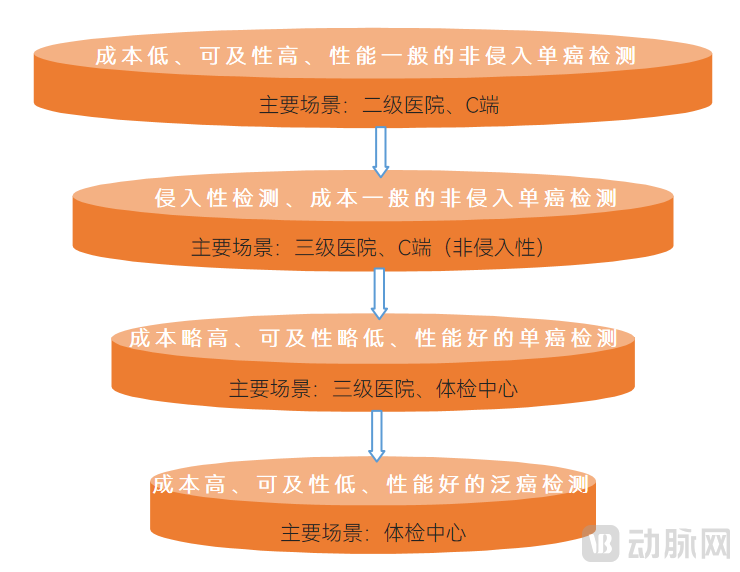

We stratified early cancer screening methods based on their characteristics and analyzed their current and future applications from the perspectives of market size and primary application scenarios, taking into account factors such as cost, accessibility, and performance.

We believe that, in the future, the first tier of the tumor early screening market may consist of non-invasive, single-cancer detection tests with low cost, high accessibility, and moderate performance. These products, priced at around RMB 100, may or may not be covered by medical insurance. Their primary application scenarios include primary healthcare institutions, the consumer market (C-end), and insurance companies; however, such solutions have not yet been realized.

The second tier comprises the current status quo, namely invasive tests and non-invasive tests with moderate costs. Invasive tests are primarily utilized in tertiary hospitals, while non-invasive tests with moderate costs are mainly applied in tertiary hospitals and the consumer market. The third tier consists of single-cancer detection products that offer high performance but at slightly higher costs and lower accessibility; these are primarily used in tertiary hospitals and health examination centers. The fourth tier includes pan-cancer detection products characterized by high performance, high costs, and low accessibility, which are mainly deployed in health examination centers, as detailed below:

Early Cancer Screening: Detection Methods, Products, and Application Scenarios

Image source: VCBeat

The comparative reimbursement prices of endoscopy and early cancer screening products are a key factor. Taking colorectal cancer, which has the most mature commercialization, as an example, the cost of a colonoscopy in the United States is approximately $2,125, whereas Cologuard is priced at only around $500 and is covered by commercial insurance. The substitution effect for colonoscopy is significant, which has contributed to Cologuard’s remarkable single-product sales success.

Additionally, considering price factors, the average market cost for colonoscopy in Hong Kong ranges from HKD 7,800 to HKD 10,000, with most expenses covered by commercial insurance. Therefore, besides expanding overseas, establishing a presence in regions such as Hong Kong, China is also a viable option.

“Belt and Road” countries exhibit a high level of acceptance for Chinese products, making them the preferred destinations for overseas expansion at this stage. During the pandemic, these regions received aid from China, through which China exported not only products but also technology.

Whether for antigen or nucleic acid testing, Chinese products have gained strong recognition across the “Belt and Road” regions. Notable successes in Southeast Asia (such as Malaysia and Indonesia) and the Middle East have laid a solid foundation for the global expansion of early screening products.

For instance, Kunyuan Bio has actively expanded into overseas markets. In Europe and the Asia-Pacific region, it has partnered with Sansure Biotech to achieve sales in Hong Kong (China), South Korea, Hungary, Malaysia, and other areas. In the United States, its early detection technology for pancreatic cancer has received FDA Breakthrough Device Designation, and it has launched Laboratory Developed Tests (LDTs) in collaboration with multiple third-party clinical laboratories.

Specifically, within Southeast Asia, countries with relatively higher paying capacity, such as Singapore, also adopt the commercial health insurance model. Moreover, existing products in these markets have not established significant brand barriers, indicating substantial market potential.

According to Frost & Sullivan, the Southeast Asian market size is projected to grow from USD 33.4 million in 2020 to USD 2.79 billion in 2030, at a compound annual growth rate (CAGR) of 55.7%.

Currently, grassroots livelihood projects have achieved a closed-loop service for early screening and early diagnosis. For instance, in May 2023, the colorectal cancer screening project of the Tumor Prevention and Control Center under the Guangdong County-level Medical Consortium was officially launched. This initiative targets high-risk individuals identified through population-wide screening and confirmed patients, establishing a "county-township joint" full-lifecycle management mechanism within the county-level medical consortium, as well as a collaborative model between "tertiary hospitals and county-level medical consortia." It aims to realize a comprehensive prevention and control mechanism for primary, secondary, and tertiary prevention of colorectal cancer, along with an early two-way referral system, thereby achieving closed-loop management for the early detection and treatment of colorectal cancer patients.

In summary, with the further deepening of the tiered diagnosis and treatment system and the formation of medical consortia, a “trinity” prevention and control system comprising public health institutions, primary care hospitals, and specialized hospitals will be established. Cancer early screening will form a grassroots coverage network alongside the tiered diagnosis and treatment system and medical consortia, facilitating the creation of a closed-loop health management model for major chronic diseases such as cancer.

For instance, Genetron Health has not only established an integrated management chain of “technology upgrade – community screening – hospital referral – treatment follow-up” for public welfare projects in Huishan District, Wuxi City, but also created a model project for “rural revitalization – medical assistance” in Dafang County, Guizhou Province, by launching the “Regional Comprehensive Prevention and Control Demonstration Project for Early Liver Cancer Screening,” thereby achieving the goal of “managing serious illnesses within the county.”

Trend: Home-based testing drives significant growth, with early screening potentially playing a key role in cost containment

ctDNA methylation has become the mainstream approach, with the rise of multi-omics and combined detection strategies, driven by the concurrent advancement of multiple technologies and platforms. From PCR and NGS to innovative omics beyond genomics—such as proteomics, metabolomics, and microbiomics—and further to multi-omics and combined detection, the technological landscape for early cancer screening continues to expand and diversify.

Currently, ctDNA methylation is the mainstream and most widely applied approach. Meanwhile, multi-omics and combined detection methods are gradually emerging, driven by the synergistic advancement of multiple technologies and platforms, which has led to breakthroughs in proprietary technologies.

Furthermore, the empowering role of AI is becoming increasingly prominent; it is currently primarily used for assisted diagnosis and will play a greater role in bioinformatics analysis for biomarker screening in the future.

Single-cancer and pan-cancer products have distinct positioning and will achieve co-development across different scenarios. Currently, technical validation has largely confirmed that PCR is more feasible for single-cancer applications, while NGS is more feasible for pan-cancer applications.

Certainly, given the cost differences between PCR and NGS, as well as the varying R&D complexities for single-cancer versus pan-cancer applications, these two product categories will differ in their positioning and use cases.

Single-cancer tests are more suitable for routine health checkups in the general population and for screening and diagnosis among clinically high-risk groups, whereas pan-cancer tests are better suited for high-net-worth individuals with strong health management needs, serving their premium health management purposes.

Home-based testing will eventually see significant volume growth, and closed-loop management can enhance user stickiness. In recent years, cancer early screening products on platforms such as JD Health have achieved impressive sales, preliminarily revealing the substantial growth potential in the consumer market. Meanwhile, the pandemic has reinforced people’s habit of home-based testing. As health awareness continues to rise, home-based early screening tests are poised for substantial adoption.

In this process, the key lies in enhancing user stickiness and improving user satisfaction; therefore, closed-loop health management is essential.

For instance, RayBiotech is committed to leveraging digital tools to build an integrated, closed-loop health management model that combines “online + offline” services and encompasses “prevention + diagnosis + intervention.” Users can easily conduct at-home colorectal cancer risk testing through a streamlined process: “place order online – collect sample at home – ship via courier for testing – receive report on mobile phone.”

Implementation of in-hospital LDT pilot documents faces challenges, potentially leading to a tortuous path forward. Responding to calls from the industry, two sets of guidelines for in-hospital LDT pilots were successively released this year, marking the eventual transition of LDT in-hospital pilots into practical implementation. Notably, under this policy framework, regulatory oversight of hospitals will shift from the National Health Commission (NHC) to the National Medical Products Administration (NMPA).

Overall, the current documents remain difficult to implement in practice, particularly regarding the requirement for enterprises to share intellectual property (IP) with hospitals. On one hand, investors place significant emphasis on corporate IP; on the other, IP constitutes a core asset for enterprises, making shared ownership inherently challenging. At present, there is no well-established solution to this issue, necessitating ongoing coordination and alignment among hospitals, enterprises, and regulatory authorities.

In short, while twists and turns are inevitable, we have reason to believe that future in-house LDT pilot programs will become an optional pathway for innovative projects, with greater standardization and a more balanced approach between enterprises and hospitals.

At present, early cancer screening products have not fulfilled their role in cost containment within insurance underwriting. Regarding the coverage amount for confirmed cancer diagnoses, insurers typically determine this through actuarial calculations that integrate the overall probability of developing cancer, average treatment costs, and the premiums paid by the insured. The coverage amounts are generally RMB 200,000, RMB 300,000, or higher.

This means that once the insured is diagnosed with cancer, the insurance company must pay out a substantial amount, and the payout remains the same regardless of whether the cancer is diagnosed at an early or late stage. Consequently, insurers have no incentive to encourage policyholders to undergo early screening; in fact, it is more financially advantageous for insurers if the diagnosis occurs later during the coverage period.

From a health economics perspective, the cost of screening for many types of cancer is far lower than the cost of treatment; therefore, the fixed-benefit payment model has failed to leverage the cost-containment potential of early cancer screening products within insurance coverage.

Cost containment for early screening in China requires the accumulation of real-world data. Currently, there is insufficient evidence-based medical data in China to demonstrate the health economic benefits of early screening, and diagnosis and treatment costs remain relatively low. Insurance companies currently lack actuarial data, yet a few are still exploring cost containment strategies in cancer early screening.

We believe that as the health economic benefits of early cancer screening products are demonstrated, such screening may play a role in cost containment in the future. Meanwhile, regardless of whether fixed-amount payment or reimbursement-based models are adopted in the future, it may be more scientifically sound for insurance actuarial practices to take into account specific cancer types and stages at diagnosis.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:

Chapter 1 Overview: Financing Prioritizes Practical Implementation, with Frequent Industrial Collaborations

1.1 Development: Large-scale screening has not been implemented for most cancer types in China, and overall development is still in its nascent stage.

1.2 Financing: A stronger emphasis on practical implementation, with opportunities still available for new technologies and solutions

1.3 Volume Surge: Inclusion of Methylation Testing in National Reimbursement May Establish Early Cancer Screening Clinics as Permanent Hospital Departments

Chapter 2 Technology: Synergistic Development of Mainstream and Innovative Omics, and the Rise of Original Research

2.1 Genomics: ctDNA Methylation is the Mainstream, While Fragmentomics is in Its Infancy

2.2 Innovative Omics: Co-development of Transcriptomics, Proteomics, Metabolomics, and Microbiomics, and the Rise of Multi-omics

2.3 Detection Technologies: Emergence of Innovative Detection Technologies and AI-Enabled Assisted Diagnosis

2.4 Originator Drugs: The Rise of Originators, with Prospective, Large-Scale Studies as the Barrier

Chapter 3 Commercialization: Initial Validation of Mainstream Models and the Emergence of Innovative Models

3.1 Stage: Commercialization is in its early stages, with low market concentration

3.2 Pathway: Synergistic Development of PCR and NGS, with an Increasingly Diverse Early Screening Product Portfolio

3.3 Models: Variations in Mainstream Model Layouts, with the Consumer Segment as a High-Potential Market

3.4 Exploration: The “Belt and Road” Region Emerges as the Mainstream Market for Overseas Expansion, with Infrastructure in Place and Volume Growth Pending

Chapter 4 Trends: Home-Based Testing Drives Incremental Growth, and Early Screening May Play a Role in Cost Containment

4.1 Technology and Products: Synergistic Advancement of Multiple Technologies and Platforms, Concurrent Development for Single-Cancer and Pan-Cancer Applications

4.2 Scenario: Home-based testing can drive significant incremental growth, while in-hospital LDT pilots may advance with challenges

4.3 Payment: Early cancer screening is gradually playing a cost-containment role in insurance coverage

Chapter 5 Corporate Case Studies

5.1 New Horizon Health – A Leader in Early Cancer Screening and At-Home Testing in China

5.2 Light and Biology: Leveraging Proteomics for Early Screening of Critical Diseases

5.3 Genetron Health—Leading Technological Innovation and Upgrading to Make Early Cancer Screening More Accessible

5.4 Ameson—Providing Superior Solutions for Early Cancer Screening

5.5 Basecare Medical – Dedicated to Developing First-in-Class Products for Early Cancer Screening and Diagnosis

5.6 LAMH Health: An AI-Driven Innovator in Early Cancer Screening and Diagnosis

5.7 Kunyuan Biotechnology: Building a Leading Enterprise in China’s Cancer Early Screening and Liquid Biopsy Sector

5.8 Zhongjing Medicine – Providing Non-Invasive Urine Medical Testing Solutions

5.9 Zhongjing Pukang—Providing Gut Microbiota Metabolite Testing and Gut Health Management Services

5.10 RayBiotech – Empowering the Digital and Automated Upgrading of the Early Cancer Screening Industry

Please scan the QR code to add the assistant and obtain the full report. If you have already added the assistant, please initiate a conversation:

Special Acknowledgments (in order of research interviews):

Mr. Liu Sheng, Senior Product Manager at Qiuzhen Medicine; Dr. Zhang Lianglu, Chairman and General Manager of Ameson; Dr. Dong Lanlan, Deputy General Manager of R&D and Manufacturing at Ameson; Mr. Sun Nengbiao, Marketing Director of Ameson; Genetron Health; Dr. He Hao, Founder and General Manager of Light & Biology; Dr. Dai Xudong, Founder and CEO of Zhongjing Pukang; Ms. Ding Yaqing, Global Vice President of LAMH Group; Dr. Xu Jianfeng, Vice President of Technology at LAMH Health; Mr. Long Hao, Product Director at LAMH Health; Mr. Yuan Shoudao, Founder and CEO of Zhongjing Medicine; Dr. Fan Jianbing, Founder and CEO of Burning Rock Biotech; Mr. Zhang Jiangli, Co-founder and CEO of GenomiCare; New Horizon Health.