Medical Industry Investment Shifts Upstream Amid Capital Winter

Gaorong Ventures

Venture Capital Institution

Legend Capital

Early-stage venture capital and growth-stage private equity investment institutions

BIOENFINE

Supplier of Animal Cell Suspension Culture Products and Services

In the first half of 2021, the total investment and financing in China's healthcare industry amounted to approximately RMB 92.7 billion. However, in the first half of 2023, this figure dropped to RMB 41.1 billion, less than half of that in the first half of 2021. Therefore,In many articles reviewing investment and financing activities in the healthcare industry during the first half of 2023, it is commonly believed that a capital market winter has arrived.。

However, although the total amount of financing has dropped significantly, the number of financing events has been steadily increasing. In the first half of 2021, there were approximately 546 investment and financing events in China's healthcare industry; in the first half of 2023, this number rose to approximately 650. What is puzzling is thatDuring the so-called "capital winter," where did the funds go in 650 financing deals? Which companies successfully secured funding? Which niche sectors were in high demand?

VCBeat has found through analysis that the upstream sector of the healthcare industry has received significant attention from investors.

In the secondary market, Boxun Bio, an upstream life sciences company, recently completed a successful IPO, while Chenguang Medical, a core component supplier for magnetic resonance imaging (MRI) systems, successfully listed on the Beijing Stock Exchange at the end of 2022.

Moreover, upstream enterprises in the healthcare industry are experiencing a doubling trend in revenue. For instance, iRay Technology, an upstream supplier of medical imaging equipment, saw its annual revenue grow from RMB 780 million to RMB 1.55 billion over the past three years, representing more than a twofold increase. Similarly, Haitai XinGuang, an upstream provider for endoscopes, witnessed its revenue rise from RMB 275 million in 2020 to RMB 477 million in 2022, nearly doubling. As the downstream healthcare market continues to achieve breakthroughs and downstream companies increasingly procure domestically produced core components and materials, upstream enterprises in China’s healthcare industry are ushering in a new wave of development opportunities.

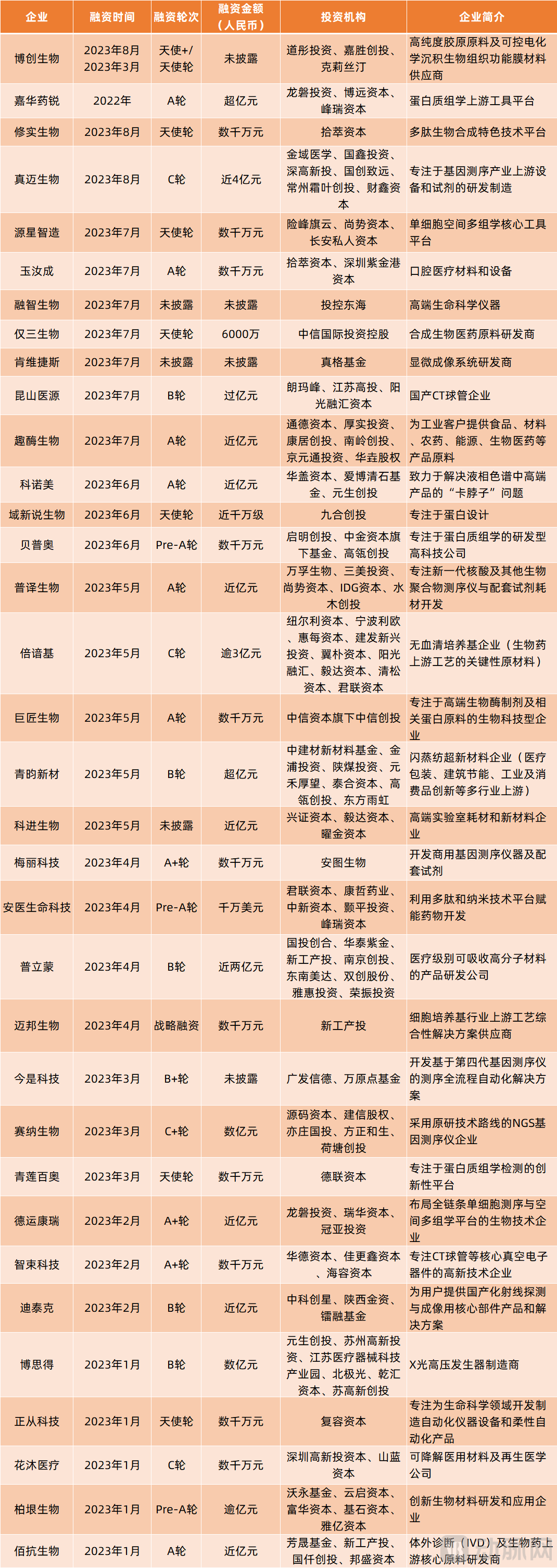

In the primary market, dozens of venture capital firms are rushing in to embrace upstream companies in the healthcare industry, such asUpstream Raw Material Suppliers for the Life Sciences IndustryGeneIII Bio-Tec, Jiahua Yaorui, Qumei Biotech, BIOENFINE, Jujiang Biotech, Baikang Biotech, and Maibang Biotech,Upstream Life Sciences Tools CompaniesYuanxing Intelligent Manufacturing, Rongzhi Biotechnology, Meili Technology, Puyi Biotechnology, Zhengcong Technology,Upstream Enterprises in the Medical Imaging Equipment IndustryKunshan Yiyuan, Shansiwei, Ditek, ZhiShu Technology, Postek,Upstream Innovative Materials Companies in the Medical Device IndustryQingyun New Materials, Pulimon, Huamu Medical, Boyin Bio…… all completed a new round of financing in the first half of the year.

According to incomplete statistics, in the first half of 2023, the upstream sector of the medical industry completed over 32 financing and investment deals, with a total financing amount exceeding RMB 2.4 billion. Prominent investment institutions, including Legend Capital, Nanjing New Industry Emerging Industry Investment Management Co., Ltd., Gaorong Ventures, Hillhouse Ventures, Matrix Partners China, IDG Capital, Vensource Capital, Boyuan Capital, Daotong Investment, and ZhenFund, have all been actively positioning themselves in the upstream segment of the healthcare industry.

(Financing Status of Some Upstream Enterprises in the Medical Industry in the First Half of 2023)

Why Are Investment Firms Collectively Betting on the Upstream Healthcare Sector During the Capital Winter? How Can Upstream Enterprises Achieve Counter-Cyclical Growth? Which Subsectors Within the Upstream Healthcare Space Are Attracting More Investor Attention? To Address These Questions, VCBeat Interviewed Multiple Investors and Compiled This Article.

Currently, there is a prevailing view in the market that intensifying competition among investors has turned downstream investment opportunities into a red ocean, compelling them to gradually shift their focus upstream toward markets with smaller scales.

In fact, this statement is inaccurate. On the one hand, although the investment logic has shifted in some sectors due to factors such as policy and market dynamics, many downstream segments within the healthcare industry remain in a blue-ocean state, including niche areas such as ophthalmic consumables, surgical robots, brain science, and generative AI.

On the other hand, every successful enterprise has emerged from fierce market competition, such as Meituan prevailing in the “Group-Buying Wars,” Pinduoduo rising from the “E-commerce Wars,” and Tencent winning out amid the “Social Media Encirclement.” Therefore, from an investment perspective, there are still numerous blue-ocean opportunities in the downstream healthcare market. Moreover, even in highly competitive segments, some institutional investors choose to bet on potential industry leaders within these red-ocean markets, aiming to achieve excess returns.

Based on the above conclusions, it can be observed that:The heated financing in the upstream sectors of the healthcare industry is not driven by investor involution.

Liu Haitao, Investment Director at Legend Capital, stated, “The surge in financing and investment in the upstream medical sector is driven by strong stimuli from multiple macro-environmental changes. An increasing number of downstream enterprises are testing and procuring domestically produced core components and raw materials to secure supply chain stability and drive cost reductions. This has created a systemic opportunity for domestic upstream companies to step into the spotlight, with expectations of rapid growth.”

Taking high-end proteins, enzymes, peptides, culture media, and other upstream raw materials for life sciences as examples, domestic enterprises in this sector developed extremely slowly before the pandemic. The market was largely monopolized by international giants. Moreover, downstream domestic companies were concerned about the inferior quality of domestically produced products and the risks associated with switching supply chains, making them reluctant to abandon international giants in favor of domestic alternatives.

“However, as a global public health emergency, the pandemic not only affected the production capacity of international giants but also disrupted the stability of their supply chains. For instance, shortages emerged in supplies from overseas giants to Chinese pharmaceutical companies, leaving downstream clients unable to place orders smoothly. This has compelled domestic enterprises to give greater consideration to domestically produced products that they previously dared not use, were reluctant to use, or lacked the incentive to adopt,” Liu Gaopeng from Nanjing New Industry Emerging Industry Investment Management Co., Ltd told VCBeat.

In this scenario, orders for upstream life sciences raw material suppliers in China have surged, rapidly attracting investor attention. From an investment perspective, while the pandemic, as an unforeseen event, has created opportunities for domestic substitution in the upstream life sciences raw materials industry, whether related companies can achieve leapfrog development ultimately depends on their technology, products, and services.

“Fortunately, leading domestic upstream raw material suppliers in the life sciences sector have not only achieved technological breakthroughs but also won the recognition of downstream enterprises by leveraging advantages such as short supply lead times, high cost-performance ratios, customized services, and rapid response capabilities,” Liu Gaopeng continued.

For example, the lead time for domestically produced catalog media is generally 2–4 weeks, whereas that for imported products is typically three months or longer. In terms of price, some domestic basal media cost only about one-third of their imported counterparts, while certain domestic feed media are priced at nearly two-thirds of imported options.

Most importantly, domestic companies have achieved technological breakthroughs and are capable of delivering high-quality products. Otherwise, neither advantages in supply lead times nor pricing would be sufficient to dislodge orders from international giants.

Le Beilin, Executive Director at Gaorong Ventures, cited as an example: “In the niche segment of protein raw materials, Yinjia Bio has developed more than 50 high-end proteins, some of which are first-of-their-kind in China, such as calcium-regulated calcineurin (PP2B), adenylyltransferase, and specialized non-viral vector proteins for cell therapy. Meanwhile, Yinjia Bio has also developed a range of raw materials that rival imported products, such as sequencing-grade recombinant trypsin. The performance of these products reaches or even surpasses international standards, thereby facilitating their acceptance by downstream markets.”

For another example, in the field of cell culture media, Maibang Biotechnology, as a domestic supplier, has achieved increased yield and reduced raw material costs while ensuring quality. In addition, the quality of several of Maibang Biotechnology’s culture media products has even surpassed that of imported brands, and they are widely used in various stages including biopharmaceutical R&D, clinical trial applications, and commercial production. “More and more customers have personally experienced the cost reduction and efficiency improvement brought about by the localization of the industrial chain,” added Liu Gaopeng.

As investors conducted in-depth due diligence, they found that leading domestic upstream life sciences raw material companies have gradually gained recognition in the downstream market in terms of products, technology, and services. Downstream enterprises are more willing to renew orders with relevant domestic upstream suppliers. Against this backdrop, their interest in the upstream life sciences raw materials industry has grown even stronger.

Even so, prudent investors require another investment rationale: long-term development potential and future exploratory capacity. Recent policy and market shifts have conveniently provided investors with a satisfactory answer.

From a policy perspective, initiatives such as centralized volume-based procurement have strengthened the negotiating power of medical insurance funds on the payment side. Meanwhile, the approval of similar products has intensified market competition, compelling downstream enterprises to place greater emphasis on upstream production costs and efficiency. This has created stronger incentives for downstream companies to source domestically produced upstream raw materials that offer lower costs and consistent or superior quality.

In terms of market size, the upstream market space is expanding alongside the stable growth and continuous expansion of the downstream market. Moreover, as an increasing number of domestic enterprises go global and compete in international markets, they have not only broken through the ceiling of the downstream market but also accelerated the expansion of the upstream market.

Driven by the aforementioned events, insights, and logic, a significant influx of investors has poured into the upstream life sciences raw materials sector. A cohort of companies, including GeneIII Bio-Tec, Jiahua Yaorui, QuMei Biotech, BIOENFINE, and Jujiang Biotech, have successively completed financing rounds to accelerate their development.

Many people believe that the upstream sector has a smaller market size.

In fact, this is a misconception. Just as the upstream sector of new energy vehicles gave rise to CATL, a company with a market capitalization in the trillions, and the upstream ventilator sector produced Meihao Medical, valued at RMB 17.8 billion, the upstream segment of the vast healthcare market can also give birth to companies with substantial market valuations.

In the life sciences tools market, Soochow Securities estimates that excluding laboratory equipment, the total domestic market size for life sciences tools in China exceeded RMB 60 billion in 2020, growing continuously at a compound annual growth rate (CAGR) of 20% from 2020 to 2024. This growth is driven by strong demand in downstream sectors such as pharmaceutical innovation, mRNA technology, and cell and gene therapy, coupled with global pharmaceutical companies’ R&D expenditures surpassing USD 100 billion, which has fueled sustained expansion in the upstream life sciences tools market.

The proteomics market, serving as an upstream tool platform, is widely applicable across various scenarios including scientific research, medical diagnostics, biopharmaceuticals, and agriculture, forestry, animal husbandry, and fisheries. Specifically, the proteomics market is valued at approximately $19 billion in scientific research, $16 billion in diagnostics, and $20 billion in pharmaceuticals. Given its significant value in target discovery, new drug development, and precision medicine, proteomics has emerged as the next major industry opportunity collectively favored by the scientific, industrial, and investment communities, following genomics.

The primary downstream application scenarios for gene sequencing are clinical testing and research services. Furthermore, gene sequencing is increasingly being applied in various fields, including forensic identification, environmental pollution control, biodiversity conservation, and agricultural and livestock breeding. According to Illumina’s projections, the global genetic testing market exceeds $20 billion. In the research services segment, as research institutions, pharmaceutical companies, CROs, and third-party laboratories extensively adopt gene sequencing, this sector accounts for approximately 30% of the total gene sequencing market. Currently, the two most mature application areas for gene sequencing are reproductive health (e.g., non-invasive prenatal testing) and oncology (e.g., screening and diagnosis), both representing markets valued in the billions of dollars.

In the upstream sector of innovative materials for medical devices, it is difficult to estimate the market size due to the broad application scope of these materials. However, a single grade of innovative medical material can be applied across various medical devices; for instance, medical-grade biodegradable materials are used in products such as cardiac stents, bone scaffolds, and implants. With the large-scale adoption of related medical devices, the revenue from these new materials is expected to experience breakthrough growth, offering companies the opportunity to become exclusive monopoly suppliers of core materials for specific products. A case in point is CeramTec, which serves as the sole supplier of ceramic materials to global joint replacement manufacturers including Johnson & Johnson, Smith & Nephew, Stryker, Zimmer Biomet, AK Medical, Chunli Medical, and Weigao Orthopaedics, thereby monopolizing the supply of core upstream components for ceramic artificial joints, namely ceramic heads and liners.

The market for upstream core components of medical devices requires analysis by different market segments. Among these, the "chokepoint" core components of high-end medical devices have a relatively large market due to technical barriers and high usage volume. For instance, Chenguang Medical has launched an IPO in the upstream core component market for magnetic resonance imaging (MRI), while Haomei Medical and Yihé Jiaye have listed on the secondary market for upstream core components of ventilators. In contrast, the market space for core components of mid-to-low-end medical devices is smaller, with limited market prospects.

Overall, the upstream segment of the healthcare industry boasts a substantial market size, and most upstream tracks have applications in non-healthcare sectors as well, further expanding their market potential. This is the core reason why investors who firmly believe in the “big pond, big fish” principle favor upstream tracks.

Nevertheless, it is undeniable that the market size and prospects in certain upstream segments are indeed relatively limited, making these areas less attractive to investors. For instance, in the life science instrumentation industry where Boxun Bio operates, although there is a wide variety of product categories, the market size for any single category (or niche segment) is relatively small. Therefore, companies in the life science instrumentation industry primarily expand their product portfolios through external mergers and acquisitions or independent R&D, ultimately evolving from single-domain service providers into one-stop scientific research service providers.

Breaking down the upstream segment of the healthcare industry reveals numerous niche sectors. Amidst these many niches, which sectors do investors favor? Which companies are their top picks?

According to statistics from VCBeat, niche sectors such as gene sequencing, single-cell spatial omics, proteomics, innovative medical materials, and upstream core components for CT equipment are experiencing a surge in financing.

In the field of gene sequencing, Genetron Health, Qitan Technology, Puyi Biotechnology, Meili Technology, and Jinshi Technology, among other related companies, all completed financing in the first half of the year. Interestingly, Genetron Health is led by a third-party medical testing industry leaderKingMed Diagnosticsand Guoxin Investment, a state-owned investment institution, jointly led the investment; Puyi Bio is a leading domestic POCT enterpriseWondfo BiotechLead Investor: Meili Technology, by a Leading IVD EnterpriseAutobioExclusive Strategic Investment... Industrial Investors Are Increasing Their Bets on Gene Sequencing.

It is reported that gene sequencing is an innovative genetic testing technology that can determine gene sequences from blood, saliva, or other tissue samples, providing guidance for life science research, clinical diagnosis, and treatment. Based on different principles, mainstream sequencing technologies have evolved into four major categories: first-generation sequencing (Sanger method), second-generation sequencing (NGS), third-generation sequencing (SMRT single-molecule real-time sequencing), and fourth-generation sequencing (nanopore technology).

Currently, gene sequencing is primarily applied in clinical diagnostics and research services. In the realm of clinical diagnostics, gene sequencing is widely used in reproductive health and oncology. For instance, non-invasive prenatal testing (NIPT) for fetal chromosomal aneuploidy helps physicians and patients assess in advance whether the fetus is affected by aneuploidy-related disorders.

Industry insiders anticipate that with the development of fourth-generation sequencing technology, along with the exploration of downstream markets and the expansion of application scenarios, the gene sequencing market will further break through its current ceiling.

In the field of proteomics,Jiahua Yaorui, Beipuao, Aikesheng Biotech, Keluosi Biotech, Qinglian Baiao, and other related companies all completed financing in the first half of the year, with investments from prominent firms including GL Ventures, Qiming Venture Partners, CICC Capital, Boyuan Capital, Taiyu Investment, and Shuimu Ventures.

It is reported that proteomics employs large-scale, high-throughput, and systematic approaches to analyze and study the composition of proteins in cells, tissues, or organisms, as well as their patterns of change. Proteomics holds significant value in the discovery of new therapeutic targets, the development of novel drugs, and the guidance of precision medicine in clinical practice.

On one hand, the growing demand for precision diagnostics and personalized medication is driving continuous growth in the proteomics market, particularly in areas such as companion diagnostics and precision therapy. On the other hand, an increasing number of pharmaceutical companies are leveraging proteomics technologies to develop new drugs and are significantly ramping up their R&D investments in this field, thereby rapidly expanding the global proteomics market. Especially in the fields of cancer, cardiovascular diseases, and neurodegenerative disorders, researchers have identified a growing number of novel protein biomarkers based on proteomics technologies in recent years and are developing corresponding new therapeutics.

With continuous breakthroughs in proteomics technologies, the global capital market widely recognizes them as the next wave of industry opportunities following genomics.

In addition to gene sequencing and proteomics, multiple companies in niche sectors such as single-cell spatial omics, innovative medical materials, and upstream core components for CT equipment have also secured financing. These include Deyunkangrui and Yuanxing Zhizao in the field of single-cell spatial omics; Qingyun New Materials, Pulimeng, Huamu Medical, and Boyin Biology in the field of innovative medical materials; and Kunshan Yiyuan, Shansiwei, Ditaik, Zhisu Technology, and Postek in the field of upstream core components for CT equipment.

Looking at the upstream companies that successfully secured financing in the first half of the year, innovation is their common hallmark. As one investor stated, “Regardless of the sector, only companies with strong innovative capabilities will gain recognition from investors.”

In terms of investment tracks, investors favor the upstream sectors of biopharmaceuticals and life science tools, which offer larger market spaces and promising prospects. In contrast, the upstream medical device sector attracts relatively less investor attention due to the fragmented nature of device products and its smaller market size.