Malo Clinics Files for Hong Kong IPO: Premium Dental Chain Reports RMB 1.2 Billion Revenue Over Three Years with Dentists Averaging RMB 2.4 Million Annual Output

MEI WEI DENTAL GROUP

Oral Health Service Provider

ARRAI

Oral Healthcare Service Provider

Another Leading Dental Company Begins Its IPO Sprint!

Following the beginning of this yearSmartee DentalRegistered for tutoring filing with the Zhejiang Securities Regulatory Bureau,SomaMedChiNext IPO Application Accepted,Dengkang Oral CareAfter becoming one of the first new stocks under the registration-based IPO system on the Main Board of the Shenzhen Stock Exchange,Ma Long DentalIt also filed its prospectus with the Hong Kong Stock Exchange on August 22, seeking a listing on the Main Board.

With this, leading enterprises across all segments of the dental industry chain—from oral care and dental instruments to dental services—have either prepared for or completed their initial public offerings (IPOs) this year, once again underscoring the sector’s robust growth momentum.

The primary market remains equally hot. Against the backdrop of a cooling overall venture capital environment, a host of well-known dental companies, including MEI WEI DENTAL GROUP, Dentifine, Eya Group, Shenzhen Yuru, Meiao Dental, Gendent, Chenglian Technology, Sailuo Medical, Wellplaece, and Proclaim, have completed new rounds of financing this year.

Returning to Malo Dental itself, it has been a star enterprise widely watched by the industry since its inception., prior to filing its prospectus, it had secured six rounds of financing, with investors including prominent institutions such as Honghui Fund, Vertex Capital, Greenland Group, Noah Asset Management, CICC, and Huaxi Securities.

This is related to its market expansion achievements. According to a report by Frost & Sullivan, ranked by 2022 revenue, Malo Dental ranks 9th among all private dental healthcare service providers in China,Ranked 2nd among all high-end private dental care service providers in China, placing it at the forefront of the industry.

(Malong Dental’s business scale. Image source: Prospectus)

(Malong Dental’s business scale. Image source: Prospectus)

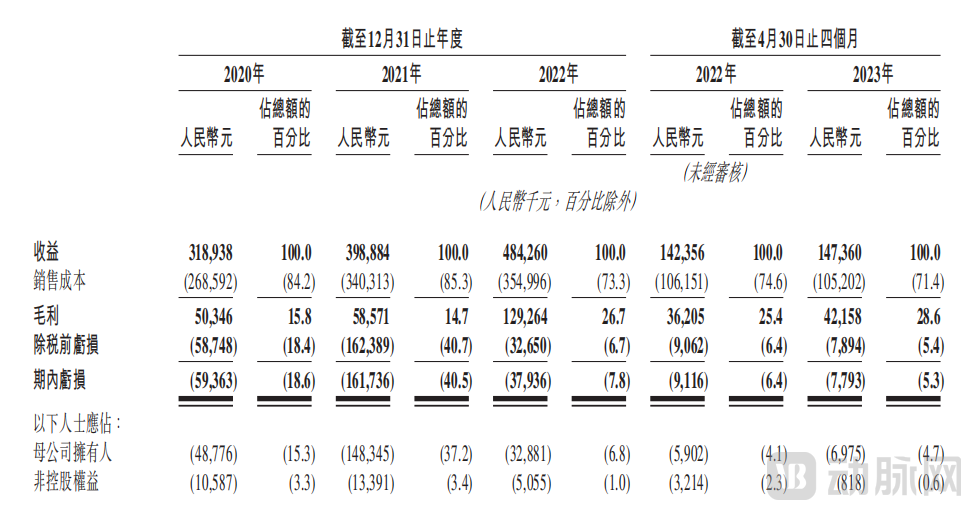

In terms of financial data, Malo Dental's revenues from 2020 to 2022 were RMB 319 million, RMB 399 million, and RMB 484 million, respectively.Total Revenue Exceeds RMB 1.2 Billion Over Three Years; In the first four months of 2023, Malong Dental's revenue increased slightly from RMB 142 million in the same period of 2022 to RMB 147 million.

It is worth noting that in 2022, Malong Dental’s operational efficiency led the industry, with each dental chair generating an average annual revenue of over RMB 1.5 million and each dentist contributing an average annual revenue of over RMB 2.4 million.

Of course, losses have also been ongoing. From 2020 to the first four months of 2023, Malong Dental's net losses were RMB 59.363 million, RMB 161.736 million, RMB 37.936 million, and RMB 7.793 million, respectively, showing a clear trend of narrowing.

(Image source: Malong Dental’s prospectus)

(Image source: Malong Dental’s prospectus)

What results did Malo Dental present in its IPO bid? What new industry trends were revealed in its prospectus? What lies behind the sustained boom in the dental care sector? And what challenges and solutions remain? In response to these questions, VCBeat will provide a detailed analysis below.

Targeting the High-End Market,

Malong Dental Makes Final Push for IPO After 10 Years of Deep Roots in China

The story of Malo Clinic began in Portugal in 1995.

At that time, Dr. Malo, then only 24 years old, decided to establish a dental clinic. After considering multiple locations, he settled on Lisbon, and this clinic later became the Malo Clinic.

An interesting anecdote is that before founding Malo Clinic, the founder worked as a model and played for the Portuguese rugby team, even participating in the Rugby World Cup. It was the establishment of Malo Clinic that set Dr. Malo’s destiny in motion: driven by his passion for the dental industry, he made a series of inventions and secured patents at the age of 27. Among these, the “All-on-4®” permanent dental implant technique and the patented “Malo Clinic Bridge” fixed denture bridge have made significant contributions to the treatment and rehabilitation of patients with missing teeth or nearly edentulous jaws. Through these achievements, Dr. Malo has become a globally renowned master in dental implantology and prosthodontics.

From a business perspective, under the leadership of Dr. Malo, Malo Clinic has experienced thriving growth and expanded globally. By 2010, Malo Clinic had established 44 branches in 28 countries, involving more than 100 partner clinics.

The year was 2013,Facing China's vast market, Shao Zongzong, sensing the opportunity, joined hands with Dr. Malo to officially introduce Malo Clinic to China, jointly founded Malo Clinic (China), marking the beginning of Malo Clinic’s commercial journey in China.

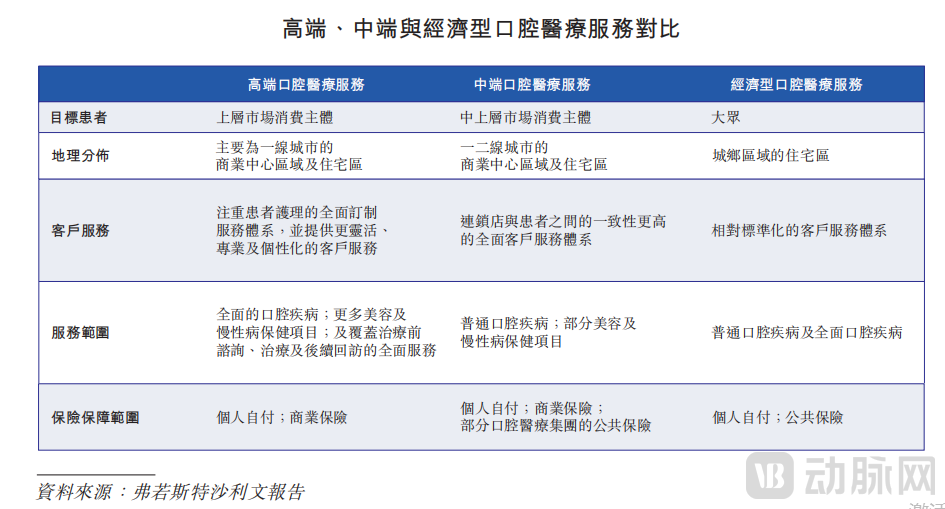

In terms of positioning, Malo Dental has chosen the high-end market.

What Constitutes High-End Dental Medical Services? According to the prospectus, compared with economy and mid-range dental medical services, high-end dental medical services place greater emphasis on comprehensive customization of patient care and provide more flexible, professional, and personalized customer service.

(Image source: Prospectus)

(Image source: Prospectus)

Focusing on high-end medical services not only helps Malo Dental establish a differentiated competitive edge in a fiercely contested market, but also enhances patient reputation.

Of course, the rapid growth of the high-end dental care services market is also a significant factor. According to Frost & Sullivan data, China’s high-end private dental care services market, measured by revenue, grew from RMB 2.7 billion in 2018 to RMB 2.9 billion in 2022, representing a compound annual growth rate (CAGR) of 1.6%. It is projected to reach RMB 5.9 billion by 2027, with a CAGR of 15.6% from 2022 to 2027.

Given that the high-end dental care market demands prime locations, top-tier dentists, and premium services—making resources particularly scarce—Malong Dental has consistently emphasized that it will not pursue blind expansion.

The data offers a glimpse into the “slow pace” of Malo Clinic. As of April 30, 2023, after ten years in China, Malo Clinic had established only 29 dental clinics across 13 Chinese cities. In contrast, within the broader industry, there are now no fewer than ten chain operators each with more than 30 clinics nationwide.

It is precisely because of its moderate expansion pace that Malo Dental has been able toExert More Precise Control Over the Single-Store ModelThe prospectus specifically noted that, during the track record period, newly opened clinics of Malo Dental became operational within a short span of four months, and such clinics were able to achieve monthly break-even within the subsequent 6 to 12 months. According to a report by Frost & Sullivan, the time required for Malo Dental’s new clinics to reach monthly break-even from the commencement of operations was approximately half of the industry standard (i.e., 12 to 24 months).

In terms of operational efficiency, Malo Dental is also at the forefront of the industry. Citing data from Frost & Sullivan, in 2022, Malo Dental ranked among the top three of the top ten industry participants in terms of both average revenue per dental chair and average revenue per dentist.

Specifically, from 2020 to the first four months of 2023, the average revenue per dental chair at Malo Dental was RMB 1.4 million, RMB 1.4 million, RMB 1.5 million, and RMB 500,000, respectively.

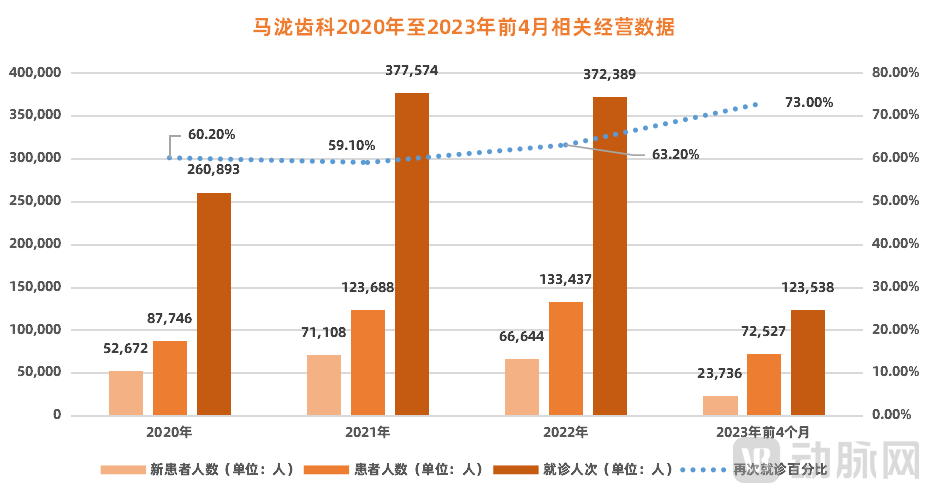

Due to its long-term focus on the high-end dental healthcare services market, Malo Clinic'sHigh user stickiness. Since 2020, Malo Clinic has demonstrated impressive customer retention data, with the repeat visit rate climbing from 60.2% in 2020 to 73% in the first four months of 2023. Malo Clinic stated that overall customer satisfaction with its services has exceeded 99.9% since 2020, while the patient complaint rate stands at merely 0.1%.

(Data source: Prospectus) (Chart by VCBeat)

(Data source: Prospectus) (Chart by VCBeat)

It is precisely by steadily consolidating its position in the high-end market that Malo Dental has gained the confidence to pursue an initial public offering (IPO).

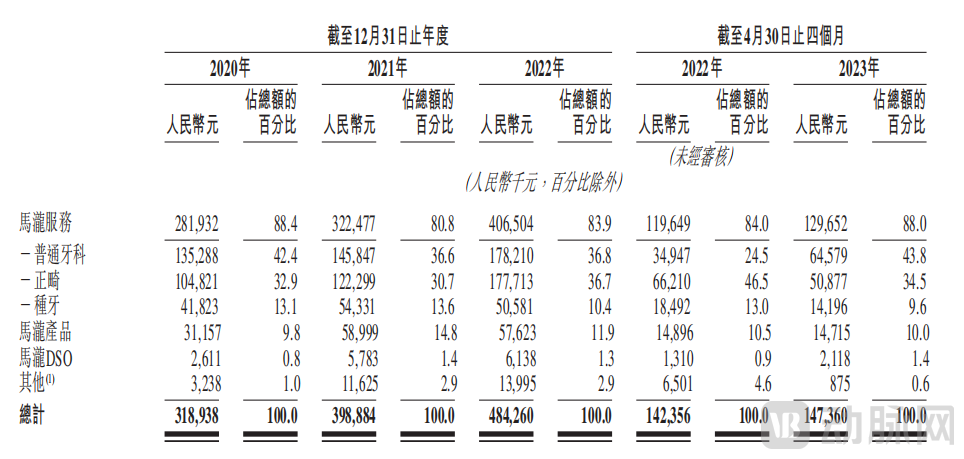

On the other hand, as its business continued to improve, Malo Dental began diversifying its operations in 2015. Building on the traditional “three pillars” of dental services—general dentistry, orthodontics, and dental implants—the company ventured into selling dental-related products, providing operational support to third-party dental clinics, and launching its own brand of oral care products.Currently, three major business segments have been established: Malo Services, Malo Products, and Malo DSO.

However, apart from Malo’s services, the scale of its two other major business segments—Malo Products and Malo DSO—remains relatively small, with their growth potential yet to be observed.

(Revenue from Three Major Business Segments; Source: Prospectus)

(Revenue from Three Major Business Segments; Source: Prospectus)

Looking ahead, Malo Clinic stated in its prospectus that it plans to establish 30 dental clinics in China over the next four years. Of these, 19 will be located in first-tier cities, while the remaining 11 will be situated in second-tier cities. Additionally, Malo Clinic intends to open eight dental clinics in several major overseas metropolitan areas during the same period.

As previously mentioned, whether in terms of IPO frequency or the pace of primary market financing, the dental industry has consistently remained a premium sector highly sought after by investment institutions.

Why? There are three reasons.

· First, as China’s population ages, the demand for oral health is gradually increasing;

· Second, the oral care sector exhibits strong “consumer-driven characteristics,” with users demonstrating increased willingness and frequency to consume oral health services;

· Third, the continuous emergence of new technologies and equipment, such as intraoral scanning, CBCT, clear aligner orthodontics, and dental implants, is driving a supply-side transformation in the dental industry.

Driven by the combined forces of supply and demand, the dental healthcare services market is expanding rapidly.According to the "2023 Dental Medical Services Insight Report" released by VCBeat, the overall market size of dental medical services in China was RMB 145 billion in 2021, maintaining an average annual growth rate of 20%. It is expected to reach RMB 300 billion by 2025, indicating broad prospects.

Consequently, a surge of capital flooded into the market, driving a rapid heating up of the dental industry. From 2014 to 2019, more than 30 institutions in the dental care service sector alone secured financing. However, following the sudden outbreak of the COVID-19 pandemic in 2020, dental service providers faced significant challenges, with revenues and profits declining sharply.

In retrospect, the COVID-19 pandemic was not the root cause, but merely a catalyst.This, in essence, exposes the numerous challenges faced by dental service providers in achieving profitability.

Last year, VCBeat conducted a survey of 1,000 dental institutions and found that, under compliant conditions,The net profit margin of most oral healthcare service providers is approximately 15% or lower, with some even reporting negative figures.. For instance, ARRAI, which went public last year, and Malo Dental, which is now racing toward an IPO.

The core reason lies in the fact that dental service providers, during their chain expansion, face multifaceted challenges in talent acquisition, marketing, management, and technology. These issues have diluted profit margins, preventing the economies of scale intended by chain expansion from being effectively realized.

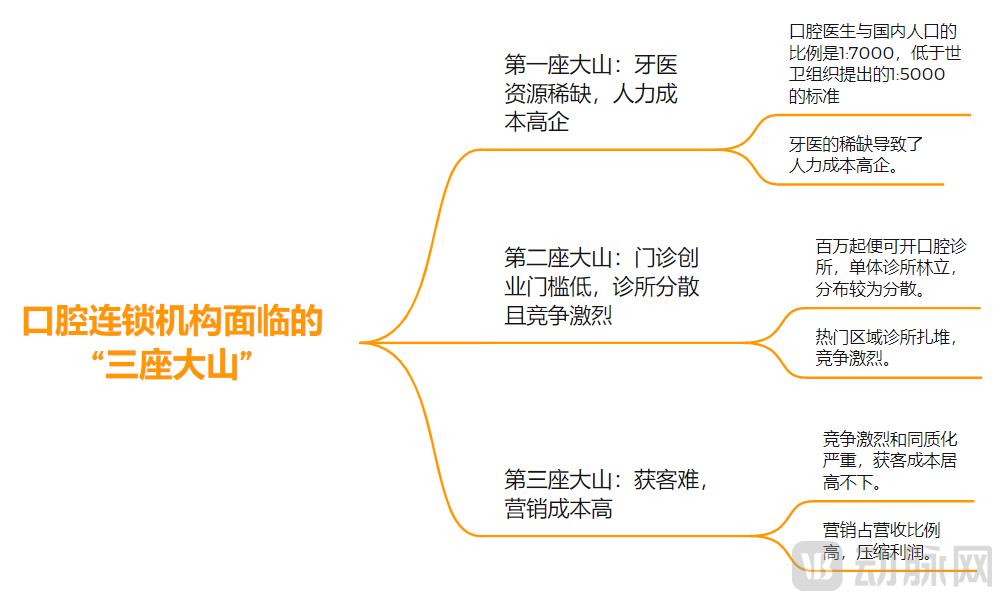

Amidst a myriad of complex issues, the most prominent challenges are the “Three Big Mountains.”

"The First Major Hurdle" Is the Scarcity of Dental Resources, which keeps labor costs persistently high. According to the Health Statistics Yearbook, China currently has more than 200,000 dentists, resulting in a dentist-to-population ratio of 1:7,000.

The World Health Organization proposes that this ratio should reach at least 1:5,000, while in some developed countries, it stands between 1:2,000 and 1:3,000. The scarcity of dentists in China has naturally driven up labor costs.

“The Second Mountain” Is the Low Barrier to Entry for Starting an Outpatient Dental Clinic, resulting in a fragmented clinic landscape and intense competition. Previously, multiple industry insiders revealed that the startup cost for a dental clinic generally starts at one million yuan, which has prompted many dentists to establish their own practices, leading to a proliferation of independent clinics in the market.

Moreover, in some high-demand areas, the number of dental clinics has grown faster than the population they can serve and the number of available dentists, resulting in intense competition.

"The Third Mountain" is the difficulty in customer acquisition and high marketing costs.Driven by the “second major hurdle,” the dental services industry is characterized by a fragmented competitive landscape dominated by small, dispersed providers. Coupled with severe service homogenization, this has made customer acquisition a significant challenge.

In response to this situation, dental outpatient clinics are adopting higher-frequency marketing strategies to acquire customers, which has increased their marketing costs.

(The “Three Big Mountains” Facing Dental Chain Clinics; Graphic by VCBeat)

(The “Three Big Mountains” Facing Dental Chain Clinics; Graphic by VCBeat)

Given these factors, the expansion path for dental chain operators has been quite arduous. Taking Malo Dental, which is currently pursuing an IPO, as an example, its cost of sales (including employee costs and costs of raw materials and consumables) has accounted for more than 70% of the company’s total revenue since 2020. When marketing expenses, administrative expenses, and other expenditures are factored in, the result is a net loss reported in Malo Dental’s financial statements.

How to achieve a breakthrough in profitability has become a critical battle for every dental chain institution.

In choosing a path to break through, the industry is attempting to provide solutions.

First, accelerate the digitalization process to support institutional scalability.For example, without digital enablement, dentists can only manually record medical records, making remote access impossible. Additionally, the inability to share data across platforms among various functional departments hinders the development of comprehensive system solutions. Furthermore, the expanded management scope of enterprises leads to untimely statistical reporting. In other words, as scale increases, so do management costs.

From this perspective, leading companies in the industry are accelerating their digital transformation. For instance, ARRAI officially launched its FRIDAY Digital and Intelligent Dental Healthcare Platform this year, while MEI WEI DENTAL GROUP has been building its “Wei Xiaomei Medical Cloud Intelligence Platform” since its inception.

Similarly, Malo Dental, which is currently sprinting toward an IPO, specifically mentioned in its prospectus that it will upgrade its digital management system to enhance overall operational efficiency. This includes clinical digitalization (such as purchasing advanced dental equipment like digital dental implant robots) and managerial digitalization (covering data transmission, as well as the storage and management of patients’ imaging data).

With the advancement of digitalization, chain institutions are theoretically poised to possess stronger replication and synergy capabilities, thereby enhancing their appeal to capital. After all, this implies that a newly opened chain store, empowered by the group’s headquarters, can attract customer traffic and even achieve profitability in a shorter time frame and at a lower cost.

From this perspective, digitalization is not merely a tool but a validated manifestation of the group’s business processes.

Furthermore, the DSO model is becoming an industry consensus.Currently, an increasing number of dental institutions are adopting the DSO model and pursuing localized and differentiated development.

What Is a DSO?DSO stands for Dental Service Organization. It provides dentists and dental clinics with support in non-clinical areas such as management, operations, finance, legal affairs, and training. This enables dentists to devote more energy to enhancing their clinical skills and treating patients, essentially empowering dental practitioners.

In recent years, including MEI WEI DENTAL GROUP, Beijing Enjoy Oral Outpatient Department Co., Ltd., ARRAI, and Malo Clinic, which is currently rushing towards an IPO, have been rapidly developing their DSO (Dental Service Organization) strategies. Taking Malo Clinic as an example, its prospectus shows that its DSO plan mainly provides operational support for third-party dental clinics, involving medical support, marketing guidance, and customer management.

Thanks to the DSO program, Malo Dental has further enhanced its brand visibility within the industry, gained a deeper understanding of China’s dental healthcare services market, and thoroughly assessed the operational performance of DSO-affiliated clinics, which may become potential targets for strategic investment or acquisition by Malo Dental.

As of December 31, 2020, 2021, and 2022, and April 30, 2023, Malo Dental had 31, 46, 38, and 50 DSO-affiliated clinics, respectively.

Next, for enterprises adopting the DSO model, the key to gaining a first-mover advantage lies in how effectively they can deeply integrate this model with China’s national conditions and local realities.

Finally, whether observed from international experience or considering the changes brought by digitalization and the DSO model to the oral healthcare services market,Large chain groups will become an irreversible trend, and the concentration of the dental industry will continue to rise.

In the current market, the vast majority of dental clinics are either single-location practices or small chains with two to five locations. These enterprises exhibit weak operational consolidation, poor financing capabilities, and low risk resilience, leaving them completely vulnerable when confronted with sudden crises such as the COVID-19 pandemic.

For large chain groups, their strong advantages in financing capabilities and brand output enable them to raise funds through equity financing, debt financing, and internal capital allocation within the group when facing special circumstances. This results in superior risk resistance and resource synergy capabilities. Therefore, large chain groups are bound to grow.

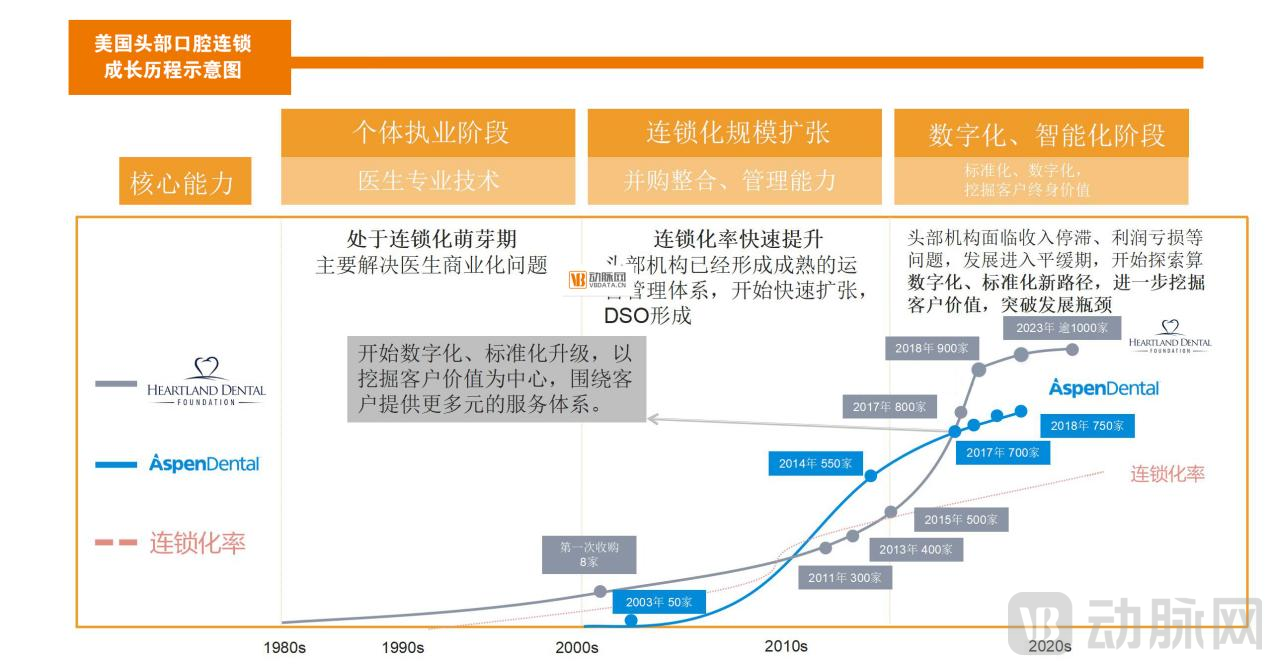

Taking the more mature U.S. dental services market as an example, large chain groups have now come of age, with a “the strong get stronger” dynamic emerging. Leading chains such as Aspen Dental and Heartland Dental have further expanded their scale in recent years, reaching hundreds or even over one thousand clinics by March 2023.

(Illustration of the “Three Big Mountains” Facing Dental Chain Clinics; Graphic by VCBeat)

(Illustration of the “Three Big Mountains” Facing Dental Chain Clinics; Graphic by VCBeat)

Returning to the domestic market,Standing at the midpoint of 2023, the dental chain industry has maintained a rapid pace of financing. Service providers such as MEI WEI DENTAL GROUP, Eya Group, and Meiao Dental have all secured funding this year. Coupled with Malo Clinic’s push for an initial public offering, signals are emerging that the consolidation and chain-based expansion of the dental services sector is accelerating.In the next 5–10 years, there is a high probability that China will see the emergence of super dental groups operating more than 500, or even over 1,000, clinics.

Of course, in the process of rapid scaling, issues such as profitability, level of informatization, and control of medical service quality are inevitable. Among these, the quality of medical services is always the key and fundamental factor.

Therefore, looking to the future, dental chain institutions must innovate, iterate, and grow sustainably while upholding the fundamental value of medical care, thereby crafting more compelling business narratives for the industry.