Biotech's Midlife Crisis: Abcam Agrees to $5.7B Acquisition by Danaher Amid Governance Struggles

“M&A King” Danaher Strikes Again: On August 28, Danaher Corporation announced an agreement to acquire all outstanding shares of Abcam, a global leading supplier of protein consumables, for $24 per share in cash, with the total transaction value reaching up to $5.7 billion.

Abcam is one of the world’s most renowned antibody suppliers, with its online catalog currently listing over 120,000 antibodies and reagents. Abcam is expected to operate as an independent operating company and brand within Danaher’s Life Sciences segment, further advancing Danaher’s strategy to help map complex diseases and accelerate the drug discovery process.

With this, Abcam’s internal strife has come to an end. Founder Dr. Jonathan Milner and the company’s board of directors had disagreements over corporate management, leading both sides to issue multiple public statements in a heated exchange over several months. Established 25 years ago, this “middle-aged” biotech company provides antibodies, reagents, biomarkers, and assay methods to researchers worldwide and holds a leading rabbit monoclonal antibody technology platform. However, prior to its acquisition, it did not enjoy the comfortable position of a “shovel seller”: the company reported a loss of £8.5 million in 2022 and a profit of only £4.4 million in 2021.

Selling to Danaher may be the best possible outcome for Abcam—and it also represents the ultimate fate of many biotech companies.

Grew by acquiring a rabbit monoclonal antibody platform

Abcam, known as the “Amazon of antibodies,” counts China as its third-largest market, yet it has long-standing ties with Chinese scientists.

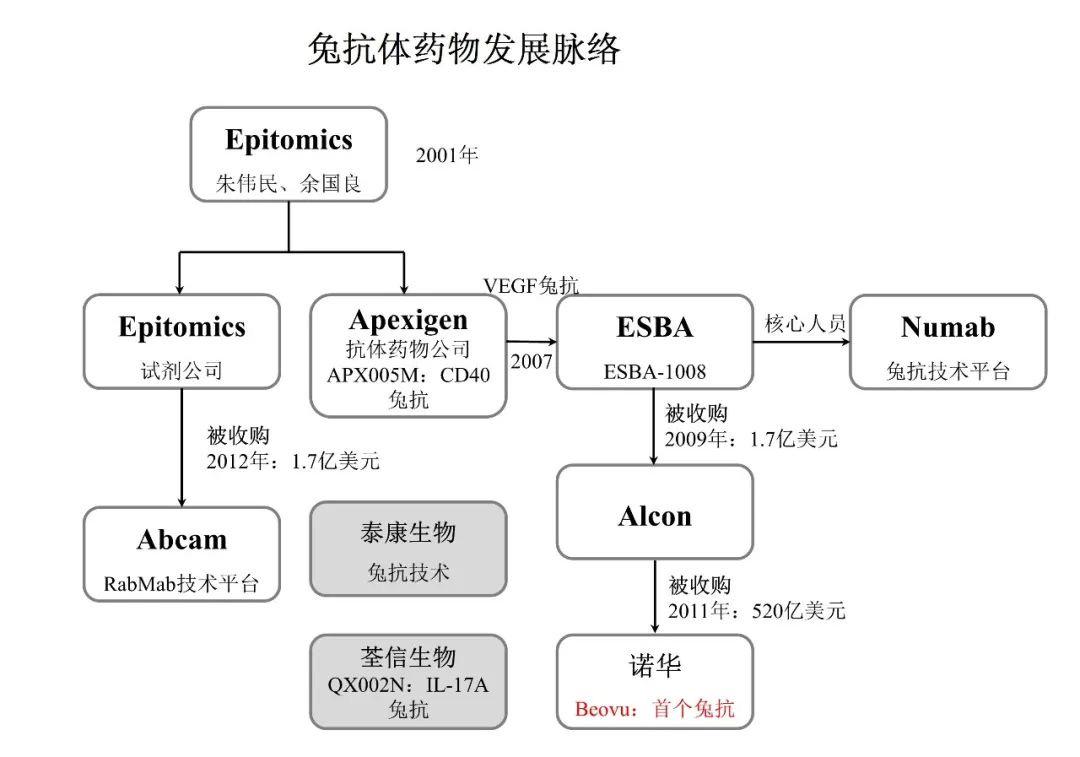

Among Abcam’s technologies, the most noteworthy is its RabMab® rabbit monoclonal antibody platform. In 2012, Abcam acquired Epitomics for $170 million, thereby obtaining the world’s first RabMab® rabbit monoclonal antibody platform.

Epitomics was founded in 2001 by Dr. Guoliang Yu and Dr. Weimin Zhu, renowned Chinese-American scientists and entrepreneurs. The company successfully developed a series of groundbreaking global patents that addressed challenges such as the stability of rabbit hybridoma cells. Rabbit monoclonal antibodies are characterized by high affinity, high specificity, high sensitivity, and great diversity, enabling the generation of antibodies that are difficult to produce in mice. As the originator of rabbit antibody therapeutics, Epitomics spun off Apexigen, whose VEGF-targeting rabbit monoclonal antibody, through licensing, optimization, and acquisition, became BEOVU®, the first FDA-approved rabbit-derived scFv monoclonal antibody drug. In China, Epitomics’ technology has been adopted by Quanxin Biologics, a company focused on the research and development of autoimmune disease therapeutics.

Early Development Trajectory of Rabbit Antidrug-Related Companies (Source: Biopharmaceuticals Editor)

Therefore, the acquisition of Epitomics represented a significant step for Abcam in expanding its antibody portfolio. In retrospect, it proved to be a highly cost-effective deal. The RabMab® rabbit monoclonal antibody platform has contributed more than 18,000 antibodies to Abcam’s offerings, including over 360 rabbit monoclonal antibody clones specifically optimized for immunohistochemistry (IHC) applications.

The RabMab® rabbit monoclonal antibody platform is a key growth engine for Abcam. In the year following its acquisition of Epitomics, Abcam announced a 19.4% increase in profit, attributing this growth to the acquisition.

After more than a decade of development and operation, the RabMab® rabbit monoclonal antibody platform has become synonymous with rabbit monoclonal antibodies in the era of life sciences and biotechnology. Abcam collaborates with thousands of companies and universities to provide custom rabbit monoclonal antibody services.

Despite the immense potential of rabbit monoclonal antibody drugs and the high regard for Abcam’s services, a leading technological platform alone cannot fully resolve this biotech company’s development challenges.

Biotech’s Midlife Crisis: Poor Governance and the Absence of Successors

Dr. Jonathan Milner, 58, founded Abcam in 1998, successfully took the company public in 2005, and served as CEO until 2014. He subsequently became Deputy Chairman, with Alan Hirzel assuming the role of CEO. In October 2020, Dr. Milner resigned from the board of directors.

After departing from the Milner postdoctoral fellowship, CEO Alan Hirzel’s management performance was far from impressive, and the company’s stock price declined steadily throughout 2022.

In May this year, Dr. Milner published an open letter criticizing Abcam’s board of directors, stating bluntly, “Since my resignation, the company has lost its focus and its performance has clearly deteriorated.” In the letter, he detailed the reasons behind Abcam’s poor performance, each of which represents a challenging issue that mid-stage biotech companies commonly face and struggle to resolve.

First, poor corporate governance.The open letter states that Abcam’s Board of Directors lacks a shareholder-oriented mindset, with the combined shareholding of management and the board totaling less than 1%. Shareholder concerns have been ignored, and investor relations have been poorly managed. Although Abcam’s business is not complex, its performance metrics have been frequently changed, and the company has failed to ensure transparency. Notably, Abcam does not even issue quarterly reports.

Secondly, there is insufficient execution capability.The company’s ERP system, which was scheduled to go live in 2017, remains incomplete to date, resulting in losses in revenue, customers, and market share. In addition to the ERP system, poor execution in operations and integration has led to a deterioration in operating margins, with the operating margin in fiscal year 2022 declining by approximately 50% compared to fiscal year 2019.

Finally, cost management.Dr. Milner stated that Abcam’s current operating costs far exceed the level of revenue growth, with its return on capital employed (ROCE) falling from around 20% under his leadership to below 9%. Meanwhile, executive compensation remains high; after Dr. Milner’s departure, Sally Crawford, Chair of the Remuneration Committee, approved a 216% pay increase for the CEO.

Based on this, Dr. Milner has called for regaining control of the company, asserting that his expertise and shareholding make him the only person capable of “swiftly turning things around, restoring shareholder trust and value, and making Abcam the ‘Amazon of antibodies’ once again.”

Finding a suitable successor manager for a company is no easy task. Although Abcam is already an established biotech firm, and CEO Alan Hirzel had years of collaborative experience with Dr. Milner before shouldering the leadership burden alone, its growth to the present stageTo a large extent, Dr. Milner’s will was infused into the company; when this pivotal figure stepped away, Abcam lost its soul.

Since May, Dr. Milner has repeatedly engaged in public exchanges with Abcam’s Board of Directors. Dr. Milner pointed out that Abcam’s current management shows no interest in exploring any strategic alternatives, and he even detailed the board members’ dereliction of duty in an open letter. Although Abcam offered Dr. Milner a board seat with limited rights, he decisively rejected the offer and, in his open letter, unreservedly exposed Abcam management’s stalling tactics.

Two months ago, Abcam had no choice but to announce that it was considering exploring strategic options, including the sale of the company.

Abcam stated that, prior to reaching a deal with Danaher, the company had engaged with 30 other potential counterparties, including “more than 20 potential strategic acquirers.”

With investors deeply dissatisfied and management taking no action, Abcam’s acquisition by Danaher may well be the best outcome Dr. Milner could achieve.

Some Biotech Companies Have Reached a Crossroads of Strategic Choices

Regarding Abcam’s development in recent years, analysts at Royal Bank of Canada wrote in a report: “In the past few years, many life sciences tools companies have benefited from industry growth and increased demand, but Abcam has not shared in these gains. The upside, however, is that the company has currently avoided the pressure of downstream customers reducing their inventories.”

Biotech firms with limited scale are inevitably constrained by the decision-making and governance capabilities of their management teams, and they also face heightened exposure to market volatility due to their reliance on a single business model.

Compared to Abcam, the buyer Danaher is an absolute commercial empire in the life sciences field.Its comprehensive upstream, midstream, and downstream industrial chain will open up new opportunities for Abcam:For instance, upstream integration of in-house production equipment and consumables can reduce Abcam’s manufacturing costs; midstream commercial leads from other brands within the Life Science segment, such as IDT and SCIEX, can be leveraged synergistically; downstream, Abcam’s extensive antibody library can be aligned with its diagnostic product portfolio to boost Abcam’s revenue while simultaneously lowering costs for the diagnostic line.

The operational issues that have drawn criticism against Abcam are likely to be resolved through Danaher’s mature management practices following its acquisition.Danaher Business System (DBS) is a comprehensive standard methodology covering all aspects of corporate management. Acquired companies that adopt the DBS system are often able to execute production, sales, and customer service more efficiently, thereby achieving revenue growth.

The biotechnology industry is undergoing a wave of market consolidation, with large companies seeking acquisition targets and leveraging economies of scale to reduce costs, while biotech firms have reached a crossroads requiring strategic, even fate-defining, decisions.

In China, the tightening of IPO regulations for biopharmaceutical companies has made public listings less attractive to many Biotech founders. Under mature conditions, selling to larger corporations has become a pragmatic choice. Furthermore, as secondary market prices gradually rationalize and mature, the M&A-driven elimination mechanism can also enhance market liquidity.

Dr. Milner is expected to discuss the acquisition plan with shareholders next week. Additionally, Danaher’s acquisition transaction still requires approval from the U.S. Federal Trade Commission, China’s State Administration for Market Regulation, and the antitrust regulators in Germany and Austria. Analysts at JPMorgan Chase pointed out that the figure of “$5.7 billion” is “reasonable” for a company like Abcam. Furthermore, “given the lack of product overlap between the two companies, little ‘regulatory resistance’ is anticipated.”

Regardless of how the details unfold thereafter, Abcam’s story suggests that M&A may be the ultimate destination for many biotech companies in the near future.

References

1. https://www.businessweekly.co.uk/news/biomedtech/milner-slams-abcam-%E2%80%9Cunderperformance%E2%80%9D-and-%E2%80%9Cvalue-destruction%E2%80%9D-and-calls-egm-take

2. https://mp.weixin.qq.com/s/dni06NseTvgJ09iOtOl8dQ