China's Biomanufacturing M&A Value Soars to RMB 36.04 Billion in 2024 with Four Deals Exceeding RMB 5 Billion Each | '2024 China Biomanufacturing Industry Development Report' Released

Recently, Rayshou Analysis, the data analytics platform for investment value of innovative and tech enterprises under Cyzone, released the “2024 China Bio-Manufacturing Industry Development Report], the core viewpoints of the report are as follows:

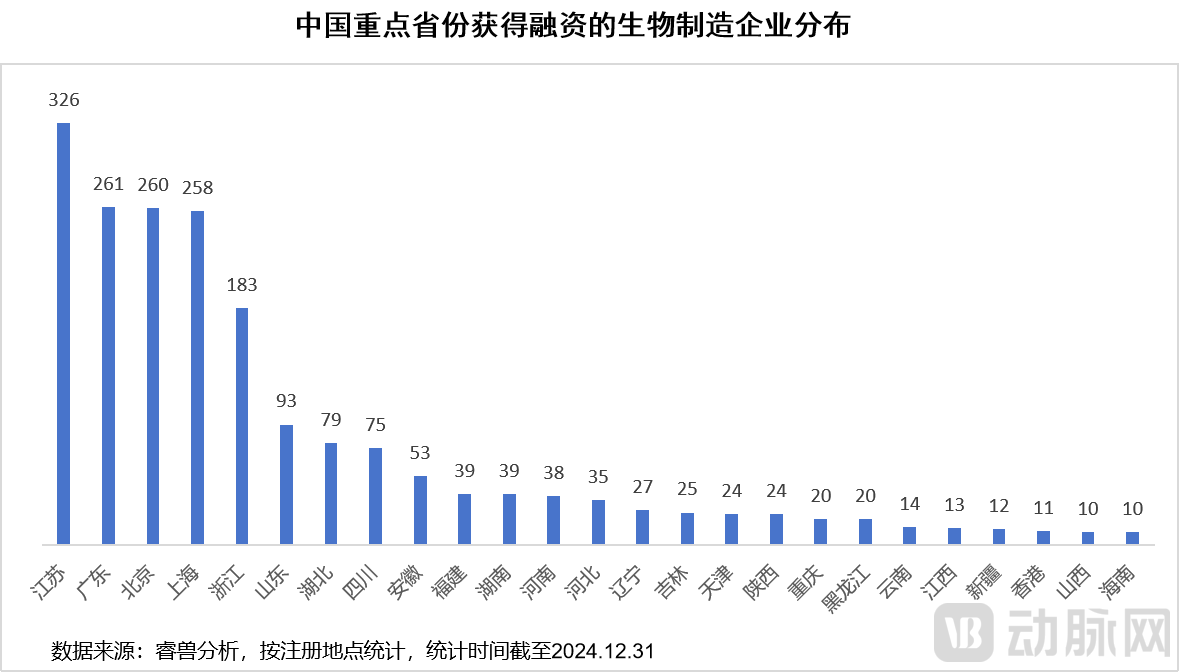

The Yangtze River Delta, the Beijing-Tianjin-Hebei region, and the Greater Bay Area account for nearly 70% of China's financing share.China has initially formed a biomanufacturing industrial landscape dominated by three major city clusters, with the central and northern regions serving as supplementary hubs. The Yangtze River Delta, Beijing-Tianjin-Hebei region, and Greater Bay Area boast abundant innovation resources and have established a new economic development model for biomanufacturing through regional collaboration, covering “R&D – commercialization – industrialization.” Companies in these regions that secured financing account for 68% of the national total. Relying on advantages in raw materials, labor, and market access, the central region focuses on deploying specialized industrial projects in pharmaceuticals, food, and other sectors, with its financed companies representing 17% of the national total. Leveraging advantages in climate, energy, and raw materials, along with a strong foundation in fermentation industries, the Northeast and Northwest regions prioritize the deployment of large-scale industrial projects.

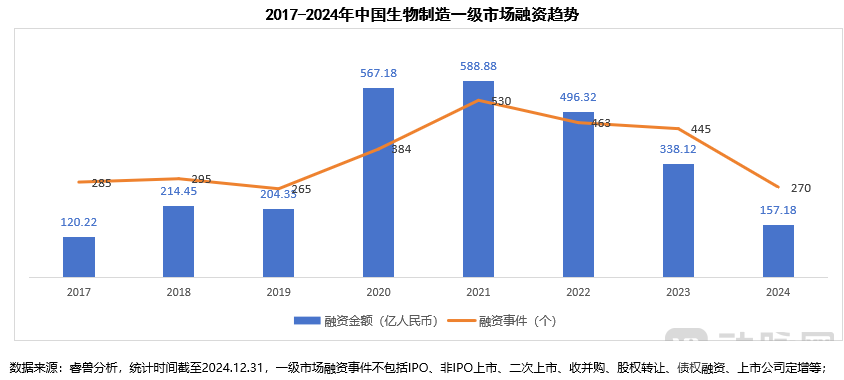

The number of financing and investment events in 2024 decreased by 40%-50%.Since 2022, primary market financing in the biomanufacturing sector has shown a year-on-year decline. Amid the “capital winter,” investment has become more rational. In 2024, there were 270 completed financing deals (a 39.3% year-on-year decrease), with disclosed financing amounts totaling RMB 15.718 billion (a 53.5% year-on-year decrease).

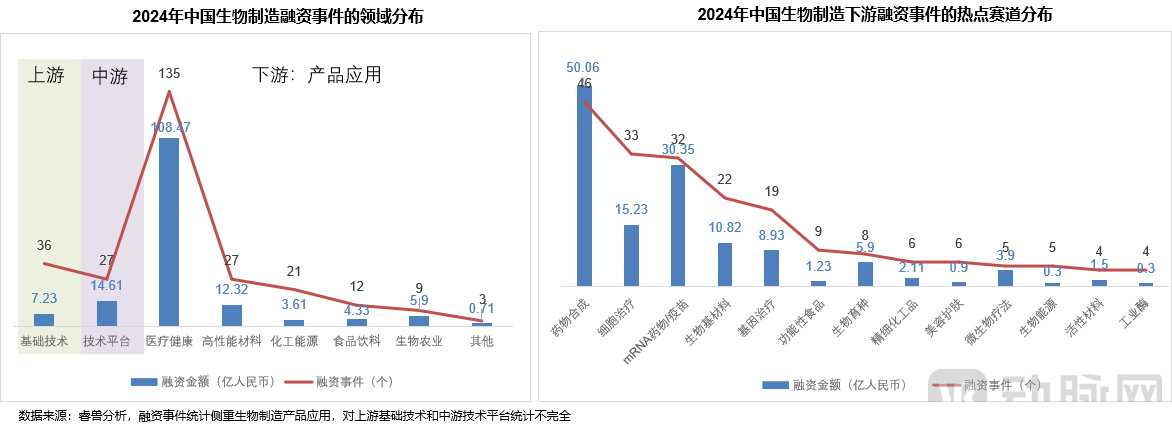

Financing events in the healthcare and medical sector accounted for 50%.In 2024, the healthcare sector recorded 135 financing deals, the highest number among all industries. Within specific sub-sectors, drug synthesis, mRNA drugs/vaccines, cell therapy, and bio-based materials attracted significant investment interest, each completing more than 20 financing deals with a total financing amount exceeding RMB 1 billion.

The M&A market is relatively active, with a significant number of large-ticket transactions.Since 2021, the M&A market has remained relatively active. In 2024, there were 25 M&A transactions, with a total disclosed amount of RMB 36.04 billion (a fourfold year-on-year increase), including four deals exceeding RMB 5 billion. International giants, listed companies, and industrial groups are seeking new growth curves in biomanufacturing, while state-owned capital investment is taking the lead, which will accelerate industrial investment, M&A, and consolidation.

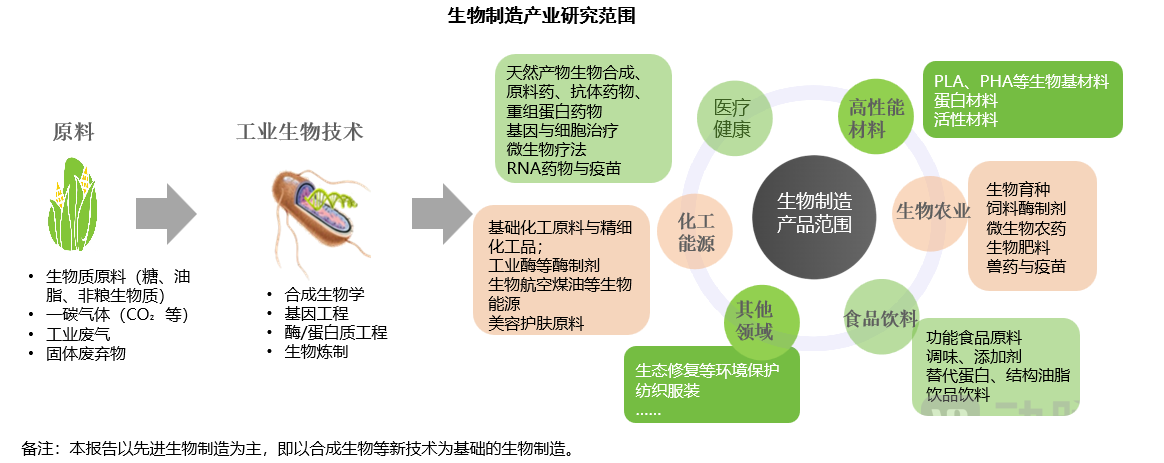

Industry Development and Market Landscape

Biomanufacturing: Fueling Industrial Upgrades and Poised to Reshape the Global Industrial Landscape

Bio-manufacturing is an advanced industrial model that transforms material production by changing raw materials and innovating manufacturing processes, thereby driving economic growth and improving public health, agricultural efficiency, and security. It is poised to become the fourth industrial wave, following the agricultural, industrial, and digital economies, and is expected to reshape the global industrial landscape.

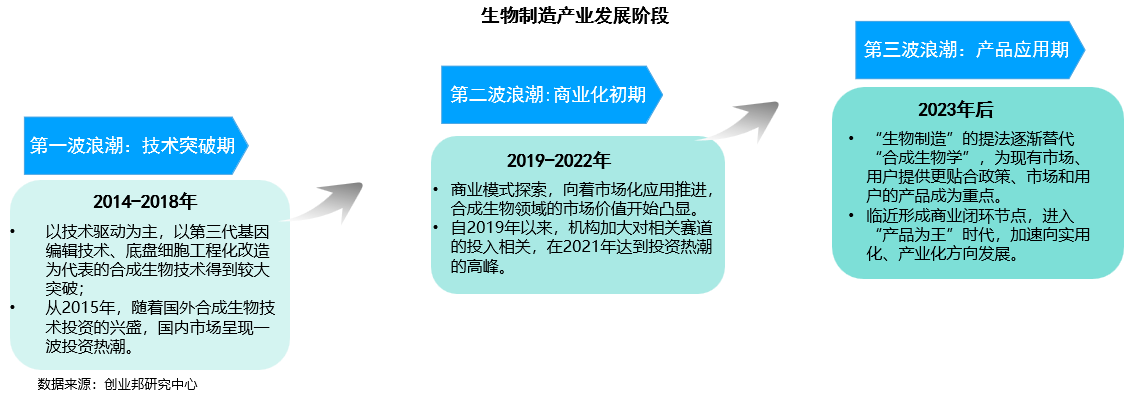

Biomanufacturing Enterprises Enter the Product Application Phase, with Large-Scale Production Becoming the Core of CompetitionStrength

As support from national and local governments intensifies and capital markets pour significant investment into synthetic biology enterprises, China’s biomanufacturing companies are approaching a critical juncture in forming a closed commercial loop, transitioning from technological breakthroughs to practical applications.

China has preliminarilyForming a structure dominated by the Yangtze River Delta, Beijing-Tianjin-Hebei region, and Greater Bay AreaIndustrial Layout

The development of the biomanufacturing industry relies on talent and raw material resources, bolstered by the overall scientific research strength of cities. Currently, a pattern has formed with the Yangtze River Delta, Beijing-Tianjin-Hebei region, and the Greater Bay Area as the leading hubs; central regions represented by Shandong, Shanxi, Anhui, and Henan serving as the backbone; followed by distributions in the southwest region represented by Sichuan and Chongqing, the three northeastern provinces represented by Heilongjiang, and the northwest region represented by Xinjiang and Inner Mongolia.

Key investment hotspots include Jiangsu, Beijing, Guangdong, and Shanghai, followed by Zhejiang, Shandong, Hubei, Sichuan, and Anhui. The biomanufacturing industry in the Yangtze River Delta urban agglomeration exhibits a pronounced clustering effect, with high levels of investment and financing activity; companies in this region accounted for 38% of the national total in terms of financing recipients.

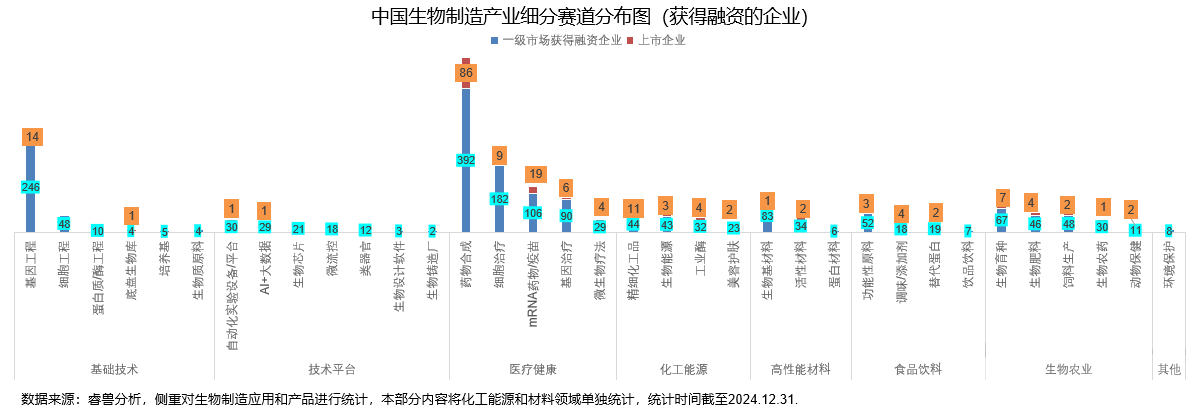

EnterpriseFocusing on the fields of healthcare, chemical energy and bio-based materials, and bio-agriculture

According to incomplete statistics from VBInsight, as of the end of December 2024, there were 1,994 registered biomanufacturing companies that had secured public financing (with a focus on the application layer), among which 1,805 companies received financing in the primary market and 189 were listed companies.

Enterprises that secured financing in the primary market were concentrated in the following sectors: drug synthesis (392 companies), genetic engineering (246 companies), cell therapy (182 companies), mRNA drugs/vaccines (106 companies), gene therapy (90 companies), bio-based materials (83 companies), and biological breeding (67 companies).

Listed companies are primarily distributed across the following sectors: drug synthesis (86 companies), mRNA drugs/vaccines (19 companies), genetic engineering (14 companies), fine chemicals (11 companies), and cell therapy (9 companies).

Venture Capital Market

Secondary Market: IPO Process Hindered, Significant Drop in Number of Listed Companies

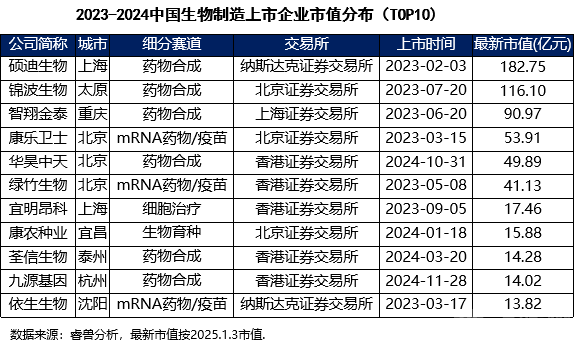

Since 2021, the global and A-share IPO markets have generally slowed down, with the number of biomanufacturing IPOs declining year by year. In 2023, nine companies went public (a year-on-year decrease of 59%), and in 2024, five companies completed their IPOs (a year-on-year decrease of 44%). Only Shuodi Biotech and Jinbo Biotech achieved market capitalizations exceeding RMB 10 billion.

M&A market remains relatively active, with a high volume of large-ticket transactions

Since 2021, the M&A market has remained relatively active. In 2023, there were 36 biomanufacturing M&A transactions, with a total disclosed amount of RMB 7.244 billion. In 2024, the number of M&A transactions reached 25, with a total disclosed amount of RMB 36.04 billion. Among these, Shanghai RAAS, Gracell Biotechnologies, Promab Biotechnologies, and Henlius each participated in M&A deals exceeding RMB 5 billion. The target companies were primarily concentrated in drug synthesis (10 deals) and genetic engineering (3 deals).

Primary Market: Financing events have declined year by year in recent years, with early-stage financing dominating.

According to data from VCBeat Analysis, financing events in the biomanufacturing sector grew steadily from 2017 to 2021, peaking in 2021 with 530 deals totaling RMB 58.888 billion. From 2022 to 2024, a year-on-year decline was observed, as investment became more rational amid the “capital winter.” In 2023, the disclosed financing amount reached RMB 33.812 billion, a 31.9% decrease year on year. In 2024, there were 270 completed financing deals, a 39.3% drop year on year, with the disclosed financing amount falling to RMB 15.718 billion, a 53.5% decline year on year.

Since 2024, financing events have been predominantly in the early stages. There were 187 early-stage (Series A and prior) financing events, accounting for 69% of the total. Among these, Series A rounds numbered 136, making it the most frequent round for investment and financing. There were 72 growth-stage (Series B–C) financing events and 11 late-stage (Series D–Pre-IPO) financing events.

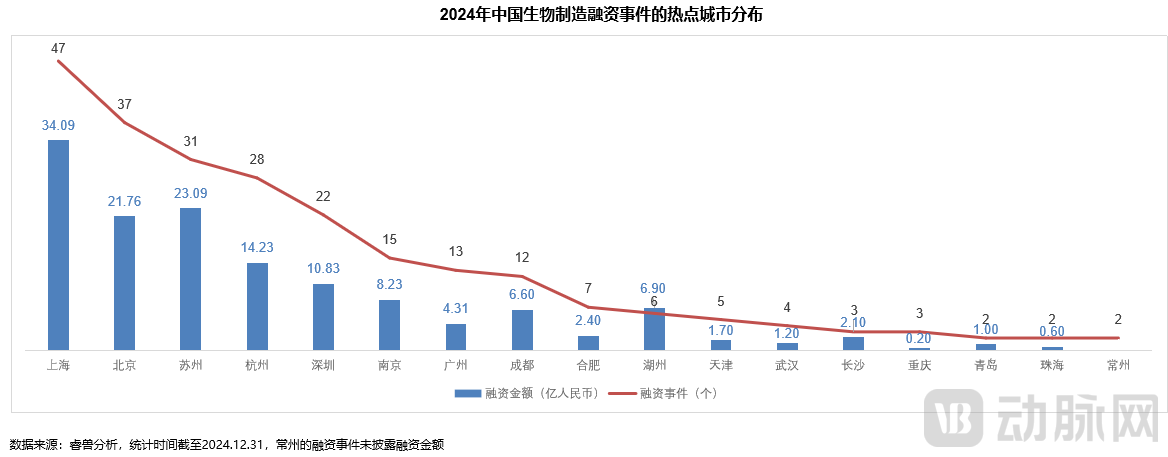

Hotspot Cities: Shanghai, Beijing, Suzhou, and Hangzhou Exhibit High Investment and Financing Activity

In 2024, Shanghai led all cities with 47 financing deals and a total funding amount of RMB 3.409 billion. Beijing and Suzhou each recorded more than 30 financing deals, with total funding exceeding RMB 2 billion; Hangzhou and Shenzhen each had over 20 financing deals, with total funding surpassing RMB 1 billion.

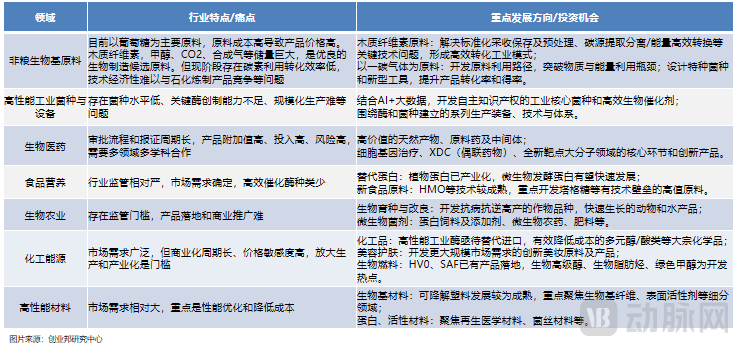

Hot Tracks: Focused on Drug Synthesis, mRNA Drugs/Vaccines, Cell Therapy, and Bio-based Materials

In 2024, the healthcare, high-performance materials, and chemical energy sectors within the product application layer witnessed a high volume of financing events. In terms of specific sub-sectors, drug synthesis, cell therapy, mRNA drugs/vaccines, and bio-based materials attracted significant investment interest, each recording more than 20 financing deals with total amounts exceeding RMB 1 billion.

Investment Firms: Shunxi Fund and Qiming Venture Partners Are the Most Active

In 2024, 410 investment institutions participated in financing deals within the biomanufacturing sector. Among them, 374 were VC/PE firms (including those with state-owned backgrounds), accounting for 91%, while 36 were corporate venture capital (CVC) firms, representing 9%. Shunxi Fund and Qiming Venture Partners ranked as the top two most active investors, each investing in more than eight companies. Among the top 11 most active institutions, those with state-owned backgrounds accounted for 33%, with Shunxi Fund, Shenzhen Capital Group, and Guangdong Science & Technology Venture Capital’s Fund of Funds being particularly active. Among active CVC firms, Legend Holdings’ venture capital arm was notably active.

There are currently 10 unicorns, concentrated in the biopharmaceutical sector.

In 2023, three new unicorns emerged (companies founded within the past 10 years with valuations exceeding $1 billion): Biocytogen Pharmaceuticals, Bluepha, and VectorBuilder. Additionally, three existing unicorns secured their latest rounds of financing. In 2024, no new unicorns were added; only Genetron Health obtained its latest financing.

Currently, there are 10 unicorns in the biomanufacturing sector (excluding Swire Biotech, which has entered bankruptcy proceedings), concentrated in the tracks of mRNA drugs/vaccines (2 companies), drug synthesis (2 companies), gene therapy (2 companies), and genetic engineering (2 companies).

Based on the above analysis, industry development trends and investment opportunities are as follows:

The bio-manufacturing industry is currently evolving toward diversified raw material utilization, highly efficient bioconversion systems, and full-chain, diversified product portfolios. As business models continue to innovate and applications in specialized sectors accelerate, the ecosystem of the bio-manufacturing industry will become increasingly robust.

The above content is excerpted from Cyzone’s “2024 Report on the Development of China’s Bio-Manufacturing Industry.” For more detailed information and data analysis, please visit VCBeat Analysis to access the full report.