Growth Halved: Is the Dental Industry Saying Goodbye to Its High-Growth Era?

ANGELAIGN

Dental Medical Consumables Supplier and Service Provider

MEI WEI DENTAL GROUP

Oral Health Service Provider

Envista

Dental consumables, equipment development, manufacturing, and sales

The high growth rates of leading dental companies have hit the “pause button.”

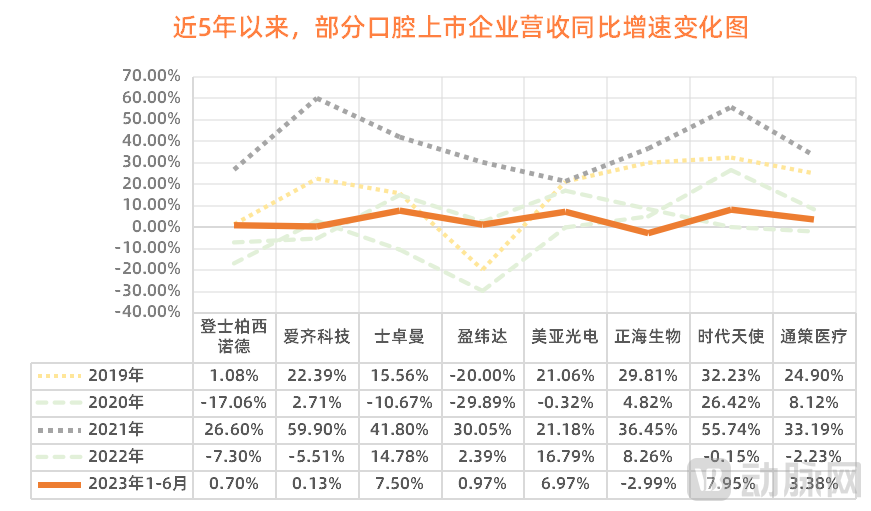

Recently, global publicly listed dental companies announced their first-half 2023 financial results as scheduled. After reviewing the financial reports of multiple dental enterprises, VCBeat found that,The previously robust performance growth rates of leading enterprises, which generally exceeded 20%, are slowing down, with year-on-year growth rates all falling below 10%, reaching a low point in recent years.

(Data source: Financial reports of listed dental companies; chart by VCBeat)

As shown in the table above, except for 2020, when the global COVID-19 pandemic led to negative year-over-year growth rates among leading dental companies, the majority of enterprises recorded growth rates exceeding 20% in 2019 and 2021, highlighting the high growth potential of the dental industry. However, since last year, the performance growth rates of leading dental companies have generally continued to decline.By the first half of this year, the growth rate was directly “halved.”

From the data, the dental industry appears to be bidding farewell to the era of high growth.

It should be noted that, from a global perspective, there are no fewer than 40 publicly listed companies in the dental sector. The data presented in this article primarily focuses on typical industry giants, particularly multinational corporations with strong ties to the Chinese market and leading domestic players.

In addition, to facilitate data alignment for observation and comparison, industry leaders with limited years of financial disclosure or those adopting different fiscal reporting cycles (such as Envista and Arrail Group) are not included in the table; however, the performance growth rates of these companies generally reflect the same trend.

Why Are the Growth Rates of Leading Dental Companies Slowing Down? What Key Challenges Is the Industry Facing? How Will It Evolve in the Future? To address these questions, VCBeat will analyze corporate financial reports and interview industry experts.

“Stalling” is unfolding in turn among the leading enterprises in the dental industry.

“Align Technology’s growth rate (with Invisalign as its subsidiary brand) has dropped to 0.13%. It’s hard to believe.” When VCBeat interviewed multiple industry insiders and presented the financial report data, they all expressed similar surprise.

It is worth noting that as a global leader in the dental industry, Align Technology has maintained an exceptionally high growth rate over the past five years, driving industry expansion. For instance, on the basis of nearly $2.5 billion in revenue in 2020, its income growth rate still reached 59.9% in 2021.

Not only that, ANGELAIGN, another leading enterprise in the clear aligner orthodontics sector alongside iOrtho Technology, reported a year-on-year growth rate of 7.95% in the first half of this year, marking a significant decline compared to the growth rates of over 30% commonly seen before 2022.

In the dental implant sector, the year-on-year revenue growth rates for the three industry leaders—Dentsply Sirona, Envista, and Straumann—in the first half of the year were only 0.7%, 0.97%, and 7.5%, respectively, falling below their historical averages. A similar trend was observed in niche segments such as CBCT, dental restorative materials, and dental medical services, with companies like Meyer Optoelectronic, Zhenghai Biotechnology, and Topchoice Medical also experiencing comparable slowdowns.

What Exactly Is Behind the Collective "Stall" of Industry Leaders?

After reviewing the financial reports of various companies, VCBeat found thatThe reasons for the slowing growth rate vary, stemming from a weak consumer environment, industry price wars, policy impacts such as centralized procurement, and subtle shifts in business models.

Specifically, Align Technology, the leader in clear aligner orthodontics, relies on North America as its primary market; however, this region is currently experiencing a consumption slowdown, leading to a decline in revenue growth. Notably, other international markets (including China) are emerging as significant growth drivers for Align Technology’s revenue.

Looking at ANGELAIGN, its growth rate turned positive in the first half of 2023, reaching 7.95%, which is higher than the industry average, although it still lags behind the levels seen in previous years compared to the negative growth in 2022. A review of the financial report reveals that ANGELAIGN’s business performance in the first half was actually quite strong, with a total of 95,400 clear aligner cases completed over the six months, representing a 23.6% increase from the 77,200 cases recorded in the same period in 2022.

But why does the revenue growth rate not reflect a consistent trend with the growth in case volume? It turns out that after calculating the revenue per completed case for clear aligner solutions, it was found that the average price per case for ANGELAIGN’s clear aligners dropped by 18.07%, from RMB 7,078 in 2022 to RMB 5,799 per case. In other words, while the volume increased, the unit price decreased, resulting in a significant discrepancy between the revenue growth rate and the case volume growth rate.

According to VCBeat, the number of companies entering the clear aligner orthodontics sector and securing financing has been rising rapidly since last year, leading to increasingly fierce market competition. Both Align Technology and ANGELAIGN are gradually expanding into lower-tier markets with lower average transaction values to achieve business growth. However, this strategy entails higher costs for market education and promotion.

TopChoice Medical, a service provider, has also been impacted by the orthodontics business. According to its financial report, TopChoice Medical’s orthodontic revenue declined by 3.9% year-on-year in the first half of this year. In response, TopChoice Medical stated that the primary reasons were the traditional off-season in the second quarter and weaker consumer demand for aesthetic-related services during the period.

An investor with long-term focus on the dental industry expressed similar views to VCBeat. He believes that the pandemic in recent years has significantly impacted people’s spending power, leading to a slowdown in the growth of discretionary consumption demand this year. “Clear aligner orthodontics is highly consumer-driven and falls under discretionary spending. With limited disposable income, consumers have naturally postponed such demands. Additionally, companies’ efforts to expand into lower-tier markets have resulted in lower average transaction values, causing a noticeable decline in growth rates.”

In the field of dental implants, the implemented volume-based procurement is undoubtedly a significant factor contributing to the slowdown in growth rates for leading enterprises.The results indicate that the centralized volume-based procurement of dental implants conducted earlier this year was characterized by its large scale and intense competition, involving 18,000 medical institutions across China and 2.87 million implant systems. The average selected price of the winning products decreased by nearly 60% compared to the median procurement price prior to the centralized procurement.

Based on the winning bid prices of Dentsply Sirona, Envista, and Straumann, the average price reductions were approximately 57%, 61%, and 63%, respectively. Taking Dentsply Sirona as an example, its financial report shows that implant-related revenue in the first half of this year decreased by 6% year-on-year.

Nevertheless, in the face of centralized procurement, multiple industry leaders have stated that although the prices of dental implant products have decreased due to the policy, their sales volume in China will rapidly expand, and the strong momentum of revenue growth will remain unchanged.

In the dental CBCT sector, financial reports from industry leader Meyer Optoelectronic show that the revenue growth rate of its medical equipment division (including dental CBCT and intraoral scanners) is at its lowest point within the overall business, standing at merely 1.28%. An insider from the company stated in a media interview that as different enterprises enter the dental CBCT market, some are constrained by limited brand recognition or product competitiveness, and can onlyPromotional price cuts aimed at expanding sales volume have intensified industry competition, which has also weighed on Meyer Optoelectronic’s revenue growth.

In the field of oral restoration, Zhenghai Biotechnology’s financial report disclosed that its oral restoration membrane and absorbable dural (spinal) membrane patches are the primary sources of revenue. Among these, the oral restoration membrane product generated sales revenue of RMB 106 million, representing a year-on-year decrease of 3.57%. In response, the company stated,The decline in revenue from oral repair membranes was driven by the dual impact of objective factors in January and February and the Spring Festival holiday.

It is not difficult to observe that behind the declining revenue growth of each enterprise lie various distinct reasons; however, within the current macroeconomic environment, the overall slowdown in consumption across the dental industry is posing significant challenges to these companies.

“This is an opportunity for structural adjustment, so neither be pessimistic nor overly optimistic.“Liu Zhenjun, a seasoned practitioner in the dental industry, told VCBeat, ‘The reason for not being pessimistic is that the expansion of the dental consumer market is a major trend, and the industry’s ceiling is far from being reached. The caution against excessive optimism stems from the fact that listed leading companies have been dominating their respective niche segments for many years; their pace of product and solution innovation must keep up with their current market standing. With an increasing number of new entrants, competition will become increasingly fierce.’”

Therefore, leading dental enterprises are seeking ways to break through the current impasse.

In response to the slowdown in revenue growth that began last year, leading dental companies have already implemented strategic adjustments to address these challenges.

For instance, in the Chinese market, where revenue is growing rapidly, Align Technology is promoting a more pragmatic “localization” product strategy by enriching its product portfolio and implementing price differentiation. It has already launched the Invisalign Adult Package and the Invisalign Standard Package to reach a broader target audience.

Envista is also optimistic about the Chinese market. At the beginning of the year, during the South China International Dental Exhibition, it officially announced its name change from “KaVo Group” to its current name, “Envista,” and unveiled its “Smile China” strategy. A key component of this strategy is localized industrial layout. Currently, Envista has established manufacturing bases in Suzhou, Jiangsu Province, and Ziyang, Sichuan Province—known as “China’s Dental Valley”—to optimize its local supply chain configuration.

Chinese innovative companies are actively expanding into overseas markets. For instance, ANGELAIGN disclosed that it has established subsidiaries in the United States, Europe, and Australia, and has initiated overseas acquisitions. In October 2022, ANGELAIGN announced the acquisition of a 51% equity stake in Aditek, a well-known Brazilian manufacturer of orthodontic products.

To cope with changes in centralized procurement, Topchoice Medical launched low-cost dental implant services this year to realize its “dental supermarket” concept covering high-, mid-, and low-tier offerings, thereby increasing market share, while simultaneously adjusting its dental implant pricing structure.

Dentsply Sirona announced a restructuring plan earlier this year, which includes an 8%-10% global workforce reduction. The plan is expected to generate annual cost savings of at least $200 million for Dentsply Sirona, thereby improving operational efficiency and performance.

Beyond multinational corporations’ heavy investments in China, domestic enterprises’ expansion into overseas markets, the development of new business strategies, and workforce optimization, more significant changes are stemming from personnel shifts.

VCBeat has observed that since the beginning of this year, Align Technology, Dentsply Sirona, and Straumann have all replaced their heads of China operations, while ANGELAIGN has also undergone significant changes in its senior management team.

Specifically, at the beginning of this year, Junho Han officially assumed the role of Vice President and Managing Director for China at Align Technology; in February, Zhang Ying was appointed General Manager for China by Dentsply Sirona; in April, Li Congzhen, General Manager for China at Straumann Group, made his public debut; and on July 31, Hu Jiezhang succeeded Li Huamin as Chief Executive Officer and Chief Technology Officer of ANGELAIGN.

Why the Change in Leadership? Taking ANGELAIGN as an example, its founder Li Huamin mentioned in a letter to all employees that ANGELAIGN no longer needs a patriarchal leader acting as a locomotive in this new phase. Instead, it requires a core leadership team equipped with a digital technology mindset and a global strategic vision to steer the company toward accelerated growth while ensuring safety and stability.

It can be seen that,Behind the leadership changes lies a clear signal: in this new phase of development, leading dental companies are urgently seeking fresh strategic vision and direction to navigate an increasingly complex market environment. This also indirectly reflects the intensity of market shifts.

“Given the significant volatility in the market, enterprises must maintain flexibility and make timely adjustments and corrections based on market feedback and internal conditions to ensure the sustained effectiveness of their strategies. Market competition is an art of ‘slicing the cake.’ Only by continuously deepening their moats can companies consistently slice the cake both larger and faster,” said Liu Zhenjun, a seasoned practitioner in the dental industry.

Despite drastic market fluctuations and a slowdown in revenue growth among leading enterprises, the overall upward trend of the dental market remains unchanged. This has kept investment and financing in the dental industry highly active.

The data speaks for itself.This year alone, a host of dental companies, including Weigao Jielikang, MEI WEI DENTAL GROUP, Dentifine, Shenzhen Yuru, Meiao Dental, Gendent, Chenglian Technology, Sailuo Medical, Yiyah Group, Wellplaece, and Proclaim, have completed new rounds of financing.

In the secondary market, Zhengya Dental filed for tutoring registration with the Zhejiang Securities Regulatory Bureau at the beginning of the year; Smiledent’s IPO on the ChiNext board was accepted; Dengkang Oral Care became one of the first new stocks listed under the registration-based system on the Shenzhen Stock Exchange Main Board; and Malo Clinic submitted its prospectus to the Hong Kong Stock Exchange. It is evident that companies across all segments of the dental industry chain—from oral care products to dental equipment and dental services—have either prepared for or completed their IPOs this year, further underscoring the high prosperity of the dental sector.

“Innovation is always the most critical factor determining whether an industry can achieve sustainable development,” said Liu Zhenjun, a senior practitioner in the dental industry.Innovation on the supply side of the oral care sector has been ongoing, with a continuous emergence of startups that have helped expand the market. Among these trends, digitalization has attracted the greatest attention from the investment community.

For instance, the company that just secured hundreds of millions of yuan in Series A financing in AugustWeigao Jielikang, focusing on the development of digital dental diagnostic and treatment equipment, dental implant systems, oral biomaterials, and surgical tools for implantology.

which completed a B-round financing of RMB 100 million in April this yearDentsplyIn building a digital dental platform, it has developed multiple devices, including 3D dental microscopes, EMOVE microscopes, dental imaging scanners, and dental CBCT systems, and launched the Kunlun CBCT with an ultra-large field of view in 2022. In August, Dentifi acquired Makovision, continuously expanding its footprint in the dental CBCT sector.

which also secured RMB 236 million in Series B financing in AprilChenglian Technology, it is building a one-stop digital solution for dental 3D printing. Chenglian Technology was formerly a supplier of 3D printing equipment and is now transitioning to a cloud printing service model. By applying the Hardware-as-a-Service (HaaS) model to the field of dental 3D printing, it enables intelligent internet connectivity for 3D printers and establishes large-scale distributed cloud factories for denture manufacturing worldwide, thereby integrating the "data–design–manufacturing" workflow in denture processing.

Service-oriented institutions are also placing increasing emphasis on digitalization. For instance, those rushing for an IPO in AugustMa Long Dental, it also specifically mentioned in the prospectus that it would upgrade its digital management system to enhance overall operational efficiency, particularly including clinical digitization (such as purchasing advanced dental equipment like digital dental implant robots) and management digitization (such as data transmission and the storage and management of patient imaging data).

having completed a new round of strategic financing by the end of JuneMEI WEI DENTALIt is also actively promoting digitalization. As the first dental chain enterprise in the industry to possess a self-developed digital system, MEI WEI DENTAL GROUP has created the “Wei Xiaomei Medical Cloud Intelligent Platform,” an information system centered on enhancing management and operational efficiency. The platform encompasses HIS, finance, supply chain, human resources, OA, and other systems, enabling both refined corporate management and comprehensive support for multi-organizational business coordination and data sharing.

It is evident that the dental industry continues to see a steady stream of innovators, with investors willing to back them with substantial capital. This further demonstrates that the long-term value of the dental sector remains unchanged, and there are still ample commercial opportunities yet to be realized.

It is worth noting that industrial synergy and capital empowerment are crucial in the process of accelerating digital innovation among dental enterprises.

In response, multiple investors told VCBeat,Innovative enterprises can optimize products and operations across all stages of their digitalization processes through in-house R&D, financing, mergers and acquisitions, IPOs, and other means, thereby strengthening product synergies and driving steady business growth.

In other words, companies should strive to expand their product portfolios through various means and deepen their technological moats, thereby establishing a strong foothold in their areas of competitive advantage.

Once consumer demand rebounds, dental innovation companies with deeper roots are bound to experience stronger growth.