China's Pet Pharmaceutical Industry Faces Three Critical Challenges Amid the Booming Billion-Dollar Market

Veterinary drugs refer to substances used for the prevention, treatment, and diagnosis of animal diseases or for the purposeful regulation of animal physiological functions.Pet Medicines as an Important Component of Veterinary Drugs, refers to drugs specifically used for the prevention, treatment, and diagnosis of pet diseases, to ensure the physical and mental well-being of pets, as well as to prevent the transmission of pet diseases to humans, thereby safeguarding the health and safety of pet owners.

The target species for pet medications primarily include cats, dogs, pet rabbits, pet rodents, reptiles, and insects kept for non-economic purposes. In contrast to traditional veterinary drugs targeting food-producing animals,Pet medicines, as an emerging blue-ocean market over the past decade, account for less than 20% of the total output value of the veterinary drug industry.(Data source: "2022 China Pet Medical Industry White Paper"), offering greater room for technological innovation and broad market growth potential.

According to QYResearch data, the global market size for pet pharmaceuticals reached USD 12.608 billion in 2019,It is projected to reach US$20.058 billion in 2026, equivalent to approximately RMB 140.1 billion.(Calculated based on the central parity rate of the US dollar against the Chinese renminbi published by the People's Bank of China from January to August 2023), the compound annual growth rate (CAGR) was 7.04%. Among these, the Chinese market has undergone rapid changes in recent years. In 2019, the size of China's pet pharmaceutical market reached USD 176 million, and it is projected to reach USD 481 million by 2026, with a CAGR of 16.44%.

Faced with a booming blue-ocean market valued at hundreds of billions, China is still in the early stages of independently developing veterinary pharmaceuticals. VCBeat, as an observer of the healthcare industry, is also closely monitoring the development of this emerging sector.This article reviews the evolution of policies and key pain points in China’s pet pharmaceutical sector, profiles industry players and identifies prevailing patterns. It also examines persistent challenges after years of development and explores pathways to commercialization, aiming to provide insights and perspectives for the industry’s growth.

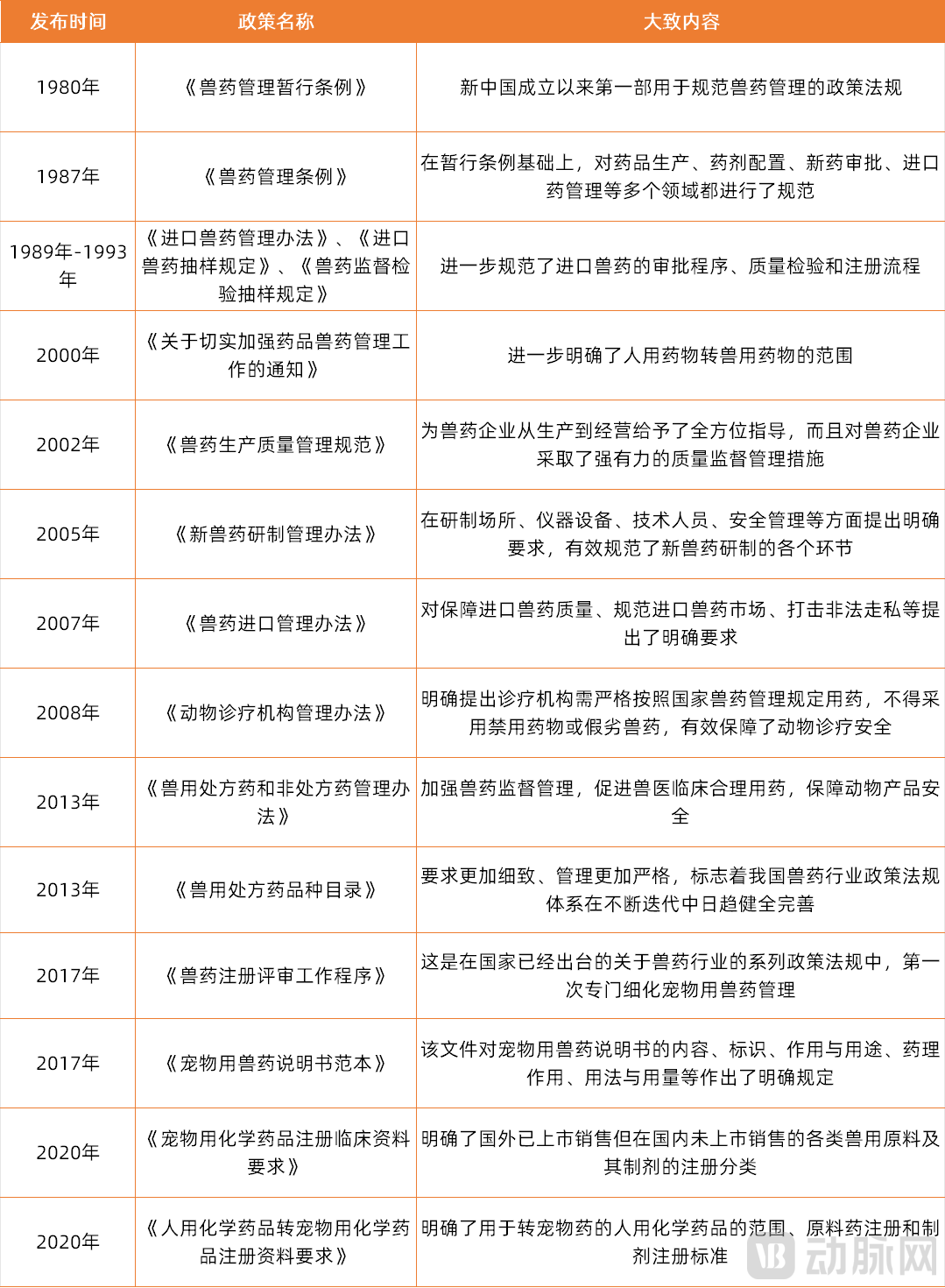

In August 1980, the State Council promulgated the Interim Regulations on Veterinary Drug Administration, the first policy and regulation since the founding of the People's Republic of China to standardize veterinary drug management. It established provisions governing the administration, production, supply, use, and research institutions related to veterinary drugs, marking a milestone policy that formally ushered China's veterinary drug industry into an era of standardized management.

According to incomplete statistics, policies and regulations regarding veterinary drugs in recent years

(Data sourced from public information)

Although China has had a legal framework governing veterinary drugs for over 40 years,However, regulations specifically targeting veterinary medicines for pets have only begun to emerge in the past six to seven years.VCBeat has compiled a selection of regulatory documents related to the veterinary drug sector in recent years, based on publicly available information, and found thatThe development history of China's veterinary drug regulations can be roughly divided into three stages:

Incubation Stage: Before 2000,During this period, most of the policies and regulations promulgated and revised in China were milestone achievements, filling previous regulatory gaps in related fields or clarifying previously ambiguous scopes and provisions. For example, the Interim Regulations on Veterinary Drug Administration, the Regulations on Veterinary Drug Administration, and the Notice on Effectively Strengthening the Administration of Human and Veterinary Drugs were respectively the first policy and regulation in China to standardize veterinary drug management, the first regulation to govern imported veterinary drugs, and the first regulation to define the scope for converting human drugs into veterinary drugs.

Phase of Rapid Development and Improvement: 2000–2010,During this phase, China primarily undertook multiple revisions to the "Regulations on the Administration of Veterinary Drugs," building upon the policy and regulatory framework established prior to 2000.Rapidly released multiple supporting regulations, establishing regulatory moats across the entire lifecycle of veterinary drugs—including manufacturing, research and development, distribution, and supervision—China’s policy and regulatory framework in the veterinary drug sector has begun to mature into a well-defined model.

Refinement and Emerging Stage: 2010 to Present,During this phase, China continued to refine the management of veterinary drugs—covering market supervision, prescription and over-the-counter drug classification, and registration categories—based on previously issued policies. Notably,Pet medicines, which had previously been encompassed within the veterinary drug sector,In the “Procedures for Review and Approval of Veterinary Drug Registrations” promulgated in 2017, certain categories were delineated for separate management for the first time, and a “priority review” mechanism was introduced for veterinary drugs specifically intended for racehorses and pets that are urgently needed clinically or in short supply on the market. This move has been regarded by the industry as a significant policy benefit promoting the development of veterinary drugs for pets.

Following this favorable policy, China has successively issued specialized regulations and policies for pet medications in recent years, including the Model Instructions for Veterinary Drugs for Pets, Requirements for Clinical Registration Data of Chemical Drugs for Pets, and Requirements for Registration Data for Converting Human Chemical Drugs to Pet Chemical Drugs. These measures demonstrate macro-level emphasis on and encouragement of the emerging field of pet pharmaceuticals.

Although the vast future market for pet pharmaceuticals has begun to take shape, it is undeniable that there are still many areas in China’s pet pharmaceutical sector that require improvement. These include the cost and pricing of veterinary medical products and services, regulatory oversight of online sales of pet medications, the misuse of human and livestock drugs in pets, and the unapproved use of unregistered drugs in animals. Only time will allow these issues to be gradually addressed and resolved.

Driven by both policy incentives and existing pain points, how will pharmaceutical companies, as upstream participants in the pet medication market, adapt and strategize?

Previously, there were few domestic enterprises specializing in the production of pet medications. Most pet drugs were manufactured by veterinary pharmaceutical companies that either expanded their production lines or restructured their pet drug production departments while producing veterinary medicines. In recent years, encouraged by policies and regulations, a large number of innovative pet pharmaceutical companies driven by emerging technologies have emerged.

However, these measures are insufficient to meet the growing demands of pet owners, as the pet population continues to rise year after year. According to big data from Petdata, the number of dogs and cats in urban areas of China reached 116.55 million in 2022, a 3.7% increase from 2021. Among them, the dog population was 51.19 million, accounting for 43.9%; the cat population was 65.36 million, accounting for 56.1%, showing a continuous upward trend with a 12.6% increase from 2021. According to Frost & Sullivan, it is estimated that the number of pets in China will grow to 446 million by 2024.

Since most traditional veterinary drug companies lack dedicated pet medicine pipelines, their production scales are relatively small and their product portfolios limited, failing to meet the rapidly growing demand for pet-specific medications driven by the pet industry’s expansion. Meanwhile, emerging companies that have recently entered the pet pharmaceutical sector face long drug development cycles; consequently, most of their pipelines remain in preclinical or clinical stages, preventing them from reaching the market and alleviating supply pressures.

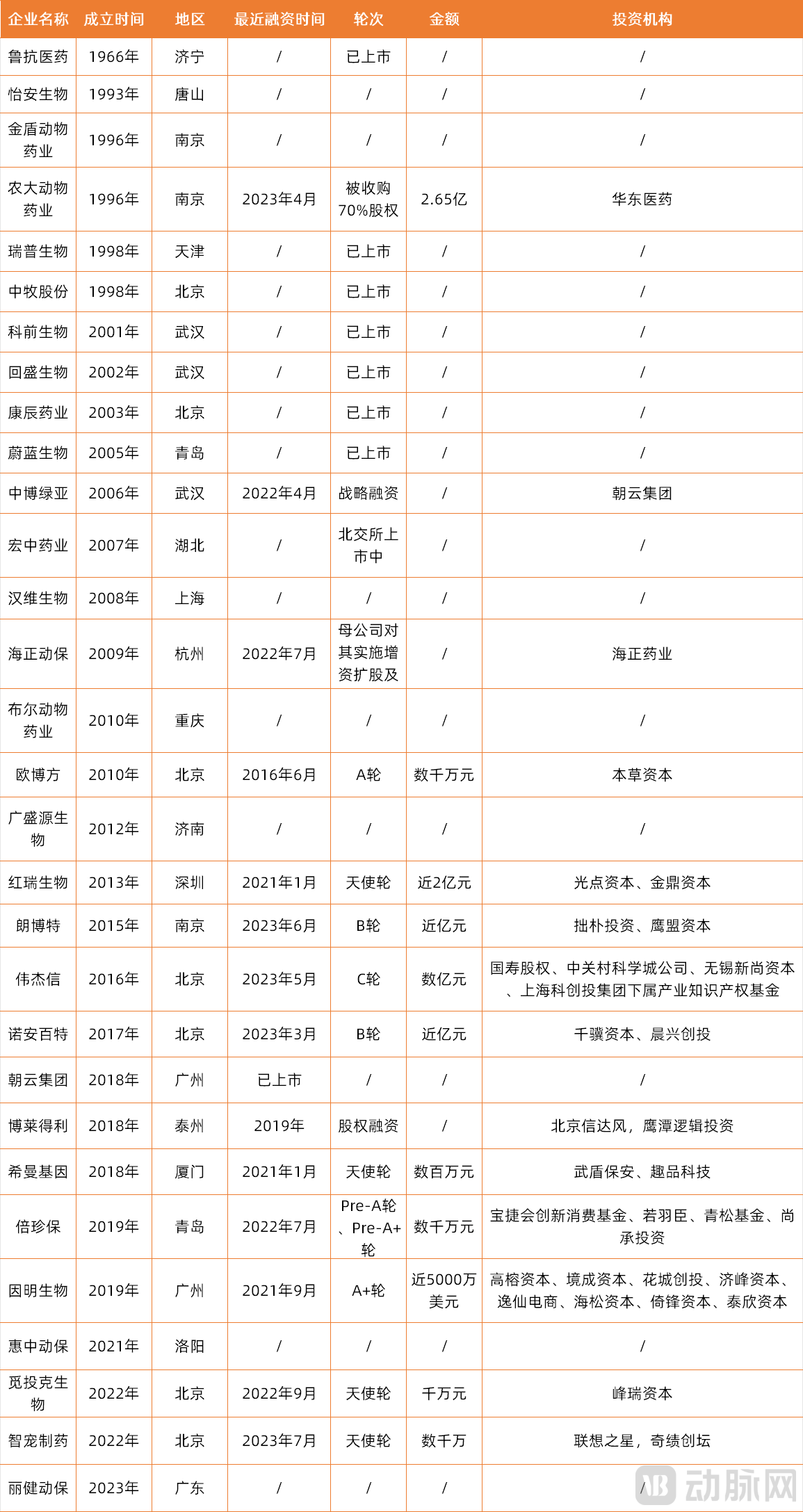

According to incomplete statistics, some companies in China that have laid out their presence in the pet pharmaceutical sector

(Data sourced from publicly available information, enterpriseArrangementThe order isChronological Order of Establishment)

Based on publicly available information, VCBeat has compiled a list of 30 companies that have entered the pet pharmaceutical sector (the list is still incomplete and feedback is welcome). It is evident that approximately half of these companies were established before 2010, while the other half were founded after 2010, aligning with the policy development milestones mentioned earlier.

According to the table data, approximately 50% of companies established before 2010 have gone public and reached a relatively mature stage of development. Most of these companies were previously engaged in the livestock and other economic animal sectors, and in recent years, they have innovatively entered the pet pharmaceutical market in response to shifting demand.

Among enterprises established after 2010, approximately 70% have successfully secured financing in recent years despite the capital winter., well-known investment firms such as Morningside Venture Capital, Gaorong Capital, and Legend Star have all entered the market. Most of these startups are concentrated in the niche sector of pet pharmaceuticals, with innovative technologies and products.

Capital is willing to bring “warmth” during the winter, which is closely related to social development in recent years. According to statistics, half of pet owners in China are post-90s generations, while the other main group of pet owners consists of the elderly.Pets not only alleviate the social pressure faced by contemporary young adults but also bring warmth and companionship to today’s aging society, making them a “basic necessity” in the new era.

It is evident that the domestic pet pharmaceutical sector is currently characterized by a balanced landscape, with traditional veterinary drug companies and emerging pet-specific pharmaceutical firms each holding half of the market.China's pet pharmaceutical sector is undergoing technological iteration and market-driven product upgrades.

In contrast, established global animal health giants such as Zoetis, Boehringer Ingelheim Animal Health, Merck Animal Health, Elanco, IDEXX, and Ceva have been deeply entrenched in the pet healthcare sector for decades. Pet vaccines and deworming medications like Purevax (a Zoetis product) and Drontal (a Bayer product) have long gained widespread recognition and trust among end consumers.

However, unmet needs persist not only in China but also globally in areas such as pet oncology and immune-mediated diseases. On the other hand, large animal health companies are less flexible in their strategic positioning compared to startups, while domestic innovative pet pharmaceutical companies enjoy greater local advantages.

According to data released by the Yachong Research Institute, China’s pet consumer market size reached RMB 206.5 billion in 2020. According to statistics from the American Pet Products Association (APPA), the U.S. pet market size had already reached $103.6 billion in 2020, equivalent to over RMB 700 billion. This indicates that, similar to China’s biopharmaceutical sector, China’s pet industry is still in its nascent stage, with significant room for future growth. Leveraging the fertile ground of China’s pet market, domestic companies are well-positioned, and there will be opportunities for a new wave of emerging enterprises focused on innovative pet pharmaceuticals to rise in China.

Although foreign countries have decades or even a century of R&D history in the field of pet medicine, most companies' flagship products are still concentrated on traditional infectious diseases, parasitic diseases, seasonal diseases, conventional vaccines, etc.For the substantial unmet clinical market demands in pet care—such as oncology, geriatric diseases, nutritional disorders, neurological conditions, and metabolic diseases—both domestic and international sectors are in their nascent stages, creating a level playing field where all participants compete on equal footing.

Taking tumor treatment as an example, there are currently approximately 130–150 anticancer drugs approved for marketing worldwide for the treatment of human tumors, and about 1,300–1,500 various anticancer pharmaceutical formulations prepared from these drugs.Only Two Drugs Are Currently Marketed for the Treatment of Pet Tumors, namely Zoetis’ tyrosine kinase inhibitor (TKI) Palladia and Merck & Co.’s PD-1 antibody Gilvetmab.

Palladia, with the generic name toceranib phosphate, is the world’s first targeted therapy for cancer in pets. It is indicated for the treatment of recurrent cutaneous mast cell tumors (with or without lymphadenopathy) classified as Patnaik grade II or III in dogs. Its primary mechanism of action involves killing tumor cells and cutting off their blood supply. Gilvetmab is a potent canine-derived anti-PD-1 monoclonal antibody that works by blocking the interaction between PD-1 and its ligand, PD-L1, and is used for the treatment of mast cell tumors or melanoma.

The product insert for Paladine recommends a dosage of 3.25 mg/kg. It is reported that, in practice, the administered dose is generally lower than this recommendation to minimize side effects. As the medication is available only in three strengths—10 mg, 15 mg, and 50 mg—actual administration requires pill splitting by healthcare professionals using specialized tools at a hospital. The fee for this pill-splitting service is approximately RMB 300 per session. The drug itself costs around RMB 250–300 per tablet for the 50 mg strength, and RMB 80–130 per tablet for the 10 mg and 15 mg strengths. The dosing frequency is once every two days.

Based on a medium-sized dog weighing 20 kg, the dosage per administration is 65 mg. The monthly cost of Palladia for tumor treatment amounts to approximately RMB 5,700, and this dosing regimen must be maintained continuously. Discontinuation of the medication will lead to renewed tumor growth, imposing a financial burden that is largely unsustainable for average pet owners.

This is also a key reason for the current scarcity of innovative pet drugs on the market. Drugs with high efficacy are often underpinned by emerging technologies; whether it involves antibody drugs, protein therapeutics, or cell and gene therapies, these novel drugs and treatment modalities entail substantial costs.How to balance the cost-effectiveness of drugs is the first pain point that needs to be overcome before initiating a project for innovative pet medications.

The second major challenge in developing innovative veterinary drugs lies in the various difficulties encountered during clinical trials.It is reported that the complexity of developing an innovative veterinary drug for pets is no less than that of developing a human pharmaceutical.Preclinical studies, including toxicology and safety assessments, pharmacological and efficacy evaluations, and pharmacokinetic studies, are required. Even under optimal conditions, the research and development cycle still takes 5–7 years. Clinical trials must be conducted in veterinary hospitals qualified under Good Clinical Practice (GCP) for veterinary drugs. According to the China Veterinary Drug Information Network (data as of August 23, 2023), most GCP-compliant trial institutions focus on livestock and poultry such as pigs, cattle, sheep, and birds; only a few institutions have the necessary resources to conduct clinical trials for pets, and most of these are affiliated with agricultural universities or animal health companies.

How to Overcome the Pain Points in Innovative Pet Drug Development and Accelerate Their Market Entry? VCBeat Summarizes the Following Three Points:

First, innovative pet pharmaceutical companies must have sufficient "backing."As indicated above, behind the successful launches of oncology drugs for pets by Zoetis and MSD stand pharmaceutical industry giants such as Pfizer and MSD. In China, most institutions qualified to conduct Good Clinical Practice (GCP) trials are top agricultural universities and animal health behemoths. Most companies entering the pet pharmaceutical sector either have backgrounds in agricultural universities or experience in human or veterinary drug development. Only with a solid foundation in underlying logic and technology can subsequent processes—such as technology transfer, optimization, and iteration of their products—proceed without encountering critical bottlenecks.

Secondly, although the R&D process of innovative drugs for pets lags behind that of human innovative drugs, this may not necessarily be a bad thing.Companies developing new veterinary drugs can proactively reserve emerging technologies such as cell and gene therapy, and then refer to the mature R&D and commercialization systems validated in human pharmaceuticals. They may advance their veterinary drug pipelines after the market launch of corresponding human drugs, or repurpose human medications for veterinary use in accordance with regulations. This approach also helps enterprises address some of the pain points related to “cost-effectiveness.”

Finally, domestic innovative pet pharmaceutical companies can also leverage China’s unique historical context to develop drugs better suited to the Chinese market.Traditional Chinese Medicine (TCM) is a treasured gem of China’s traditional medical heritage. According to relevant literature, TCM can be used in the clinical treatment of various pet diseases, such as gastroenteritis in dogs and cats, acute and chronic eczema in dogs, and canine distemper. However, numerous challenges remain, including unclear active ingredients and mechanisms of action, inconsistent drug quality and efficacy, and a lack of pharmacological and safety evaluations. Furthermore, there is currently an absence of relevant policies and regulations clearly addressing clinical trials and the application of TCM for pets. Integrating modern pharmaceutical technologies and big data analytics with TCM for pets can facilitate the extraction, identification, separation, and purification of its active ingredients. Therefore, the development of TCM-based veterinary drugs may represent another distinctive pathway for innovative Chinese pet pharmaceutical companies.

It is undeniable that China’s pet pharmaceutical market still has many areas requiring improvement. Compared with foreign animal health giants that have histories spanning decades or even centuries, emerging domestic pet pharmaceutical companies are still in their nascent stages. However, guided by the mature market systems established by multinational corporations, innovative pet drug products developed in China will gradually achieve commercialization after completing standard development cycles. Perhaps the current state of development in the pet pharmaceutical sector is analogous to where China’s biopharmaceutical industry stood a decade ago. Building on the robust growth of the biopharmaceutical sector, we look forward to the day when new pet drugs from China will rapidly emerge and stand shoulder-to-shoulder with international giants.

References:

1. Luo Zunping, Research on the Policy and Regulatory Management System for Veterinary Drugs Used in Pets in China, Chinese Journal of Veterinary Drug, Vol. 56, No. 10, October 2022

2. Pei Shuli, Zhou Min, Yin Ling, Li Aixin, "Problems and Countermeasures for the Development of China's Pet Pharmaceutical Industry," Agricultural Sciences, 2019, Issue 6 (Part II).

3. Xu Kepeng, Ou Qianqian, Xue Hong, Luo Dongli, Zhang Shuyue, Xu Yan. Traditional Petism: The Influence of Pet Owner Identity, Pet Type, and Pet Traits on the Moral Status of Pets. Acta Psychologica Sinica, 2023, Vol. 55, No. 10, 1662-1676

4. “2022 White Paper on China’s Pet Healthcare Industry (Industry Research Report)”

5. Dashuai's Doghouse, "Pet Targeted Drug—Palladia"