How Mehow Medical Became a Shining Star in Medical Device OEM Export with 93.54% Overseas Revenue

Mehow

Medical Device R&D and Manufacturing Service Provider

Even when engaging in OEM, one must strive to be the strongest OEM manufacturer—this may well be one of the development philosophies of Shenzhen Mehow Innovative Ltd. (hereinafter referred to as “Mehow”).

For a long time, although OEM has been the most mature model for Chinese medical device companies expanding overseas at the current stage, compared with directly acquiring foreign brands or establishing independent brands for international expansion, OEM is often labeled as having “low bargaining power,” “limited influence,” and even “low technological content,” evoking little sense of pride when mentioned.

However, the emergence of Mehow has, to some extent, shattered such prejudices—both the “Buy” recommendations issued by major securities firms and the recent increase in holdings via the Shenzhen Stock Connect underscore the capital market’s optimism about the company’s future prospects. Moreover, Mehow’s prospectus is replete with pride in its innovative technologies, manufacturing capabilities, and ability to expand its customer base.

This impression is not unfounded,Mehow is indeed the largest manufacturer in China of components for home-use ventilators and cochlear implants. Since its inception, overseas sales have been its primary source of revenue. As of today, overseas sales still account for 93.54% of Mehow’s total revenue.(Note: Data source is Mehow's 2022 annual report; the 2023 semi-annual report did not disclose the breakdown of domestic and overseas revenue.)

Furthermore, sinceSince disclosing its revenue data, Mehow has maintained steady revenue growth.——From 2018 to 2021, Mehow’s revenue increased from RMB 582 million to RMB 1.137 billion, with a CAGR of 25%; from 2021 to 2022, Mehow’s revenue also maintained a growth rate of 24.43%.

andWhile maintaining steady revenue growth, Mehow has kept its gross profit margin at 45%-50% and its net profit margin at 28%-31% in recent years.It is indeed challenging for a manufacturing enterprise.

Beyond its revenue success, Mehow’s decade-long partnership with its largest client, Client A—highlighted by being named Client A’s “Best Supplier” for ten consecutive years and Client B’s “Most Valuable and Excellent Partner for Five Years of Service” for five consecutive years—underscores its success as an OEM manufacturer and indirectly validates the effectiveness of its overseas expansion strategy. This offers valuable insights for other Chinese OEM manufacturers pursuing global markets.

However, once a sapling that was once “attached” to a large tree grows into a tree itself, it will naturally be unwilling to continue living in dependence. Therefore, in recent years, Mehow has indeed been striving to shed this label and seek a broader path of development while maintaining its core business. This approach can also serve as a reference for the iterative development of domestic OEM manufacturers.

Although Mehow has begun to gradually lay out its independent products,Overall, Mehow remains a B2B business—leveraging its innovative technologies to provide domestic and international medical device clients with end-to-end services, ranging from product design and development to mass production and delivery.

Since the target clientele consists of B-side customers, two key questions arise: which B-side customers to serve, and how to serve them effectively.

andStarting from the question of what type of B-end clients to serve, two more specific questions arise: which industry sector’s clients to serve, and what scale of clients to serve.

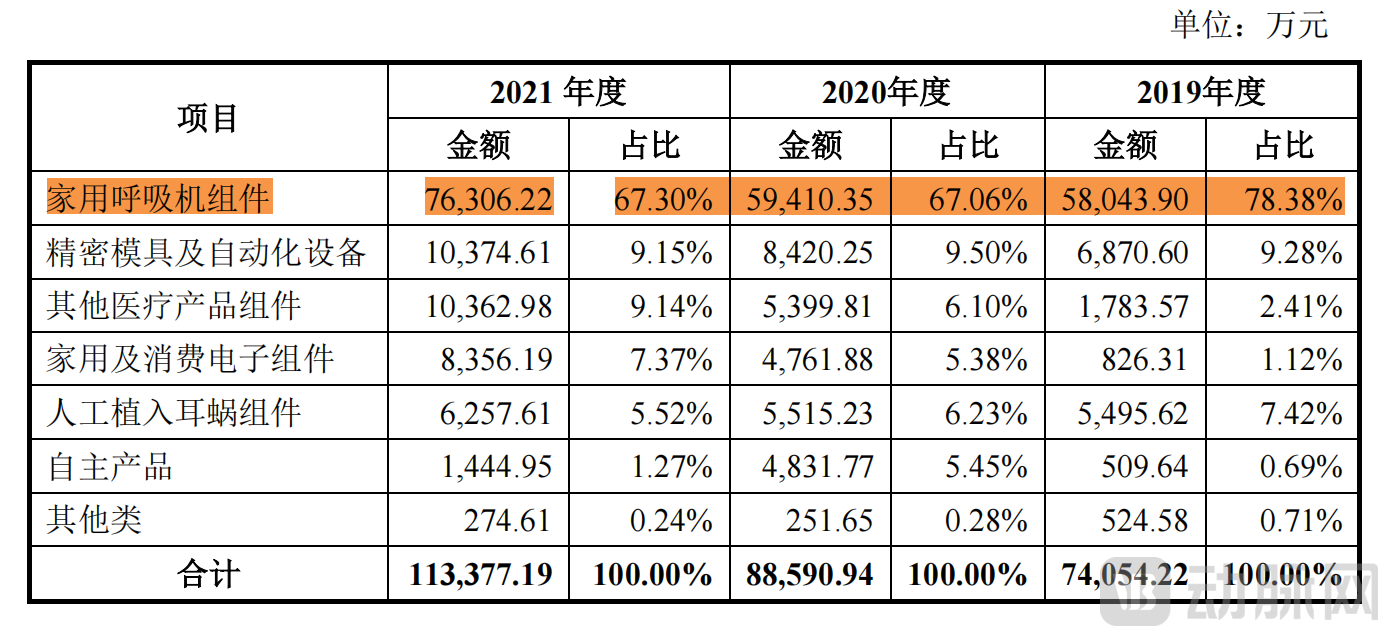

Regarding the former, from today’s perspective, we can ascertain thatHome ventilators and cochlear implants are the two most important sectors selected by Mehow. Among them, revenue from ventilator components holds the most significant position, contributing 74.8% of the total revenue in 2022., representing a year-on-year increase of 38.73%, while components for manual cochlear implants contributed 6.92% of the revenue, with a year-on-year growth of 56.61%.

Excerpt from Mehow's Prospectus

Furthermore, the design, development, and production of ventilator components and cochlear implant components have been Mehow’s core business direction since its inception. While we cannot ascertain with certainty why founder Xiong Xiaochuan firmly chose the ventilator and cochlear implant sectors in 2010, facts have proven this decision to be highly prudent.

According to market data from BMC Medical’s prospectus, the global market for home non-invasive ventilators grew from $1.707 billion in 2016 to $2.709 billion in 2020, representing a compound annual growth rate (CAGR) of 12.23%. During the same period, the global market size for respiratory masks (based on ex-factory prices) increased from $1.12 billion to $1.62 billion, with a CAGR of 9.83%.

As for the cochlear implant market, it grew from $1.051 billion in 2015 to $1.45 billion in 2019, with a compound annual growth rate (CAGR) of 8.38%.

Although market growth appears modest, favorable policies—such as long-term plans for chronic disease prevention and control, and the inclusion of cochlear implants in medical insurance reimbursement—are expected to further expand future market potential.

andFrom an industry perspective, ventilators and cochlear implants are both classified as high-end medical devices, with high entry barriers. Cochlear implants, in particular, represent the most advanced hearing assistance technology currently available, resulting in exceptionally high industry barriers.Higher entry barriers imply that successful market entrants gain industry recognition for their capabilities, which raises the difficulty for latecomers to catch up. This dynamic helps companies further consolidate their strengths, reinforcing a “strong-get-stronger” effect.

Meanwhile,High barriers to market entry also imply a high level of industry concentration.In other words, the global high-end medical device market is dominated by developed countries and regions in Europe, the United States, and Japan. Specifically, the global home ventilator market has long been controlled by ResMed and Philips Respironics. In 2020, these two companies collectively held a 78.1% market share, with ResMed accounting for 40.3% of the total. (Source: BMC Medical Co., Ltd. Prospectus)

The cochlear implant market is primarily dominated by Cochlear, Advanced Bionics, and MED-EL, with Cochlear holding an absolute leading position and capturing 60% of the global market share.

From the perspective of corporate management, a concentrated competitive landscape means that once a supplier becomes the industry leader, it will enjoy sustained and ample order volumes, which not only spread fixed costs but also ensure stable profitability.

Moreover, high-end medical devices generally entail stringent quality requirements, with rigorous standards and extended timelines for component selection and certification. For certified products, switching core component suppliers would incur additional costs for mold development, re-validation of product quality, and recertification, while sufficient component production capacity cannot be secured in the short term. Therefore,The selection of precision component suppliers for high-end medical devices exhibits stability. This is particularly evident when industry leaders choose their suppliers.

In light of the aforementioned factors, Mehow has formulated its current market development strategy—focusing on expanding into the global high-end medical device supply chain market, with its primary target customers being the top 100 global medical device companies.

As for which industry-leading device manufacturers it has partnered with, we will leave that aside for now, as related topics will be addressed later in the article. At this point, we need only clarify one fact: Mehow’s primary revenue sources at the current stage are derived from its partnerships with the leading companies in the home ventilator and cochlear implant industries.

However, it must be noted that Mehow has not completely abandoned serving small and medium-sized enterprises (SMEs). Its prospectus explicitly states: “At the same time, we are committed to providing innovative product development services for promising innovative SMEs in niche segments of the global medical device market.”

However, this is merely a small service market carved out on the foundation of serving the top 100 global medical device companies, not the “core” market it intends to develop.

The reasons are also clearly explained in its prospectus—““If a company primarily serves small customers, it often encounters scenarios characterized by high volumes of individual orders and a wide variety of order types. Coupled with the inherent nature of component products as non-standard parts, this increases the workload for mold development, as well as the frequency of production line debugging and product changeovers, thereby raising costs and impacting the company’s profitability.”

At this point, we have a clear understanding of why Mehow chooses to focus on serving large clients. However, having chosen the right ship, how does one board it and stay aboard? This relates to the second question mentioned earlier—how to effectively serve these enterprises.

Mehow indeed “has what it takes” in serving large-scale clients. Otherwise, its largest client, Client A, would not have maintained a partnership with Mehow for over a decade, nor would Client B have sustained a collaboration of at least five years. Moreover, both major clients have highly affirmed Mehow as their partner by presenting it with awards.

So, what exactly are these “two brushes”?

Before the official unveiling, we need to reiterate one point: Mehow’s primary business model is B2B, which means that Mehow can achieve positive growth simply by serving its B-end clients well. Serving B-end clients well naturally entails meeting their needs, and even anticipating their expectations.

So,What are the needs of Mehow’s B-end customers for component suppliers like Mehow?

First, ventilators and cochlear implants are both high-end medical devices; the manufacturing of their components requires precision engineering processes, which in turn demands that manufacturers possess advanced precision manufacturing capabilities.

Secondly, different users have varying requirements for the structure, outsourced components, performance, color, and texture of precision medical device components, and different brands typically have their own unique industrial designs, which requires component suppliers to possess customized production capabilities;

Furthermore, the quality level of components is also critical to the quality of medical device products; therefore, medical device manufacturers typically require component suppliers to have a robust quality control system and the capability to produce high-quality components.

Finally, on the basis of ensuring quality, precision, and customizability, medical device brands also require component suppliers to possess excellent delivery capabilities—namely, rapid and high-volume production—to accelerate product commercialization.

Overall,In terms of manufacturing, medical device brands generally require component suppliers to meet five key criteria: precision manufacturing, customization, high quality, high efficiency, and high production capacity.To some extent, precision manufacturing and customized production may be paradoxical to high efficiency and high capacity.

Therefore, it is already challenging for a component supplier to master even one of these elements, let alone all of them. Yet Mehow has achieved this. It is precisely the integration of these five capabilities that has established Mehow’s leading position in the supply of components for domestic home-use respiratory devices and cochlear implants. This integration also constitutes the core competitive moat built by Mehow. (Note: Leveraging its deep expertise in precision manufacturing and automated production, Mehow has even independently developed a business line focused on precision mold manufacturing and automated equipment, which contributed 9.15% of its revenue in 2021.)

According to Mehow’s prospectus, the company possesses 29 core technologies covering the design, development, and manufacturing of ventilators, cochlear implants, and spirometers (its proprietary products).

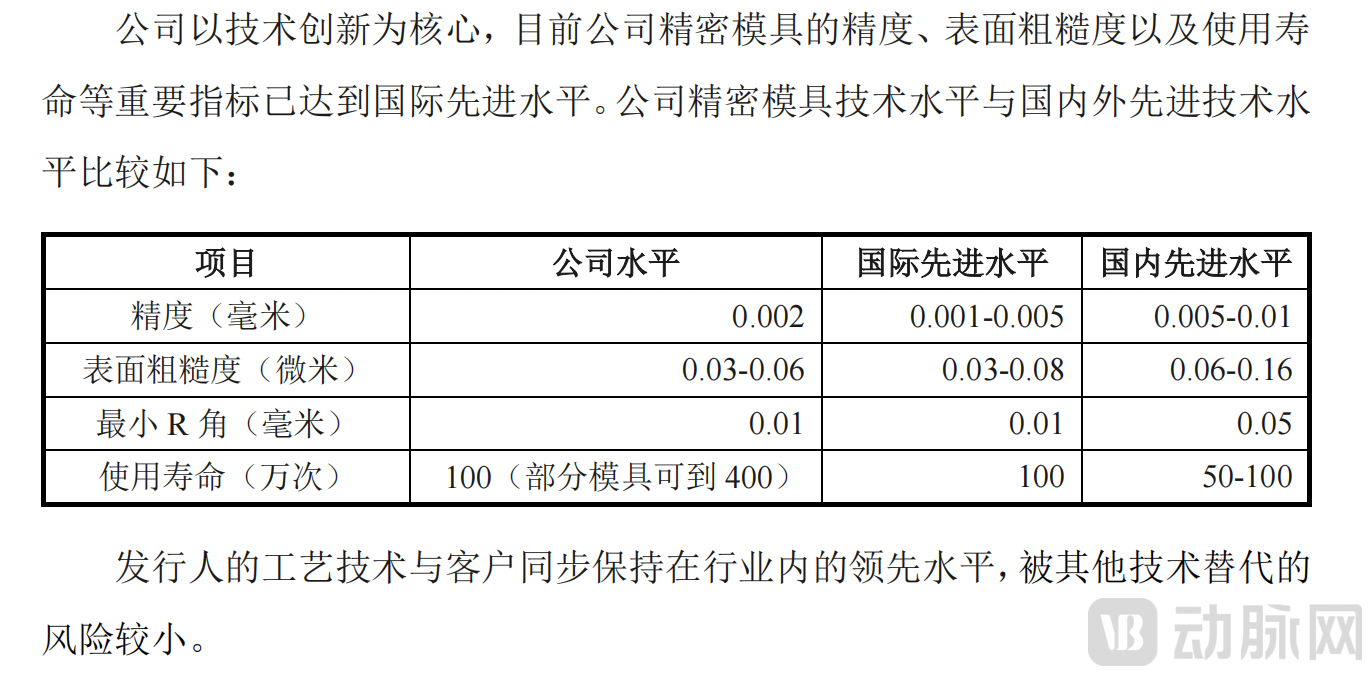

Specifically,In precision manufacturing, Mehow's precision molds have reached an internationally advanced level in terms of accuracy, surface roughness, and service life.

Excerpt from Mehow’s IPO Prospectus

In terms of quality and production efficiency,Leveraging precision injection molding technologies for plastics, liquid silicone rubber (LSR), and implantable devices, Mehow ensures high quality and stability in product molding, enables rapid changeovers across various product lines, and achieves a high production plan fulfillment rate.

Meanwhile, Mehow has established a comprehensive automation design and development team, mastering core technologies such as automated mechanical design and electronic control system design, and utilizing various types of automation equipment to meet customer needs for automation in new product development.

Furthermore, as previously mentioned, customized production may be paradoxical to high efficiency, implying that it can reduce production efficiency to some extent.

In this regard,Mehow’s independently developed layered molding mold design and manufacturing technology for liquid silicone rubber enables multi-layer, multi-shot molding during the LSR product forming process. It also allows for the integration of functional and structural components, such as chips, cables, and magnets, within the layered structure. This enhances design flexibility and resolves the challenge of integrated molding for multi-material, multi-structure, and multi-functional products.

Thus, issues related to precision manufacturing, quality, and efficiency have been properly resolved. (Solutions for customization and capacity challenges are detailed later.) In practice, the application of numerous innovative technologies has not only met the needs of device brand owners but also reduced Mehow’s labor costs and improved its profitability.

andAmong the many innovative technologies it applies, the most noteworthy is precision liquid silicone rubber (LSR) injection molding. This can be regarded as Mehow’s core competency.

This is because liquid silicone rubber has a wide range of applications. Although its molding process offers greater efficiency and cost advantages compared to conventional solid silicone rubber, it is more sensitive to raw material ratios, reaction temperature, mold quality, and catalysts during the reaction process, thereby entailing a higher level of technical sophistication.

If the application of numerous innovative technologies has enabled Mehow to build core competitive barriers, securing its “ticket” and allowing it to remain aboard the “big ship” for the long term, then its ecosystem development in overseas markets and its market expansion strategies are the key factors that deeply bind it to this “big ship.”

Once on board, in addition to sustaining a long-term presence, every enterprise with grand ambitions would undoubtedly seek to forge closer ties with the vessel.

How to achieve deep integration with it has become Mehow’s “second specialty.”

Specifically,Mehow has undertaken two key initiatives: first, it formulated a market expansion strategy focused on “deepening and broadening business with existing high-quality clients”; second, it strengthened and refined its overseas ecosystem layout to respond more rapidly to customer needs.

Among them, the former demonstrates a more pronounced implication of deep binding with customers. It is reported thatFor existing product lines, Mehow will propose valuable solutions for product and process innovation based on strategic insights into products and technologies, thereby securing a first-mover advantage in next-generation product development while maintaining its current business operations.Thereby deepening business engagement with target customers and enhancing customer stickiness. This is what was previously mentioned as anticipating customers’ needs to the greatest extent possible.

Building on the collaborative relationship established through their existing product pipelines, Mehow can also wait for the right moment to seek opportunities to expand the scope of cooperation with target clients and diversify the range of collaborative products, thereby broadening the breadth of its business partnerships.

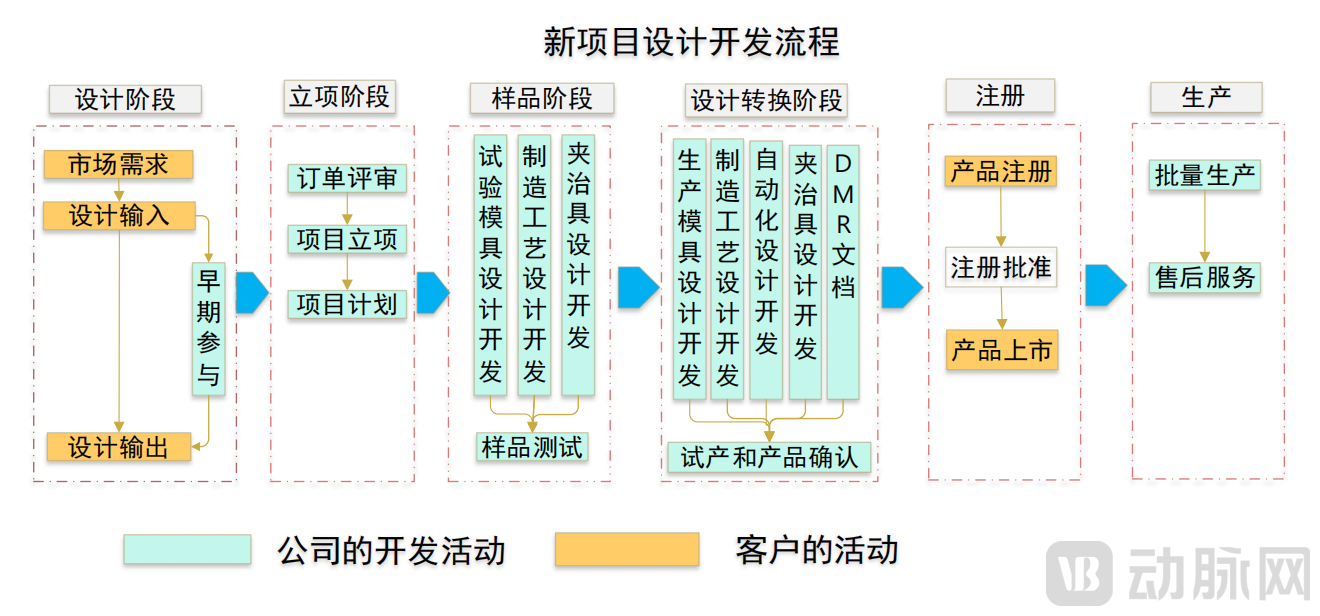

Furthermore,Mehow engages with target clients at a very early stage—entering during the project design phase and remaining involved throughout nearly the entire product development and commercialization lifecycle, including design, project initiation, sample testing, design transfer, mass production, and after-sales service.

Mehow: Medical Device Component and Product Design and Development Process (Excerpt from Mehow’s Prospectus)

Such deep involvement not only creates opportunities for collaboration but also enables Mehow to gain a deeper understanding of brand owners’ needs, thereby better meeting their requirements.

Furthermore, active participation from the project design phase facilitates the early identification and resolution of potential issues, thereby shortening the new product development cycle for brand owners and accelerating time-to-market. The value-added services provided by Mehow enhance brand owners’ “reliance” on the company, further solidifying the partnership and creating opportunities for new collaborations.

However, we must not overlook a fundamental fact: Mehow’s core business lies in the overseas expansion of components for home-use ventilators and cochlear implants, serving international giants in these respective fields. A key issue often highlighted in the global expansion of medical devices is the establishment of localized ecosystems in overseas markets.

While some domestic companies are still preparing to establish overseas production bases and even build their own sales networks, Mehow began its overseas localization ecosystem earlier and has achieved a relatively more mature stage, though its essence remains focused on meeting the needs of B-end clients.

As of now,Mehow has established four overseas subsidiaries—Mehow Hong Kong, Mehow Malaysia, Mehow Cayman, and Mehow Singapore—with a “coverage area” encompassing Singapore and Australia, which closely aligns with the operational regions of its key Customer A and key Customer B.

From an architectural perspective, the primary function of Mehow Hong Kong is the sales of components and mold products, while Mehow Malaysia mainly undertakes the production of ventilator components. Mehow Cayman and Mehow Singapore are also primarily engaged in the sales of medical device components. Therefore,Mehow’s overseas localization ecosystem is primarily centered on sales and production.

In its prospectus, Mehow Innovative Ltd. explicitly explainedReasons for Establishing a Production Base in Malaysia: Primarily to Enhance Service Quality and Deepen Customer Partnerships.

By establishing a production base in Malaysia, Mehow can communicate with customers more conveniently and efficiently, gaining early insights into their product development plans, R&D directions, and specific progress. This facilitates timely information exchange, enabling Mehow to secure collaboration opportunities and adjust its own R&D strategies accordingly, thereby enhancing the alignment between its capabilities and customer products.

Furthermore, establishing a production base in Malaysia helps shorten the product transportation radius, reduce transportation costs and time, lower the uncertainty of product delivery lead times, and effectively support customers’ supply chain and inventory management;

Meanwhile, the establishment of a production base in Malaysia also enables Mehow to promptly monitor after-sales product performance and receive feedback. By responding in a timely manner, the company can further delve into customer needs, thereby enhancing the breadth, depth, and closeness of its collaborations with clients and continuously strengthening these partnerships.

However, Mehow, which has been continuously deepening its partnerships with existing clients, is well aware of the principle that one should not put all eggs in one basket. Moreover, with its growing strength, Mehow also aspires to become a major player in the industry.

Over the past few years, Mehow has weathered the depreciation of the US dollar, rising raw material costs, and the COVID-19 pandemic, which is truly commendable. In reality, however, while most people have applauded Mehow’s achievements, some have also expressed skepticism.

In this article, we will not focus on the Sino-US trade friction or some common issues faced by OEM manufacturers, such as profit margins being constrained by both upstream and downstream sectors. Instead, we choose to explore a more critical issue—Mehow suffers from “big-client dependency.”

Admittedly, it is understandable that Mehow’s primary clients are among the global top 100 medical device companies. However, a cause for concern lies in Mehow’s significant dependence on a single customer.

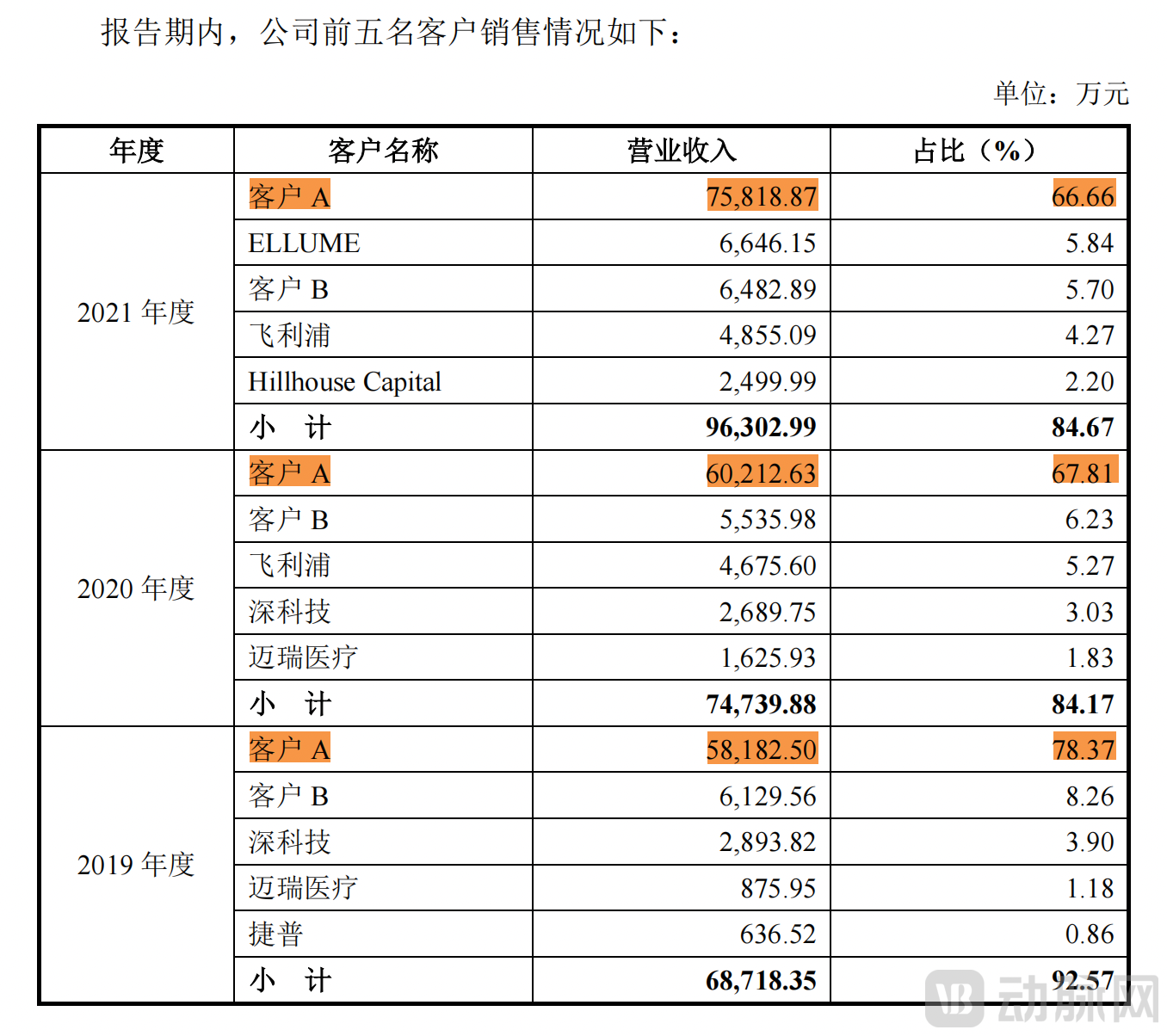

From 2019 to 2021, according to Mehow’s prospectus, the proportion of revenue derived directly and indirectly from Customer A was 82.27%, 70.84%, and 68.65%, respectively; in 2021, direct revenue from Customer A accounted for as high as 66.66%.

Excerpt from Mehow's Prospectus

The revenue share from Customer A is indeed declining, yet it remains as high as 66.66%. Furthermore, since the relevant data was not disclosed in the 2022 annual report, we are currently unable to verify whether this downward trend persists. (Note: While some perspectives suggest that the share is decreasing further, no definitive conclusion can be drawn as Mehow has not officially released the corresponding data.)

Mehow’s significant reliance on a single customer has also drawn inquiries from the Shenzhen Stock Exchange. In response,Mehow explained that its reliance on Customer A is primarily determined by the competitive landscape of the industry and the company’s strategic positioning. Given Customer A’s stable operational performance and the highly stable cooperative relationship between the two parties, Mehow asserted that its significant dependence on Customer A would not have a material adverse impact on its ability to continue as a going concern.

However,Some argue that the stable partnership claimed by Mehow may not be as stable as asserted.. The underlying reasons trace back to Client A.

Although Mehow referred to its largest customer as “A” in its prospectus, nearly all industry insiders knew exactly who “A” was—ResMed.

Why ResMed? This question has been addressed in numerous articles and will not be reiterated here. It suffices to note that ResMed, which held a 78.1% market share together with Philips Respironics in 2020, achieved record-high annual revenue of $3.6 billion in 2022 following the urgent recall of Philips Respironics ventilators in 2021. Furthermore, the company reported revenue of $1.03 billion in Q2 2023, representing a 16% year-over-year increase and underscoring its continued positive growth trajectory.

However, media reports have stated that while ResMed’s revenue increased by 13.44% in 2020 (with its home ventilator business also experiencing rapid growth), the proportion of Mehow’s sales derived from ResMed grew by only 3.11%. Furthermore, when ResMed surged in 2021, Mehow’s sales attributable to ResMed returned to normal levels.

While the exact circumstances remain unclear, some articles have speculated that ResMed has begun seeking partnerships with other suppliers, citing the company’s annual reports’ repeated emphasis on supply chain security issues. (Note: The so-called supply chain security issues faced by Mehow may stem from US-China trade frictions and the COVID-19 pandemic.)

These are the external pressures facing Mehow. Internally, Mehow is unwilling to remain confined by the OEM label and constrained by the dynamics of its upstream and downstream supply chain.

Therefore, Mehow is also seeking a broader and more expansive path for development.

Given the criticism over its heavy reliance on a single customer, Mehow has actively expanded its client base. It must be acknowledged that Mehow demonstrates robust capabilities in acquiring new customers—having secured partnerships with global top-100 medical device companies such as Johnson & Johnson, Abbott, Siemens, and Resound across various niche segments, with actual revenues ranging from tens of thousands to millions of yuan.

Meanwhile, Mehow is also actively expanding its product pipeline—from home ventilators and cochlear implants to monitoring, sterilization, and emergency care.

One point that warrants special attention is that the innovative development and manufacturing technologies previously mentioned by Mehow have established a platform advantage, which is applicable not only to the production of related medical device components but also to the manufacturing of related home and consumer electronics.

Therefore,Leveraging Mehow’s precision mold-making and liquid silicone rubber (LSR) technologies, the company has also expanded into the home appliance and consumer electronics sectors. Notably, Mehow has partnered with Philips on coffee maker components.

andTo shed its OEM label, Mehow has also launched its own brand, with spirometers as its main products.However, according to the data presented in Mehow’s prospectus, the revenue share from its proprietary products accounted for only 1.27% in 2021. Meanwhile, some argue that launching its own brand could lead to direct competition with downstream brand owners, thereby impacting its core business. This implies that Mehow’s path to shedding its reliance on contract manufacturing will be far from smooth and remains a long journey ahead.

The future remains to be seen. Mehow needs time to explore and validate its path, while we must patiently await the day when Mehow reaches new heights and its medical device exports truly bear fruit.