Hong Kong Biotech IPOs Show Signs of Recovery, Yet Market Differentiation Is Inevitable

Since the start of the interim reporting season for Hong Kong-listed stocks, Henlius, Harbour BioMed, and Akeso have successively delivered impressive results. Many biotech companies have made significant improvements in business development (BD) or commercialization, as well as in cost control and operational efficiency, approaching or reaching their profitability inflection points. Positive cash flow has boosted these companies’ stock prices and restored confidence in the Hong Kong biotech sector.

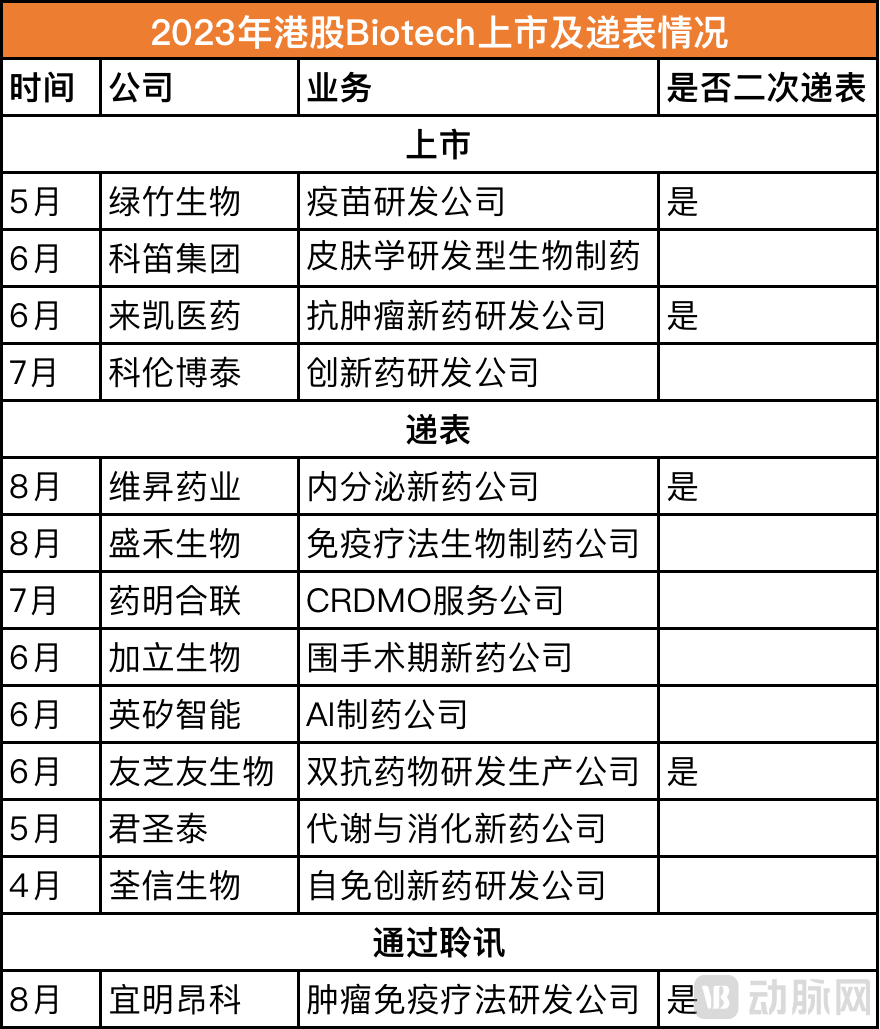

Biotech companies listing in Hong Kong also showed signs of recovery in the second quarter. Since April, Luye Biopharm, Cutia Therapeutics, Laekna Therapeutics, and Kelun-Biotech have gone public in succession; Yimingangke has passed the hearing, and eight other companies have filed their prospectuses.

Some biotech companies remain mired in difficulties, and investors struggle to identify subsequent positive signals from their financial reports and pipelines. Overall, the Hong Kong stock market is in a weak state: low trading volumes and poor liquidity have led to distorted stock prices. There are even reports that some investment institutions now include clauses in their contracts prohibiting portfolio companies from listing on the Hong Kong Stock Exchange.

The “adventure story” of Hong Kong-listed biotech companies will continue, but it will no longer be a “happy ending for all.”

Increasingly Competitive Application Submissions

Hong Kong’s biopharmaceutical IPO market experienced a prolonged stagnation: only five biopharmaceutical companies listed in Hong Kong in 2022, and after 3D Medicines went public in December, the Hong Kong stock exchange did not welcome another biopharmaceutical listing for an entire quarter.But after April this year, the Hong Kong stock market IPOs showed signs of recovery.

Several companies that have successfully gone public have avoided the predicament of their share prices falling below the IPO price. Kelun-Biotech is no exception; as the first pre-revenue biopharmaceutical company this year to pass the listing hearing upon its initial prospectus filing, it holds a substantial deal with Merck & Co. Its stock surged by nearly 6% at its peak on the first day of trading, and its current market capitalization has reached HK$17 billion.

Green Bamboo Biopharma’s stock price fell more than 30% on its first day of trading, but it quickly rebounded thereafter, reflecting market recognition of its fundamentals and growth prospects. Corti Pharma’s R&D and commercialization outlook remains uncertain; its shares dipped slightly after listing, but subsequently rose to trade above the IPO price. Laekna Therapeutics, which focuses on solid tumors, saw its share price surge by nearly 30% in the first two days of trading, demonstrating strong performance.

The companies filing for IPOs each boast impressive backgrounds. For instance, Quanxin Biologics is one of the few clinical-stage biotechnology companies in China fully dedicated to biologics for autoimmune and allergic diseases. Its founder, Qiu Jiwan, and co-founder, Dr. Yu Guoliang, are both prominent figures in the field of rabbit monoclonal antibody technology. Junshengtai focuses on metabolic diseases, the hottest therapeutic area this year, with its core candidate HTD1801 leading the way in the concurrent treatment of diabetes and liver disease. As a pioneer in AI-driven drug discovery, Insilico Medicine is poised to accelerate its IPO, leveraging the momentum of generative AI.

Each company’s prospectus reads like a narrative of the rise of a leader in its niche sector.

However, compared with the cluster of listings in 2021 and earlier years, competition among companies pursuing IPOs on the Hong Kong Stock Exchange has intensified significantly. The market subjects biopharmaceutical companies’ pipelines and technologies to rigorous scrutiny regarding their innovativeness and differentiated advantages, while also demanding outstanding commercialization and operational capabilities; otherwise, these companies will struggle to meet investors’ profitability expectations.

Amid the current climate of heightened uncertainty, the market prioritizes pipelines with high-certainty progress and tangible profitability. To make a significant impact, companies must secure headline-grabbing partnerships or report positive late-stage clinical results. Several Hong Kong-listed biotech firms that achieved profitability in the first half of this year have jointly driven this “turnaround wave,” each leveraging its unique strengths:

Henlius’s profitability is the most tangible, driven primarily by sales of products such as Hanquyou (trastuzumab), Hansizhuang (serplulimab), and Hanbeitai (bevacizumab), along with cost reduction and efficiency improvements. Akeso’s profitability stems mainly from the $500 million upfront payment from Summit Therapeutics; however, its robust product pipeline ensures strong future cash flows. Harbour BioMed’s profitability arises not only from license-out deals but also significantly from asset restructuring and adjustments to its management team.

Profitability reflects the normal progression of a company’s life cycle and is the most effective way to alleviate market concerns about the value of innovative drugs. Biotech companies are vying to demonstrate their profitability in order to secure more resources in an increasingly stringent environment.

However, profitability does not represent everything.An investor told VCBeat’s New Medicine channel, “At present, most Chapter 18A-listed pharmaceutical companies still rely on one-time gains from licensing deals or asset sales to achieve profitability, with very few cases of profits generated through the sale of self-developed products. Rather than short-term profitability, investors are more focused on product potential. As seen in the financial reports of companies like BeiGene, despite reporting losses, their investments are primarily directed toward R&D and innovation, reflecting a strong emphasis on long-term development and competitiveness.”

Hong Kong Biotech Stocks Diverge

Hong Kong stocks were once a favored destination for pre-profit biopharmaceutical companies, but in the past two years, the Hong Kong stock market has faced difficulties, with declining liquidity being one of the biggest issues.The average daily turnover rate has continued to decline, with more than 60% of Hong Kong-listed companies recording an average daily trading volume below HK$1 million. Meanwhile, the overall delisting rate in the Hong Kong stock market remains very low, and the absence of an effective merger and acquisition mechanism for eliminating underperforming firms has led to the fragmentation of limited trading capital across an excessive number of listed companies, thereby reducing individual stock liquidity.

The appeal of Hong Kong stocks to global investors was once a key driver behind the success of Chapter 18A companies. However, consecutive interest rate hikes by the Federal Reserve, the sluggish performance of the Hong Kong stock market, and broader environmental factors have eroded foreign investors’ confidence in generating profits from Hong Kong-listed equities. As mainland Chinese capital has stepped in to fill the void, differences in investment preferences compared to foreign investors have contributed to greater market volatility, thereby undermining the efficiency of resource allocation.

Overall, the Hong Kong stock market has remained weak year-to-date, with the Hang Seng Index declining by more than 10%. On August 18, the Hong Kong stock market entered a bear market, having fallen 21% from its peak at the beginning of the year. A bear market is defined as a decline of at least 20% from recent highs, a relatively rare signal indicating severe investor pessimism about the economy. The healthcare sector of Hong Kong stocks has performed even worse, dropping nearly 30%.

Based on this, some investors have stated that the improvement of Hong Kong stocks depends on two factors: on one hand, the strength of future policy support for Hong Kong stocks; on the other hand, whether there will be an injection of US dollars from regions such as the Middle East into Hong Kong stocks.

Amid such volatility, biopharmaceutical companies listed on the Hong Kong Stock Exchange appear riskier, prompting investors to seek “a sense of security” and demand proof of revenue-generating capabilities. Meanwhile, some companies benefited from the boom and associated conveniences of the Hong Kong stock market around 2021 but failed to translate this into actual revenue, thereby exhausting investor expectations.

Li Zhenxing, Managing Director at China Securitiesstated: “From the perspective of the capital market regulatory framework,It remains a consensus that the Hong Kong capital market is still the more direct and convenient choice for biopharmaceutical companies pursuing an IPO.“However, recent changes in Hong Kong’s capital market and the commercialization landscape for innovative drugs have affected investors’ valuation and exit considerations for companies at Series C or later stages, posing challenges for biopharmaceutical companies seeking listings on the Hong Kong Stock Exchange.”

In light of the current IPO environment,Managing Director, BlueRun VenturesRong JingIt is believed that: "For companies planning to go public within six months to a year, cash management is crucial.For some early-stage companies, it is advisable to remain undisturbed by the current environmental changes for the time being,“The key lies in successful project initiation and product development.”

Li Zhenxing also suggested that, given the inherent uncertainties in pharmaceutical R&D and the current state of the capital markets, biotech companies should fully leverage their core competencies and concentrate resources on their most promising pipelines to alleviate investor concerns about uncertainty.

He analyzes that the Federal Reserve’s slowing pace of interest rate hikes, or a potential halt, is positive for Hong Kong stocks. While there are some favorable short-term windows, a comprehensive recovery in the Hong Kong stock market will still take time. High-quality biopharmaceutical companies are expected to be more favored by investors.For instance, Kelun-Biotech’s decade-plus dedication to the ADC field, coupled with significant talent acquisition and capital investment, has yielded a robust pipeline. Its proprietary linker-payload technology became the key factor in securing its partnership with Merck & Co., while the company’s IPO served as a major boost to the Hong Kong healthcare sector this year.

The optimism toward companies such as Kelun-Biotech, along with the long-term bullish outlook on BeiGene and Innovent Biologics, suggests thatHong Kong stocks will move toward differentiation, including differentiation in commercialization:A cohort of companies has successfully crossed the break-even point in sales, with scaled revenue and stable profitability propelling them toward genuine commercial success. In contrast, companies unable to present a clear business model will find no market acceptance.

as well as the divergence in business value and operational proficiency:A distinct product pipeline, robust business development (BD) capabilities, and effective cost control have enabled some companies to stand out and mature into established biotech or biopharma enterprises.

And all of this will be reflected in the divergence of market capitalizations.“I believe that the divergence in the Hong Kong stock market will become increasingly pronounced. The market capitalization of some biopharmaceutical companies may remain below HK$2 billion, or even HK$1 billion, while others could surge to reach hundreds of billions of Hong Kong dollars,” said Rong Jing, offering his outlook on the future of Hong Kong-listed Biotech firms.