Reshaping the Biotech Investment Landscape Amid Capital Winter

The Capital Winter in the Biotech Sector Is Reshaping the Investment Landscape of the Capital Market.

Over the past decade, a surge of capital has flowed into biotech startups, ushering in a period of prosperity for the biotechnology sector.However, in 2023, venture capital investment in biopharmaceutical startups fell to its lowest level since 2016.

Many biotech companies are undergoing layoffs, shutting down, or filing for bankruptcy, but the risks are not confined to these startups. Angela Lee, Professor of Finance and Venture Capital at Columbia University, noted that some venture capital funds have yet to recoup significant returns from their prior investments, and it appears that everyone has consequently paused new fundraising activities.

STAT, a biotechnology media outlet, released its “2023 Ranking of Top Biotech Venture Capital Firms” report this month. The report evaluated 18 venture capital firms and revealed that approximately a dozen of them posted lower returns than the previous year, as capital exits became increasingly rare due to a lack of initial public offerings (IPOs) and only moderate levels of mergers and acquisitions (M&A). Venture capital funds are struggling to cope with the ongoing weakness in the capital markets.

Nevertheless, adversity has always presented an opportunity for industry reshaping, and the investment and financing landscape in the biotechnology sector is undergoing significant changes.

In China, the landscape of investment and financing is undergoing transformation. Local government funds have injected momentum to break the ice in biopharmaceutical industry financing, even playing a leading role in helping the sector recover. While representative investment firms such as Sequoia Capital and Hillhouse Capital have reduced their transaction frequency, they have firmly shifted their focus toward earlier-stage innovative projects.

Shifts in the investment and financing landscape are equally pronounced abroad. According to statistics from the biotechnology database Bay Bridge Bio, the share of traditional venture capital (VC) in the biotech sector is increasingly being encroached upon by emerging investment institutions, leading to a restructuring of the landscape across all funding rounds.The IPO market has begun to slow down, with reduced VC activity in crossover and Series B rounds. Changes in the downstream investment and financing environment have brought about the most significant shifts for Series A funding.

AWhat changes occurred in the funding round?

According to Bay Bridge Bio, the landscape for crossover and Series B financing has undergone significant changes as the pace of IPOs in the capital markets has slowed. Activity among crossover funds and mature biotech venture capital firms at the Series B stage has declined, while participation from other investors—including family offices, sovereign wealth funds, and European funds—has increased.

Changes in crossover and Series B financing have driven a restructuring of the Series A funding landscape,Single-stage Series A venture capital funds are beginning to face pressure from diversification trends, ceding market share to numerous VCs that previously focused on later-stage financing rounds.

Over the past decade, established biotech venture capital firms such as RA Capital, Atlas Venture, Versant Ventures, and Third Rock Ventures have captured the majority of investment share in the biotechnology sector. As representatives of both specialized biotech venture funds and crossover funds, they serve as the backbone of the biotechnology industry, securing substantial returns from well-functioning IPO markets.

Bay Bridge Bio analyzed the top biotech venture capital funds from 2018 to 2023. The data shows that over the past five years, Flagship, RA Capital, Orbimed, ARCH, and Versant have remained the most active investors. Meanwhile, they have also been the biggest beneficiaries of investment returns in recent years, with Flagship leading the pack at $7.7 billion in gains, followed closely by Orbimed and Viking Global.

However, after 2019, the COVID-19 pandemic plunged the market into turmoil, leading to a stagnation in the IPO market.These venture capital funds, which focus on late-stage investments, have begun to slow their pace of activity.During the Series A financing stage, only ARCH, Flagship, and Versant continued to actively deploy capital, remaining the most active funds during the COVID-19 pandemic. However, as downstream capital markets deteriorated, firms such as Third Rock Ventures and Atlas Venture steadily tightened their investment strategies. Once prominent on the rankings in 2018 and 2019, they have gradually faded from the list in recent years, with a declining number of Series A deals participated in.

This has created more opportunities for new investors, with a wave of emerging venture capital firms accelerating their expansion into the biotechnology sector and even ramping up their activities during the COVID-19 pandemic. It is certain that established VC firms are ceding market share to up-and-coming venture capital companies.

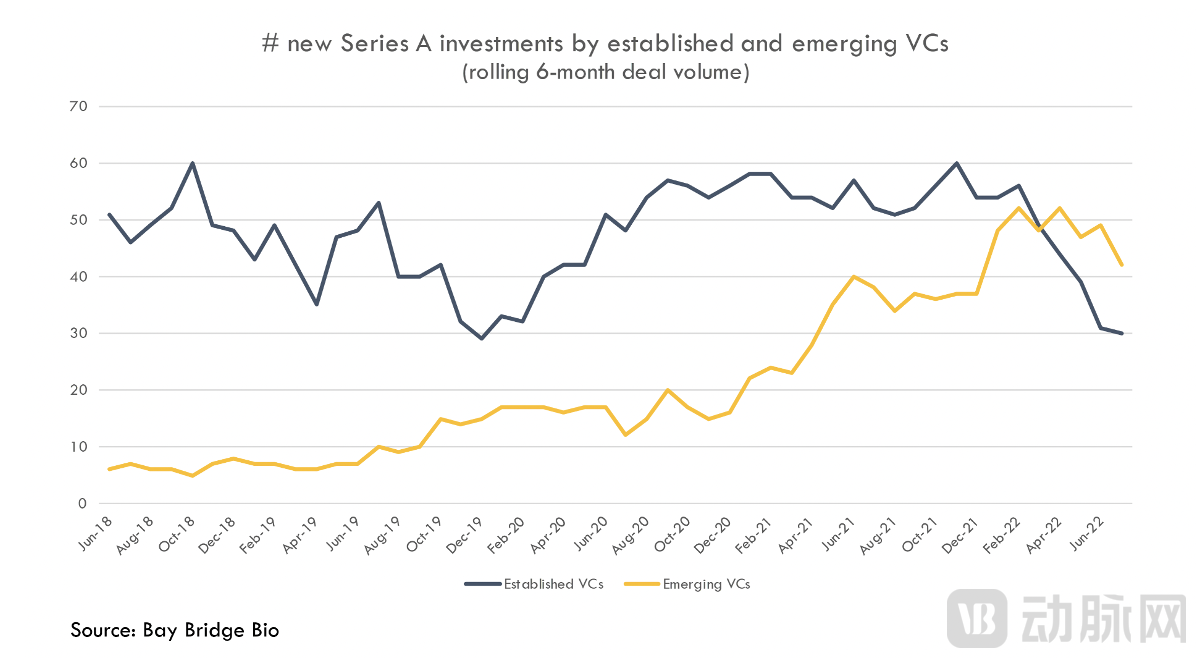

Performance of Established VCs and New Industry VCs in Series A Financing Rounds, Image Source: Bay Bridge Bio

The chart above shows Bay Bridge Bio’s statistics on the number of Series A financing deals involving established venture capital firms and emerging industry VCs. It can be seen that,Since the beginning of 2022, established venture capital (VC) firms have seen a continuous decline in their investment activity, while new VC firms have intensified their investment efforts, surpassing their established counterparts in the number of deals.

Who isANew Investment Star in This Round?

For over a decade, a handful of funds have dominated the Series A financing market.Since the influence on downstream investors is concentrated in these few funds, it means that if a biotech company does not appeal to this small group of investors, it will not secure financing, even if it has genuine potential.

And now, established U.S. biotech venture capital firms at the Series A financing stage are ceding ground to generalist technology investment institutions or TechBio venture capital firms.

In fact,The upstart VCs that have begun to capture the Series A investment share of established, veteran VCs are not necessarily “new” investors,Among them, some have been investing in biotechnology for years or even decades. These include cross-sector funds and venture capital arms of pharmaceutical companies. Historically, these VCs have concentrated their investments in either the seed stage or late-stage rounds, or have only occasionally invested in the biotech sector. Today, however, they are focusing their attention on Series A financing rounds.

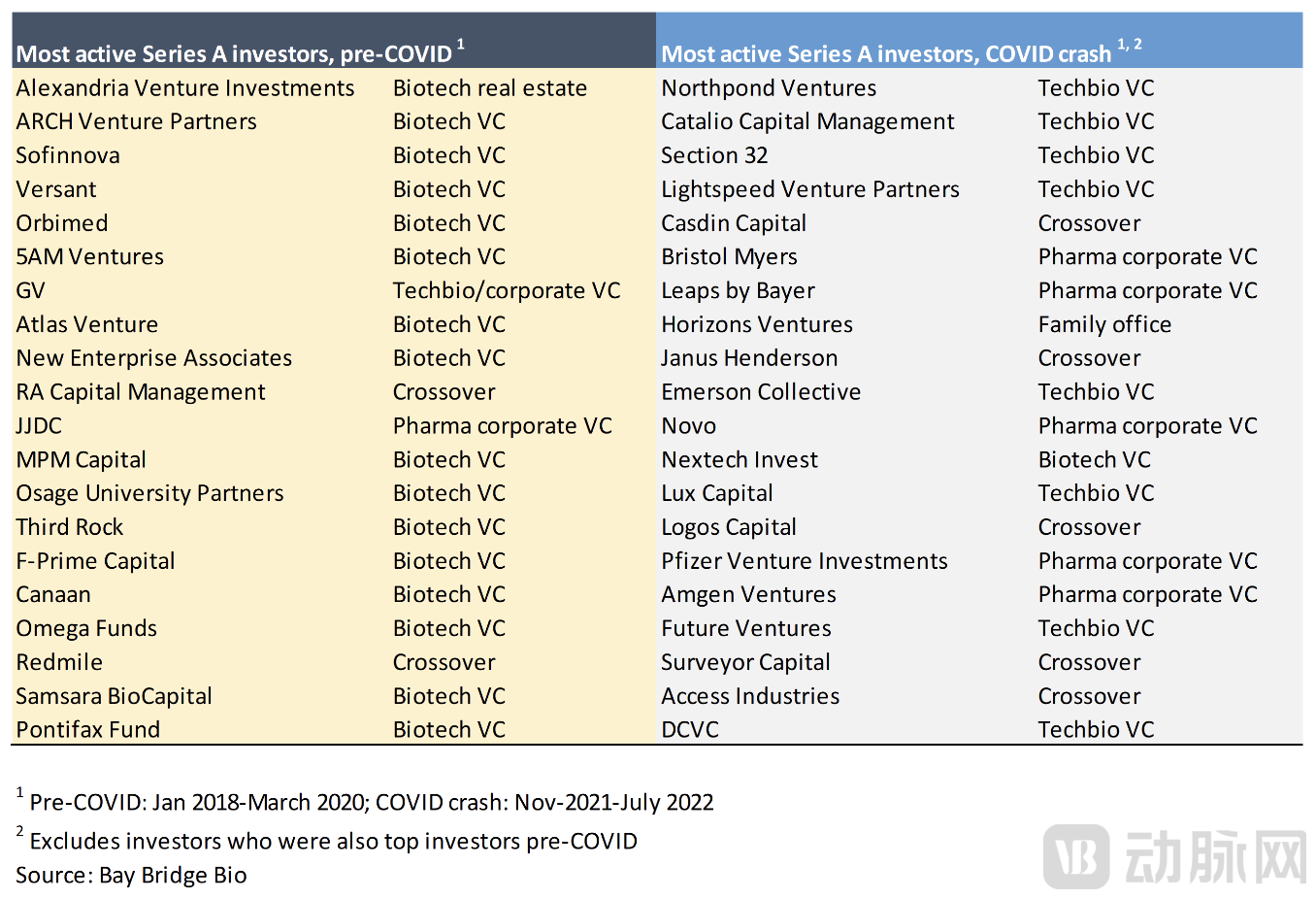

This trend has become even more pronounced, particularly in the period surrounding the COVID-19 pandemic. The figure below presents Bay Bridge Bio’s analysis of the most active investors in Series A financing before and after the pandemic, showing thatThe number of techbio venture capital firms, crossover funds, and MNC venture capital funds has grown significantly, with family offices even making an appearance.These new entrants that can adjust their investment strategies to adapt to Series A financing will have a significant advantage over investors who are slower to adapt to market differences.

The Most Active Investors in Series A Financing Before and After the COVID-19 Pandemic, Image Source: Bay Bridge Bio

Many newly established TechBio VC firms are beginning to emerge.For example, Catalio Capital Management, founded in 2020, has invested in 64 biotech companies within just three years and oversubscribed its third venture capital fund in 2022. Many of the portfolio companies were founded by Catalio Venture Partners, whose team comprises 36 world-renowned entrepreneurs from top academic institutions in the United States and Europe. Catalio’s investment strategy leverages this unique venture partner structure to identify breakthrough biotechnologies and provide proprietary investment opportunities for its portfolio companies.

Northpond Ventures, established in 2018, focuses on the commercialization of scientific and technological achievements. Its Northpond Labs is dedicated to supporting, funding, and engaging in early-stage scientific research at leading academic institutions such as Harvard University and the Massachusetts Institute of Technology (MIT), while Northpond Builds transforms research outcomes from Northpond Labs into startups suitable for further investment. The fund has invested in 72 companies.

Cross-sector funds are the backbone of the biotech financing ecosystem, capable of accelerating companies’ IPOs.Since the pandemic disrupted crossover deals, these investors have increasingly sought refuge in the Series A market. Some of them were already active in Series A financing rounds even before the pandemic.

During the COVID-19 pandemic, valuations of some biotech companies plummeted and their fundamentals deteriorated. In this context, crossover funds emerged, adopting a more market-centric approach by making investments based on downstream investors’ willingness to purchase and the companies’ fundamentals. This has provided crossover funds with an opportunity to solidify their position as upstream investors in the exit strategies of established venture capital firms.

In the Series A financing round, venture capital funds from multinational corporations (MNCs) such as BMS, Pfizer, and Novo Nordisk drew significant attention.Unlike crossover funds, these entities have been actively participating in Series A financing rounds for years. Their role extends beyond helping portfolio companies achieve financial targets; they are also tasked with advancing the strategic objectives of their parent companies. With the loss of exclusivity for key drugs, large pharmaceutical firms face substantial revenue declines in the coming years. Large-scale mergers and acquisitions (M&A), particularly those involving de-risked assets, have long been a common strategy to address this challenge. During periods of capital market downturn, these multinational corporation (MNC) venture capital funds can not only support the growth of early-stage biotech startups but also fulfill their own needs for pipeline expansion.

Notable Shift: Early-Stage Seed Rounds Are Becoming More Structured

Prior to 2018, there was no genuine seed-stage market in the biotechnology sector, and it attracted little attention from investors. Startups had few avenues to raise initial capital unless they were part of, or closely affiliated with, traditional venture capital firms. While some active family offices and angel investors did participate in seed-stage financing, the terms offered were generally unfavorable. The seed-stage funding ecosystem in the biotechnology field was underdeveloped.

In recent years, seed-stage financing in the biotechnology industry has experienced explosive growth, with dozens of new investors emerging. The funding ecosystem in the biotech sector is now more mature, attracting capital interest from founders of diverse backgrounds. Consequently, the value of seed-stage financing has gained greater recognition.

In 2022, Third Rock Ventures launched its sixth fund, raising $1.1 billion—the largest in the firm’s history—with the majority of the capital earmarked for Series A financing.

However, fund partner Reid Huber noted that one of the areas this fund focuses on is seed-stage financing. “We will consider focusing on and funding companies at the seed stage to help them mature their pipelines more than in the past, so that they can have a clearer product vision and value proposition for investors.”

Over the past year or two, the market has been unfriendly toward certain listed companies. Some of these companies have faced significant criticism for going public without a clear timeline for clinical trials or data releases.

Abbie Celniker, another partner at Third Rock, also noted, “We believe that the seed round is where true value is created, as it ensures that the company has secured a viable, off-the-shelf asset ready for clinical development.”

Providing support since the seed funding round has become a risk mitigation strategy for venture capital funds.