Fallen Star in Digital Health: Can M&A Rescue the Industry? — The Case of Babylon Health

AliHealth

Medical and Health Services Network Service Provider

Plummeting stock price, suspension of core business operations, asset divestitures... Since 2023, Babylon Health (hereinafter referred to as “Babylon”), a global star player in the internet healthcare sector, has been mired in continuous turmoil.

On August 31, Babylon announced the latest developments in the turmoil: After exploring strategic alternatives, most of the remaining assets of its UK business have been acquired by the US healthcare services company eMed.com.

In the past few years, Babylon has experienced a period of rapid growth, with its annual revenue increasing from $8 million in 2018 to $1.11 billion in 2022. In the first quarter of 2023, the company’s revenue continued to grow steadily, and it expects to achieve profitability by mid-2024.

Since 2023, following the peak years of growth, there have been reports in China of internet hospitals and online healthcare platforms being deregistered, transferred, or seeking mergers and acquisitions. A similar situation has emerged in the global market. What exactly is the problem?

Founded in the UK, Babylon has long been well-known within the industry. By the end of 2022, its three major business segments—value-based healthcare services, clinical services, and software licensing services—had expanded to cover 15 countries worldwide.

Babylon’s initial core business was in the United Kingdom. After entering the U.S. market in 2020, it experienced rapid growth and went public on the New York Stock Exchange in 2021 through a SPAC merger. Revenue from value-based care services in the United States has become Babylon’s core source of income.

Despite a surge in revenue, Babylon remained in the red. In its 2023 performance forecast, Babylon projected that revenue for the new year would remain close to 2022 levels, at approximately $1.11 billion, and anticipated achieving profitability by mid-2024.

However, a series of incidents occurred in 2023.

In May, Babylon announced its privatization and restructuring, causing its stock price to plummet from $7 to $0.50.

In August, Babylon failed to release its audited financial results for the second quarter of 2023 on schedule. Instead, it disclosed several significant developments: the previously planned merger with MindMaze has been terminated; its U.S. company and operations are being shut down; it is seeking to sell its UK business; and the sale of Meritage Medical Network (its IPA business), which began in October 2022, is still ongoing.

By August 31, progress was made on one of the divestitures, with eMed.com, a U.S. healthcare services company, acquiring most of Babylon’s remaining assets in its UK business.

In fact, Babylon has been striving to secure financing for its business in recent months, ultimately forcing it to sell assets and shut down its core operations.

A review of Babylon’s development history reveals that the primary drivers of its current situation lie in the capital markets and the business itself.

Since going public via a SPAC, Babylon’s share price has remained depressed, even falling below $1, which has impaired its ability to raise capital.

In terms of business operations, Babylon’s primary revenue source over the past three years has been value-based care services. The company’s revenue grew from the tens of millions of dollars to over $1 billion, a growth trajectory significantly supported by contributions from its value-based care services.

In 2020, 2021, and 2022, Babylon’s revenue from value-based care services amounted to US$26 million, US$219 million, and US$1.026 billion, accounting for 32.9%, 68.2%, and 92.5% of its total revenue, respectively.

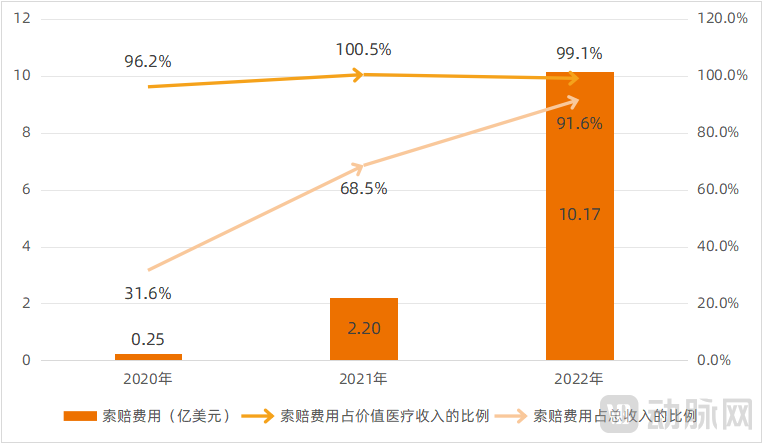

However, high revenue also came with enormous costs. In Babylon’s cost structure, claims expenses accounted for the largest share, even those paid to third-party institutions (for medical services provided to Babylon members).Cost. Babylon strengthens chronic disease management for its members through proactive, preventive care, keeping them healthy and avoiding unnecessary emergency visits and hospitalizations. Only by reducing medical service costs to a certain level can it achieve profitability through the “surplus” from membership fees.

Babylon's Claims Expenses and Their Proportion of Revenue, Source: Babylon Financial Reports

Since 2020, Babylon’s claims costs as a percentage of value-based care service revenue have ranged from 96.2% to 100.5%, while their share of total company revenue has continued to climb, reaching 91.6% in 2022. In the first quarter of 2023, claims costs remained persistently high, accounting for 99% of value-based care service revenue and 91.3% of total revenue.

The company also incurs a range of costs, including clinical nursing expenses, platform and application fees, and R&D expenditures. Overall, it has nearly fallen into a situation where the larger its business grows, the greater its losses become.

Persistent massive losses and limited fundraising capacity were insufficient to sustain further deficits, ultimately leading to the predicament faced by Babylon.

Coincidentally, a similar situation has also emerged in China’s internet healthcare industry.

Recently, VCBeat in the “A Wave of Cancellations and Transfers Is Here—Why Are People Still Flocking to Launch Internet Hospitals?” article, an analysis was conducted on the current status of license cancellation and transfer. However, licenses primarily focus on service qualifications. Currently, many enterprises obtain licenses to generate synergy with their core businesses; when the core business is adjusted, the qualifications may also change accordingly. In the future, the cancellation or transfer of licenses may even become a norm.

What requires in-depth analysis at present is the current state of internet healthcare platforms.

In 2023, internet healthcare platforms in China reported news of layoffs, business line reductions or adjustments, and even sought mergers and acquisitions, including both comprehensive and specialized platforms.

China’s healthcare service delivery system, payment mechanisms, and public healthcare-seeking behaviors differ significantly from those in the UK and the US. Although the industry landscape appears similar, the underlying drivers are markedly different.

Across the industry, with the exception of a few internet healthcare companies in China that have achieved profitability, most are still exploring viable business models. For these enterprises, financial difficulties or slow business progress are primarily attributable to numerous internal challenges.

For example, the business model is singular, focusing primarily on either online medical services or pharmaceutical sales.

Demand for medical services is low-frequency and uncertain. Although the volume of online medical services has grown significantly over the past three years, a portion of this growth represents only temporary demand. Over a longer term, while the number of online medical users is indeed on an upward trend, the low-frequency nature of demand remains an inherent characteristic that cannot be overcome.

Therefore, if a company’s revenue is primarily derived from medical service-related income (such as consultation fee sharing and platform usage fees tied to medical services), it will be difficult to rapidly achieve large-scale revenue through average transaction value and service volume alone.

Some platforms also rely on post-consultation medication sales as their primary revenue source. However, if a platform has limited scale, its competitiveness in terms of drug pricing and delivery speed is likewise constrained. Coupled with the low gross profit margins of pharmaceuticals, major e-commerce platforms can only achieve a certain level of profitability by leveraging substantial sales volumes. For platforms with limited sales volume, it is difficult to scale up profits.

Meanwhile, enterprises exhibit a high reliance on financing and weak self-sustaining capabilities.

In recent years, internet healthcare was the darling of capital, with frequent large-scale financing rounds. For technology research and development and business expansion, cost investment is inevitable.

In recent years, portfolio companies have actively expanded their markets, with some even pursuing excellence in physician or user services. However, due to the aforementioned issue of a single-source revenue structure, these companies suffer from weak self-sustaining capabilities and limited cash flow. Consequently, when investors seek exit, the companies’ existing funds are insufficient to repurchase equity.

When companies adjust their business strategies under external pressure, the effects may not be immediately apparent.

Typically, one of the strategies for companies facing difficulties is to compress or adjust their business operations. However, internet healthcare has been explored for many years, and each business line was not built overnight. Adjusting the direction will naturally have little immediate effect, especially when a company has been moving in its original direction for too long.

Meanwhile, business adjustments require the deployment of a robust execution team; failure to recruit a sufficiently strong team may result in weak implementation outcomes, even if the strategic direction is correct.

From a broader perspective, the challenges posed by environmental issues within certain industries have also contributed to corporate distress.

Firstly,The absence of robust payers—characterized by weak willingness to pay among individual consumers, a B2B market still in its incubation phase, and limited coverage under public health insurance—represents the most significant difference between China’s internet healthcare sector and that of the United States.

The public’s strong preference for consulting specialists and renowned physicians makes it difficult to charge them significantly higher fees than those for offline visits with general practitioners, and also hinders their willingness to pay for preventive and management services. Currently, drug sales remain the primary source of scalable revenue in the consumer (C-end) market.

The B2B market primarily consists of insurance companies and large enterprises that purchase medical and health services for their customers or employees. However, due to limitations such as corporate health management concepts, cost and budget constraints, and the level of acceptance of internet-based medical services, market education is still ongoing.

Medical insurance was once one of the payers on which the industry pinned high hopes. Over the past three years, medical insurance payment has indeed rapidly expanded in public internet hospitals, but support for third-party internet healthcare platforms remains extremely limited. Furthermore, reimbursement for internet healthcare services covers only outpatient medical and pharmaceutical expenses, which are significantly smaller in overall scale compared to inpatient costs. Consequently, medical insurance payments are unlikely to generate substantial revenue.

Secondly,In the past, internet healthcare ventures attracted primarily financial investments, with very little strategic investment, leaving portfolio companies to “fight alone.”

Round after round of investment—scaling up the business—exit via IPO: this is the ideal pathway for investing in internet healthcare. However, given that the penetration of internet technologies into the healthcare sector is significantly more challenging than in other industries, the realization of this ideal may be compromised.

As previously mentioned, the major challenges facing payers are a reality that cannot be reversed in the short term. To explore more diversified business models and identify payers with sufficient willingness to pay, internet healthcare platforms require greater strategic synergy, which has been lacking in past investments. Previously, synergy was primarily reflected in traffic diversion—integrating consultation portals of portfolio companies into internet platforms—which has had limited impact on resolving fundamental issues.

Of course, everything has two sides. The challenges faced by enterprises and industries do not mean that their value should be completely denied.

Opportunities always favor those who are prepared. Pioneers crossed the river by feeling the stones, while latecomers contributed their efforts to build bridges together. The healthcare industry had already accumulated a certain foundation before 2020, which enabled it to demonstrate its value during special periods and gain recognition and strong support from government authorities. In the medical field, where policy guidance plays an extremely powerful role, policy support is a fundamental prerequisite. Nowadays, nearly all programmatic documents related to medical services mention support for “Internet+” medical services.

At the same time, over these years, enterprises have been expanding their reach to doctors and attracting patients one by one, thereby allowing more people to recognize internet healthcare.

The number of online healthcare users has been steadily rising in recent years. By the end of 2022, the user base reached 363 million, accounting for 34.0% of all internet users in China. Among the top 100 hospitals nationwide, most have launched internet-based medical services, enabling high-quality medical resources to be better distributed to regions beyond first- and second-tier cities.

From a corporate perspective, some companies have achieved notable success in physician appeal, user recognition, brand influence, and operational systems. In the short term, even with internal operational gaps, the impact on patient and physician perceptions is minimal, allowing services to continue nearly as normal.

Recently, media reports have indicated that a major internet conglomerate has submitted a bid to acquire a well-known internet healthcare platform. Over the past decade, internet healthcare has been a key area of strategic interest for major tech companies. From the perspectives of traffic integration, strategic synergy, and financial strength, these large internet firms are indeed ideal potential acquirers.

Currently, achieving business continuity through mergers and acquisitions may be the optimal solution for both enterprises and investors. For the industry, this approach preserves resources accumulated over many years, preventing prior efforts from being wasted.

Collaboration between major internet companies and internet healthcare platforms can generate synergies across multiple dimensions.

First, the integration of doctor-patient resources, particularly the supplementation of physician resources.

In recent years, internet healthcare platforms of various sizes have emerged in large numbers, intensifying the competition for physician resources. Given physicians’ limited capacity, the number of online consultation apps they use is also constrained. A survey conducted by VCBeat’s Eggshell Research Institute in its “2022 Internet Hospital Report” found that as many as 71.5% of internet-based physicians used only one to three platforms, with merely 11.1% practicing on more than four platforms.

Factors such as the number and quality of users, compliance of diagnostic and treatment processes and content, social influence, and user experience are all decisive factors for physicians when choosing to join a platform.

Major internet companies excel in consumer-side customer acquisition and operations, but serving physicians entails higher barriers to entry and requires long-term efforts to build reputation among them. Therefore, if these tech giants directly enter the internet healthcare sector, they may encounter obstacles at the most fundamental level—physician resources. A platform that has been operating for many years and boasts a large pool of high-quality physicians can largely compensate for this shortfall.

Meanwhile, constrained by the low-frequency nature of healthcare service demand, the conversion rate from public internet traffic to digital health services remains low, indicating that traditional consumer-internet monetization models are ineffective in the healthcare sector. In contrast, digital health platforms have long attracted patients through a “physician-referral” model, thereby acquiring more precise traffic with genuine healthcare needs, which serves as a valuable supplement for major tech companies.

Second, integrate customer channels to explore diverse commercialization pathways.

In the process of expanding payer channels, it is difficult to achieve breakthroughs in consumer willingness to pay and comprehensive opening of medical insurance in the short term, and they may not necessarily become the main payers in the long run. Therefore, B-side entities have become the most likely targets for developing stable payment sources.

Health management services, which account for 20% of health insurance products, along with corporate health management services, both represent market opportunities worth hundreds of billions of yuan. With their diverse business lines, major internet companies can leverage the nearly mature product ecosystems of their internet healthcare platforms to identify and meet the growing needs of B-end clients.

Third, data synergy to unlock the value of healthcare data.

For a long time, healthcare data has been a sensitive topic within the industry. Of course, data security should always remain a central theme for the sector. Historically, this sensitivity stemmed primarily from issues surrounding data ownership rights and lawful usage.

In 2022, the Central Committee of the Communist Party of China and the State Council issued the “Opinions on Building a Basic Data Institution to Better Leverage the Role of Data as a Factor of Production,” proposing to advance the implementation of mechanisms for confirming rights and authorizing the use of public data. Through various benefit-sharing models such as dividends and royalties, these measures aim to balance and coordinate the distribution of interests among stakeholders involved in different stages, including data collection, processing, circulation, and application.

With top-level design serving as the foundational framework, the extraction of value from medical and health data has become significantly more certain. For major internet companies, which possess both comprehensive consumer-side (C-end) data and precise clinical visit records, there are greater possibilities for unlocking the value of medical and health data.

Among the current major internet tech giants, which one is most likely to acquire an internet healthcare company? To answer this, we must examine each company’s existing strategies and business operations.

Both Alibaba and JD.com, the two e-commerce giants, have established independent internet healthcare platforms and are publicly listed companies.Meanwhile, the two tech giants exhibit strong synergies in traffic and logistics between their comprehensive retail and pharmaceutical retail operations, while pharmaceutical retail further aligns with healthcare services. Currently,Healthcare service revenue accounts for a relatively small proportion of total revenue for both companies; however, both have designated it as a core business segment, with particular emphasis on expanding specialized medical services.AliHealth had previously acquired Xiaolu TCM to complete its traditional Chinese medicine service segment.

Baidu and Tencent have been highly active in the healthcare sector. For instance, Baidu has invested in Health Road and Weimai, and incubated the health management platform “Baidu Health.” Its business spans five major scenarios: health science popularization services, online consultation services, health e-commerce services, internet hospital services, and digital disease-specific alliances.Baidu Health is currently focusing on offline hospital partnerships, online disease-specific management, and digital marketing.

Tencent has invested in platforms such as Dingxiang Yuan, WeDoctor, Medlinker, and Haodf Online, and established its own Hainan Tencent Internet Hospital. However, data released by the Health Commission of Hainan Province indicates that the volume of self-operated online services remains relatively low.Tencent has not been heavily involved in the direct operation of internet healthcare services. Instead, it has focused its efforts in the medical sector on technology enablement, such as the research and development of products like medical AI and smart healthcare solutions, as well as the opening of its technological ecosystem.

ByteDance has been highly active in the healthcare sector over the past two years, pursuing a dual strategy of direct involvement and investment., it successively established Xiaohe Health and its affiliated internet hospital, invested in the online mental health platform Haoxinqing, and acquired the women’s and children’s healthcare provider Amcare and the oncology care provider Hongda Airui. Having entered both online and offline medical service sectors, its business model has become increasingly asset-heavy.

Given that ByteDance’s two major platforms, Douyin and Toutiao, host a vast amount of medical and health-related content, they have generated substantial traffic, offering significant opportunities for deeper value extraction. However, the healthcare service sector is highly specialized. On the supply side, physicians cannot engage in “live-streamed e-commerce” as seen in other industries, and online consultations and diagnostic activities are subject to strict regulations. On the demand side, converting short-video traffic into monetizable healthcare services is far from straightforward. In summary,ByteDance is strongly committed to healthcare services, but it must still break through the high barriers in the medical sector to better integrate them with its existing traffic advantages.

As a short-video platform, Kuaishou has maintained a relatively light footprint in the medical services sector. In addition to integrating health education videos and health consultation features within its platform, Kuaishou previously established offline clinics and announced plans in 2021 to build online medical service brands named “Xiaoyu” and “Qingchan.” However, public information indicates that these initiatives have made minimal progress.

Meituan is also one of the major tech companies that has made significant inroads into the healthcare services sector in recent years; however, overall,Meituan’s strategy primarily focuses on building a platform ecosystem, with an emphasis on connecting various stakeholders.For example, Meituan’s home-delivery business connects offline pharmacies with internet hospitals, creating an end-to-end service flow from medical consultation to medication dispensing within the “Meituan Medicine” section. Meanwhile, its in-store business links offline dental clinics, ophthalmology centers, and other healthcare providers, empowering merchants through a digital platform and helping users identify suitable institutions. Although Meituan has also established its own internet hospitals and large-scale pharmacies, its strong focus on local life services necessitates a vast and diverse network of service providers across China to meet local user demand. Therefore, platform-based operations remain the mainstream approach.

In summary,Large tech companies seeking to deepen and strengthen their presence in the healthcare services sector, particularly where there is a significant gap in their online medical service offerings, are most likely to acquire a mature internet healthcare platform.

Certainly, other internet healthcare companies with strong revenue performance may also pursue strategic acquisitions.In general, any enterprise that creates value for its users and society deserves respect. Seeking the optimal solution to break through current challenges is also the pathway for enterprises to continue realizing their own value in the future.