Divergent Growth Trajectories Among China's Ophthalmic Device Leaders: Market Logic Across Four Key Segments

Autek China

Rigid Gas-Permeable Contact Lens Manufacturer

Haohai Biological Technology

Medical Biomaterials R&D and Manufacturer

Gaush Meditech

Ophthalmic Medical Device and Product R&D Manufacturer

In the first half of 2023, ophthalmology-related stocks surged. This was driven by a rapid recovery in ophthalmic diagnosis and treatment volumes following the relaxation of pandemic controls, leading to across-the-board business growth for relevant companies.

For example,Cataract Segment, the relevant revenues of Aier Eye Hospital, Huaxia Eye Hospital, Purui Eye Hospital, and He's Eye Hospital increased by 60.3%, 44.89%, 137.04%, and 76.1% year-on-year, respectively;Refractive Services Market, Aier Eye Hospital, Huaxia Eye Hospital, Purui Eye Hospital, and He's Eye Hospital saw their respective revenues increase year-on-year by 17.1%, 13.84%, 33.37%, and 18.23%;Optometry Business Segment, Aier Eye Hospital, Huaxia Eye Hospital, Purui Eye Hospital, and He's Eye Hospital saw their respective revenues increase by 30.5%, 17.75%, 52.87%, and 17.48% year-on-year.

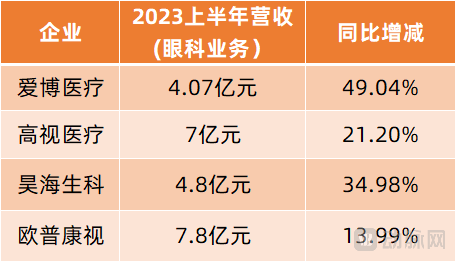

As downstream markets such as ophthalmic surgery and eyewear fitting continue to boom, upstream companies specializing in ophthalmic devices and consumables have also seen a significant surge in revenue. Ophthalmic medical device manufacturers, including Autek China, Gaush Meditech, Haohai Biological Technology, and iCare Medical, all achieved rapid growth in the first half of the year.

Among them, Aierbo Medical reported H1 2023 revenue of RMB 407 million, a year-on-year increase of 49.04%, making it the fastest-growing listed ophthalmic device company in China during the first half of the year. Autek China posted H1 revenue of RMB 780 million, up 13.99% year on year, and had the highest ophthalmic business revenue among the four major listed ophthalmic device companies.

It is worth noting that although all segments of the ophthalmic device industry achieved growth compared to the same period, different segments exhibited varying growth trends.

For example, in the first half of the year, the growth rate of cataract surgery volume among listed ophthalmic medical service companies in China ranged from 45% to 137%, driving a leapfrog increase in cataract-related products such as intraocular lenses; the growth rate of optometry services ranged from 17% to 50%, promoting rapid growth in related optometric products; and the growth rate of refractive services ranged from 13% to 33%, leading to steady growth in refractive-related products.

What specific changes have occurred in each market segment of ophthalmic devices? How has the competitive landscape shifted within these segments? How will the market evolve in the future? In response to these questions, we have identified partial answers through interviews and a review of companies’ semi-annual reports.

Currently, cataracts are the leading cause of blindness worldwide, and surgical implantation of intraocular lenses is the only effective treatment for cataracts.

In the first half of 2023, benefiting from the increase in cataract surgery volume, the intraocular lens products of Aier Medical, Gaush Meditech, and Haohai Biological Technology all achieved year-on-year growth of 30%-58%.

According to the financial reports of various companies, Aier Medical’s intraocular lens (IOL) products generated RMB 245 million in revenue in the first half of the year, a year-on-year increase of 37.88%. Among this, overseas IOL revenue grew by 115.75% year on year. Haohai Biological Technology’s cataract product line achieved approximately RMB 260 million in revenue during the same period, up 55.2% year on year. Within this business segment, its IOL products contributed RMB 203 million in revenue, representing a 58.15% year-on-year growth. Gaush Meditech’s proprietary IOL products recorded RMB 162 million in revenue in the first half of the year, a 30.3% increase compared to the same period last year.

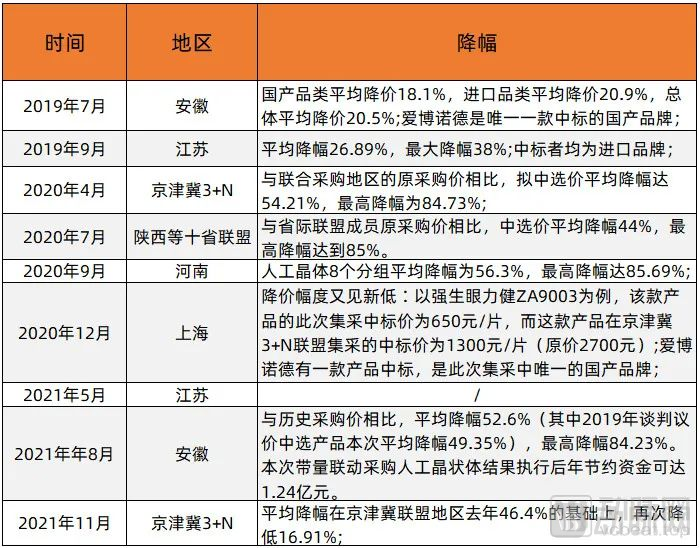

The significant surge in intraocular lens product revenue for the aforementioned three companies is attributable not only to increased surgical volumes but also to volume-based procurement.

Since July 2019, nearly all provinces and municipalities across China have implemented (or participated in) volume-based procurement (VBP) for intraocular lens (IOL) products. For instance, the Shaanxi-led Ten-Province Alliance launched IOL VBP in July 2020, achieving an average price reduction of 44%, with a maximum reduction of 85%. The Sichuan Provincial Healthcare Security Administration completed the implementation of IOL VBP in March 2022, resulting in an average price reduction of 43% and a maximum reduction of 78%. In February 2023, Shanghai publicized the proposed winning bids for IOL VBP: the non-toric, spherical, non-preloaded group saw an average price reduction of approximately 36%; the non-toric, spherical, preloaded group decreased by approximately 9.63%; and the non-toric, aspheric, non-preloaded group experienced a price reduction of approximately 33%.

In successive volume-based procurement programs for intraocular lenses (IOLs), domestically produced IOLs have achieved breakthroughs from zero to one, with an increasing number of manufacturers securing winning bids. Meanwhile, domestic companies such as Aibotech Medical, Gaush Meditech, and Haohai Biological Technology have rapidly gained market share and earned recognition from clinicians for their IOL products following the implementation of volume-based procurement, leveraging advantages in product performance, distribution channels, and cost efficiency.

Aier Medical stated in its semi-annual report: “With the implementation of centralized procurement, the company’s intraocular lenses (IOLs) have gained greater popularity than imported IOLs in China’s ophthalmic surgery market and are expected to maintain rapid growth in the short term. In addition, the existing distribution channels established through centralized procurement, along with extensive hospital-side resources, have laid a solid foundation for the commercialization of the company’s upcoming new functional IOLs and phakic intraocular lens products.”

The revenue from domestically produced intraocular lenses has surged, as Chinese companies have broken the monopoly held by international manufacturers in high-end intraocular lens technology and the market, launching domestic high-end intraocular lens products.

Previously, domestic companies mainly produced and sold mid- to low-end products such as monofocal aspheric intraocular lenses (IOLs), rigid IOLs, and spherical IOLs, with the high-end market monopolized by international manufacturers. Nowadays, domestic companies have successively launched functional IOLs, including toric and toric multifocal models, achieving a comprehensive product portfolio covering the high-, mid-, and low-end markets.

For example, Aier Medical provides spherical and aspheric monofocal intraocular lenses (IOLs) for basic cataract surgery, as well as functional IOLs (including multifocal IOLs). Meanwhile, its “Pronote” brand offers a range of preloaded IOLs, providing a more convenient surgical experience for both doctors and patients.

Haohai Biological Technology offers a comprehensive portfolio of intraocular lenses (IOLs), ranging from mass-market foldable monofocal IOLs to high-end foldable premium functional IOLs. Notably, the sales volume of its high-end refractive multifocal IOL product, SBL-3, increased by 169% year-on-year in the first half of 2023.

As domestic companies launch high-end products,The domestic market for intraocular lenses in China is expected to see an accelerated increase in the localization rate. Chinese-made intraocular lenses will even be exported globally, making inroads into overseas markets., with Aier Medical's overseas revenue from intraocular lenses increasing by 115.75% year-on-year, a growth rate higher than that in the domestic market.

Furthermore, with policy support,The intraocular lens business revenue of relevant domestic enterprises is expected to continue maintaining high-speed growth.The National Health Commission’s “14th Five-Year National Eye Health Plan (2021–2025)” proposes that, by 2025, China should strive to achieve a cataract surgical rate of over 3,500 per million population, with a continuous increase in the effective cataract surgical coverage rate. The rapid rise in cataract surgery penetration will drive high-speed growth in the intraocular lens market.

Orthokeratology Lenses Are an Effective Method for Myopia Control. Clinical studies have demonstrated that long-term wear of orthokeratology lenses can reduce or eliminate peripheral hyperopic defocus, slow axial elongation, and significantly retard the progression of myopia.

In the first half of 2023, the growth rates of orthokeratology (OK lens) businesses varied across companies, with significant disparities observed.

Among them, Aiboyi Medical’s orthokeratology lens sales maintained this momentum in the first half of this year following a significant surge over the past three years, achieving RMB 105 million in revenue, a year-on-year increase of 38.97%. Aiboyi Medical expects this trend to continue in the coming years.

Autek China, the first manufacturer in mainland China to receive a product registration certificate for orthokeratology lenses from the NMPA, reported H1 revenue of RMB 380 million for its rigid gas permeable contact lenses, representing a year-on-year increase of 10.88%. The growth was primarily driven by the continued upward trajectory in the adoption of orthokeratology lenses.

Haohai Biological Technology’s ophthalmic end-user products include orthokeratology lenses and accompanying lubricating eye drops, functional spectacle lenses, and the Yijing phakic posterior chamber refractive lens (PRL), among others. In the first half of the year, revenue from its ophthalmic end-user product business reached RMB 95.68 million, a year-on-year increase of 11.31%, primarily driven by growth in its orthokeratology lens business.

Compared with the 30%-58% growth of intraocular lenses, the growth rate of orthokeratology lenses was 10.8%-39%.

On the one hand, although the overall market for orthokeratology lenses is expanding, the number of market participants is also increasing, leading to gradually intensifying competition and resulting in varying revenue growth rates among companies. A search on the official website of the National Medical Products Administration (NMPA) using the keyword “orthokeratology” reveals that nine rigid gas permeable contact lenses for orthokeratology from nine enterprises have been approved, with the majority of approvals granted in 2022 and 2023.

On the other hand, not only has the number of competitors in the orthokeratology lens industry increased, but orthokeratology lenses themselves have also faced new competitive alternatives.. Previously, orthokeratology lenses were an important means of myopia control and were widely used for myopia prevention and management in adolescents. Currently, the more popular products on the marketDefocus Lenses, and also contributes to myopia prevention and control.

According to reports, defocus lenses are not classified as medical devices, and marketing regulations are relatively lenient. With optical retail stores serving as the primary distribution channel due to their large number, some myopic children have chosen defocus spectacle lenses as a corrective tool. Currently, key players in the defocus lens market include optical lens manufacturers such as Essilor, Zeiss, Hoya, and Aier Medical.

Aibo Medical's first-half financial report shows that revenue from its vision care products, including defocus lenses, contact lenses, and contact lens care solutions, reached RMB 45.32 million, a year-on-year increase of 402.84%.

According to reports, standard-designed spectacle lenses for myopia can only correct refractive errors in the central retinal area, while peripheral retinal images are focused behind the retina, resulting in hyperopic defocus. Studies have shown that this hyperopic defocus is one of the causes of axial elongation. For every 1 mm increase in axial length, myopia progresses by 3.00 diopters.

Defocus lenses can slow down the elongation of the axial length.. After wearing defocus lenses, the lenses not only provide clear correction for central vision but also feature a lower optical power in the peripheral zones compared to the central area. This design projects images onto the peripheral retina or in front of it, thereby reducing hyperopic defocus and helping to slow the progression of myopia. Clinical data show that,Defocus lenses have an efficacy rate of approximately 30% in controlling myopia.。

Currently, industry giants such as Aier Medical and Haohai Biological Technology have begun to promote and sell defocus lenses, whileWith the large-scale commercialization of defocus lenses, the growth rate of orthokeratology lenses, also used for myopia control and prevention, has been forced to slow down.。

Meanwhile, unlike orthokeratology lenses, which must be fitted at medical institutions, defocus lenses can be directly fitted at the vast number of optical stores. Furthermore, while orthokeratology lenses are classified as Class III medical devices, defocus lenses do not fall under the category of medical devices, resulting in less stringent regulations on marketing and promotion.

This may allow defocus lenses, which hold advantages in distribution channels and marketing, to capture a larger user base and squeeze the market share of orthokeratology lenses, even though orthokeratology lenses achieve a myopia control rate of 40%–60%, outperforming defocus lenses.

However, overall,。

It is worth noting that some domestic ophthalmic device manufacturers are currently accelerating their challenge to imported brands, further promoting the substitution of domestically produced products in the ophthalmic device market.

For example, among the OCT devices listed on public hospital procurement platforms in 2022, a total of 485 units were awarded through bidding, including 209 units from domestic brands, 258 units from imported brands, and 18 units with untraceable origins. Among the 467 ophthalmic OCT products with traceable sources, domestic brands accounted for 45%, approaching half, indicating a clear trend of domestic substitution.

However, the ophthalmic laser equipment market in China remains dominated by imported brands. In the ophthalmic laser therapeutic equipment market, there were 71 bid-winning records in the first half of 2023, with Zeiss, Iridex, and VisionStar ranking as the top three, accounting for 47.7%, 11.9%, and 10.8% of the total bid-winning amount, respectively. In the ophthalmic laser diagnostic equipment market, there were 65 bid-winning records in the first half of 2023, with Optos, Heidelberg Engineering, and Nidek ranking as the top three, accounting for 53.1%, 45.2%, and 1.7% of the total bid-winning amount, respectively. (Data source: Medical Device Data Cloud)

In the first half of the year, listed ophthalmic device companies adopted diverse market strategies aligned with their respective strategic needs: Aiboy Medical entered the consumer market; Autek China acquired downstream ophthalmic medical institutions; Haohai Biological Technology integrated its entire industry chain; and Gaush Meditech increased the revenue share of its proprietary products.

Among them, Aier Medical has expanded its portfolio of consumer-grade products through acquisitions, including colored contact lenses, clear contact lenses, and spectacle lenses.Gradually Expanding into the Vision Care Consumer Market. From a financial perspective, contact lenses, contact lens care products, etc.Vision care products saw the highest year-on-year growth in the first half of the year, reaching 402.84%., delivering substantial returns to Aier Medical.

Currently, Aier Eye Hospital Group remains highly optimistic about the vision care consumer market and is ramping up production capacity for products such as contact lenses to meet customer order demands. Meanwhile, in July 2023, Aier Eye Hospital Group signed an agreement to acquire a 51% equity stake in Fujian Younikang Optical Co., Ltd. Upon completion of the acquisition, this move will further enrich Aier Eye Hospital Group’s contact lens product portfolio and accelerate its strategic layout in the contact lens sector.

Unlike Aier Medical, which has heavily bet on contact lenses,Autek China Chooses to Enter the Downstream Ophthalmic Medical Institution Market. In June 2023, Autek China acquired partial equity interests in 13 controlling subsidiaries and sub-subsidiaries for RMB 506 million in cash, among which Kunming Shikang Ophthalmic Clinic Co., Ltd., Shenzhen Mingmou Ruishi Ophthalmic Clinic, and Xiantao Jiashi Ophthalmic Outpatient Department Co., Ltd. are ophthalmic medical institutions. Upon completion of the acquisition, Autek China will hold, either individually or jointly with its subsidiaries, a 90% equity stake in these controlling subsidiaries and sub-subsidiaries.

As of the end of June, Autek China had gained controlling interests in 61 ophthalmic medical institutions, including Anhui Medical University Kangshi Eye Hospital Co., Ltd. and Xuancheng Kangshi Eye Hospital Co., Ltd., through mergers, acquisitions, and equity investments, along with over 360 optometry service terminals.

Autek China continues to expand its downstream ophthalmic medical institutions.. In July 2023, its wholly-owned subsidiary, “Autek Investment,” invested RMB 22.44 million in Fengxian Huaming Ophthalmic Hospital Co., Ltd. Upon completion of this investment, Autek Investment will hold a 51% equity stake in Fengxian Huaming Hospital.

Haohai Biological Technology has initially completed its full industry chain layout for intraocular lens products.Through its subsidiary Contamac, Haohai Biological Technology has integrated the upstream raw material production segment of the intraocular lens (IOL) industry chain; through its subsidiaries Aaren, Henan Universe, and Saimeshi, it has mastered the R&D and manufacturing processes for hydrophilic and hydrophobic IOL products; and through Shenzhen New Industry’s specialized marketing platform for high-value ophthalmic consumables, Haohai Biological Technology has strengthened the downstream sales channels for its IOL products.

It is reported that Contamac, a subsidiary of Haohai Biological Technology, is one of the world’s largest independent manufacturers of ophthalmic materials. It supplies raw materials for ophthalmic products, such as intraocular lenses and orthokeratology lenses, to customers in more than 70 countries and regions worldwide. In the first half of the year, Contamac’s ophthalmic materials business generated revenue of RMB 110 million, a year-on-year increase of 42.21%, primarily driven by the recovery of global production and operations, as well as the continued expansion of high-oxygen-permeability materials and other products in international markets such as the United States.

Gaush Meditech focuses on increasing the revenue share of its proprietary productsIn the first half of 2023, Gaush Meditech's revenue from proprietary products reached RMB 190 million, a year-on-year increase of 36.5%; revenue from distributed products amounted to approximately RMB 400 million, representing a year-on-year growth of 17.9%.

Currently, Gaush Meditech has made significant investments in the research and development of intraocular lenses, orthokeratology (OK) lenses, rigid gas permeable contact lenses, ophthalmic surgical consumables, electrodiagnostic equipment and associated consumables, ophthalmic surgical knives, and optometric devices.

Gaush Meditech’s semi-annual report indicates that its intraocular lens (IOL) R&D is expected to sequentially obtain registration certificates starting in the fourth quarter of 2024; clinical trials for its orthokeratology (OK) lens project have been initiated; the first batch of prototypes for the electroretinography (ERG) equipment R&D project has been completed; the autorefractor has entered the registration phase; and core technological breakthroughs have been achieved for the optical biometer, with prototype assembly and debugging underway... With continued investment in R&D, Gaush Meditech’s portfolio of proprietary products is projected to become increasingly diverse.

Overall, the four major listed ophthalmic device companies hold differing perspectives on China’s ophthalmic device industry and have adopted distinct strategies based on their respective considerations. Despite these strategic differences, it is foreseeable that all four companies will maintain high growth rates against the backdrop of the rapidly expanding domestic ophthalmic market, gradually overcome technical challenges in high-end ophthalmic devices, and increase the localization rate of China’s ophthalmic device market.