Shenzhen Capital Group: A 24-Year-Old State-Backed VC Powerhouse with Nearly 200 Pharma Bets Sets the Benchmark for Local Government Investors

BGI

Scientific and Technological Service Provider and Precision Medical Service Operator

Yuanhua Tech

Medical Robot Developer

SCGC

Investment Institutions in Innovative Fields

Mindray

Medical Device R&D Manufacturer

August 25, 2023, marked the exact 24th anniversary of the founding of SCGC.

On this day, SCGC publicly announced two major updates: first, it unveiled its historical performance record. As of July 31, 2023, SCGC managed a total asset base of RMB 446.6 billion across various funds, had invested in 1,420 companies with a cumulative investment amount of RMB 97.7 billion, and had exited from 531 portfolio companies, among which 259 had been listed on 17 capital markets worldwide; second, it announced75 Portfolio Companies Have Collectively Completed Signing and Will Officially Settle in Shenzhen。

The release of these two pieces of news quickly attracted attention from the venture capital and private equity community. This interest stems not only from SCGC’s extensive influence as a leading RMB-denominated fund, but also from its industry-guiding role as a pioneer among local state-owned assets. Particularly against the backdrop of the growing importance of local state-owned capital in the capital markets, every move by SCGC has become even more noteworthy, making research into its activities increasingly significant.

But where should the story begin?

Twenty-Four Years of Turbulence

Strictly speaking, SCGC is still a product of the last century.

In March 1998, with the opening of China's ChiNext market“Proposal on Drawing from Foreign Experience to Accelerate the Development of China’s Venture Capital Industry” (also known as “Proposal No. 1”)Officially announced. As one of the cities designated for the launch of the ChiNext board, Shenzhen responded promptly and prepared to host the first National High-Tech Fair in October 1999, aiming to seize the initiative. However, at that time, there was no trace of venture capital activity in Shenzhen. Consequently, the Shenzhen Municipal Government quickly formed a preparatory team and began intensive planning to establish the city’s first local venture capital firm, appointing Zhuang Xinyi as the project leader.

The preparatory work was no easy task. At that time, Guangdong International Trust and Investment Corporation (GITIC) was in dire straits due to blind investment and the failure of multiple projects. Therefore, Shenzhen municipal leaders explicitly stated their desire to avoid establishing a venture capital institution with a “bureaucratic style.” As a result, identifying a lead executive adept at market-oriented operations became Zhuang Xinyi’s top priority.

Coincidentally, Shanghai was also in the process of planning to establish a state-owned asset management company and intended to inviteKan Zhidong, One of the “Three Titans” of Shanghai’s Securities IndustryAppointed as the person in charge. Upon learning this information, Zhuang Xinyi took the initiative to retrieve Kan Zhidong’s personnel file from Shenzhen Development Bank. After further communication and negotiations with Shanghai, he swiftly brought Kan Zhidong to Shenzhen. On August 26, 1999, the inaugural meeting was held at the Wuzhou Hotel, establishing the company under the name Shenzhen Innovation Technology Investment Co., Ltd., with Kan Zhidong serving as President.

Upon assuming office, to rapidly gain in-depth insight into the venture capital industry and earn market trust,Kan Zhidong innovatively proposed the “One Step Away” enterprise model, which is now known as the Pre-IPO model.By investing in 23 Shenzhen-based companies prioritized for listing on the ChiNext Board and the top three enterprises nationwide receiving key support from various provinces and municipalities for ChiNext listings, SCGC rapidly placed bets on dozens of companies that were “one step away” from going public. In 2001, it successfully facilitated the Hong Kong IPOs of three companies—Yisheng Technology, Zhongda International, and Guoxun International—propelling SCGC to sudden prominence.

But the good times did not last long. As SCGC deviated from its core venture capital business, its profitability model was widely questioned by the industry at that time. Meanwhile, the bursting of the internet bubble and the continuous fermentation of multiple stock market scandals also contributed to the situation.The launch of the ChiNext board was put on hold at the end of 2001, leaving domestic venture capital firms with their exit channels suspended in mid-air., SCGC, which was established for the ChiNext board, consequently endured "hard times."

It was also at this time that Kan Zhidong chose to return to the securities industry, his long-cherished field. He accepted an emergency appointment to take over Southern Securities, departed from SCGC, which he had built from the ground up, and recommended a former university professorChen Wei Takes Over as President. After Chen Wei assumed office, he had few opportunities to make a significant impact, as SCGC was then facing difficulties: the industry’s outlook was uncertain, exits from existing investments were proving difficult, and most of the wealth-management funds entrusted to securities firms had turned into bad debts due to across-the-board losses in the securities sector. Thus, for Chen Wei, there was no choice but to hold fast in the dark.

However, the anticipated relief failed to materialize. By 2004, SCGC was on the verge of collapse. It is reported that although its registered capital stood at RMB 1.6 billion, its outstanding entrusted wealth management funds amounted to approximately RMB 1.6 billion. Nevertheless, the Shenzhen Municipal Government did not abandon the firm; it soon identified what would later becomeJin Haitao, revered in the industry as the “Southern Emperor”, making him the third head of SCGC since its establishment.

After Jin Haitao assumed office, he steered SCGC back to its core investment business. Although the company still faced the challenge of substantial funds being tied up in entrusted wealth management products with securities firms,Jin Haitao opted to invest by securing bank loans and partnering with government-guided funds through a new model., in addition, regarding the selection of specific targets, Jin Haitao proposed a "wolf-like" strategy for domestic venture capital, namelyCultivate a keen sense of smell; when encountering truly promising projects and opportunities, do not hesitate due to external factors, but dare to compete with foreign VCs for deals.. Following this investment logic, SCGC has made significant investments since 2006, with the number of investments increasing year by year.

Finally, on October 30, 2009, the ChiNext Board, dubbed “China’s Nasdaq” and crafted by the China Securities Regulatory Commission (CSRC) over a decade, was officially launched.Among the first 28 companies listed on the board, SCGC accounted for four.. One year later, SCGC made significant strides forward,A total of 26 portfolio companies have gone public, setting a world record for the highest number of IPO exits in a single year within the global industry.。

However, five years later, as Jin Haitao had exceeded the age of 60, he had to comply with the organizational decision to officially retire, leaving SCGC after 11 years of service and passing the baton toCurrent Chairman: Ni Zewang. At this point, SCGC had already become a diversified comprehensive financial group spanning venture capital funds, public mutual funds, funds of funds (FOFs), and real estate funds.

Tuwei Medical

In November 2017, at a public forum, Ni Zewang stated that,Not Investing in Tencent: SCGC’s Greatest Regret. This is a long story.

According to official data, by June 2018, SCGC’s assets under management had cumulatively reached RMB 296.357 billion. However, this did not create a significant gap with its peers; indeed, in the “Top 50 Chinese Venture Capital Firms” list released by Zero2IPO that year,SCGC ranks only fourth, with the top three being Sequoia, IDG, and Morningside.This disparity arose because SCGC missed out on Tencent, a "golden son-in-law."

It is reported that Tencent is one of the listed companies with the fastest market capitalization growth. When it went public in 2005, Tencent’s market cap was approximately $1.5 billion; by 2017, it had surpassed $400 billion, representing a more than 200-fold increase over 12 years. In fact, as a Shenzhen-based company, Tencent had reached out to SCGC (Shenzhen Capital Group Co., Ltd.) on multiple occasions, proactively seeking financing. However, SCGC declined these opportunities at the time, citing an inability to understand Tencent’s business model.

Having missed out on Tencent’s wave of internet growth, SCGC has also faced industry criticism for failing to adapt in time as investment hotspots shifted from traditional industries to the internet sector, instead sticking to its conventional logic of investing in traditional sectors. However, some hold a different view, believing thatAs a state-owned capital entity, SCGC is inherently more inclined to invest in high-tech manufacturing, demonstrating a strong preference for technological innovation while naturally lacking sufficient acumen for business model innovation.。

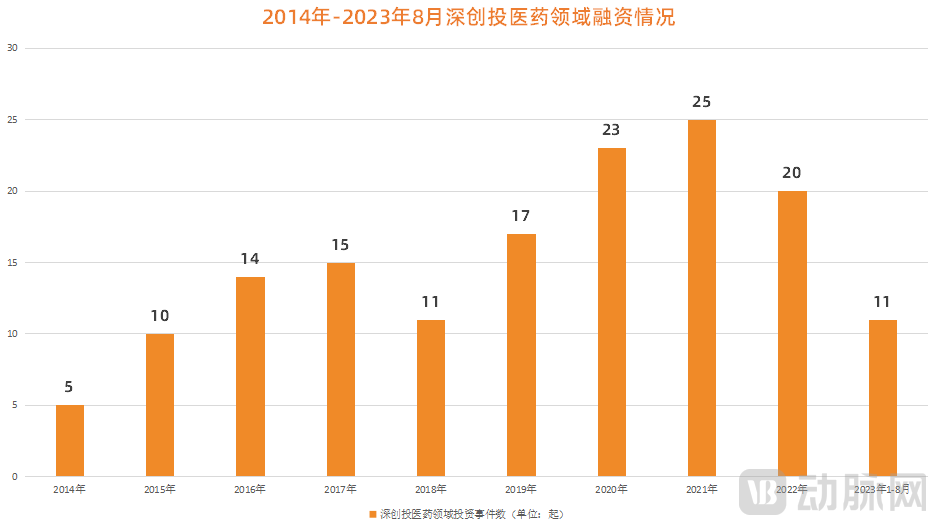

Figure 1. SCGC’s Financing Activities in the Pharmaceutical Sector from 2014 to August 2023 (Source: VCBeat)

It is precisely for this reason that, after Ni Zewang assumed office, SCGC began to focus its investment attention more on the pharmaceutical sector, which was gradually gaining momentum in the domestic market. According to incomplete statistics from the VCBeat Orange Database,Between 2015 and 2016, SCGC completed a total of 24 financing deals in the pharmaceutical sector, with its investment volume roughly equaling the sum of the previous years.. It is also worth mentioning that Mindray, Pumen Technology, Akeso, YHLO, and Joint Pharma, which were listed subsequently, were also successfully identified during this period.

However, SCGC’s true entry point into the pharmaceutical and healthcare sector was in 2018. In that year,SCGC Hongtu Healthcare Industry Fund Officially Launched: First Healthcare-Focused Fund Under SCGC’s “Specialization” Strategy, a Ph.D. in Medicinal Chemistry from Peking University with extensive investment experience in the pharmaceutical and healthcare sectorsZhou YiServes as the General Manager of the fund. In addition, the core team also includesYi Hongxiangincluding multiple professional investors in the pharmaceutical and healthcare sectors.

In other words, at this stage, SCGC had already achieved specialization in the field of pharmaceutical investment. So, how exactly did SCGC structure its layout?

First, in terms of overall investment logic, SCGC continues to adhere to the strategy of “investing early, investing in small businesses, and investing in innovation.”. According to incomplete statistics from the Artery Orange database, among the 79 financing deals completed by SCGC in the pharmaceutical sector from 2019 to August 2023,The proportion before Series A reached 40%.. In terms of specific niche sector selection, SCGC focuses its strategic investments onInnovative DrugsandMedical DevicesTwo Core Sectors: It is reported that over the past five years, more than 95% of SCGC’s investments in the pharmaceutical sector have been concentrated in these areas.

There are certainly reasons behind this. From the perspective of the entire pharmaceutical industry, as the process of domestic substitution deepens, original innovative technologies have become a key industry keyword, and this trend is becoming increasingly pronounced over time. From SCGC’s own perspective, as a local state-owned enterprise, it naturally has strategic considerations; therefore, it needs to make early investments in frontier technologies. Even if such investments fail, they can still contribute to industrial accumulation in the local region.

From an investment perspective, industry experts note that while early-stage pharmaceutical projects carry high risks, the overall fund returns are secured if just one or two projects succeed. Furthermore, the overall return on investment for late-stage projects in the pharmaceutical sector is gradually declining, and Shenzhen holds no significant advantage in investing in such late-stage ventures.

In a 2021 interview, Zhou Yi, General Manager of SCGC’s Healthcare Industry Fund, outlined its strategy for selecting niche sectors, “First, we aim to invest in differentiated sectors., such as ophthalmology, orthopedics, dermatology, and the central nervous system. These fields currently attract relatively little attention, yet they face substantial market demand;Second, we aim to invest in companies with a richer product pipeline., such as those that can achieve strong synergy between in-house R&D and License-in;Third, it is essential to establish a presence on emerging technology platforms., such as gene therapy, cell therapy, and nucleic acid drugs. In the field of biotechnology, areas including gene editing, synthetic biology, and gene therapy will continue to receive close attention.”

Based on SCGC’s investments in the pharmaceutical sector over the past two years, it has largely followed this logic in its strategic focus. For instance, in the field of gene therapy, SCGC has invested in more than a dozen companies, including Jinlan Gene and Huihe Biopharma.

Having discussed our focus areas and investment strategies, let us now turn to SCGC’s operational model in the pharmaceutical investment sector. As is well known, SCGC once operated against a backdrop of capital constraints.Jin Haitao innovatively proposed the model of government guidance funds and established China’s first government-guided venture capital fund in Suzhou in 2007., with a total scale of RMB 300 million. It is worth mentioning that Yuanhe Holdings, which later played a decisive role in Suzhou’s pharmaceutical industry, was also established in the same year.

According to industry veterans, government-guided funds have not only addressed the shortage of SCGC’s own capital but also enabled SCGC to leverage its government backing to secure prime access to local deal flow. Consequently, SCGC has adopted this investment model in the pharmaceutical and healthcare sector. Incomplete statistics show that over 65% of the companies SCGC has invested in within this sector over the past five years are based outside Shenzhen, with a primary concentration in Beijing, Shanghai, and Jiangsu Province.

Of course, SCGC has not forgotten its original mission. As a local state-owned enterprise,SCGC has invested in nearly 40 local pharmaceutical companies in Shenzhen over the past five years., and has also successfully facilitated the public listings of domestic pharmaceutical and medical enterprises such as BGI Genomics, Mindray, Chipscreen Biosciences, Pumen Technology, Winner Medical, YHLO, Breo, and Yiju Medical.

Breaking the Definition

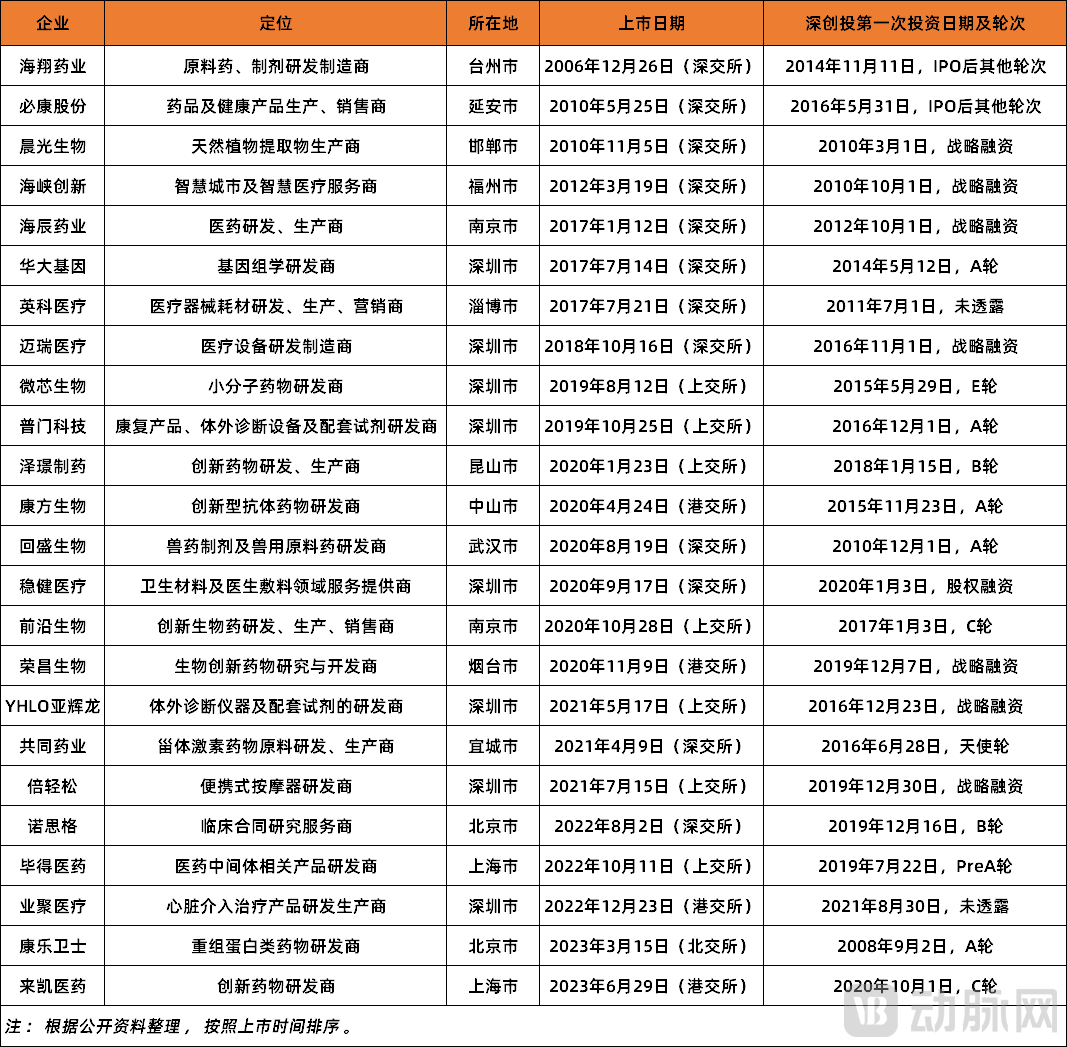

According to incomplete statistics from VCBeat,As of August 31, 2023, SCGC had invested in nearly 200 companies in the pharmaceutical sector and successfully facilitated the public listing of 24 pharmaceutical enterprises.. Behind the glamour, what exactly did SCGC do right?

Figure 2. Listed companies in the pharmaceutical sector invested by SCGC (Source: Public information)

Figure 2. Listed companies in the pharmaceutical sector invested by SCGC (Source: Public information)

First, excel at identifying cutting-edge projects, avoid following trends, and consistently maintain your own investment pace.. The essence of venture capital is value investment, which involves using capital to identify companies with genuine innovation capabilities and market potential. SCGC recognized this early on,Established the first postdoctoral workstation in China's venture capital industry as early as 2003., conducts in-depth research on cutting-edge technologies and related sectors, and selects leading companies from these sectors to provide references for the company’s investment decisions. According to data as of the end of 2021, the SCGC Postdoctoral Workstation had 62 postdoctoral researchers who had completed their programs and 35 currently enrolled, making it the most important think tank and vital force within SCGC.

It was revealed that in the past year or two,The recruitment efforts for postdoctoral workstations have significantly intensified, particularly with the introduction of a cohort of clinicians who have long been working on the front lines., with the aim of identifying more potential projects that not only meet clinical needs but also feature disruptive technologies.

Secondly, it features a flexible investment mechanism that breaks through the inherent constraints of the state-owned asset system.. In previous surveys, many industry veterans considered SCGC’s greatest advantage to be its mature and flexible mechanism for fundraising, investment, management, and exit. For instance, at the decision-making level, SCGC has established a specialized investment team in the pharmaceutical sector, which eliminates cumbersome review processes and avoids multi-layered approvals at the group level. Moreover, final investment decisions are not left to “laypersons” but are fully managed by professional teams.

This point is crucial. During the research, a senior industry expert told VCBeat, “If local state-owned capital lacks a mature mechanism, requiring every project to undergo a lengthy review process, it will be difficult to advance to the next stage, regardless of the abundance of resources or the amount of funding provided.”

Third, it leverages the governmental advantages of state-owned capital while simultaneously accommodating the innovative nature of market capital.. In fact, the biggest difference between state-owned capital and market capital lies in the government endorsement behind state-owned capital. SCGC has made good use of this advantage, for example, by creatively pioneering the government guidance fund business and establishing a series of regional funds under the name “Hongtu” (Red Soil). Specifically, supported by government resource channels, SCGC has been able to build a vast fund management network across China in a low-cost and fast-paced manner.

Yet on the other hand, SCGC has firmly grasped the essence of venture capital, namelyFully Respect Market Principles, which is reflected not only in the selection of portfolio companies but also in its mechanisms; for instance, regarding incentives, it aligns with market practices to address the challenge of talent attrition.SCGC upgraded its initial “2+8” incentive mechanism to “4+10” at an early stage., meanwhile, in the newly established commercialization fund, SCGC has also begun to implement an equity ownership plan for its management team and core key personnel, aiming to keep pace with market trends.

The final point is to integrate industrial chain resources by connecting upstream and downstream sectors within the relevant fields.. In an interview, Zhou Yi discussed SCGC’s value-added services for its portfolio companies: “We previously invested in Yuanhua Tech, which primarily develops orthopedic surgical robots. Leveraging our extensive network of portfolio companies, we facilitated collaborations with other orthopedics-focused firms in our investment portfolio during Yuanhua Tech’s clinical trials.”This is one of SCGC’s strengths: it can foster synergies among its portfolio companies by leveraging existing resources, while also building complete industrial chains anchored by “chain leader” enterprises.

However, this is only one component. As SCGC’s personnel, investments, and managed funds reached a certain scale, the firm began to emphasize achieving refined management through informatization, thereby ensuring the long-term development of its portfolio companies.

Obviously, SCGC was not built in a day, nor were these advantages formed overnight. The most critical factor is that behind SCGC stands a team of professionals with sufficient risk-taking spirit. As early as the inaugural meeting, Kan Zhidong established three fundamental principles with the Shenzhen municipal leadership:No forced personnel appointments, no forced project assignments, market-oriented operations, ensuring that SCGC could be born and grow in a favorable environment.

Throughout its subsequent long journey of growth, although SCGC occasionally took detours and felt constrained due to its state-owned background, it consistently broke through conventional models via innovation. This enabled SCGC to stay ahead of the industry time and again, naturally granting it a privileged view of the sector’s landscape.

More Than Just Big

In VCBeat’s previous surveys of local state-owned assets across various regions, many institutions openly hailed SCGC as the gold standard, but in factSCGC also has its own “idol,” namely the U.S. “King of PE,” BlackShi. In fact, SCGC’s decision to name its government-guided funds “Hongtu” is a true reflection of its benchmarking against Blackstone.

Between 2015 and 2016, in addition to increasing its investments in the pharmaceutical sector, SCGC was also considering how to further enhance its brand influence. During this period, SCGC turned its attention to Blackstone and embarked on a path of diversified development, namelyCentered on venture capital operations, expand into upstream and downstream segments of the venture capital industry chain or pursue related diversified businesses, including M&A funds, S funds, real estate funds, and public mutual funds.。

It is precisely for this reason that SCGC has been able to rapidly grow into the king of domestic VC. But SCGC does not stop there; it continues to explore more of its own potential.

For instance, in the sector of government-guided funds, SCGC is actively exploring the “Government-Guided Sub-Fund 2.0 Model,” namelyAt the fund level, we are exploring the removal of geographic restrictions on investments made by local government capital, thereby permitting nationwide investment; at the reinvestment level, we are deepening cooperation by leveraging the resources of the entire SCGC group rather than individual funds to assist local governments in conducting targeted investment promotion tailored to local conditions, thus covering their capital contributions and fulfilling reinvestment obligations.。

On the other hand,SCGC Has Also Extended the Reach of Government Guidance Funds to County-Level Cities, SCGC has currently established government guidance funds with local governments in Kunshan and Gaoyou in Jiangsu Province, as well as Huaining in Anhui Province. In addition,SCGC is also extending its investment reach into some less developed regions., such as Xinjiang and Heilongjiang. It is reported that SCGC’s funds under management currently cover 25 provinces and autonomous regions across China.

But this is not enough, against the backdrop of RMB-denominated funds beginning to become the absolute mainstay,SCGC’s Next Goal Is to Become a Top-Tier Global Investment Group. Therefore, in February this year, SCGC organized a delegation to visit the Middle East, traveling to Kuwait, the United Arab Emirates, and Saudi Arabia, among other places. The visits received favorable responses, and relevant collaborations are currently underway.

Certainly, beyond the opportunities, SCGC also faces numerous immediate challenges. On one hand, when the industry is in a downturn,To survive in adverse conditions as an investor, SCGC needs to demonstrate greater genuine competence than ever before.; on the other hand, with changes in the capital market, an increasing number of local state-owned assets have stepped forward, committing substantial investment.Therefore, SCGC also faces increased competition., competition has consequently intensified, SCGC still needs to withstand more tests.

Finally, here is a recent interview with Ni Zewang, in which he discussed SCGC’s future track selection: “In fact, there are many areas that SCGC needs to focus on. If we were to summarize them into three ‘mosts,’The primary focus should be on artificial intelligence; the second is the transformation and upgrading of the manufacturing industry, with the clearest direction being the comprehensive integration of digitalization and intelligence into manufacturing; and the last is breakthroughs or innovations in the field of foundational technologies.”

Will SCGC make the right bet this time?

1. "The Great River Flows On: Twenty Years of SCGC" — Hardcore Finance;

2. “At 24, SCGC Manages RMB 440 Billion!” — Investment Circle;

3. “Exclusive Interview with Zhou Yi of SCGC | The Line Between Primary and Secondary Markets Blurs Amid the Healthcare Investment Boom” — EO Health Talk;

4. “Two Decades of RMB Funds: Between Life and Death” – 36Kr;

5. “SCGC Chairman Ni Zewang: Not Investing in Tencent Is Our Greatest Regret” — Yicai