Why Are So Many Pharma and MedTech Companies Raising 'A+', 'A++', or Even 'A++++' Rounds?

ADDOR

Venture Capital Institution

HAOYUE CAPITAL

Financial Advisory Service Agency

Given the lengthy product development cycles and substantial capital requirements, fundraising is an unavoidable topic for nearly all startups in the medical sector.

For companies, the ideal scenario is to secure each round of financing swiftly, smoothly advance R&D and commercialization, successfully go public, enter a new growth phase, and realize both commercial and social value. For investors, the ideal scenario is to identify promising projects, invest at the right time, see the portfolio companies’ businesses grow steadily, and achieve financial returns after an IPO or large-scale profitability.

In recent years, the primary market for healthcare investments has been booming. Innovative companies have been able to secure funding at relatively favorable valuations, with smooth progress through Series A, B, and C financing rounds. Both enterprises and investors have acted decisively, with single transaction amounts frequently reaching new highs. A number of rapidly growing companies have already gone public.

However, since 2022, the industry has frequently seen “split” financing rounds such as Angel+, Angel++, Pre-A, Pre-A+, A+, and A++. This trend has elongated the cycle of each funding round, suggesting that significant subsequent milestones remain somewhat distant.

Typically, when companies encounter special circumstances between two rounds of financing, they complete a “transitional” financing round through structures such as Pre-X or X+. However, the latest trend suggests that a single “transitional” financing round is no longer sufficient.

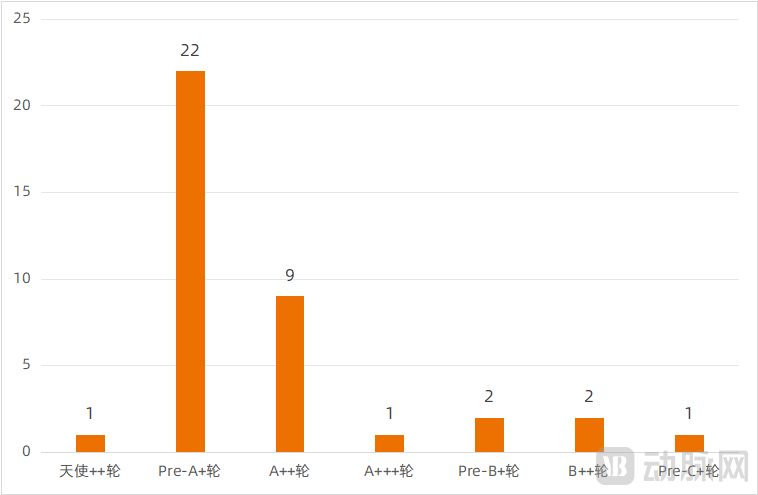

According to statistics from Artery Orange,From 2022 to the present, a total of 38 financing rounds were completed with two or more “add-on” tranches based on a single round.For instance, a Pre-A+ round may follow the Pre-A round, an A++ round may follow the A+ round, and even after the angel round, there may be Angel+ or Angel++ rounds.

Events with Two or More Rounds of Additional Financing in the Healthcare Sector from 2022 to Present, Source: VCBeat

Among the 38 financing rounds, Pre-A+ rounds were the most frequent, totaling 22; followed by A++ rounds, with 9. This indicates that companies in stages around Series A accounted for the largest proportion. These enterprises are primarily pharmaceutical and medical device companies, including 16 innovative drug developers and 14 innovative medical device manufacturers, most of which were established between 2017 and 2019, confirming their early-stage status.

Based on the disclosed use of proceeds by various companies, funding is primarily concentrated across various stages of product development, including technological optimization, clinical trials, regulatory submissions, pipeline expansion, and team building.

In terms of transaction amounts, among the 38 deals, more than half involved single-round financing in the tens of millions of yuan range, while 11 deals were around RMB 100 million. A Pre-B+ round nearing RMB 200 million represented one of the larger amounts. Given the substantial costs associated with innovative R&D, these financing levels are not particularly high. Meanwhile, many companies had relatively short intervals between financing rounds, typically ranging from a few months to about one year, with the shortest interval being just three months.

In general,Such "add-on" financings, occurring two or more times, are characterized by the company’s short operating history, its position in a critical early-stage R&D phase, intensive fundraising activities, and relatively small individual transaction sizes.

Currently, “investing early and in small ventures” has nearly become a consensus among primary market investment institutions.In early 2023, during VCBeat’s special interview series “2023 Investment Barometer,” most of the 12 participating investment firms highlighted the significance and trend of “investing early and investing in small ventures.”

Multiple investment institutions, including Sequoia China and Huagai Capital, have established venture capital funds focused on seed-stage and early-stage investments. Government guidance funds in various regions have also collaborated with local state-owned assets to set up technology transfer funds and seed funds supporting medical innovation ventures.

However,Early-stage investment is inherently high-risk.

“From 2019 to 2020, early-stage financing progressed rapidly through angel, Series A, and Series B rounds, a scenario rarely seen today.” Wang Haijiao, Deputy General Manager of GTJA Investment Group, believes that the proliferation of sub-series early-stage funding rounds indicates that early-stage financing has become more difficult.

Innovative startups that secure financing, or even frequently attract capital favor in the short term, must possess specific industrial value. Everything has multiple facets; if we examine the issue from more dimensions, why have so many ++ rounds emerged?

Meng Xiaoying, a partner at ADDOR Capital, explained that under traditional definitions of financing rounds, the criteria for distinguishing Series A, B, and C were clear: first, significant milestones must be achieved; second, there must be notable differences in valuation. Adjustments leading to structures such as Pre-A or A+ occurred only in response to a few specific circumstances, including timing considerations, distinctions based on investor type, or follow-on investments within the same round. “We have also observed that ++ series financing rounds have become more common than in the past, reflecting an overall elongation of the same financing cycle.”

Milestone events are closely tied to corporate financing rounds; in other words, if a company conducts multiple financings within the same round, the direct reasons include:The business or product has not yet reached certain milestones, and the funds previously raised are insufficient to drive progress toward the next milestone. Without sufficient milestone achievements, it is impossible to justify a valuation significantly higher than that of the previous round, necessitating a continuation of fundraising within the same financing round.

As for indirect factors, the difficulty enterprises face in raising sufficient funds to support milestone-driven progress in a single round is also related to investment institutions and the market environment.

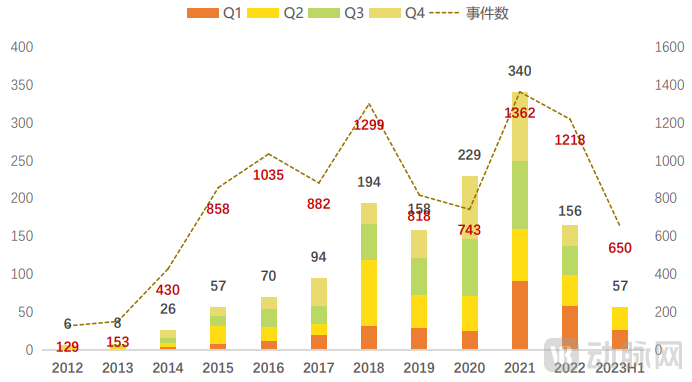

According to data from VCBeat and VBInsight’s “Global Healthcare Industry Capital Report for H1 2023,” the total investment and financing in China’s healthcare industry exceeded $5.6 billion (approximately RMB 41.051 billion) in the first half of 2023, representing a year-on-year decline of over 43%. The number of financing transactions totaled 650, an increase of 27 compared with the first half of 2022.

Total Financing Amount and Number of Deals by Quarter in China, 2012–H1 2023 (Unit: USD 100 million)

Image Source: "Global Healthcare Industry Capital Report H1 2023"

A decline in total financing coupled with an increase in the number of transactions indicates a drop in the average deal size. Investment institutions are exercising greater caution; given limited capital, they are reducing their investment in each project to mitigate risk.

Ding Yameng, Founding Managing Partner and Chief Operating Officer of Haoyue Capital, stated that investment institutions have become more cautious than in previous years, with increasingly meticulous post-investment management. They even assess the achievement of milestones, hoping that companies can achieve their phased goals quickly, effectively, and cost-efficiently.

Regarding the market, Wang Haijiao stated that the overall market landscape has shifted. If a company secured a high valuation in its previous funding round, it may not necessarily achieve a significantly higher valuation in the current round, even if its fundamentals have improved markedly. “Take innovative drugs as an example: suppose a company was valued at RMB 1 billion during its Series A financing, with its product in the preclinical stage. Now, although Phase I clinical trials have been completed, due to changes in the market environment, the company may only secure a valuation of RMB 1 billion or slightly higher, resulting in what is effectively an A+ round.”

Since 2023, many investors have believed thatValuations of companies by primary market investors are in a correction phase; valuations do not necessarily see significant increases between financing rounds, may remain stable, or could even decline.

“Companies have become more pragmatic. When valuations or fundraising amounts fail to meet preset expectations, they adopt the approach of ‘closing deals in batches as they mature.’ If parties continued to wait on each other, as was common in the past, the entire transaction might well fall through,” said Ding Yameng.

Companies resort to unconventional financing methods to secure funding and ensure normal operations, leaving them with little choice. Will such financing approaches become a normalized strategy?

From Ding Yameng’s perspective, such financing methods are posing increasingly greater challenges to founders and entrepreneurs. “Companies must adapt to changes in the market environment and must never be self-centered. When raising capital, regardless of whether the investors are venture capital funds, industrial capital, or local governments and industrial parks, companies should secure as much funding as possible and must not wait.”

Such a pace dictates that companies are either in the process of raising funds or on their way to do so. “Companies need to focus on both core business operations and fundraising simultaneously. Founders must remain engaged in both the capital markets and industrial markets.”

VCBeat has observed that some companies announce the launch of their next funding round concurrently with the completion of their current one.Historically, with clearly defined funding rounds, companies typically raised capital every 18 months or so, with each round closing within three to six months. This meant that founders dedicated three to six months per round to fundraising efforts, focusing on business development during the remaining time. However, if ++-round financing becomes the norm, it will inevitably significantly drain the energy founders can devote to their core business operations.

“How can a company move forward when its founder’s attention is diverted?” Wang Haijiao admitted that this is a scenario neither companies nor investors wish to see. “Financing rounds such as Series ++ are merely stopgap measures, not long-term solutions.”

Meng Xiaoying also believes that the ++ round of financing is less a strategy and more akin to a “Have to” status quo. “This model is unsustainable and poses uncertainties for enterprises, investment institutions, and the entire industry.”

Since this model is not the result of a single party’s actions, breaking the deadlock will require concerted efforts from multiple stakeholders.

From Meng Xiaoying’s perspective, the most immediate imperative for enterprises is to formulate capital plans more prudently and rationally, avoiding excessive optimism or unconvincing capital utilization models. “While maintaining confidence, companies should scale their ambitions to match their available resources.”

In the early stages of operation, companies rely heavily on financing. Given the less-than-optimistic overall conditions in the primary market, it may be worthwhile to consider an early-stage “monetization” model. Multiple investors interviewed by VCBeat stated that investment institutions hope to encourage companies to establish self-sustaining revenue mechanisms at every stage. For instance, besides raising capital from the financial markets, companies should seek external partnerships and diversify their funding sources through industrial collaborations, with the priority of ensuring survival.

“If securing a large sum of capital quickly can help a company reach its next milestone, it is advisable for the enterprise to moderately compromise on its valuation expectations,” said Wang Haijiao. He suggested making strategic trade-offs in the pipeline: for instance, if a Series A round initially aimed to raise RMB 100 million to advance three drug candidates, but sufficient funding cannot be raised in the short term, it would be more prudent to promptly terminate or suspend one candidate and concentrate resources on advancing the remaining two to the next milestone before raising a Series B round. This approach represents a more realistic path.

Investment institutions should likewise have sufficient confidence in their own judgment. “Where a company meets the fund’s investment criteria, it is advisable to provide the full committed capital in a single tranche, rather than through staggered disbursements; this helps avoid trapping portfolio companies in a vicious cycle of frequent fundraising rounds that distract founders from their core business,” said Wang Haijiao.

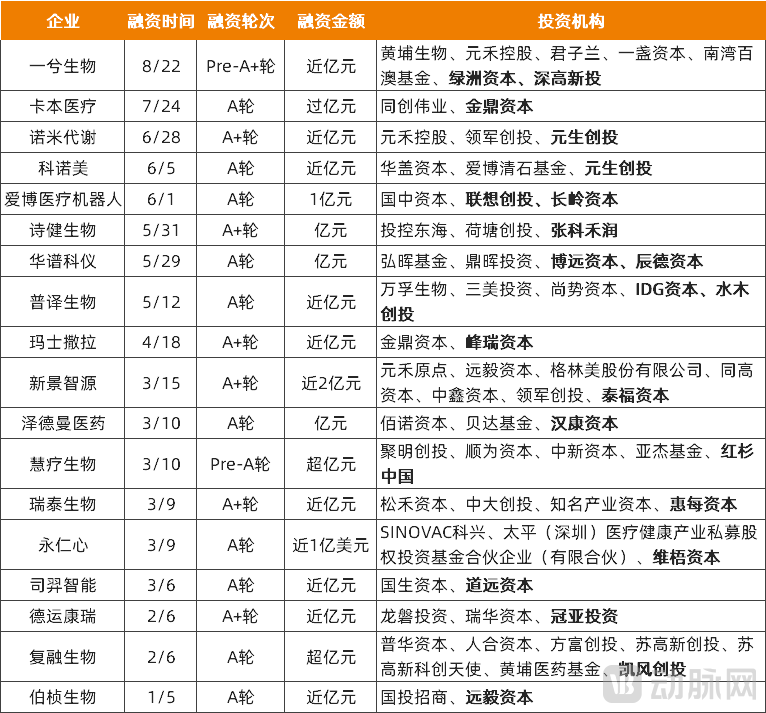

Since 2023, early-stage financing rounds with additional investments from existing shareholders have been recorded; bold font indicates existing shareholders (due to space limitations, only single-round financings of RMB 100 million or more, and Series A and earlier rounds are displayed). Source: Artery Orange

What should be done if a portfolio company fails to secure follow-on financing, yet the project remains of high quality? Some firms have adopted the strategy of allocating a certain proportion of their new fund to existing portfolio companies to continue injecting capital.

According to data from Artery Orange, since 2023 (as of September 20), more than 90 companies have received additional investments from existing shareholders. Among them, 48 are early-stage companies at Series A or earlier.

Although existing shareholders’ continued investment in enterprises is not necessarily driven by all the factors analyzed above, it does demonstrate institutional investors’ confidence and determination to fully support specific innovative sectors and high-quality projects. Such alignment is critically important in the current market environment.

Amid the capital winter, the phenomenon of difficult corporate financing can ultimately be traced back to the fundraising challenges faced by investment institutions.

In 2022, the number of healthcare venture capital deals and the total investment amount decreased, while decision-making processes slowed significantly. This trend reflects, on one hand, a return to rationality following the investment boom of 2020–2021, and on the other hand, is also attributable to an unfavorable fundraising environment.

Since 2023, government-guided funds have been highly active, with some industrial capital also making moves. Cities such as Guangzhou, Chongqing, and Hangzhou have established mother funds at the hundred-billion-yuan level, with healthcare being one of the key sectors supported.

According to VCBeat, from January to May 2023, a total of 58 new funds named after healthcare, biopharmaceuticals, and general health completed registration, with a total scale of approximately RMB 24.3 billion. Both the number and size were slightly higher than those in the same period of 2022 and 2021. Among them, Qiming Venture Partners and Fortune Capital (Dachen Caizhi) successively announced the completion of fundraising for funds worth billions of yuan, with key investment areas including healthcare.

Recently, there has been a steady stream of positive news, with multiple government guidance funds soliciting general partners (GPs) specializing in the healthcare industry, and numerous GPs successfully raising substantial capital for healthcare-focused funds.

In September, Huagai Capital’s Healthcare Growth Fund IV completed its first closing, with signed commitments totaling RMB 1.5 billion. The fund’s final size is expected to be no less than RMB 3 billion, and it will continue to focus on four key sectors: biopharmaceuticals, medical devices, healthcare services, and digital health.

The Beijing Municipal Government Investment Guidance Fund has issued a public announcement to select the fund management institution for the Beijing Pharmaceutical and Health Industry Investment Fund. With a scale of up to RMB 20 billion, the fund will primarily target key industrial sectors such as innovative drugs and innovative medical devices, as well as emerging fields including cell and gene therapy and digital healthcare, while also covering areas such as public health security and clinical production services.

In August, after the first closing of the Shenzhen Futian Taiping Medical Health Fund reached RMB 1.501 billion, it commenced investment operations. The fund targets a total size of RMB 3.001 billion and primarily invests in the medical and healthcare industry within the Greater Bay Area, with coverage extending to health technology and health consumption sectors.

……

The pace of innovation and venture capital may slow, but it will not halt. Currently, industry stakeholders—including enterprises and investment institutions—are all facing challenges. The strength of any single company or institution is insufficient on its own; only by remaining steadfast in our convictions and uniting for mutual support can we overcome these difficulties together.