Google at 25: The Tech Giant's Decade-Long Quest to Become a Pharma Powerhouse

Google DeepMind

Artificial Intelligence Technology Researcher

GV

Google's Investment Fund

Calico Life Sciences

Compound Developer

Google Cloud

Cloud Computing Service Provider

Internet-related services and product providers

Verily

Hardware and Software Developer in the Health Field

This September, Google turns 25, marking a full decade of its foray into the biopharmaceutical sector.

In 2013, one year after shutting down its first healthcare project, Google returned to the healthcare arena with greater ambition. On September 18, Google announced the establishment of California Life Company (known as “Calico”), a new healthcare company focused on aging and related diseases.

This time, the focus shifts from healthcare services to biopharmaceuticals.

This is a bold gamble by tech giants. For even today, when cross-sector forays from the internet industry into healthcare have become commonplace, those with the courage to establish biotech companies and charge into the pharmaceutical sector remain few and far between.

Calico was born out of Silicon Valley billionaires’ obsession with “immortality.” In 2013, three of the world’s ten wealthiest individuals—Google co-founder Sergey Brin, Facebook founder Mark Zuckerberg, and billionaire Yuri Milner—offered a $33 million prize for the most promising longevity research. That same year, Harvard University genetics professor David Sinclair first demonstrated in Cell that elevating NAD+ levels could make animals physiologically one-third younger.

Subsequently, Google ventured into the "uncharted territory" by establishing Calico.

When the news broke, it caused a public uproar, with Time magazine posing the question on its cover: “Can Google Defeat Death?”

Clearly, ten years on, Google still cannot provide an answer.

But over the past decade, Google has indeed used its internet-derived profits to map out a vast biopharmaceutical landscape. This map is replete with their fervor and dedication to the life sciences.

Thus, as Google marks ten years of pursuing its biopharmaceutical ambitions, the more realistic question is: Will Google become the next pharmaceutical giant?

After investing $250 million to establish Calico, Google co-founder Larry Page told Time magazine, “This is what I truly care about, rather than focusing on insignificant speculative deals.”

Since then, Google has embarked on a long-distance race in biopharmaceuticals, accompanied by the repeated splits and mergers of its healthcare initiatives.

The First Major Push, Originating from the 2015 Spin-off, Revealed Google’s Initial Healthcare Landscape.In 2015, Page announced that Google would undergo restructuring and establish a new parent company, Alphabet. Page spun off units with limited relevance to the core business—such as Google X, Calico, Google Ventures, and Nest—as independent subsidiaries under a decentralized management model.

This restructuring had a profound impact on Google. In the healthcare sector, Calico was no longer “fighting alone” but joined Life Sciences, Google X, Calico, and Google Ventures in a landscape of “fierce competition.” Subsequently, these subsidiaries all experienced a significant expansion in value. At the end of 2015, Life Sciences was renamed Verily.

However, Page may not have realized at the time that this “siloed” approach also sowed the seeds for Google’s later quagmire in the healthcare sector.

At its inception, Calico was positioned as the “Bell Labs of aging research,” focusing on preclinical studies. It established its own automated laboratory and has maintained a long-term collaboration with the biopharmaceutical company AbbVie since 2014 to jointly develop therapies for age-related diseases such as neurodegeneration and cancer.

Meanwhile, its sibling company Verily focuses primarily on improving clinical technologies and early-stage drug discovery. Major pharmaceutical companies have begun partnering with Verily to leverage digital platforms that streamline and accelerate clinical trials. Concurrently, Google X has deepened its involvement in medical research, aiming to utilize genetic data and biomarkers to understand human health issues at the molecular and genetic levels. In 2016, Verily partnered with GSK to establish Galvani Bioelectronics for the development of “bioelectronic medicines.”

Thus, Google’s biopharmaceutical dream set sail.

The second ambitious launch came three years later, when Google established its massive healthcare task force—Google Health.

Google has spun off the healthcare divisions of its Search, Cloud, and Google Brain businesses, along with DeepMind’s health unit and the Streams team, consolidating them under Google Health. This integration also incorporates Calico’s anti-aging technologies. This segment of Calico’s business focuses on leveraging AI to analyze large datasets in order to combat aging and age-related diseases. The restructuring is led by David Feinberg, a prominent figure in the healthcare industry who was recruited externally, and he serves as CEO.

With this restructuring, Google’s intention to concentrate its efforts on “AI + Healthcare” is evident.Since then, Google Health, Verily, and Calico have formed a tripartite structure. Regrettably, despite boasting the most prestigious team, Google Health’s journey in healthcare has remained precarious.There was even a major clash between “technology” and “medicine” within the leadership.

When the company was dissolved in 2021, insiders revealed that the state of Google Health was the result of a lack of respect for professionals and an imbalance in internal influence, which led to the “tech faction” driving out the “medical faction.” Ultimately, CEO David Feinberg departed, Google Health was disbanded, and relevant personnel went their separate ways.

Perhaps it is precisely this “cultural mismatch” that has prevented Google Health from gaining the upper hand, even in Google’s internal race for “AI + healthcare” over the past three years.

For example, Fitbit falls under Google’s Devices and Services division, while YouTube launched its own health team in early 2021 to combat medical misinformation. Onduo, a virtual care company specializing in chronic diseases, is affiliated with Verily, which also established a new artificial intelligence R&D center in Israel that year. Notably, AlphaFold, Google’s most significant achievement in life sciences, does not fall under Google Health.

Trapped in these awkward predicaments, it is likely the result of bugs stemming from Page’s previous “siloed” strategy. Google Health, intended to enable unified group operations, has in fact lacked the capacity to end the era of “fragmented fiefdoms.”

Clearly, even Google had to pay its dues when first entering the healthcare sector. Its fragmented, overlapping, and complex business operations have hindered cohesive development, leading to repeated setbacks in the healthcare field.

According to the 2021 financial report, Google’s healthcare business within the Other Bets segment incurred a loss of $5.3 billion that year.

But amidst the chaos surrounding Google Health, Google’s “AI + Healthcare” initiatives have proliferated wildly across various departments.

Marked by the groundbreaking emergence of AlphaFold 2.0 in 2020, Google began to make significant strides in the AI-driven drug discovery sector.

In November 2021, to continuously promote the commercialization of related technologies, Isomorphic Labs was spun out from DeepMind as a drug discovery subsidiary.

Upon its spin-off, Demis Hassabis, founder and CEO of DeepMind, explicitly stated: “Isomorphic may not develop its own drugs, but will instead license its models and focus on building partnerships with pharmaceutical companies.” It is hard to argue that this does not reflect the lessons Google has learned from its forays into the healthcare sector in recent years. We are witnessing a realignment where medicine and technology return to their proper roles.

Following substantial losses, Google promptly adjusted its strategy, refocusing on patient data, clinical trial facilitation platforms, and AI-driven drug development.

Google Cloud and quantum computing are also major players entering the AI drug discovery space.

In January 2021, Boehringer Ingelheim announced a three-year collaboration with Google Quantum AI. The partnership focuses on researching and implementing cutting-edge use cases of quantum computing for drug development, marking Google Cloud’s first collaborative venture into the pharmaceutical sector. In February 2023, Google spun off its original quantum computing operations to establish SandboxAQ, a quantum technology company that collaborates with biotechnology businesses. Currently, pharmaceutical giants AstraZeneca and Sanofi are among its partners.

And this July, Google Cloud also launchedAI Drug Development Plan. Google claims that Pfizer, Cerevel, Colossal, and others are using these AI drug discovery solutions.

Google Cloud’s AI Drug Discovery Tools:

Target and Lead Identificiation Suite: Helps researchers predict and understand the structure and properties of proteins.

Multiomics suite: Helps drug developers extract, store, analyze, and share large volumes of genomic data to enhance precision medicine solutions.

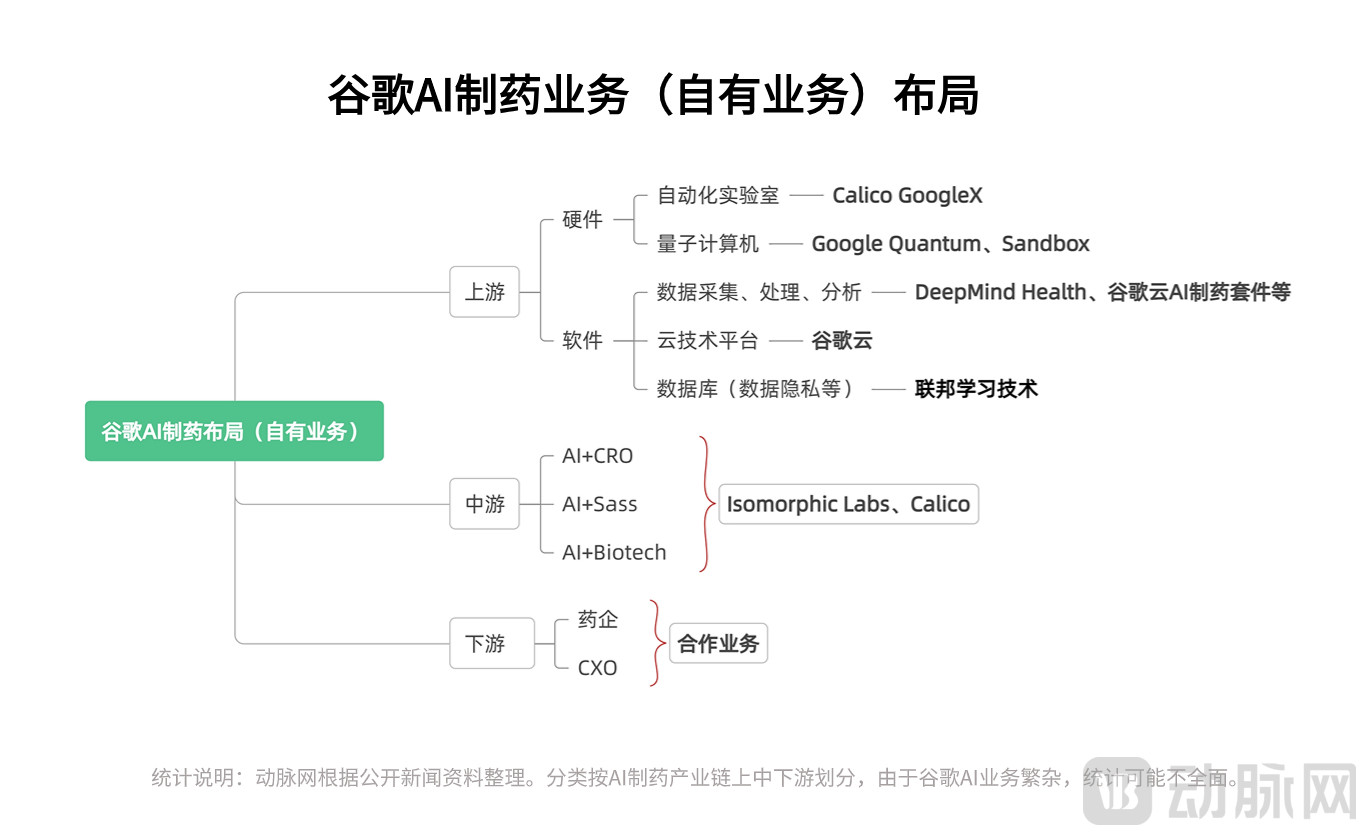

We can see that Google is currently taking a very active position in the AI drug development industry chain, with significant resources committed across its various divisions. Its capabilities are concentrated in the upstream hardware and software segments of AI-driven drug development, with value primarily manifested in the field of drug discovery.

The core elements of AI-driven drug discovery remain computing power, algorithms, and data. As a global technology giant, Google possesses the capability to aggregate, store, share, and process massive volumes of data. Its robust tool development and algorithmic analysis capabilities constitute its first-mover advantage in delivering AI-based pharmaceutical solutions.

The barriers between the internet and biotech that have plagued Google for a decade are being broken down.AI-driven drug discovery has gradually become the interface between two worlds, bridging Google’s core business with its pharmaceutical ambitions.

Benefiting from the accelerated integration of AI technology with its business operations, Google saw a rebound in its second-quarter performance, with revenue rising 7% year over year. Notably, the Other Bets segment, which includes healthcare initiatives, recorded a 48% year-over-year revenue increase, reaching $285 million.

In early September, Google’s current CEO, Sundar Pichai, stated in an open letter celebrating Google’s 25th anniversary that Google is going “all in” on AI.

To understand Google’s pharmaceutical landscape, one must examine its external investments, which serve as the foundation for its entry into this sector.

Google’s first investment in healthcare dates back to 2007. However, the majority of its investments occurred after the establishment of Google Ventures (hereinafter referred to as GV) in 2009.GVWithin less than six months of its founding, it became one of the most active venture capital funds in the United States.

In 2015, GV restructured and became an independent entity, doubling down on its focus on the healthcare sector.

According to The Wall Street Journal, GV’s investments in health and life sciences accounted for 36% of its total investment portfolio during 2014–2015, reaching a peak. Currently, life sciences and health remain one of its primary investment sectors.

According to VCBeat, Google now holds stakes in nearly 100 biotech companies (most through GV, based on data from Artery Orange).

Among these, Google has already invested in publicly listed companies. But more importantly,16 years of continuous investment have enabledGoogle has established a presence across all key segments of the pharmaceutical industry and ventured into multiple therapeutic modalities.

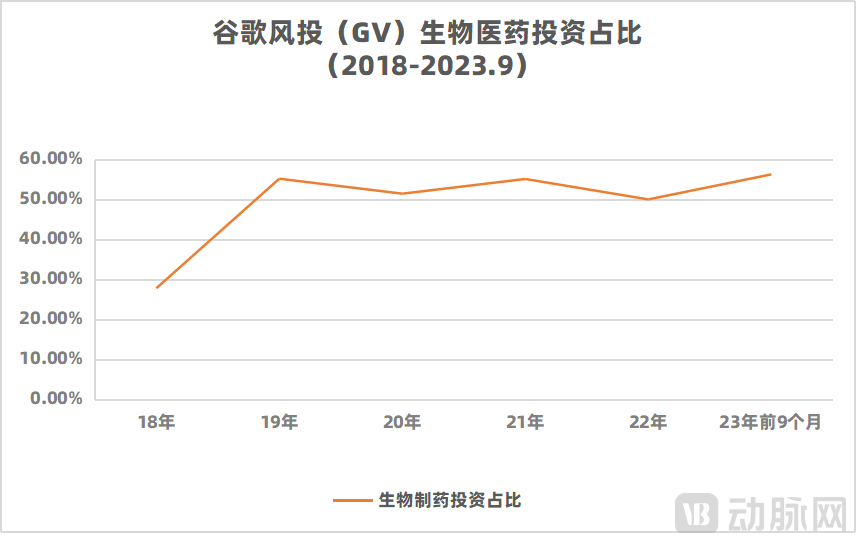

Specifically, since 2019, biopharmaceuticals have become GV’s most closely watched healthcare subsector, consistently accounting for over 50% of its investments. Notably, the pace of investment has accelerated significantly since 2021. Over the past three years, Google has made a total of 51 investments in the biopharmaceutical sector.

This is also an example of Google Health’s future strategic tilt toward biopharmaceuticals. AI-driven drug R&D is likely to be a key focus for Google in the coming period.

Figure: Data source: Artery Orange

Furthermore, GV’s investment style also demonstrates Google’s determination to engage in a long-term commitment to the pharmaceutical sector.

Investing in new ventures, investing at an early stage, and providing long-term support have been its consistent style in this sector.

For instance, Cerevance and Ventus Therapeutics, both affiliated with Google, were included in the 2023 Fierce 15 list released by Fierce Biotech. Cerevance, which focuses on developing therapeutics for brain disorders, has received investment from Google since 2020. Last year, Cerevance entered into a $1.1 billion collaborative research agreement with Merck & Co. in the field of Alzheimer’s disease, advancing multiple pipeline candidates into clinical stages.

Earlier this year, Cerevance announced positive results from its Phase I study of the orexin 1 receptor (Ox1R) antagonist CVN766 in healthy subjects. In February, GV increased its investment.

For another example, Google invested this year in Bitterroot Bio, a developer of therapies for cardiovascular diseases. It is the world’s first biopharmaceutical company to develop drugs targeting CD47/SIRPα for the treatment of atherosclerosis. Previously, 95% of drugs targeting CD47/SIRPα were developed for oncology indications; to date, no such products have been approved for marketing, with the most advanced candidates currently in Phase III clinical trials. In fact, receiving investment from GV has become a significant mark of recognition for biotech companies.

GV’s focus on emerging fields has not only made it a bellwether in healthcare investment but also helped Google identify suitable acquisition targets.These innovative companies could become the core of Google’s in-house medical team. It was GV that spearheaded the establishment of Calico back then. Today, the anti-aging sector is booming, yet Google made substantial investments in this field as early as ten years ago.

We have integrated Google’s investments with our own biopharmaceutical operations. On paper, Google’s reach into the pharmaceutical sector has long permeated even the most minute details, far exceeding our expectations for a typical pharmaceutical company.

In fact, the tech giants’ blueprints have already been laid out on paper.

Moreover, he seems to be brimming with confidence again.

A major challenge for technology companies entering the AI-driven drug discovery sector is the scarcity of high-quality, large-scale, purpose-specific datasets for development and testing. Pharmaceutical companies may be reluctant to share their proprietary R&D data.

But for Google, which has made approximately 250 healthcare investments and holds stakes in nearly 100 innovative pharmaceutical companies, this may not be a challenge.

Finally, we must return to reality.

Looking at Google’s healthcare initiatives, change has been the dominant theme over the past decade. Calico, however, is an exception. Regardless of how other departments’ structures were adjusted during this period, it has remained “as stable as Mount Tai,” shrouded in mystery.

Even industry insiders are largely unaware of what Calico is actually doing. Felipe Sierra, former director of the Division of Aging Biology at the U.S. National Institutes of Health, once stated, “We want to know what they are doing, so that we can focus on other areas or collaborate with them.”

Calico is the core division of Google’s biopharmaceutical initiatives. How has it performed over the past decade?

All that can be said is: there are results, but not many.

In October 2022, after a nine-year hiatus, Calico announced that its new drug candidate, ABBV-CLS-7262, had entered the design phase for inclusion in the HEALEY ALS Platform Trial. This marks the only pipeline asset to have advanced to the clinical stage at Calico in the past decade.

Calico believes that, if all goes well with ABBV-CLS-7262, it could be commercialized within 5 to 10 years, entering the anti-aging market currently dominated by Rejuvant, and accelerating the realization of humanity’s ideal of “reversing aging.”

Calico is frequently criticized by outsiders for its slow progress. The prevailing criticism within the industry is that it has been overly fixated on exploring the “fundamental mechanisms” of aging, without applying existing findings from aging research.

Meanwhile, latecomers to the industry are making a formidable entrance. For instance, Altos Labs, founded in 2021, secured $3 billion in its seed round—the largest angel investment globally—within just one year of establishment. In less than two years, it has published multiple significant papers on cellular reprogramming and aging research. The team claims that it will ultimately use molecular technologies to fundamentally extend human lifespan by 40 years or more.

Calico has long failed to achieve a self-sustaining business model, leading to disappointment within Google.

Bill Maris, founder and CEO of Google Ventures, who facilitated the establishment of Calico. After leaving Google in 2016, he publicly expressed his deep disappointment with Calico’s slow progress. “I don’t know why they aren’t publishing papers. I don’t know why we haven’t seen any research findings released. I don’t know why it seems no one knows what they are doing… This is completely different from what I had envisioned.”

In fact, the situation with Calico is also a microcosm of Google’s overall poor commercial performance in healthcare.

Google shareholders have pointed out that the company’s Other Bets segment generated $3 billion in revenue over the past few years, while incurring $20 billion in operating losses.

Indeed, the quest to conquer death marks both the beginning and the end of Google’s biopharmaceutical ambition. With milestones achieved over the past decade, it has arguably delivered on its promise. Yet losses remain a pressing reality. Early this year, Verily, a subsidiary under the same health business segment, announced the termination of its innovative initiatives and a 15% workforce reduction due to revenue falling short of expectations.

At this juncture, going all-in on AI-driven drug discovery remains a case of “delayed gratification.”

On one hand, from a technical perspective, AI performs well in single-dimensional tasks, such as predicting drug-protein binding efficacy; however, for complex tasks characterized by high dimensionality and limited data, such as toxicology and pharmacokinetics, continued technological advancements are still required.

On the other hand, the AI drug discovery arms race among various industry leaders has reached a fever pitch. Although Google holds technological advantages, it faces blockades from tech giants such as Microsoft and NVIDIA ahead, while traditional pharmaceutical companies are catching up from behind. Moreover, the critical tipping point for market commercialization has not yet arrived. To date, no AI-discovered drug has been approved for market launch.

Google will also continue to pour massive investments into its biopharmaceutical ambitions.

According to previous forecasts by CCID Consulting, a batch of AI-developed drugs will enter Phase II clinical trials, known as the “Valley of Death,” between 2023 and 2025, with the first AI-driven pharmaceutical product likely to reach the market only in 2026–2027.

Article reference:

“Google’s Anti-Aging Efforts, Year 10” TimePie

“Leveraging Google Cloud to Uncover Aging Mechanisms, Calico Develops New Anti-Cancer and Anti-Aging Drugs” 36Kr

“Inside the ‘Spinoff’ of Google Health: A Frustrated CEO, an Arrogant Jeff Dean, and Zealous AI Believers” Leifeng.com

“Google’s Ambition: The Next AI Drug Discovery Company” by Sheng Jie Qianyan