Wanbang Pharma, a Generic Drug-Focused CRO, Lists on ChiNext: Where Do Opportunities Lie for Mid-Sized CROs?

Wanbang Pharmaceutical Technology

Pharmaceutical CRO Service Provider

Amid the recovery of the pharmaceutical sector, a generic drug CRO company has joined the ChiNext board.

Anhui Wanbang Pharmaceutical Technology Co., Ltd. (hereinafter referred to as “Wanbang Pharmaceutical”), an integrated CRO provider, launched its IPO today,Becoming the “First CRO Stock in Anhui,” with a market capitalization of RMB 4.3 billion.Through this fundraising, Wanbang Pharmaceutical will gradually expand its Phase I-IV clinical research and pharmaceutical studies on innovative drugs.

The number of IPOs in the biopharmaceutical sector has declined again this year compared to 2022, with only 11 companies listing on the A-share market and six on the Hong Kong stock exchange. Since the second half of the year, several additional companies have voluntarily terminated their IPO processes. The listing journey of Anhui Wanbang Pharmaceutical Technology Co., Ltd. also spanned two years. The company first disclosed its prospectus for the ChiNext board in September 2021, experienced two suspensions of review in March and July 2022, and ultimately passed the listing committee’s review in October 2022 after responding to two rounds of inquiries.

Listing standards for the ChiNext board emphasize a company’s net profit or operating revenue. Although Anhui Wanbang Pharmaceutical Technology Co., Ltd. met these performance criteria, it remained under close scrutiny by regulators. According to documents released by the Shenzhen Stock Exchange, the inquiries directed at Wanbang Pharmaceutical primarily focused on two aspects: one concerning the company’s core technologies and competitiveness, and the other revolving around its revenue recognition practices and the sustainability of its financial performance.This reflects the increasingly stringent and standardized market access requirements, and also mirrors the fact that generic drug CROs have reached a critical juncture amid the evolution of China’s biopharmaceutical industry.

Seizing Demand from Generic Drug Manufacturers, Accounting for Nearly One-Tenth of China’s Bioequivalence Trials

Founded in 2006, Wanbang Pharmaceutical is one of the earliest CRO companies in China to provide drug R&D services. Its founder, Tao Chunlei, originated from the Hefei No. 6 Pharmaceutical Factory and established Wanbang Pharmaceutical as a side venture while serving as a lecturer at Anhui University of Chinese Medicine, before fully resigning from her public-sector position in 2021.

From the company’s history, founder Tao Chunlei has demonstrated boldness and resilience. According to her own account,Following the release of the “722 Clinical Trial Verification” policy in 2015, Wanbang Pharmaceutical experienced a significant crisis. Starting in 2017, the company embarked on a second entrepreneurial phase, seizing new industry opportunities and achieving rapid growth.

During the “722 Verification,” the quality of a large volume of clinical data was called into question and subjected to scrutiny. Many CROs were publicly cited, leading to rapid industry consolidation and the elimination of homogeneous, low-quality CROs. Subsequently, the launch of the generic drug consistency evaluation further facilitated the growth and success of many CROs.

Anhui Wanbang Pharmaceutical Technology Co.,Ltd. is one of the CROs that not only survived but also thrived at this turning point. Leveraging its technological expertise, accumulated client base, and corporate management reforms, the company has achieved a leapforward in its business scale.

The prospectus of Anhui Wanbang Pharmaceutical Technology Co., Ltd. shows that,Since the issuance of the “722 Clinical Trial Verification” policy, the company has cumulatively undertaken more than 500 clinical research service projects,Abundant clinical institution resources and extensive clinical trial experience have enabled the company to maintain a solid market position in bioequivalence (BE) studies: according to the official website of the Center for Drug Evaluation (CDE) and company data, Wanbang Pharmaceutical’s market share of annual BE study filings reached 6.53%, 7.50%, and 9.77% in 2020, 2021, and 2022, respectively.

Bioequivalence (BE) studies, which involve administering the same dose of a generic drug and its originator counterpart to subjects under identical conditions to observe therapeutic effects, constitute a critical component of generic drug consistency evaluations. Currently, pharmaceutical products from domestic companies in China remain predominantly generics. In 2020, the consistency evaluation policy was extended to include generic injectables, further expanding the scale of the existing market for consistency evaluations. Since only a few large pharmaceutical enterprises in China possess the capacity to independently undertake these evaluations, while the majority lack sufficient time and resources to conduct them on their own, there is a significant reliance on Contract Research Organizations (CROs).

Wanbang Pharmaceutical has been developing in central China for many years and has established stable clinical research service providers in the region, including Anhui Jimin Cancer Hospital, Chenzhou No. 1 People's Hospital, The Second Affiliated Hospital of Anhui Medical University, Hefei BOE Hospital Co., Ltd., Wuhan Jinyintan Hospital, and Changsha No. 3 Hospital.Proficient in the selection of collaborative clinical institutions, assessment of bed availability, and scheduling of clinical trials, thereby securing a certain degree of bargaining power.

Generic drug manufacturers need to maximize efficiency at every stage prior to market launch to compete for market share. Experienced bioequivalence (BE) trial service providers can save generic drug companies significant time. Anhui Wanbang Pharmaceutical Technology Co., Ltd. has project experience across a wide range of dosage forms, including tablets, capsules, enteric-coated formulations, orally disintegrating tablets, dry suspensions, chewable tablets, soft capsules, controlled-release tablets, fat emulsions, gel patches, drops, and injections, having conducted over 500 BE trials. For clients, if a product development project proceeds smoothly, they will prioritize Wanbang Pharmaceutical for other drugs in the same therapeutic area to reduce costs.This also explains why Anhui Wanbang Pharmaceutical Technology Co., Ltd. accounts for nearly one-tenth of all bioequivalence (BE) trials in China.

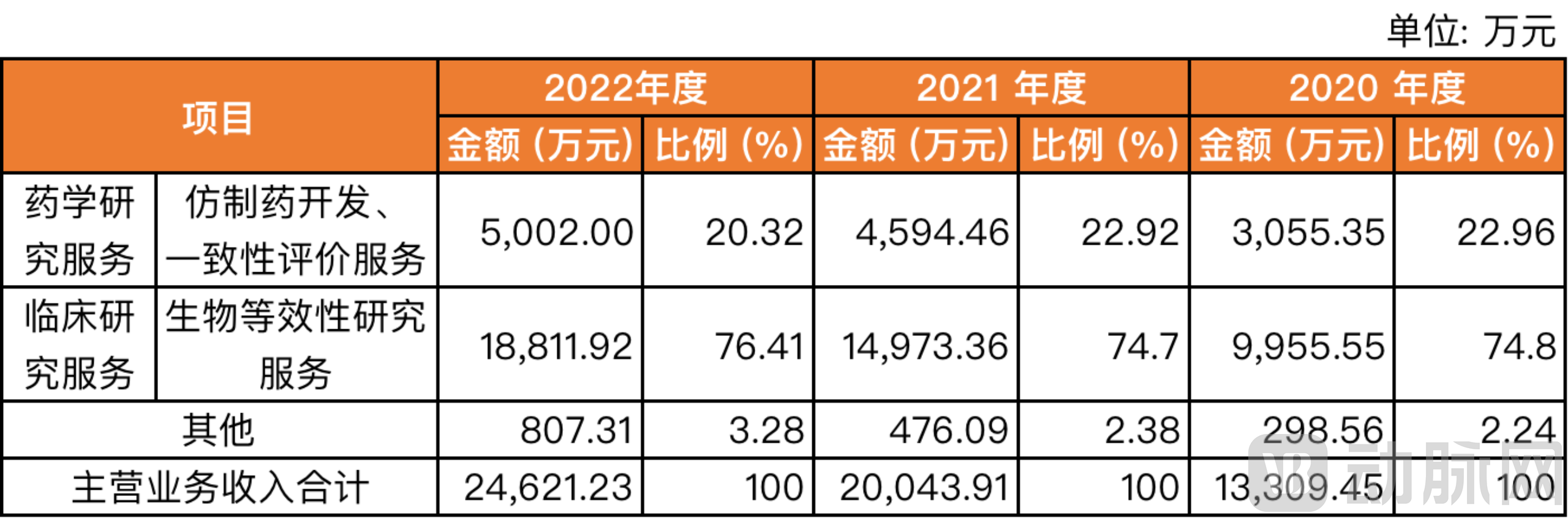

Wanbang Pharmaceutical’s Main Business Revenue, Source: Company Prospectus

Bioequivalence (BE) trials have generated substantial revenue for Wanbang Pharmaceutical. From 2020 to 2022, the company’s BE trial services recorded revenues of RMB 99 million, RMB 149 million, and RMB 188 million, accounting for 74.8%, 74.7%, and 76.4% of its total core business revenue, respectively. BE trials provide extensive clinical data guidance for the company’s other core business segment—pharmaceutical research—while the technical expertise accumulated in pharmaceutical research, in turn, supports BE studies.

Stability and reliability are among the hallmarks of a high-quality generic drug CRO.Wanbang Pharmaceutical’s client base covers well-known domestic pharmaceutical companies, including multiple subsidiaries under China Resources Group such as China Resources Saike and China Resources Double-Crane Pharmaceutical, as well as Kelun Pharmaceutical, Shanghai Modern Pharmaceutical, and Jichuan Pharmaceutical. The company’s major clients are relatively concentrated; in 2022, the revenue from its top five clients accounted for 27.6%, including Shanghai Ideal Pharmaceutical, Kelun Pharmaceutical, Shijiazhuang No.4 Pharmaceutical (Shisiyao), Anhui Beck, and Nanjing Komor. Meanwhile, the number of new clients has shown a rapid upward trend: from 2019 to 2022, the company added 16, 30, 27, and 56 new clients, respectively, demonstrating a strong growth momentum.

Anhui Wanbang Pharmaceutical Technology Co., Ltd. Achieves Steady Growth by Addressing Core Needs of Generic Drug Manufacturers; Net Profit for January–September 2023 Is Projected at RMB 82.875 Million to RMB 87.125 Million, Representing a Year-on-Year Increase of 20.24% to 26.4% from RMB 68.9261 Million in the Same Period Last Year

Behind High Gross Margins: The Crossroads for Generic Drug CROs

As a generic drug CRO, the low ceiling is an unavoidable issue.

A comparison of the 2022 operating data between major domestic CRO companies and Wanbang Pharmaceutical reveals that Wanbang Pharmaceutical has a relatively narrow business scope and smaller scale. In contrast to Tigermed, a leading enterprise that entered the innovative drug services sector early on, Wanbang Pharmaceutical reported an operating revenue of RMB 260 million in 2022, whereas Tigermed’s revenue exceeded RMB 7 billion.

Comparison of Business and Revenue Between Wanbang Pharmaceutical and Comparable Companies, Source: Compiled from the Company’s Prospectus

Behind its stable profits and high gross margin levels lie the company’s development bottlenecks:

Anhui Wanbang Pharmaceutical Technology Co.,Ltd.'s high gross margin in clinical research stems from its business focus on bioequivalence (BE) trials primarily conducted in healthy volunteers, as it has not yet entered the more challenging Phase II–IV clinical trial services, which are more closely associated with innovative drug development.

The high gross profit margin in pharmaceutical research is largely attributable to Anhui Wanbang Pharmaceutical Technology Co., Ltd.'s limited R&D investment and relatively homogeneous technology portfolio.

This also represents the two major crossroads facing many generic drug CROs: maintain current scale or compete for market share to expand operations? Continue relying on generic drugs to “make ends meet” or venture into innovative drugs?

It is evident that the traditional service model for generic drug CROs is becoming increasingly saturated, with intensifying competition not only on pricing but also on payment terms and collection periods. To compete at a high level in the future, companies must undertake difficult yet correct initiatives.

The intense competition among generic drug CROs is driven not only by insufficient technical barriers but also significantly by shifts in the pharmaceutical market landscape: According to Frost & Sullivan, the growth rate of China’s innovative drug market will outpace that of the generic drug market. In 2021, the size of China’s innovative drug market was RMB 947 billion, and it is projected to reach RMB 2,058.4 billion by 2030, representing a compound annual growth rate (CAGR) of 9.0%. In contrast, the generic drug market is expected to grow from RMB 644.2 billion in 2021 to RMB 680.5 billion in 2030, with a CAGR of 0.6%.

Traditional generic drug CROs have multiple pathways to seek new growth through transformation.For instance, Tigermed provided clinical services for domestic generic drugs in China before 2010, then transitioned into clinical services for innovative drugs and built an integrated platform. To date, it has participated in and facilitated the R&D of more than 50 Class 1 innovative drugs already marketed in China, although such a transformation requires substantial financial support.

Adding services for Class 2 innovative drugs, i.e., improved novel drugs, offers a higher cost-performance ratio for many CROs.Class 2 innovative drugs include improvements to active ingredients, new formulations, novel manufacturing processes and administration routes, new combination products, and new indications. They address substantial market demand and have a higher success rate than Class 1 innovative drugs.

According to data published by relevant professional research institutions, the market size of improved innovative drugs in China is projected to reach RMB 561.3 billion by 2025, with a compound annual growth rate (CAGR) of 11.6%, and to reach RMB 795.2 billion by 2030, with a CAGR of 7.2%.

Source: Compiled based on Yaozhi Data

In recent years, traditional pharmaceutical companies—longstanding clients of generic drug CROs—have increasingly entered the field of improved new drugs, which presents a more accessible growth opportunity for generic drug CROs.

However, to secure a share of this market, companies must be willing to make bold investments in technology, including the research and development of advanced drug formulations and the accumulation of technical platform capabilities.For instance, among the aforementioned comparable companies, Boji Medicine’s formulation technologies include injections, sustained-release formulations, and topical preparations; Baihuacun is involved in multiple raw material synthesis processes—such as peptide synthesis, peptide recombinant technology, targeted drug delivery, and sustained/controlled release—as well as complex formulation technologies.

Anhui Wanbang Pharmaceutical Technology Co.,Ltd. is clearly aware of the promising prospects in the innovative drug market. One of the primary uses of the funds raised from this IPO is to expand its pharmaceutical research into the field of innovative drugs.However, compared with Tigermed’s 30 patents, Baicheng Medicine’s 15 invention patents, and Baihuacun’s 60 invention patents, Wanbang Pharmaceutical, with only two invention patents and two utility model patents, still has a long way to go.

Having crossed the IPO watershed, can companies seize opportunities before the industry landscape solidifies?

This IPO marks a significant watershed for Anhui Wanbang Pharmaceutical Technology Co., Ltd. For domestic CXO companies, achieving annual revenue in the tens of millions is relatively easy, whereas reaching RMB 200 million represents a critical “threshold” that determines whether a company is capable of going public.Anhui Wanbang Pharmaceutical Technology Co., Ltd. surpassed this key figure after 2021 and successfully listed on the ChiNext board today. After clearing successive hurdles, the company now faces a post-watershed landscape.

Following its initial public offering, the CRO company faces mounting pressure to sustain performance growth, signaling its entry into a new phase characterized by scaling and enhanced corporate governance. The company may experience volatility as it strives to reach higher revenue milestones, with potential setbacks in both R&D capability enhancement and business expansion. This poses a significant challenge for a generic drug-focused CRO of modest size.

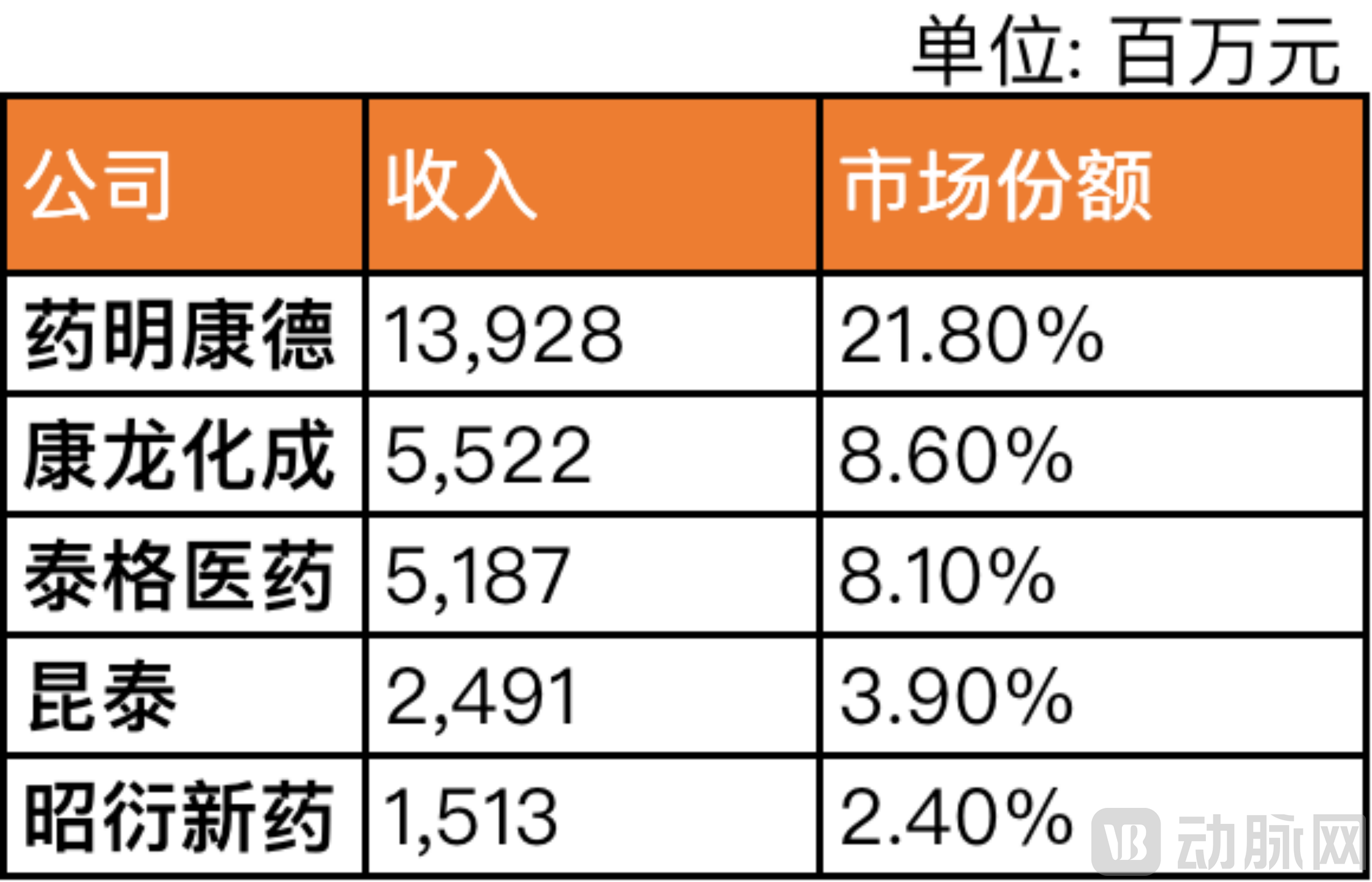

However, Anhui Wanbang Pharmaceutical Technology Co.,Ltd. still has the opportunity to break through, as it targets the domestic clinical CRO market—particularly the innovative drug clinical CRO sector.Still in its early stages, the industry exhibits low concentration, allowing small and medium-sized CROs to remain competitive in the market.According to Frost & Sullivan, in terms of revenue and market share, the top five competitors in China’s CRO market in 2021 accounted for approximately 45% of the total market share.

Market Share of the Top Five Players in China’s CRO Market in 2021, Source: Frost & Sullivan

In the more mature North American market, leading companies have nearly carved up the industry. According to data from a research report by Soochow Securities, the top five clinical CROs in North America—PPD, IQVIA, ICON, LabCorp, and Syneos Health—accounted for approximately 73.3% of the market share in 2022. Moreover, these five companies held a substantial 65.4% share of the global clinical CRO market.

The competitive landscape of China’s CRO industry remains unsettled, yet it is beginning to show signs of consolidation. Particularly amid significant pressure on biopharmaceutical financing and investment, clinical CROs are also facing demand-side pressures. Industry leaders, with their healthier cash flows and superior operational capabilities, are better positioned to gain recognition from pharmaceutical companies.This means that the consolidation of small and mid-sized clinical CROs is accelerating.

Anhui Wanbang Pharmaceutical Technology Co., Ltd. is embarking on its “third entrepreneurial venture.” In the realm of pharmaceutical research services, it is expanding its business into complex generics, improved new drugs, Marketing Authorization Holder (MAH) transitions, and innovative drug development. The company is establishing a Phase I–IV clinical research service platform to seize opportunities in innovative drug development, continuously broadening its bioanalytical services for large-molecule drugs and other testing services related to pharmacokinetics/pharmacodynamics (PK/PD) of innovative drugs, and building a bioanalytical testing platform that complies with dual submission requirements in both China and the United States.

Wanbang Pharmaceutical, having secured IPO financing, still has the opportunity to become a core player among China’s CROs.