Three Wuhan Tongji Alumni Co-found Biotech Pioneer in Bispecific Antibody Therapeutics, YZY Bio Goes Public on HKEX

On September 25, after navigating minor setbacks, Wuhan Youzhiyou Biopharmaceutical Co., Ltd., an innovative drug company based in Wuhan, Hubei Province, listed on the Hong Kong Stock Exchange. This marks the sixth mainland Chinese pre-revenue biotechnology company to list on the Hong Kong Stock Exchange this year.Youzhiyou Biopharma Opens with a Market Cap of HK$3.2 Billion, as of now, this is the smallest biotech stock with a “B” listing designation to have debuted on the Hong Kong Stock Exchange year-to-date. Prior to publication, the share price of Youzhiyou Biopharma stood at HK$16.36, with a market capitalization of HK$3.157 billion.

Youzhiyou Biopharma Real-Time Quotes | Data Source: Xueqiu

Wuhan Youzhiyou Biopharmaceutical Co., Ltd., established in 2010 and located in the East Lake High-Tech Development Zone of Wuhan, develops innovative biologics to combat major diseases based on its bispecific antibody platform. Unlike most peers that focus on developing innovative drugs targeting specific tumors, Youzhiyou Biopharmaceutical primarily addresses severe complications of cancer, namely malignant ascites and malignant pleural effusion, which represent a significant unmet need in clinical practice.

Wuhan Youzhiyou Biopharmaceutical’s core product, M701, is a recombinant bispecific antibody that targets EpCAM-expressing cancer cells and the T-cell surface antigen CD3. It is primarily indicated for the palliative treatment of malignant ascites and malignant pleural effusion. In January 2022, M701 completed its Phase I clinical trial for the treatment of malignant ascites and is currently undergoing Phase II clinical trials, with commercial launch planned for the fourth quarter of 2025. Among comparable innovative drugs, M701 is among the most advanced in development. Additionally, Wuhan Youzhiyou Biopharmaceutical has a pipeline of six other investigational products, all of which have entered clinical stages, covering cancer-related complications, cancers, and age-related ophthalmic diseases. From a commercialization perspective, Wuhan Youzhiyou Biopharmaceutical presents considerable promise.

Prior to its initial public offering, Wuhan Youzhiyou Biopharmaceutical Co., Ltd. completed multiple rounds of financing, raising hundreds of millions of yuan in total. This attracted investment from institutions with state-owned, industrial, and professional venture capital backgrounds, including Wuhan High-Tech Group, Hubei Science and Technology Investment Group, Optics Valley Financial Holdings, BGI Win-Win, and Panlin Capital. According to the pre-IPO shareholding structure, Enbipu Pharmaceutical, a subsidiary of CSPC Pharmaceutical Group, was the largest shareholder of Wuhan Youzhiyou Biopharmaceutical Co., Ltd.

So, what awaits Wuhan Youzhiyou Biopharmaceutical as it defies the trend to list on the Hong Kong stock exchange?

To date, discussions about biotech companies listing on the Hong Kong Stock Exchange with a “B” designation are met with greater caution alongside excitement. The wave of post-IPO price declines since the second half of 2021 has significantly heightened uncertainty surrounding the performance of new biotech listings on the HKEX. However, since the beginning of 2023, the sluggish issuance trend for unprofitable biotech firms in the Hong Kong market has shown signs of improvement.

On the first trading day following the May Day holiday, Luye Bio listed on the Hong Kong Stock Exchange (HKEX), becoming the first unprofitable biotech company to go public in the Hong Kong stock market in 2023. On its IPO day, Luye Bio’s closing share price dropped by more than 30%. In the subsequent months of June, July, and September, Cosmo Pharmaceuticals, Laekna Therapeutics, Kelun-Biotech Biopharmaceutical, and ImmuneOnco all went public under Chapter 18A of the HKEX Listing Rules (“Listed with a ‘B’”), with their share prices remaining stable or rising on their listing days. Notably, Laekna Therapeutics saw its share price surge by over 20% on its IPO debut. As a result, among the unprofitable biotech companies that have gone public on the HKEX this year, four out of five experienced share price gains on their IPO days, while only one declined, generally reversing the trend of such companies breaking their issue price upon listing.

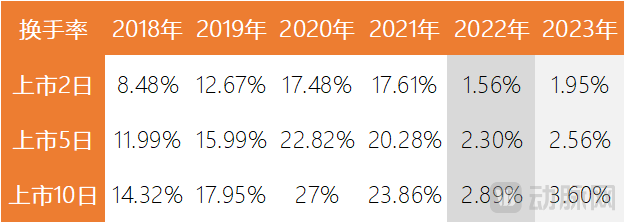

At present, the primary pressure facing pre-revenue biotech companies listed on the Hong Kong Stock Exchange lies in liquidity. A simple assessment using turnover rates reveals that in 2022, the stock liquidity of these pre-revenue biotech firms listed in Hong Kong plummeted to historic lows. Since entering 2023, the liquidity of these stocks has improved slightly, but overall remains at historically low levels.

Average Turnover Rate of Unprofitable Biotech Stocks Listed in Hong Kong Data Source: Calculated by VCBeat based on Choice market data

For biotech companies, the fundamental purpose of going public is to expand financing channels. From an investor’s perspective, low stock liquidity implies significant difficulty in converting holdings into cash. In financial terms, the greater the difficulty in liquidation, the higher the investment premium investors demand as compensation for risk. During periods of overall market downturn, investors have little willingness to hold illiquid assets. In other words, if stock liquidity is low, biotech companies will struggle to raise capital by transferring equity to the general public. Such a listing would provide virtually no substantive benefit to the operational performance of biotech companies.

A further analysis of the liquidity performance of unprofitable biotech companies reveals that even during the 2022–2023 period, there were newly listed “-B” stocks with high liquidity. For instance, Kelun-Biotech Biopharmaceutical, which listed on the Hong Kong Stock Exchange in July 2023, recorded turnover rates of 5.3%, 6.8%, and 10.6% at 2, 5, and 10 days post-listing, respectively, approaching the median levels of “-B” biotech IPOs in 2021. Therefore, at least in terms of liquidity, the performance of unprofitable biotech companies on the Hong Kong stock market shows significant divergence.

Since the market opened its doors to unprofitable biotech companies in 2018, investors in the Hong Kong stock market have gradually adapted to these new investment targets that cannot be measured by traditional metrics. As a new trading system has been established, it is no longer feasible to assess the market performance of individual companies based solely on the common characteristics of their sector.

For Wuhan Youzhiyou Biopharmaceutical Co., Ltd., whether its Hong Kong stock listing journey will proceed as desired depends on an analysis of its products under development.

As a company primarily engaged in the development of innovative drugs, Wuhan Youzhiyou Biopharmaceutical Co., Ltd. boasts a highly robust technological platform and pipeline portfolio.

Wuhan Youzhiyou Biopharmaceutical Co., Ltd. is a pioneer in the independent research and development of bispecific antibody drugs in China. As early as 2012, the company initiated the development of its early-stage pipeline candidate, M802, which became the first independently developed bispecific antibody drug in China to receive Investigational New Drug (IND) approval. Currently, M701, being advanced as its core product, commenced development in 2013 and is the second original bispecific antibody new drug in China to obtain IND approval. Since then, Wuhan Youzhiyou Biopharmaceutical has vigorously promoted the development of M701. In the global race to develop specific therapeutics for malignant ascites and malignant pleural effusion, M701 has consistently remained at the forefront.

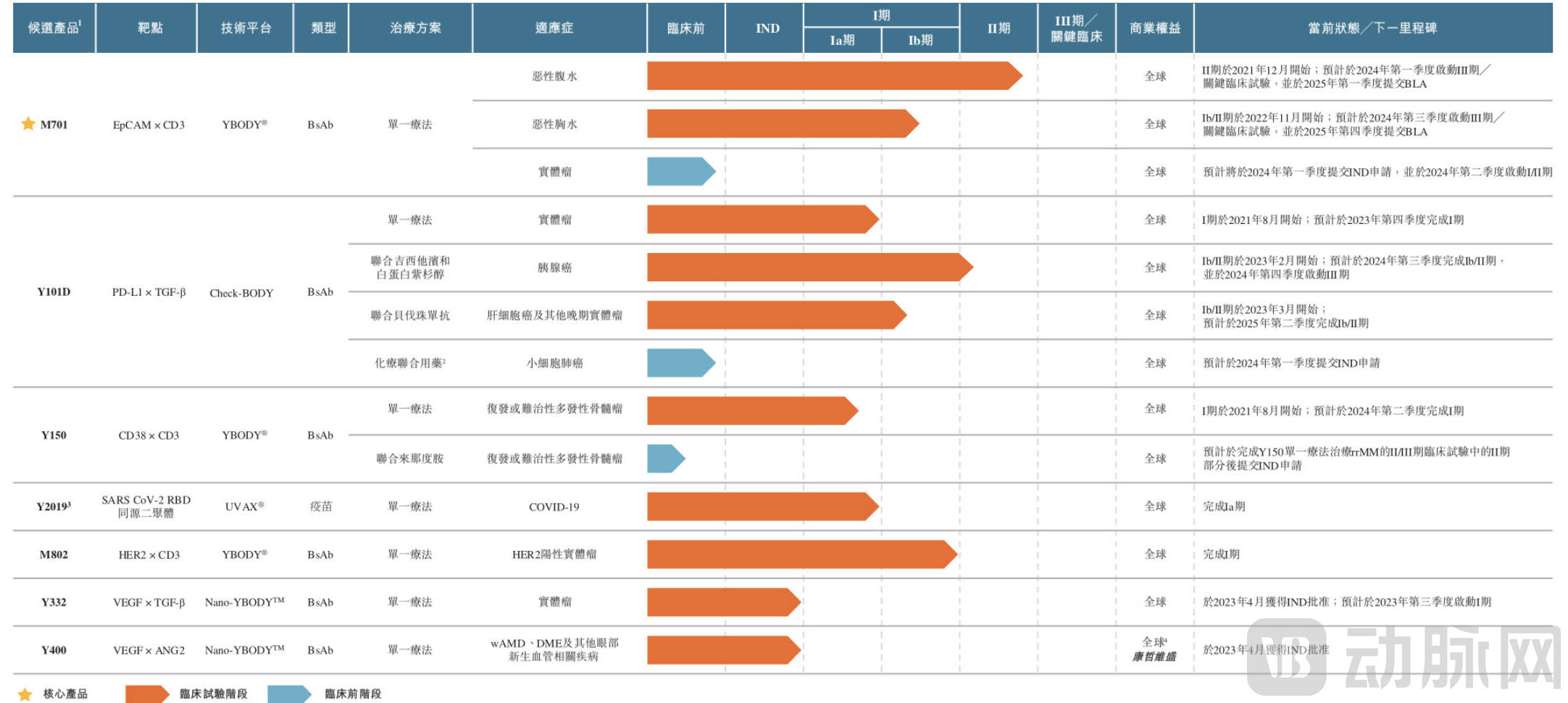

In addition to M701 and M802, Youzhiyou Biopharma has successively expanded its pipeline with new drug candidates such as Y101D, Y332, and Y400. Among these, Y400 has been licensed to Kangzhe Weisheng.

YzyBio’s R&D Pipeline Image Source: Prospectus

All of Wuhan Youzhiyou Biopharmaceutical’s investigational pipeline candidates are developed based on its in-house technology platforms. Since its establishment, the company has developed four technology platforms, including its proprietary YBODY® platform, Check-BODY platform, and Nano-YBODY™ platform, as well as the UVAX® platform co-developed with the Wuhan Institute of Virology.

Among these, the YBODY® platform focuses on the development of asymmetric human immunoglobulin G (IgG)-class bispecific antibodies featuring a single-chain variable fragment–antigen-binding fragment–crystallizable fragment (scFv-Fab-Fc) structure. M701, M802, and Y150, three T-cell-engaging bispecific antibody candidates in Wuhan Youzhiyou Biopharmaceutical Co., Ltd.’s pipeline, were all developed using the YBODY® platform. The Check-BODY platform is specifically dedicated to the development of symmetric tetravalent bispecific antibodies, yielding Y101D. The Nano-YBODY™ platform is specifically designed for the development of symmetric tetravalent bispecific antibodies based on single-domain antibodies, achieving higher binding affinity, greater stability, lower immunogenicity, and improved product yield. Leveraging the Nano-YBODY™ platform technology, Wuhan Youzhiyou Biopharmaceutical Co., Ltd. discovered and developed Y400 and Y332. Furthermore, in collaboration with the Wuhan Institute of Virology, the UVAX® platform was utilized during the COVID-19 pandemic to develop Y2019 for combating SARS-CoV-2.

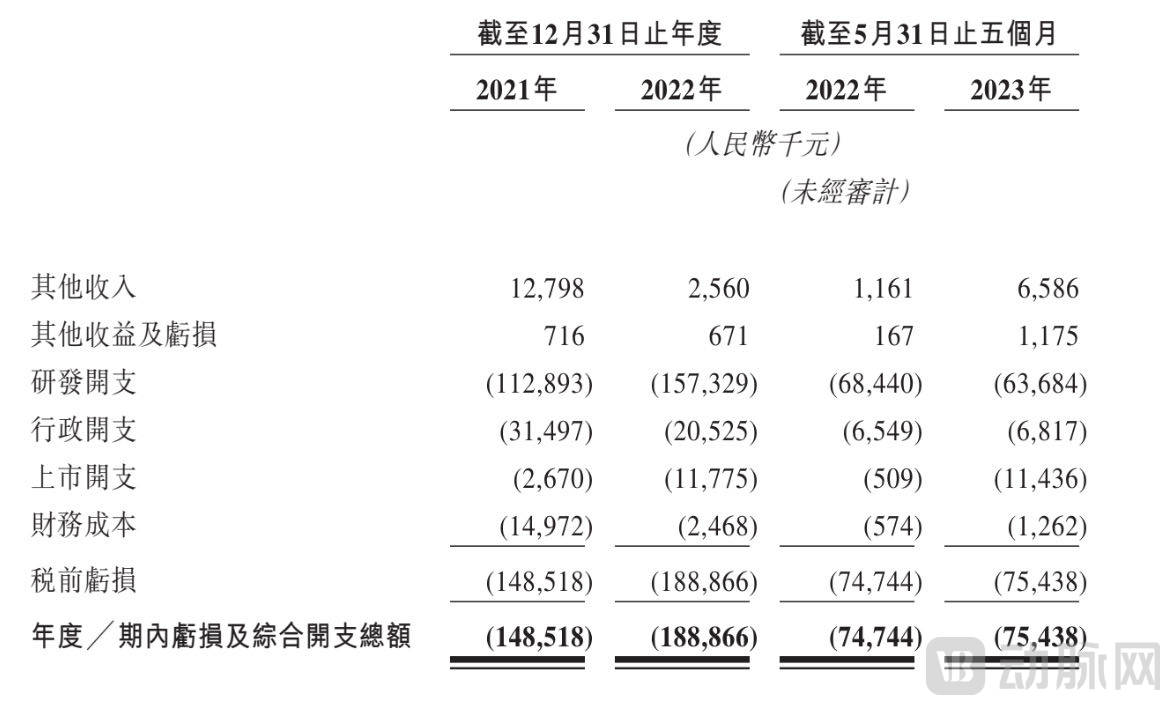

Of course, behind its robust core capabilities lies long-term investment in capital and personnel. Since its establishment 13 years ago, Wuhan Youzhiyou Biopharmaceutical Co., Ltd. has generated no revenue from its primary business operations. Apart from several rounds of external financing, its main sources of funding have been government subsidies, with protein antigen sales contributing a small but unstable amount of income. In contrast, as its core pipeline progresses into the mid-to-late stages of development, R&D expenditures have risen year by year.

Revenue and Expenditure Structure of Youzhiyou Biopharma Image Source: Prospectus

According to the prospectus, Wuhan Youzhiyou Biopharmaceutical Co., Ltd. incurred R&D expenses of RMB 58.2 million, RMB 78.5 million, and RMB 49.4 million for its bispecific antibody new drug pipeline in 2021, 2022, and the five months ended May 31, 2023, respectively, placing increasing strain on its already limited cash flow. In October 2022, the company completed its Series C financing, raising RMB 153.5 million in cash, which slightly alleviated its financial pressure. However, within just six months, the company’s cash reserves were halved. In addition to routine operational expenditures, the continuous R&D of its pipeline places significant demands on cash flow.

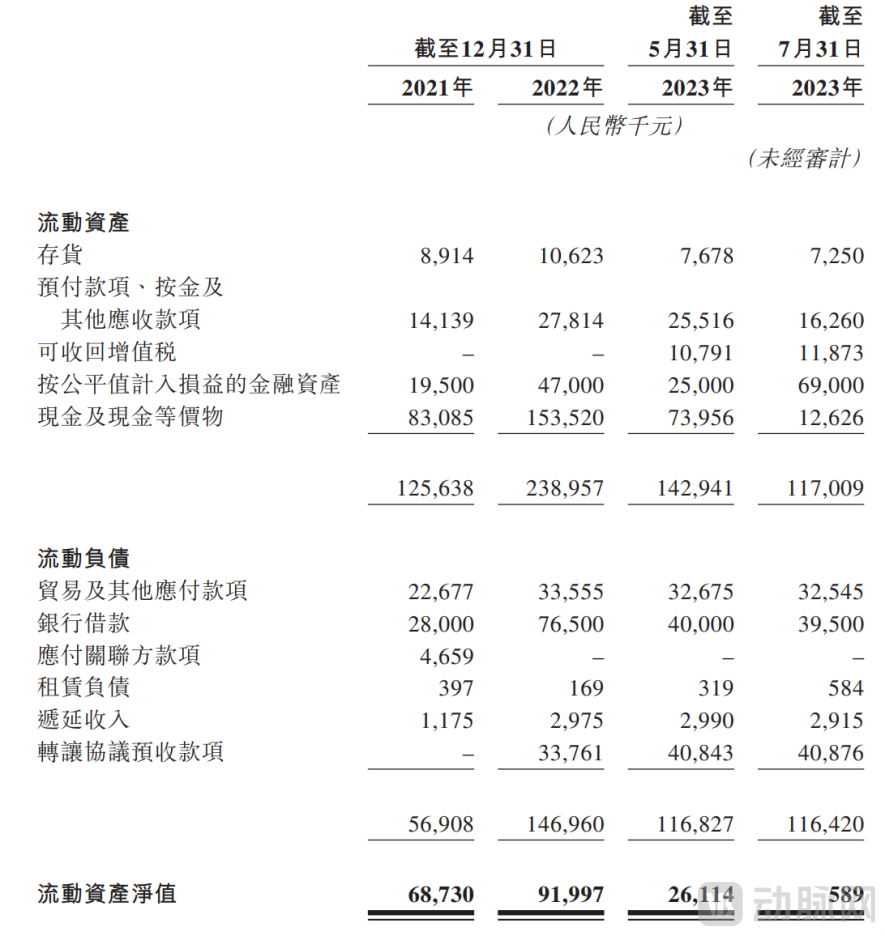

Balance Sheet of Youzhiyou Biologics Image source: Prospectus

Over the past decade, Youzhiyou Biopharmaceutical has allocated the largest share of its R&D funding to M701.

Data shows that between 2013 and 2020, the total R&D expenditures for M701 consistently exceeded those of any other drug candidate under development at the time. However, M701 truly became a financial black hole after 2021. According to the prospectus, driven by the initiation of Phase II clinical trials for malignant ascites in December 2021 and the expansion into other indications, R&D spending on M701 rose from RMB 9.9 million in 2021 to RMB 23.5 million in 2022. By 2023, the burn rate for M701 accelerated further; in the first five months alone, it consumed RMB 25.5 million, accounting for approximately 40.1% of the total R&D expenditures during the same period. Whether such substantial investment in M701 is justified will be analyzed in detail later.

In fact, M701 is not an isolated case; the advancement of any innovative drug pipeline entails substantial capital investment. For instance, in February 2021, Wuhan Youzhiyou Biopharmaceutical Co., Ltd. initiated the development of Y101D, a bispecific antibody injection targeting PD-L1 and TGF-β, intended for the treatment of highly challenging solid tumors such as pancreatic cancer, cholangiocarcinoma, and small cell lung cancer. In 2021, the company invested RMB 27.1 million to complete the preclinical development of Y101D in preparation for its Investigational New Drug (IND) application. In 2022, an additional RMB 13.6 million was spent to advance the clinical research of Y101D. During the first five months of 2023, Wuhan Youzhiyou Biopharmaceutical invested RMB 18.7 million in Y101D to conduct two Phase Ib/II clinical trials evaluating its combination therapy. Without significant financial backing, there can be no new drugs.

For Wuhan Youzhiyou Biopharmaceutical Co., Ltd., robust technical capabilities provide a solid foundation, instilling confidence to press on even in the absence of revenue. However, funding remains a pressing challenge at present, which is likely a key reason why the company has persisted in its efforts to list on the Hong Kong Stock Exchange.

Next, let’s examine whether the drug on which Wuhan Youzhiyou Biopharmaceutical Co., Ltd. has placed heavy bets is worth it.

M701 targets malignant ascites and malignant pleural effusion, which are among the most common complications in cancer patients and pose significant clinical challenges. Clinically, malignant ascites can arise from the growth of primary or metastatic malignancies within the peritoneum. This complication is frequently observed in patients with various cancers, including ovarian, breast, gastric, lung, and pancreatic cancers. Malignant pleural effusion has a broader prevalence; data indicate that it occurs in approximately 45% of lung cancer patients, 2%–11% of breast cancer patients, 41.6% of lymphoblastic lymphoma patients, and 33% of ovarian cancer patients.

Typically, malignant ascites and malignant pleural effusion are associated with malignancies involving multiple organs and a poor prognosis, making them extremely difficult to treat. At present, therapeutic options for patients who develop malignant ascites or malignant pleural effusion are very limited, particularly for those with advanced-stage cancer, where management is largely confined to symptomatic relief.

In clinical practice, conventional paracentesis, diuretics, intraperitoneal or intrapleural infusion of chemotherapeutic agents or anti-angiogenic drugs, and immunosuppressants used in conjunction with paracentesis are employed to treat malignant ascites and malignant pleural effusion. However, these measures address only the symptoms rather than the underlying cause, may induce new complications, and can delay further definitive treatment. For instance, intraperitoneal or intrapleural administration of anti-angiogenic agents can downregulate tumor cell surface factors associated with angiogenesis and vascular permeability, modulate related signaling pathways (such as VEGF), thereby inhibiting tumor growth and differentiation, exerting anti-tumor effects, and reducing fluid accumulation. Nevertheless, this approach has limited efficacy and a high recurrence rate, and is not recommended by clinical guidelines.

If judged solely by the number of patients, malignant ascites and malignant pleural effusion do not represent large indications; however, treatment for these conditions is costly. Taking intraperitoneal and intrapleural infusion of anti-angiogenic drugs as an example, the annual treatment cost per patient can reach tens of thousands of yuan. Therefore, despite a scarcity of therapeutic options, the market size for treatments targeting malignant ascites and malignant pleural effusion still amounts to tens of billions of yuan. According to the prospectus of Wuhan Youzhiyou Biopharmaceutical Co., Ltd., between 2018 and 2022, the domestic market size for malignant ascites treatment grew from RMB 9.9 billion to RMB 10.8 billion, while the market size for malignant pleural effusion therapies increased from RMB 10.9 billion to RMB 11.7 billion. With the emergence of more effective innovative therapies, the market size for treatments targeting malignant ascites and malignant pleural effusion is expected to continue expanding.

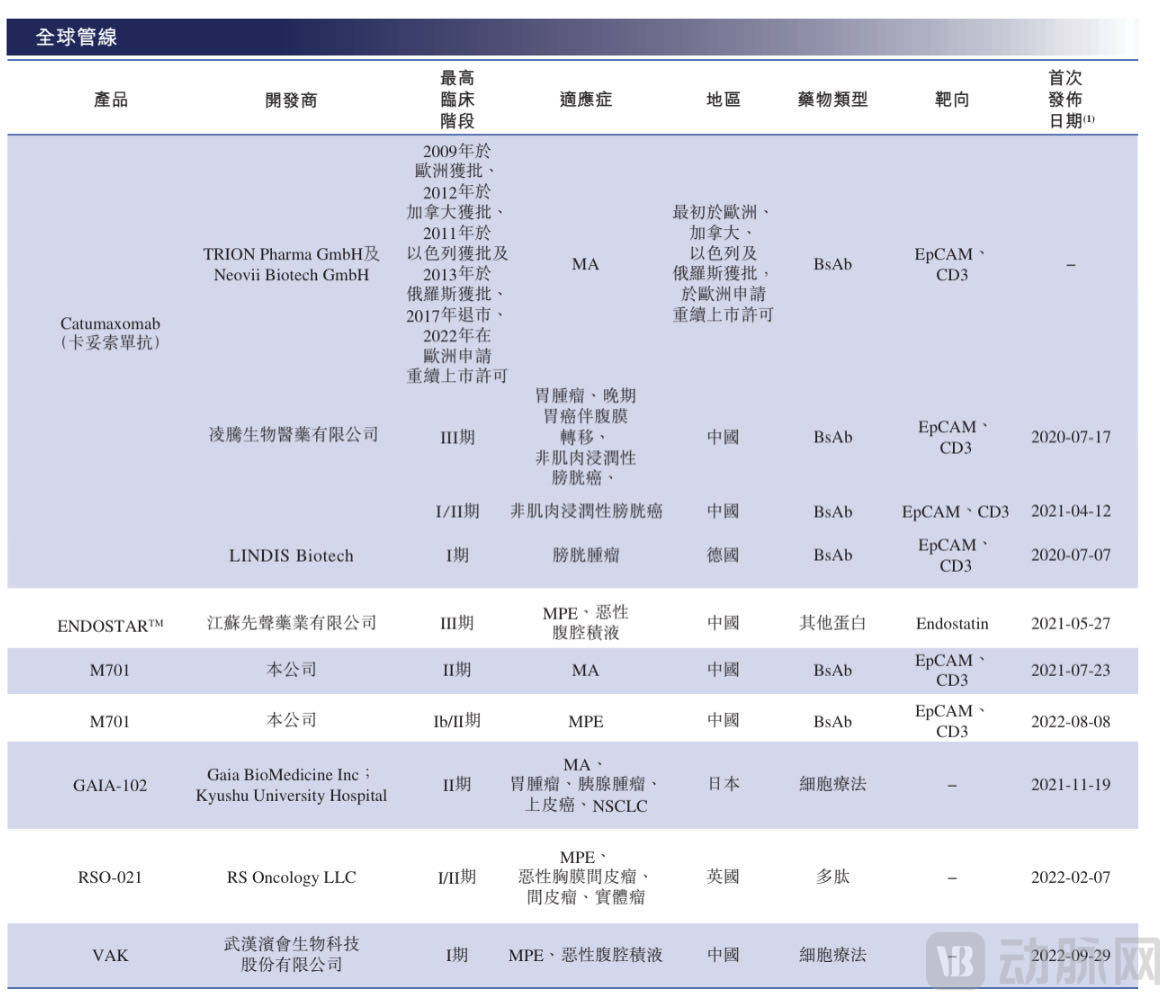

In fact, the development of targeted therapies for malignant ascites and malignant pleural effusion to address this significant clinical unmet need has long been a key focus in new drug research and development worldwide. In 2009, catumaxomab became the first bispecific antibody approved globally for the treatment of malignant ascites. However, due to suboptimal commercial performance, catumaxomab was subsequently withdrawn from the market. In August 2022, the developer of catumaxomab submitted an application to the European Medicines Agency (EMA) for renewal of its marketing authorization, which is currently under review.

Innovative Drugs Under Global Development for Malignant Ascites and Malignant Pleural Effusion Image Source: Prospectus

At present, in addition to catumaxomab, there are six other innovative drug pipelines worldwide specifically developed for the treatment of malignant ascites or malignant pleural effusion that have entered clinical research. Apart from the bispecific antibody adopted by Wuhan Youzhiyou Biopharmaceutical Co., Ltd., these investigational pipelines include innovative therapeutic modalities such as cell therapies and peptide drugs. However, compared with bispecific antibodies, which already have marketed products, peptide drugs are still in the early stages of clinical development. Although cell therapies have demonstrated significant efficacy, they are costly and require further optimization.

Among all relevant products under development, Wuhan Youzhiyou Biopharmaceutical’s M701 is relatively advanced in its development progress. Apart from Lingteng Bio, which is also developing catumaxomab, and Simcere Pharmaceutical, which is targeting Endostatin, Youzhiyou Biopharmaceutical has advanced M701’s indication for malignant ascites to Phase II clinical trials. This places it in the first tier of innovative drug development, with the potential to become a blockbuster therapy for malignant ascites and malignant pleural effusion. In this sense, the substantial upfront investment made by Youzhiyou Biopharmaceutical in M701 is well justified.

Of course, M701 is not the entirety of Wuhan Youzhiyou Biopharmaceutical Co., Ltd. For the company, the near- to mid-term outlook hinges on M701, while the long-term prospects depend on its pipeline reserves. Both Y101D, a fast-follow candidate, and Y150, which continues to receive increased investment, are highly anticipated.

From M701, targeting tumor complications, to Y101D, aimed at pancreatic and biliary tract cancers, Wuhan Youzhiyou Biopharmaceutical Co., Ltd. has been striving to tackle the most challenging issues in clinical oncology treatment. We also hope to see such a hardcore biotech company continuously surpass itself and achieve success step by step.