Who Is Rebuilding the 'Medical Aesthetics Money Machine'? A Comparative Analysis of Bloomage BioTechnology and HANMI

IMEIK

Developer of Biomedical Soft Tissue Repair Materials

Bloomage Biotech

Developer of bioactive substance products, producer of hyaluronic acid raw materials

In the just-concluded month of September, Kweichow Moutai was anything but quiet. It first launched the “Moutai-flavored Latte” in collaboration with Luckin Coffee, and later introduced “liquor-filled chocolates” with Dove. Each move successfully tapped into the industry’s restless sentiment. In fact, the medical sector also has its own “Moutai-like” entity—often referred to as the “Aesthetic Medicine Moutai.” This moniker primarily highlights the exceptionally high gross profit margins characteristic of the upstream segment of the medical aesthetics industry.It is reported that Imeik’s gross profit margin reached as high as 94.85% in 2022, nearly 3 percentage points higher than that of Kweichow Moutai in the same year.。

Recently, Imeik released its 2023 semi-annual report. During the period, the company achieved operating revenue of RMB 1.459 billion, a year-on-year increase of 64.93%; net profit amounted to RMB 963 million, representing a year-on-year growth of 64.66%.Among them, the second quarter achieved revenue of RMB 829 million, a year-on-year increase of 82.6%, hitting a record high.。

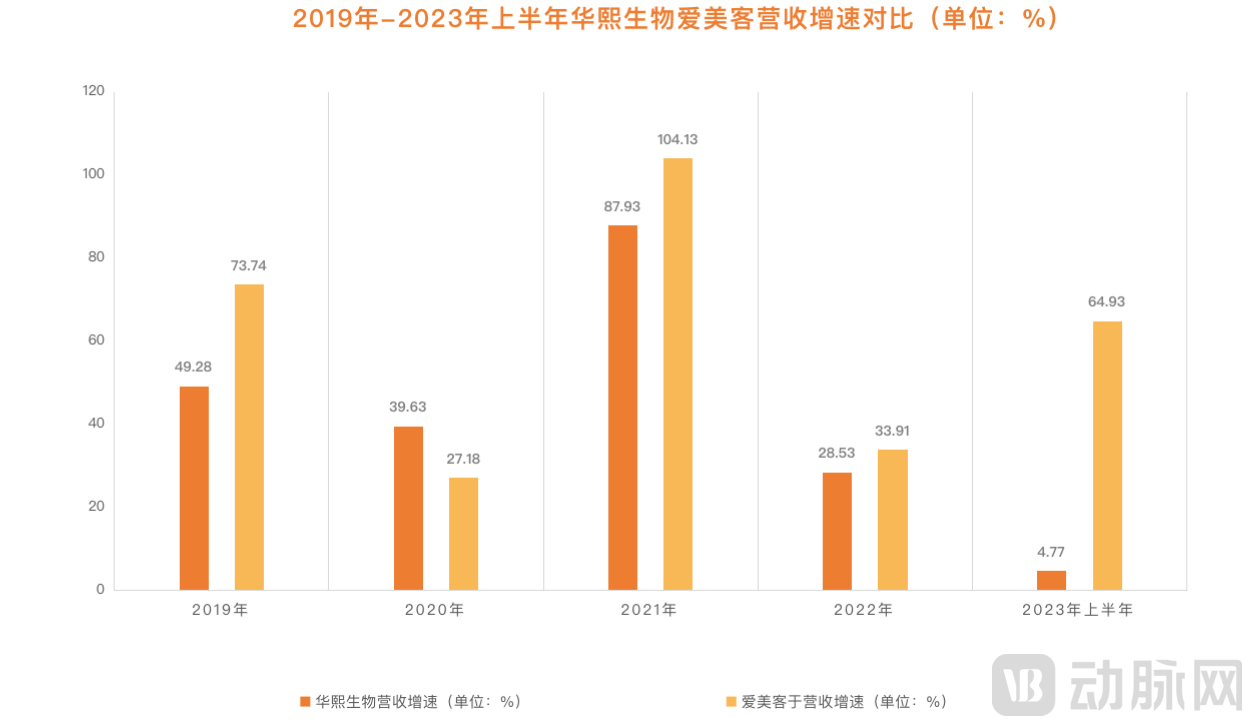

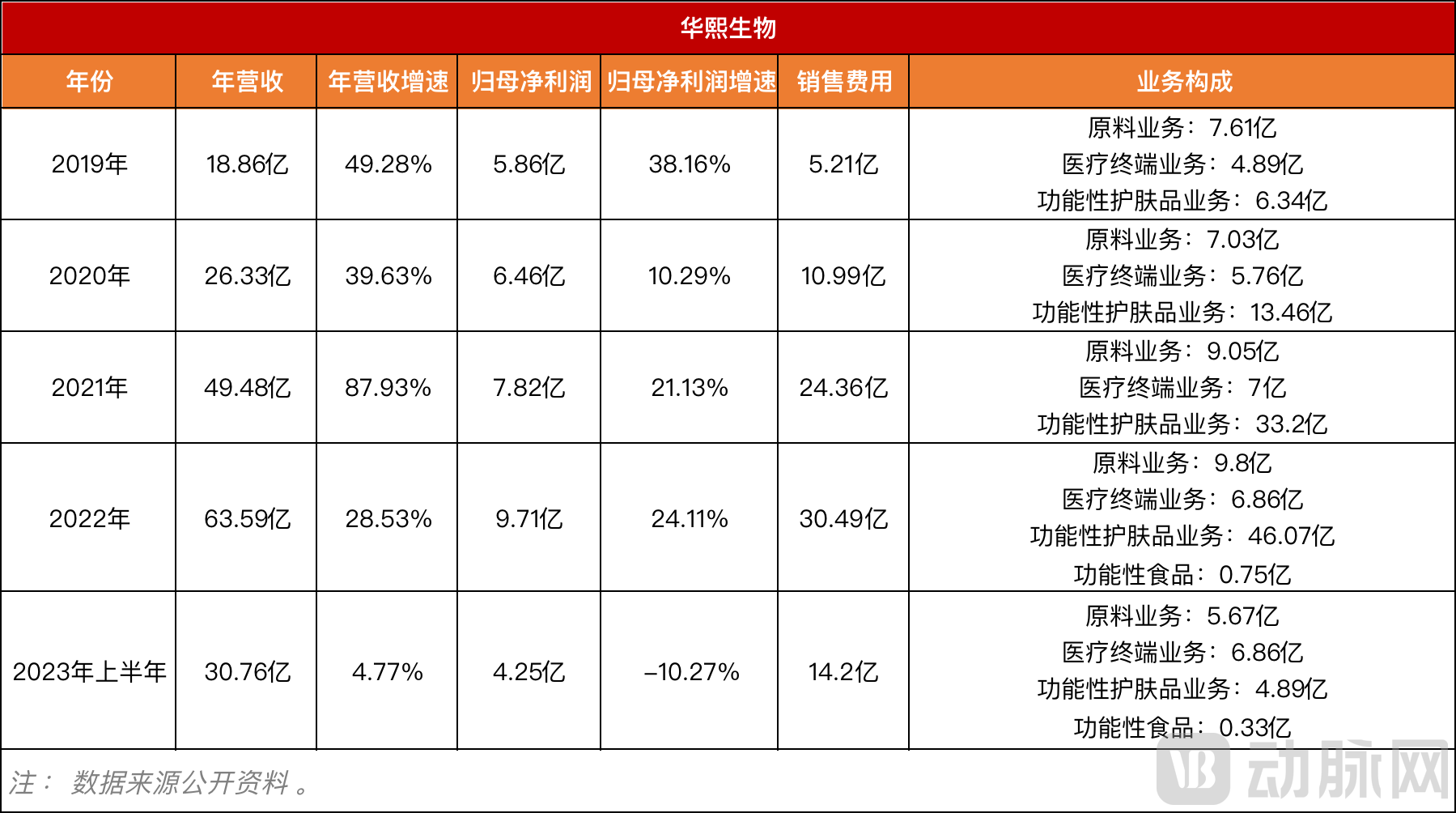

Unlike Imeik, whose performance has continued to surge, Bloomage Biotech, known as the “first hyaluronic acid stock,” reached a business turning point in the first half of 2023. According to its semi-annual report, although Bloomage Biotech’s revenue reached RMB 3.076 billion—nearly double that of Imeik—the growth rate declined significantly, standing at only 4.77%.In addition, the net profit was RMB 425 million, a year-on-year decrease of 10.27%, marking the first decline in net profit for Bloomage Biotech since its listing in 2019.。

Given these data, everyone must have some questions:Why Do Two Companies with the Same Blockbuster Product Have Vastly Different Performance Results?Looking more closely, why is Bloomage Biotech’s net profit nearly half that of Imeik despite generating higher revenue, and where exactly did the money go? Furthermore, against the backdrop of shrinking margins in the hyaluronic acid market, what preparations have these two companies made, and what is the current status of their progress?

If these answers can be unraveled,Perhaps we are witnessing the quiet unveiling of a transformation hidden within the medical aesthetics industry.。

Bloomage Biotech Heads Left, Imeik Goes Right

2021 was regarded as the inaugural year for hyaluronic acid, during which Bloomage Biotech and Imeik both experienced a significant surge in performance. According to their annual reports for that year, Bloomage Biotech’s annual revenue growth rate reached 87.93%, while Imeik’s soared to 104.13%.

In 2022, although the entire medical aesthetics market suffered a significant impact due to the pandemic, Bloomage Biotech and Imeik still maintained a revenue growth rate of around 30%. Bloomage Biotech’s revenue exceeded the RMB 6 billion mark for the first time, while Imeik chose to list on the Hong Kong Stock Exchange during this period. Both companies achieved their own milestones, so it can be largely considered a “draw.”

Figure 1. Comparison of Revenue Growth Rates Between Bloomage Biotech and Imeik in the First Half of 2019–2023 (Data Source: Annual Reports)

However, in 2023,Divergences Finally Begin to Emerge, by examining the semi-annual report, Bloomage Biotech’s revenue growth rate was merely 4.77%, while its net profit growth rate declined for the first time. In stark contrast, Imeik reported both revenue and net profit growth rates exceeding 60%, making the disparity particularly pronounced. So, what exactly happened?

In fact,Parting ways was destined from the very beginning.。

First, in terms of business orientation, Bloomage Biotech targets the C-end (consumers), while Imeik targets the B-end (businesses).. As the two giants in the hyaluronic acid industry, Bloomage Biotech and Imeik both initially targeted the B2B market. However, a shift occurred in 2018, when Bloomage Biotech fully entered the C2C market, while Imeik remained committed to the B2B sector.

There are certainly reasons for this. It is reported that Bloomage Biotech was initially focused on the upstream supply of raw materials and did not enter the medical terminal market until 2012, a full three years later than Imeik. As a result, Bloomage Biotech recognized early on that it would be difficult to compete with Imeik in hyaluronic acid terminal products, and thus began to shift its focus toward functional skincare products. Furthermore, Bloomage Biotech’s listing on the STAR Market in 2019 significantly boosted its visibility and public attention, further accelerating its transition to consumer-facing (ToC) business operations.

Amidst these subtle, imperceptible changes,The market positioning of both has also been quietly shifting.。

Figure 2. Bloomage Biotech’s Operational Performance in the First Half of 2019–2023 (Source: Annual Reports)

Zhao Yan, Chairman of Bloomage Biotech, has emphasized on more than one occasion, “Bloomage Biotech is not a medical aesthetics company, but a biotechnology and biomaterials company.”, aiming to convey that Bloomage Biotech is not solely focused on the upstream segment of the medical aesthetics industry, but rather emphasizes a comprehensive layout across the entire industrial chain. This strategy is clearly reflected in its business composition. According to annual report data, Bloomage Biotech operates across three major sectors: raw materials, medical aesthetics, and skincare products. Among these, the medical aesthetics business accounts for the smallest proportion, while the majority of revenue comes from functional skincare products. Taking 2021 as an example, Bloomage Biotech’s medical terminal business generated RMB 700 million, accounting for 14.1% of total revenue, whereas the functional skincare business reached RMB 3.32 billion, representing 69.1%.

Figure 3. Imeik’s Operational Performance in the First Half of 2019–2023 (Source: Annual Reports)

Unlike Bloomage Biotech, which is moving toward “comprehensive diversification,” Imeik has chosen to deepen its focus within the medical aesthetics sector. It is reported that Imeik has launched as many as five products in the hyaluronic acid category alone, comprehensively covering the entire market from low-end to high-end segments. In terms of business composition, nearly all of its revenue comes from the medical aesthetics track; data show that, aside from its skincare business, which accounts for less than 1%,Nearly 99% of Imeik’s business is concentrated in the medical aesthetics end-market., which also lays the foundation for its high profitability.

Divergent market positioning has also led the two to adopt vastly different paths in marketing promotion.

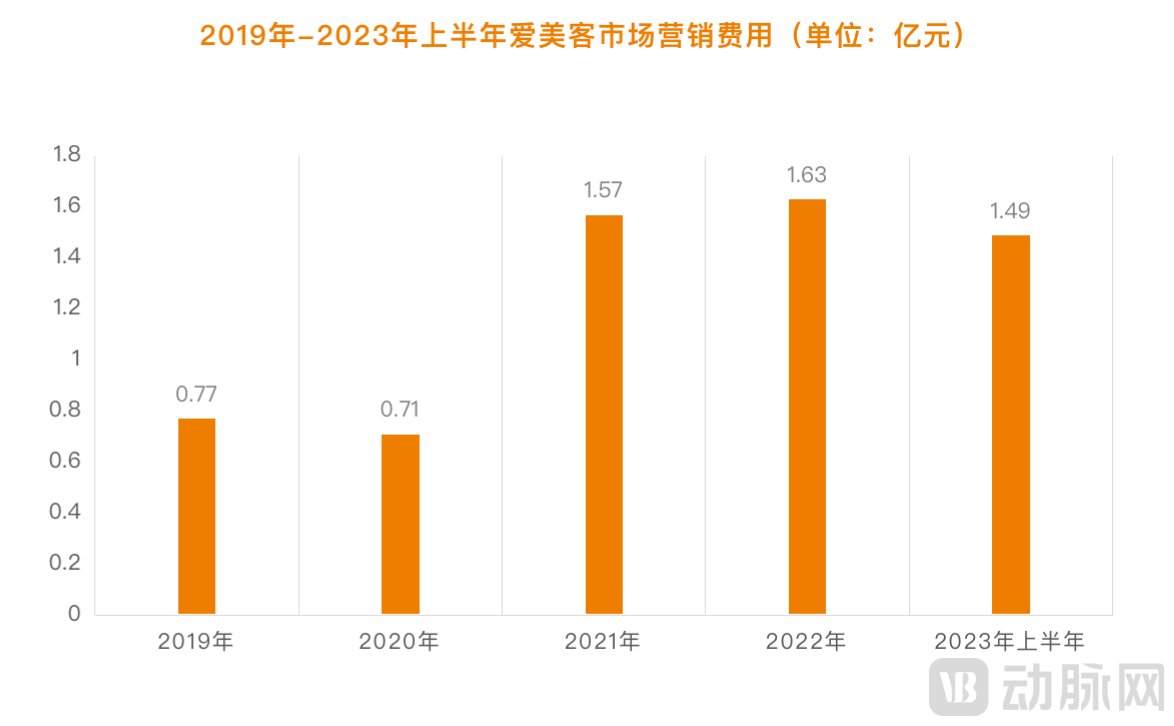

As previously mentioned, Bloomage Biotech primarily targets the consumer (C-end) market, with its core business focused on skincare products, resulting in a heavy reliance on marketing. According to annual report data, the company’s selling expenses reached RMB 2.436 billion in 2021, representing a year-on-year increase of 121.62%. In 2022, these expenses further rose to RMB 3.049 billion, accounting for nearly half of its total revenue.

In response, Bloomage Biotech stated that this was primarily due to the expansion of its sales team, which led to a year-on-year increase in employee compensation. Additionally, the company has vigorously expanded its online sales channels, increased information flow advertising on e-commerce platforms such as Douyin, and strengthened collaborations with mainstream influencers on platforms like Tmall and Douyin, resulting in a significant rise in online promotion and advertising expenses.The persistently high customer acquisition costs have also directly resulted in Bloomage Biotech’s net profit falling short of Imeik’s.。

Figure 3. Sales Expenses of Imeik from 2019 to the First Half of 2023 (Source: Annual Reports)

So, how exactly has Imeik managed to maintain such strong net profit margins? According to annual report data analysis, over the past five years, Imeik’s selling and marketing expenses have remained stable at around RMB 100 million. Even in 2021, when its performance surged by 104.13%, the company’s selling and marketing expenses amounted to only RMB 157 million, accounting for just 10.8% of total revenue.

Behind the data lies Imeik’s unique market strategy. On one hand, Imeik, which focuses on B2B business, has consistently adhered to"Direct sales as the primary channel, with distribution as a supplementary channel"differentiated marketing model, thereby securing greater initiative for itself; on the other hand, according to its own disclosures, in the past few years,Imeik Has Been Strengthening Its Marketing System Construction, driving brand value growth and sustaining volume expansion of core products. It is for this reason that Imeik has been able to consistently maintain a net profit margin above 60%.

Therefore, in retrospect, although both companies are giants in the hyaluronic acid industry, their divergent initial choices led to distinctly different growth trajectories. Bloomage Biotech pivoted to the consumer (C-end) market, targeting the larger skincare sector. However, due to intense competition and its late entry, the company had to incur higher marketing costs, resulting in continuously shrinking profit margins. In contrast, Imeik remained focused on the business-to-business (B-end) market, steadily expanding its profit margins by continuously strengthening its product capabilities and broadening its market channels.

As Hyaluronic Acid Fades, Whose New Story Is More Compelling?

Although Imeik is currently still in a state of high growth, this does not mean that Imeik can “rest easy.” In fact, Imeik is also facing its own dilemmas.

The most intuitive manifestation lies in Imeik's substantial R&D investments in recent years. According to financial report data, Imeik’s R&D expenditure reached RMB 173 million in 2022, a 69.2% increase from RMB 102 million in 2021. Furthermore, in the first half of this year, Imeik continued to ramp up its efforts, with R&D spending rising by 61% to RMB 104 million.

The reason for this is stillStemming from Imeik's concerns about its reliance on a single blockbuster product to sustain long-term healthy corporate development, as competitors continue to enter the market, the first-mover advantages of its two core products, HiTi and Ru Bai Angel, will gradually dissipate over time, making it imperative to identify new growth drivers for revenue.

Furthermore, as the hyaluronic acid sector becomes increasingly crowded, prices have been declining year by year across the entire value chain, from raw materials to end products. According to a Frost & Sullivan report, the average price of hyaluronic acid raw materials decreased gradually from RMB 210 per gram in 2017 to RMB 124 per gram in 2021, representing a drop of over 40%. Meanwhile, the price of end-product hyaluronic acid formulations fell from approximately RMB 1,557 per vial in 2018 to RMB 1,111 per vial in 2021, significantly compressing overall profit margins.

Therefore, whether it is Bloomage Biotech, which has already encountered business bottlenecks, or Imeik, which remains in a phase of rapid growth,have all been striving to identify new business growth curves in recent yearsSo, how did each of them proceed? Whose “new product” is more competitive? VCBeat conducted an analysis based on publicly available data and information.

Let's start with Bloomage Biotech.。

After 2018, Bloomage Biotech fully entered the consumer market.Strategic focus is shifting toward efficacy-based skincare. According to financial report data, although Bloomage Biotech’s overall revenue after its transformation is quite substantial, the nature of its functional skincare products leans more toward consumer goods, necessitating significant marketing investment. Furthermore, as Bloomage Biotech entered the functional skincare sector at a later stage, breaking through in this highly competitive market, where space is nearing saturation, remains no easy task.

After finding that efforts in the efficacy-based skincare segment yielded little reward, Bloomage Biotech began cultivating a new growth driver: food-grade hyaluronic acid, which falls under its core business ofFunctional Food Business, and in 2021, it launched three major product lines: the hyaluronic acid water brand “Shuiji Quan,” the hyaluronic acid food brand “Hei Ling,” and the hyaluronic acid fruit drink brand “Xiu Xiang Jiao Luo.” However, the results have been minimal thus far. The revenue reached RMB 75 million in 2022 and RMB 33 million in the first half of 2023, which is almost negligible compared to the total revenue. This is mainly because its products have been highly controversial, with public opinion even questioning them as a “intelligence tax.”

In fact, both functional skincare products and functional foods have relatively low technical barriers, making it difficult for Bloomage Biotech to establish a "moat." Therefore, Bloomage Biotech is also exploring frontier tracks in the upstream segment of the medical aesthetics industry, with its primary focus onBotulinum ToxinandCollagen Sector。

On May 7, 2015, Bloomage Biotech and the South Korean biopharmaceutical company Medytox signed a joint venture agreement to establish Huaxi Medytox in Hong Kong. The joint venture was created to develop, expand, and sell specific injectable Type A botulinum toxin products and other medical aesthetic products manufactured by Medytox in mainland China.However, after eight years of preparation, its recent plans to deploy botulinum toxin in China through a partnership with Medytox have been completely terminated., Bloomage Biotech’s “face-slimming injection” business has come to naught.

The botulinum toxin market has stumbled, prompting Bloomage Biotech to shift its focus to the collagen sector. In the first half of 2022, Bloomage Biotech officially entered the collagen industry by acquiring Yierkang Biology. By late August of the same year, it launched collagen raw material products, announcing its intention to establish a comprehensive presence across the entire collagen industry chain. According to the recently disclosed record of investor relations activities,Bloomage Biotech currently has 7 to 8 types of collagen under development., has achieved the preparation of recombinant collagen macromolecules and completed the market launch of recombinant type III humanized collagen raw material products in August.

However, it must be recognized that Bloomage Biotech entered the collagen sector relatively late and does not possess a distinct competitive advantage. The company, which originally built its business on collagen,Giant BiogeneDeveloped proprietary bioactive recombinant collagen ingredients in 2000, and launched China’s first recombinant collagen product classified as a medical device in 2011. Additionally, it is known as the “first stock for injectable collagen.”Jinbo BiotechIt is also scheduled to be successfully listed on the Beijing Stock Exchange this July.

However, Bloomage Biotech has its own strategic vision, as disclosed in public records,It has currently invested nearly RMB 2 billion in the field of synthetic biology., and has launched various research projects on bioactive substances through this technology, including collagen. However, to date, Bloomage Biotech has not yet commercialized any products manufactured using synthetic biology technology; only certain raw materials are in the pilot-scale production stage. The investment required for pilot-scale production encompasses R&D, operations, personnel, and facility construction, among other factors, resulting in higher costs.

Back to Imeik。

In fact, Imeik and Bloomage Biotech share certain similarities in their pursuit of new growth curves, as both have targeted the botulinum toxin and collagen segments, which hold significant promise in the medical aesthetics sector. However, their development paths and project progress differ.

In September 2018, Imeik signed a cooperation agreement with South Korea’s Huons regarding Type A botulinum toxin products in China. Under the terms of the agreement, Huons authorized Imeik to import, register, and distribute its Type A botulinum toxin products within the Chinese market, while Imeik assumed responsibility for conducting clinical trials and submitting registration applications for these products in China.

To date,Imeik’s “Botulinum Toxin Type A for Injection” has completed Phase III clinical trials and is currently in the registration application stage., if it successfully obtains marketing approval, it will become the fifth botulinum toxin product in China. In fact, Aimeike is not the only player in the botulinum toxin field; other companies includeFosun Pharma, Huadong Medicine, Haohai Biological TechnologyThese products have also entered the drug registration application phase, and are inevitably poised to become formidable competitors to Imeik in the market launch of botulinum toxin products.

In the field of collagen, Imeik acquired Harbin Peiqilong Biopharmaceutical Co., Ltd. in 2022 with RMB 350 million of its own funds. Following the acquisition, Imeik has sought to explore additional market opportunities in the application of collagen products. However, no substantial progress has been publicly disclosed to date; it has only been indicated that related business activities are underway.

In addition, Imeik has also turned its attention to weight-loss drugs, mentioning in its 2022 annual report that there areLiraglutide Injection, Semaglutide InjectionandDeoxycholic Acid InjectionThree weight management products are under development. Among them, the liraglutide injection has completed Phase I clinical trials, while the other two products are in the preclinical research stage.

However, this does not mean that Imeik can let its guard down. In fact, the vast weight-loss market is not entirely a blue ocean. Currently, there are only two GLP-1 receptor agonist weight-loss drugs approved globally: Novo Nordisk’s semaglutide and liraglutide. Meanwhile, several Chinese companies, including Huadong Medicine, Renee Biopharm, Sciwind Biosciences, and Innovent Biologics, have made rapid progress. This means that there are numerous drug candidates targeting GLP-1R for weight loss in the global pipeline. In terms of development progress, Imeik’s investigational products lag behind many competitors, making it difficult to gain a first-mover advantage.

Therefore, whether it is Bloomage Biotech, which is mired in the dilemmas of diversified development, or Imeik, which is striving to break free from its reliance on a single product, both appear to be navigating a challenging path of transformation, facing both opportunities and obstacles. However, it is too early to draw conclusions about the future. As Zhao Yan, Chairman of Bloomage Biotech, stated during the performance briefing, current investments in innovation are made with a five- to ten-year horizon in mind.Therefore, whether they can break out ultimately depends on whether they can achieve disruptive breakthroughs in relevant technologies and densely integrate their existing advantages with their new product pipelines.。

The Second Half of the Medical Aesthetics Race: Who Will Ultimately Prevail?

The medical aesthetics sector has experienced its ups and downs in recent years, shedding its aura of mystery; yet, it is undeniable thatIt remains a lucrative business in China.。

According to Frost & Sullivan, China has become the world’s third-largest medical aesthetics market, with its market size reaching RMB 189.12 billion in 2021 and projected to reach RMB 399.81 billion by 2026.CAGR of 16.2% over the next five years。

Its growth logic lies in the vast demand scenarios. Currently, the market penetration rate of China's medical aesthetics industry is relatively low. In 2018, the number of medical aesthetic procedures in China was 14.8 per thousand people, which was only half that of Japan and less than one-fifth of South Korea’s, indicating significant room for future growth. On the other hand, with the increase in penetration rates and repurchase frequency among existing users, the market demand for medical aesthetics in China will continue to expand further. According to the "SoYoung 2022 White Paper on the Medical Aesthetics Industry,"In 2023, the number of medical aesthetics consumers in China is projected to reach 23.54 million.。

Furthermore, the continuous integration of innovative technologies into the medical aesthetics sector, coupled with the increasing maturity of existing techniques and the industry’s progressive compliance under a series of regulatory policies, has further bolstered confidence in its rapid future growth.

It is precisely for this reason that in recent years, not only have typical medical aesthetics companies represented by Bloomage Biotech and Imeik continued to increase their investments, but a large number of pharmaceutical companies have also been crossing over into the medical aesthetics sector through various channels, such asHuadong Medicine, TeYi Pharmaceutical, Yunnan Baiyao, Fosun Pharma, Jiangsu Wuzhong, Xingkerong Medicine, Sihuan Pharmaceutical, China Medical Systemetc.

Through observation, VCBeat has found that its focus is mainly concentrated on two aspects,On one hand, expanding the medical aesthetics business pipeline through acquisitions, for example, Fosun Pharma’s subsidiary had its licensed-in Type A botulinum toxin accepted for review by the National Medical Products Administration in July 2023.

On the other hand, efforts are being made to strengthen market channels., taking Xihong Pharmaceutical, which focuses on the regenerative medical aesthetics sector, as an example, it recently announced a strategic partnership with So-Young Technology. The collaboration aims to leverage So-Young’s extensive expertise in online visibility, product operation capabilities, and supply chain management to drive market growth for its two core products: “skin boosters” and “poly-L-lactic acid fillers.”

Therefore, although the medical aesthetics industry remains a growth market, with more players crowding into the sector,Market competition will become more open, and fierce battles among enterprises will be unavoidable.. Therefore, for Bloomage Biotech and Imeik, it may be necessary to monitor not only each other but also more potential “peers.”

1. "Opening Up Imeik""The Trump Cards of Bloomage Biotech and Its Peers: Where Is the Next Trend in Medical Aesthetics?" — Jinduan;

2. “The Hyaluronic Acid Bonus Period Is Over; Bloomage Biotech Urgently Needs a New Narrative” — Caijing Shiyiren;

3. “Imeik Breaks Through, Bloomage Biotech Falls Behind” – Laohu Finance;

4. “Business Hits the Brakes: Is Bloomage Biotech’s Story Harder to Tell?” — Beiduo Finance