Another Giant Files for Bankruptcy Protection: Over 10 Medical Unicorns Have Collapsed This Year

SmileDirectClub

Orthodontic Service Provider

Surgalign

Spine Solutions Provider

Athenex

Disease Treatment Drug Developer

Rotech Healthcare

Home Medical Device Provider

Kleiner Perkins

Venture Capital Firms

Pear Therapeutics

Developer of Digital Healthcare Solutions

Amyris Biotechnologies

Producer of Renewable Products

Spark Capital

Venture Capital Firms

Bad news keeps coming.

Recently, across the ocean, global dental care giant SmileDirectClub announced that it has initiated the process of asset restructuring and filed for bankruptcy protection, sparking widespread attention within the industry.

Notably, the plight of SmileDirectClub is not an isolated case this year; the collapse of medical unicorns and large corporations has become increasingly frequent. A review by VCBeat reveals thatFrom January to October, no fewer than 10 global healthcare unicorns and major companies have collapsed, either filing for bankruptcy protection or awaiting sale.

(Data source: VBData, public reports; graphic by VCBeat)

This group includes star enterprises across various niche sectors, such as clear aligner leader SmileDirectClub, synthetic biology giant Amyris, digital therapeutics pioneer Pear Therapeutics, prominent digital health company Babylon, top-100 global orthopedic device manufacturer Surgalign, and innovative oncology drug developer Athenex, all of which have achieved remarkable success in their respective fields.

If even the leading companies in niche segments are facing such significant challenges, it goes without saying that mid-tier and smaller enterprises are in an even more precarious position. For instance, in terms of primary market financing, the "Global Healthcare Industry Capital Report for H1 2023" released by VCBeat shows that the total amount of global healthcare industry financing continued to decline in the first half of this year, dropping from $61.26 billion in 2021 to the current $30.2 billion, effectively halving.The cooling of the financing environment has led to numerous projects in the market seeking discounted financing.

(Image source: VCBeat Research Institute’s “Global Healthcare Industry Capital Report for H1 2023”)

Undoubtedly, the biting chill has spread across nearly the entire healthcare innovation industry.

Caught off guard.

The news of SmileDirectClub filing for bankruptcy protection instantly sent shockwaves through the U.S. venture capital community. As a unicorn in the global clear aligner market, SmileDirectClub enjoys immense prominence in the dental industry: by bypassing dentists and enabling consumers to purchase clear aligner products directly via e-commerce or live-streaming platforms, it has sparked a major transformation worldwide with its Direct-to-Consumer (DTC) model.

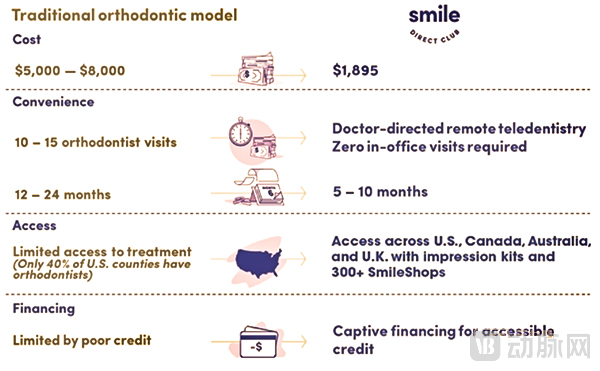

Specifically, in the traditional clear aligner orthodontic process, patients must visit a hospital or clinic to have a professional dentist take dental impressions. SmileDirectClub has disrupted this workflow by offering two impression methods: one involves purchasing an “Impression Kit” online and taking bite impressions at home, then mailing the dental molds back to the company; the other involves visiting its offline locations (SmileShop or SmileBus) for a 3D intraoral scan to obtain the necessary modeling data.

After completing the above steps, patients can place orders directly online, and custom-made clear aligners will be mailed to them within three to four weeks. During this period, patients can transmit their orthodontic progress to the company via selfies; authorized dentists will then conduct remote diagnoses through the Smile Check virtual platform and make necessary adjustments to the treatment plan. The average duration of the entire correction cycle is six months, compared to 12–24 months for traditional treatment.

This model has led to a reduction in orthodontic costs. According to data from SmileDirectClub’s prospectus, traditional orthodontic treatment costs between $5,000 and $8,000, whereas SmileDirectClub charges only $1,895 by eliminating intermediaries.

(Advantages of the SmileDirectClub Business Model; Source: SmileDirectClub Prospectus)

Benefiting from business model innovation, SmileDirectClub rapidly achieved commercialization, with revenue reaching $470 million in fiscal year 2022.

On one hand, it boasts strong revenue-generating capabilities; on the other, it is filing for bankruptcy protection. What exactly went wrong with SmileDirectClub?

A review of SmileDirectClub's financial reports reveals that,A substantial debt became the key factor.It turns out that in 2020, the COVID-19 pandemic led to a decline in consumer spending power, which adversely affected the purchasing power of SmileDirectClub’s core customer base, primarily consisting of low- and middle-income individuals.

Furthermore, pandemic-induced supply chain disruptions and labor shortages have impaired SmileDirectClub’s order fulfillment capabilities. Compounding this issue, SmileDirectClub has consistently reported revenue growth without corresponding profitability; it posted net losses of $340 million in 2021, $280 million in 2022, and $119 million in the first half of 2023, indicating its persistent failure to achieve profitability.

Misfortunes never come singly: SmileDirectClub lost its long-running legal dispute with Align Technology, the parent company of Invisalign and a pioneer in using 3D printing to create its clear aligner system, and was ordered to pay $63 million in damages. This ruling has impacted its cash flow and collaborations with third-party customers.

To address these challenges, SmileDirectClub raised $747.5 million through convertible notes and other financial instruments as early as 2021 to accelerate business expansion, and in 2023, it launched two key initiatives: building an AI-driven platform and offering higher-value products to high-net-worth individuals.

Despite ongoing efforts to change its circumstances, SmileDirectClub has faced continuous setbacks due to mounting debt and a lack of third-party investment. When SmileDirectClub recently filed for bankruptcy protection, its accumulated debt had reached $890.6 million.

Ultimately, SmileDirectClub had hoped to leverage its ample capital to stage a turnaround. However, due to its failure to resolve persistent losses, the company was forced to file for bankruptcy protection as its debts neared maturity. A key hearing has been scheduled for October 24, 2023, at which time a specific reorganization plan will be disclosed.

Like SmileDirectClub, many medical unicorns that collapsed this year did so due to debt challenges.

For example, Rotech Healthcare Inc., a leading player in the home ventilator market; Goldfinch, a biotechnology company specializing in nephrology drugs; Surgalign, one of the top 100 global orthopedic medical device companies; and Babylon, a star enterprise in internet healthcare.

An examination of the development trajectories of these unicorns reveals a common pattern: they all pursued aggressive business expansion through large-scale debt financing before fully establishing profitability.

Taking Rotech Healthcare as an example, as a leading player in the home ventilator market, Rotech Healthcare operates across 300 locations in 45 U.S. states and has acquired more than 65 companies over the past four years. Its product portfolio covers a range of devices, including ventilators, nebulizers, and oxygen concentrators. Leveraging its comprehensive product lineup, Rotech Healthcare achieved sales of $503.2 million in 2020, equivalent to RMB 3.655 billion.

In 2020, amid a period of rapid business expansion, Rotech Healthcare began pursuing an initial public offering (IPO) and secured $425 million in loans from multiple banks with a five-year term to accelerate its growth. According to CEO Tim Pigg, this debt financing round would enable the holding company to distribute a special dividend of $100 million.

However, Rotech Healthcare’s path to going public was not as smooth as expected. In mid-2022, documents released by Rotech Healthcare showed that its IPO registration statement had been abandoned by the U.S. Securities and Exchange Commission.The failed IPO thwarted Rotech Healthcare’s financing efforts, compelling it to seek a sale to raise funds for debt repayment and other obligations.

Another example is the medical device unicorn Surgalign, which ranked 21st among the top 100 global orthopedic companies in 2019. Its core products focus on the field of spinal surgery, encompassing navigation systems, orthopedic implants, bone regeneration materials, and more.

To sustain the expansion of its business scale, Surgalign made a significant push into the field of medical AI imaging after 2020, acquiring multiple AI companies while leveraging debt. In January 2022, it launched the world’s first AI-driven augmented reality (AR) navigation system for spine surgery—the HOLO Portal Navigation System—which received FDA approval.

However, Surgalign’s AI imaging products received critical acclaim but failed to achieve commercial success. Since venturing into this new field, Surgalign failed to generate positive cash flow from commercial operations in fiscal years 2020 and 2021. Coupled with acquisition costs and substantial R&D expenditures, this led to a heavy debt burden, ultimately forcing the company to file for bankruptcy protection.

In addition to heavy debt burdens toppling medical unicorns, the failure of products to gain regulatory approval has also been “the last straw” for many innovative enterprises.

For instance, as a star enterprise in the field of innovative oncology drugs, Athenex has developed for more than 20 years and already has 39 products on the market. In order to maintain its leading position in the industry, Athenex has placed high hopes on its oral formulation technology platform since around 2010, aiming to convert commonly used intravenous chemotherapy drugs into oral formulations. Among them, the oral paclitaxel + Encequidar project (Oraxol) is the company's main pipeline and has also become an important future revenue growth point.

After approximately 10 years of research and development, in September 2020, the U.S. Food and Drug Administration (FDA) accepted Athenex’s New Drug Application (NDA) for oral paclitaxel plus encequidar for the treatment of metastatic breast cancer, granting it accelerated approval designation. However,In March 2021, the FDA rejected the marketing application for this therapy., on the grounds that oral paclitaxel may increase the safety risk of neutropenia-related sequelae compared with the intravenous paclitaxel group.

In this context, Athenex decided to abandon the U.S. market and launch its oral paclitaxel formulation in the European market, only to announce failure in January 2023.The prolonged absence of new business growth drivers has left Athenex facing depleted cash flows.According to figures reported by foreign media, Athenex had only $36.7 million in cash and cash equivalents remaining at the end of 2022.

Left with no choice, Athenex had to file for bankruptcy protection and seek a buyer.

Thus, regulatory approval has become a major “stumbling block” for medical innovation companies prior to commercialization.Moreover, failures during the clinical trial phase can rapidly cause a medical innovation company to collapse before its drug candidates are submitted for regulatory approval.

This is exemplified by the Dutch biotechnology company Xenikos and Calithera Biosciences, a developer of novel therapies for renal cell carcinoma. Xenikos’s experimental therapy for its orphan drug T-Guard failed in Phase III clinical trials, while Calithera’s glutaminase inhibitor Telaglenastat (CB-839) did not meet the primary endpoint in the CANTATA clinical trial conducted in patients with advanced or metastatic renal cell carcinoma (RCC).

Clinical trial failures forced two healthcare unicorns to lay off staff in a bid to survive, ultimately leading them to file for bankruptcy protection after their capital chains broke.

From the above situation, it is evident that medical unicorns mainly failed on the eve of clinical trials and the commercialization of new businesses. However, even at the critical moment of market expansion, there are still enormous unknowns ahead.

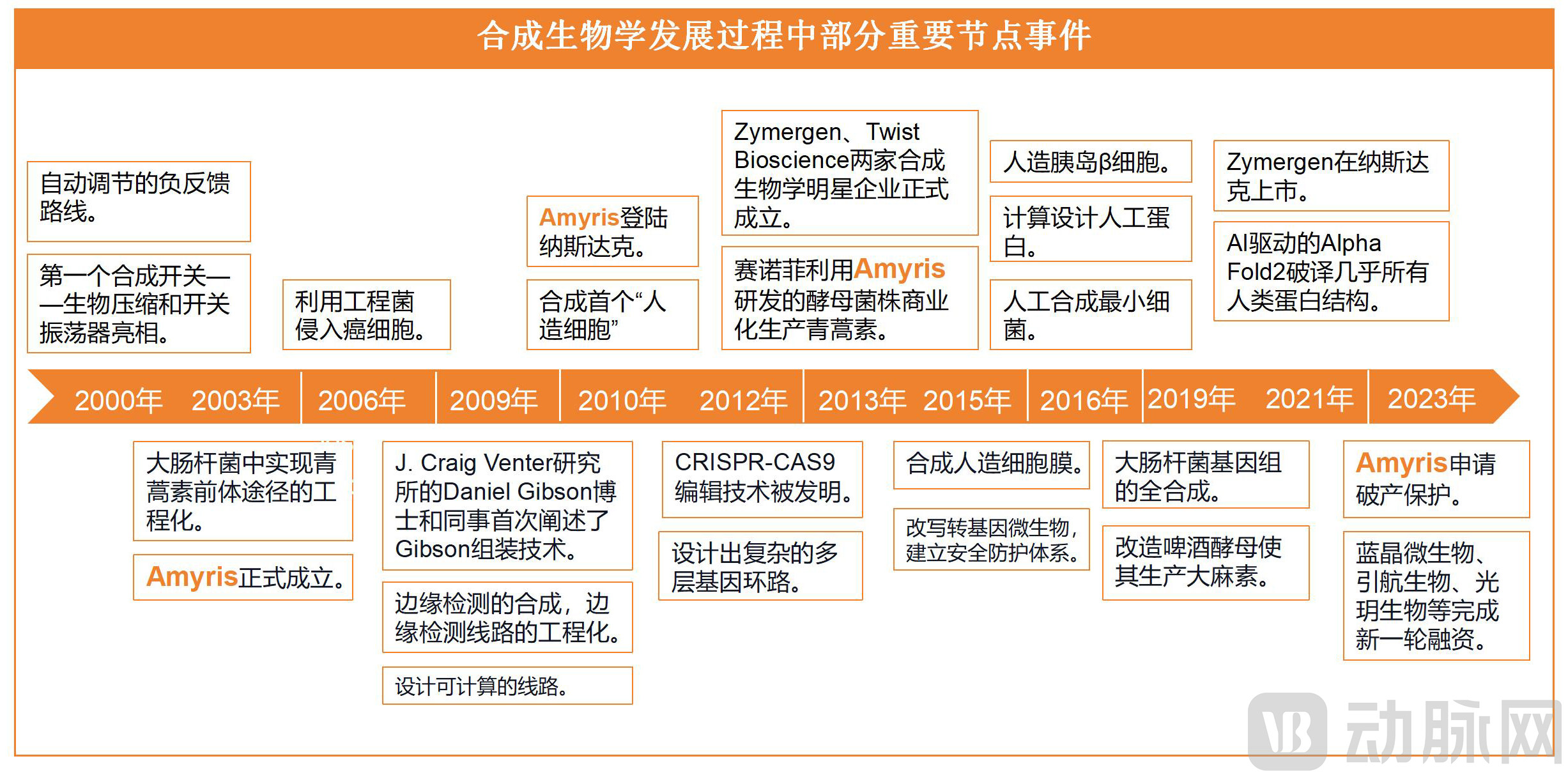

For instance, Amyris, a “pioneer-level” unicorn in synthetic biology, has garnered widespread attention amid the sector’s recent surge. As one of the earliest companies in the field, Amyris leveraged genetic engineering of yeast cells to produce artemisinin, a critical antimalarial drug, and subsequently expanded its portfolio to cover multiple brands in the health, beauty, and wellness sectors.

However, Amyris was not spared from collapse. The reason lies in its aggressive commercial expansion from the B2B sector into the consumer goods market, where it failed to control business costs, resulting in substantial losses. Financial report data shows that in the first quarter of 2023, Amyris’s revenue was $56.08 million, a year-on-year decrease of 2.8%, while its loss reached a record high of $200 million.

As profitability continued to decline, Amyris’s cash reserves were insufficient to weather the crisis, ultimately leading the company to file for bankruptcy protection.

Mirroring the situation with Amyris, Pear Therapeutics, a pioneer in digital therapeutics, has encountered bottlenecks amid its rapid commercialization efforts. Reportedly, Pear currently has three digital therapeutic products approved for market launch, targeting substance use disorder, opioid use disorder, and chronic insomnia, respectively. Additionally, it has 14 products in development, covering multiple fields including psychiatry, neurology, gastroenterology, oncology, and cardiology.

Despite having built a robust product portfolio, Pear is not profitable. Financial reports show that Pear’s operating revenue in 2022 was $12.7 million, while its net loss reached $123.4 million.

Thus, in response to market headwinds, Pear initiated significant layoffs last year to cut costs; however, as its commercial monetization failed to show marked improvement, the company ultimately filed for Chapter 11 bankruptcy protection in April this year.

It is not difficult to find that,When reviewing the reasons for these companies' failures, even those that had grown into industry unicorns, every factor—high debt levels, clinical progress, regulatory approvals, and profitability—could still become the “last straw” that breaks an innovative enterprise.

“It is often said that entrepreneurship is a high-stakes game with slim odds of survival. Compared with most other industries, healthcare entrepreneurship is more difficult, more arduous, and has an even lower probability of success. Throughout the entire journey from having a technology or idea in the laboratory to achieving commercial scale-up, every stage is critical; a single misstep can lead to a cascade of errors,” an anonymous venture capital executive told VCBeat. “And as reflected in the current landscape,”The constrained financing environment has further exacerbated the survival challenges for innovative enterprises, making widespread business failures inevitable.”

Only through the winnowing of great waves can true gold be sifted out.

Although medical unicorns have fallen one after another this year, the pioneers have traversed the rough terrain, charting a course for those who follow in the industry.

For instance, in the field of dentistry, SmileDirectClub has significantly contributed to the continuous expansion of the clear aligner market through its Direct-to-Consumer (DTC) model. It is worth noting that there is a substantial global shortage of orthodontists; in the United States alone, 40% of counties lack access to orthodontic specialists. By offering online orders for orthodontic kits and leveraging a global network spanning the United States, Canada, Australia, the United Kingdom, and other regions, SmileDirectClub has enabled a large number of patients to easily access orthodontic care.

Following SmileDirectClub’s successful IPO, it has attracted a significant influx of investment institutions and innovators. According to incomplete statistics previously compiled by VCBeat, there are approximately 20 direct-to-consumer (DTC) brands in China alone, with nearly one-fifth of them having secured financing.

(Invisible orthodontics is gradually forming three sales models. Image source: Invisible Aligner Research Report)

Of course, the direct-to-consumer (DTC) model has long been a subject of significant controversy within the industry. This is because many orthodontists believe that clear aligner therapy is, first and foremost, a medical procedure that must be administered by licensed professionals. Providing aligners to patients without proper diagnostic examinations or radiographic imaging poses medical risks. Furthermore, patient-submitted photographs may not accurately reflect clinical realities compared to real-time monitoring by professional dentists.

For example, in the field of synthetic biology,The licensing of Amyris’s artemisinin-producing yeast strain to Sanofi marked a critical step toward the industrialization of global synthetic biology., also attracting a large number of entrepreneurs to enter the field, with one synthetic biology company after another being established.

When Amyris Biotechnologies, Inc. entered the financial markets and became the first NASDAQ-listed company in the field of synthetic biology, it ignited investor enthusiasm, turning synthetic biology into a sector fiercely competed for by venture capital (VC) and private equity (PE) firms.

From this perspective, Amyris has held a pivotal position and significance in the nearly two decades of exploring the industrialization of synthetic biology. Its collapse serves as a cautionary tale for the current industry: while technology is crucial in frontier fields like synthetic biology, it is equally important to recognize that commercialization and management capabilities are key, such as product category selection and cost control. These factors are essential for synthetic biology companies to achieve steady and long-term success in market competition.

Since Amyris filed for bankruptcy protection, R&D at synthetic biology companies has continued to accelerate, with investment and financing activities remaining active.

(Key Milestones in the Development of Synthetic Biology; Graphic by VCBeat; Data Source: Publicly Available Internet Information)

Looking at another industry pioneer, Pear Therapeutics, a unicorn in the digital therapeutics sector, has made it its mission to redefine healthcare since its founding in 2013, becoming a trailblazer in the digital therapeutics industry.

In 2017, when the FDA began to encourage digital health innovation,Pear was selected for the Software Pre-Certification Pilot Program, a new initiative aimed at developing regulatory approaches for medical software, and in September, it secured De Novo approval for ReSET, the first prescription digital therapeutic. The digital therapeutics industry rapidly heated up as a result.

This is because, compared with pharmacotherapy, digital therapeutics based on cognitive behavioral therapy and contingency management can avoid the side effects caused by drug treatments, ensure standardization and consistency in treatment, enhance accessibility through internet-based delivery, and prevent treatment discontinuation due to stigma associated with face-to-face therapy. As a result, the industry has high expectations for digital therapeutics, attracting numerous innovators to join this entrepreneurial surge.

(Digital therapeutics reconstruct core medical processes and access interfaces, achieving comprehensive penetration in stages. Image source: VCBeat)

However, as an emerging field, digital therapeutics is still in the early stages of business model development. Pear Therapeutics consequently encountered significant commercialization setbacks due to its overreliance on in-hospital prescriptions. Ultimately, unable to achieve profitable scale, Pear Therapeutics collapsed.

Of course, it is important to recognize that Pear’s failure was driven not only by its own inability to identify a more suitable business model, but also by objective factors such as the current downturn in the capital markets and the early-stage nature of the digital therapeutics industry.

Although Pear Therapeutics failed, its attempts and explorations have undoubtedly provided valuable lessons for the digital therapeutics industry, enabling market participants to address commercialization and management issues more prudently and scientifically.

In summary,The Fall of a Unicorn Is Not the End, But a New Starting Point for the Healthcare Industry: Every Industry Undergoes Value Chain Reshaping and Consolidation; The “Blood-and-Tears Lessons” of Pioneers Will Ultimately Open Faster Pathways for Those Who Follow.

It is through each cycle of disruption and advancement that the industry truly achieves a spiral upward trajectory.

True innovation is a near-death experience.

Taking drug development as an example, up to ten projects may enter clinical trials, but only one successfully reaches the market. Therefore, the costs of the nine failed projects are ultimately amortized into the single successfully marketed drug.

This is not only the case for biopharmaceutical companies, but also for niche sectors such as medical devices and life science tools:The pressure of massive capital investment in R&D has become an unbearable burden for healthcare startups.

Every step forward for an innovative company is like traversing the "Valley of Death," where a single misstep could cause the company to collapse midway.

So, what should innovative enterprises do? In response to this question, a seasoned investor offered four recommendations in a previous interview with VCBeat.

First, the more difficult the times, the more companies must concentrate their firepower on critical issues.Cash flow is critically important when financing conditions are unfavorable and companies are in a crucial R&D phase. Therefore, healthcare innovation enterprises need to cut businesses with low probabilities of success and focus more on areas that can create value and generate revenue. After all, project failures are often not due to inherent flaws in the projects themselves, but rather due to environmental constraints, such as the pandemic or a capital winter.

Second, it is crucial to plan ahead during the development process.When a company is performing well or maintaining healthy cash flow, it should proactively engage with investment institutions and even pursue fundraising, while gaining a thorough understanding of equity financing, debt financing, and other innovative financing models. This approach not only helps maintain connections with capital providers but also provides insight into their perspectives on the project, enabling the company to quickly identify the optimal solution when facing cash flow difficulties.

Third, enterprises must identify the most suitable talent at each critical stage of their development.Medical innovation is a long-cycle journey. From basic research to foundational technology development, and then to market introduction, the talent requirements differ at each stage. Therefore, company founders must carefully plan their organizational talent structure; upon achieving each milestone, they should begin preparing talent reserves for the next phase.

(Schematic of the Medical Innovation Chain, Chart by VCBeat)

Fourth, company founders should engage in frequent communication with customers and maintain strong relationships with investors and shareholders.If founders focus solely on technology or business operations, it is detrimental to the company’s development. Therefore, founders must engage in comprehensive strategic planning and adeptly manage relationships with various stakeholders to stabilize internal and external relations, thereby securing greater support when the company encounters difficulties.

Of course, the path to innovation is fraught with complex challenges and uncertainties. As one innovative medical enterprise after another steps forward to develop products that address unmet clinical needs, the healthcare innovation ecosystem is poised for greater prosperity.

In this process, although a large number of companies will fail for various reasons, their breakthroughs and trial-and-error experiences have become valuable assets and nutrients that nourish the industry's growth.