Q3 Global Biopharma Investment Report: Global Funding Down 40%, China Down 50%, with Radiopharmaceuticals and CGT Defying the Downturn

In Q3 2023, total financing amounts in both the global and Chinese markets declined significantly year-on-year, with a slowdown in investment and financing activity as the capital market remained in a “winter.” Early- and mid-stage funding rounds continued to be the primary focus for investment institutions.

Small molecules, large molecules, and the CXO sector remain the areas of greatest focus for capital markets, with domestic IPOs in China dominated by these three major sectors;

Beijing and the Yangtze River Delta region are hotspots for biopharmaceutical investment and financing across China, with government guidance funds continuing to increase their support.

Two Concept-Driven Companies Rank Among the Top 10 Global Biopharma Fundraisers in Q3 2023. China’s Gene Therapy Sector Shows Strong Performance, with Companies Distributed Across Diverse Subsectors.

I. Trends in Global Biopharmaceutical Investment and Financing from Q3 2022 to Q3 2023

1.1 In Q3 2023, total financing amounts in both the global and Chinese markets declined significantly year-on-year, with a marked slowdown in the pace of investment and financing activities.

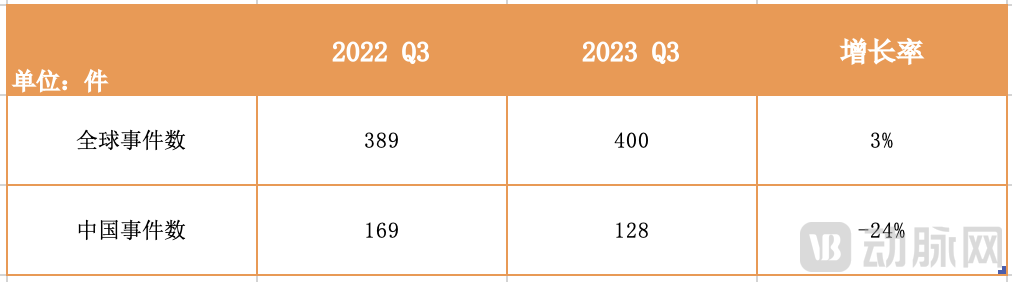

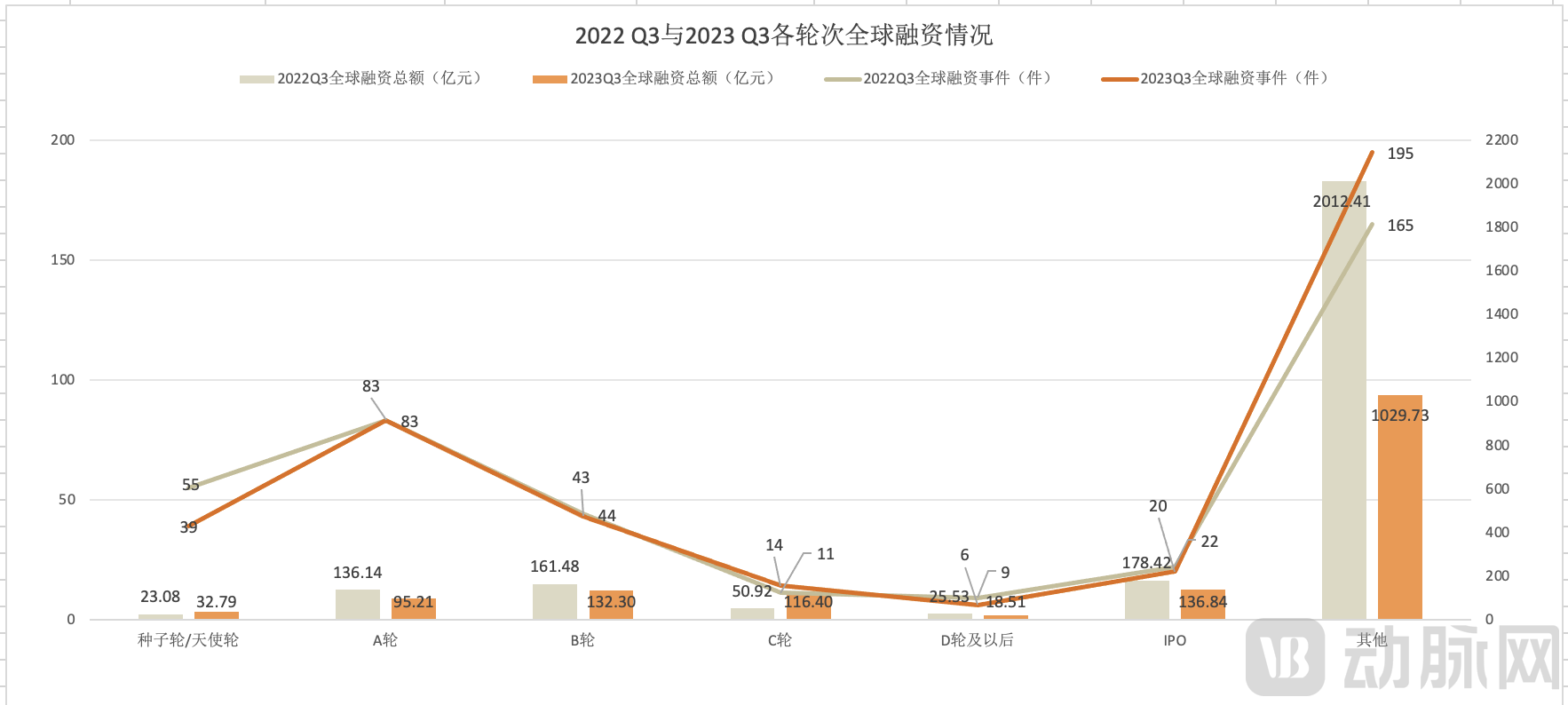

Comparison of the Number of Financing Events in Q3 2022 and Q3 2023

Data source: Artery Orange

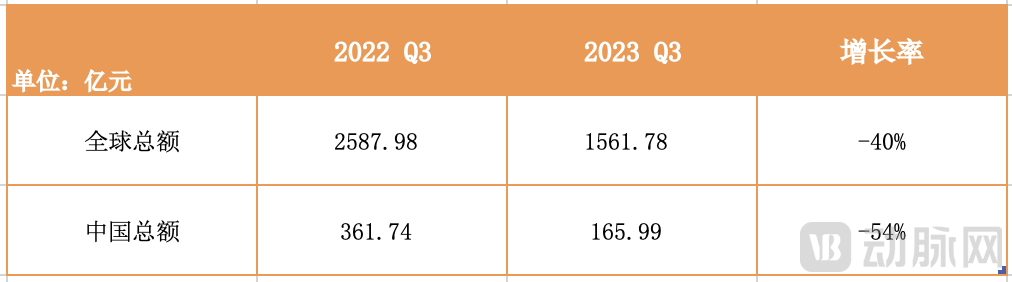

Comparison of Total Financing Amounts in Q3 2022 and Q3 2023

Data Source: Arterial Orange

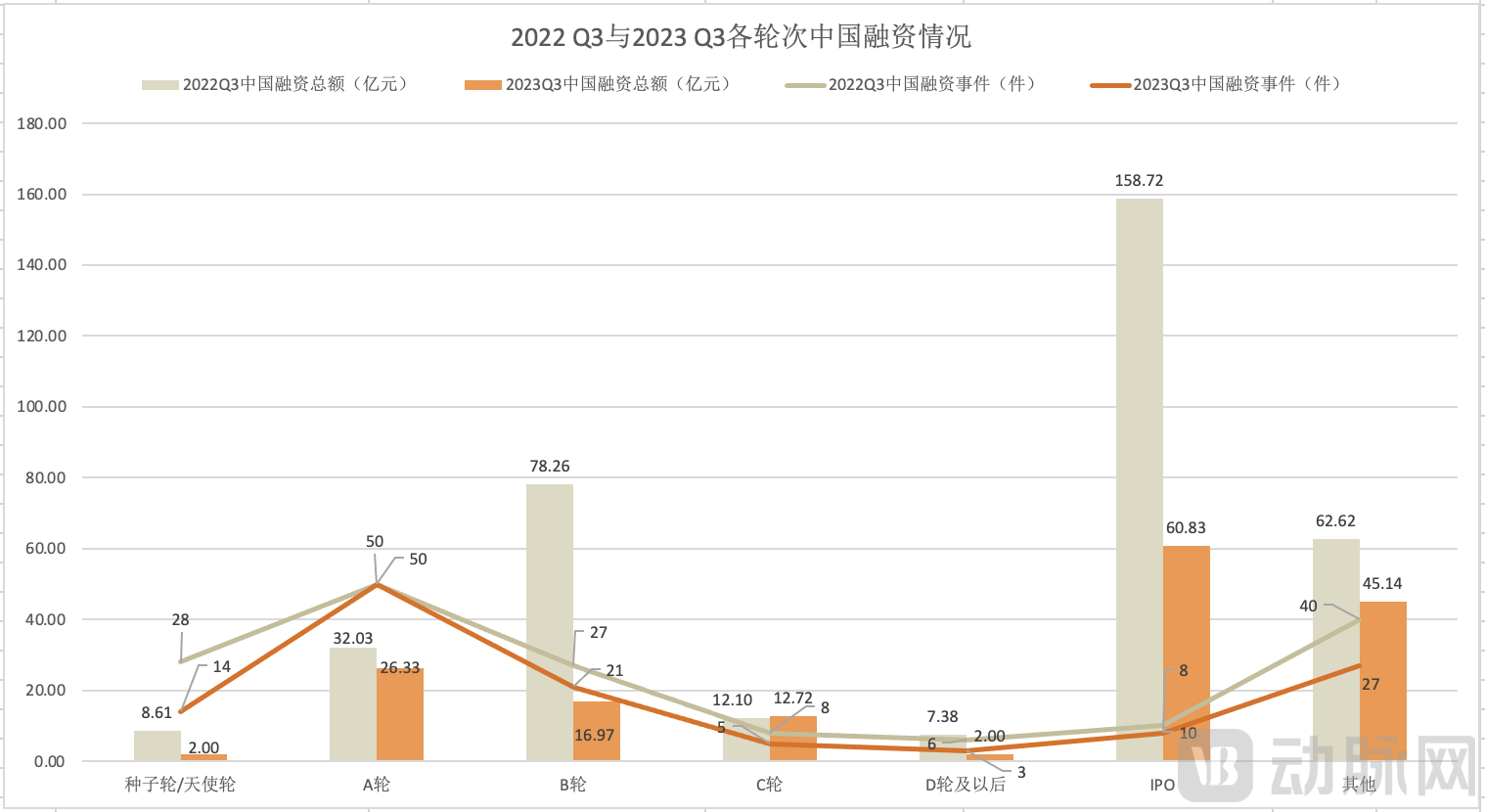

In the third quarter of 2023, there were 400 global financing events, totaling RMB 156.178 billion. Among these, China recorded 128 financing events, with a total amount of RMB 16.599 billion.

In Q3 2023, the number of global financing events increased by 3% year-on-year, with an addition of 11 deals, while the total financing amount decreased by 40% compared to the same period last year.The increase in the number of financing events indicates that the biopharmaceutical industry is actively responding to the capital winter, while the decrease in total financing amount reflects the ongoing contraction in the global biopharmaceutical sector.

In Q3 2023, the number of financing events in China decreased by 24% year-on-year, while the total financing amount was halved compared to the same period last year.The sharp decline in both data sets indicates that investment firms remain cautious in their deployments, and the capital winter continues to be the defining theme of China’s biopharmaceutical industry this year.

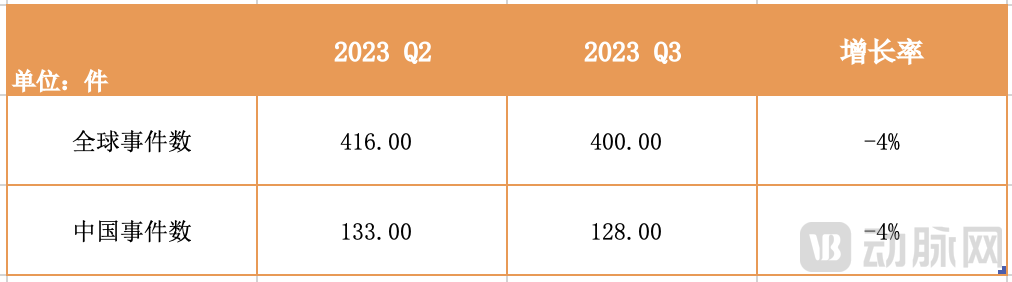

Comparison of the Number of Financing Events in Q2 2023 and Q3 2023

Data source: Artery Orange

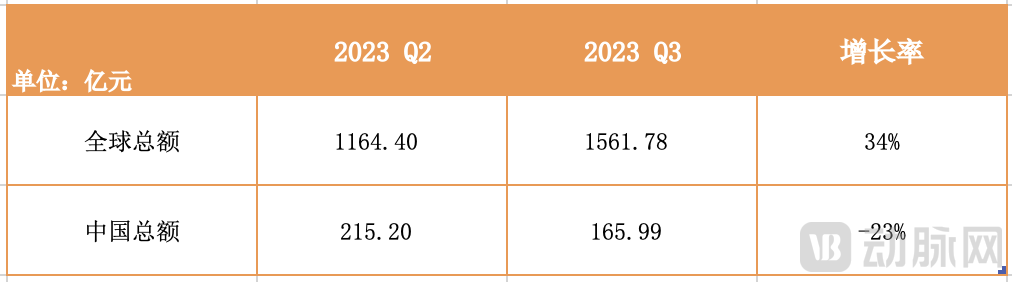

Comparison of Total Financing Amounts in Q2 2023 and Q3 2023

Data source: Artery Orange

A comparison of Q3 2023 data with Q2 2023 data reveals that the number of financing deals in both the global market and China remained largely stable between the two quarters. The global number of financing deals decreased by 16, while China’s decreased by 5.

In terms of total financing, the global total in Q3 increased by 34% compared to Q2, while China’s total financing in Q3 decreased by 23% from Q2.

Although overall financing figures appear somewhat lackluster, the emergence of waves of mergers and acquisitions (M&A) and overseas expansion cannot be overlooked. Particularly in China, against the backdrop of a phased tightening of initial public offerings (IPOs), private equity (PE) and venture capital (VC) firms are more inclined to pursue M&A as an exit strategy. Meanwhile, the trend of Chinese biotech companies going global is gaining momentum, serving as another important avenue for industry players to secure financial support.

1.2 Early- to mid-stage rounds remain the primary focus for investment institutions

Data source: Artery Orange

Data Source: Arterial Orange

A comparison of global financing in Q3 2023 with Q3 2022 reveals that investment institutions remain cautious in their deployment of capital. Except for a slight increase in the total financing amount for seed/angel rounds and Series C, financing amounts for Series A, Series B, Series D, and later stages have declined slightly, while other rounds have seen drops of up to 50%.

In China, Series A, B, and C financing rounds, as early- to mid-stage funding stages, remain the primary focus of the domestic biopharmaceutical industry due to their relatively lower investment risks.

Compared with the financing data in Q3 2022, China’s financing amounts for Series B and IPO rounds in Q3 of this year showed a clear downward trend. Particularly in the IPO stage, although the number of deals remained relatively stable, the total financing amount decreased by 62%.

II. Hot Sectors in Global Biopharmaceutical Financing and Investment in Q3 2023

2.1 Small Molecules, Large Molecules, and CXO Lead the Investment and Financing Market; China’s CXO Sector Draws Significant Attention

Data Source: Arterial Orange

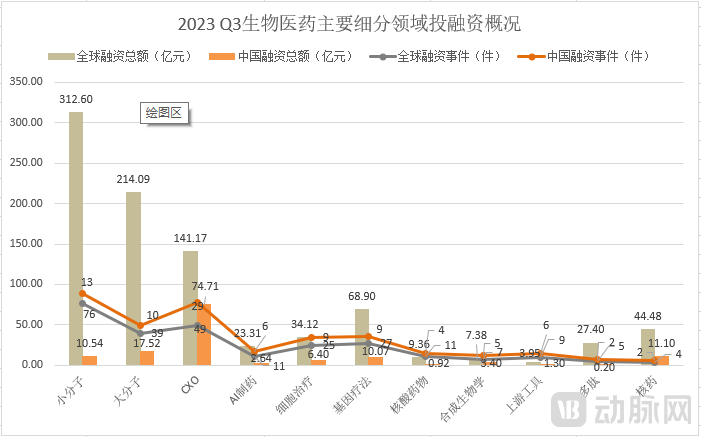

From a global perspective, small molecules, large molecules, and the CXO sector remain the areas of greatest interest to capital markets, with gene therapy and cell therapy following closely behind.

The nuclear medicine sector, which attracted significant attention in Q2 2023, continued to deliver strong performance in Q3., with substantial financing volumes both globally and in China. Among these, overseas radiopharmaceutical company RayzeBio completed its U.S. IPO in September, closing 33.33% higher on its first day of trading. Meanwhile, domestic radiopharmaceutical firm Xiantong Medicine secured a new round of financing exceeding RMB 1.1 billion in July.

In China, the CXO sector has demonstrated robust performance in financing and investment, with a total funding amount of RMB 7.471 billion, surpassing both the small-molecule and large-molecule segments and leading the Chinese biopharmaceutical industry’s financing and investment market. Among these, four CXO companies completed initial public offerings (IPOs): Haofan Biology, Jinkai Shengke, Wanbang Medicine, and Kangpeng Technology.

2.2 IPOs Concentrated in the Small Molecule, Large Molecule, and CXO Sectors

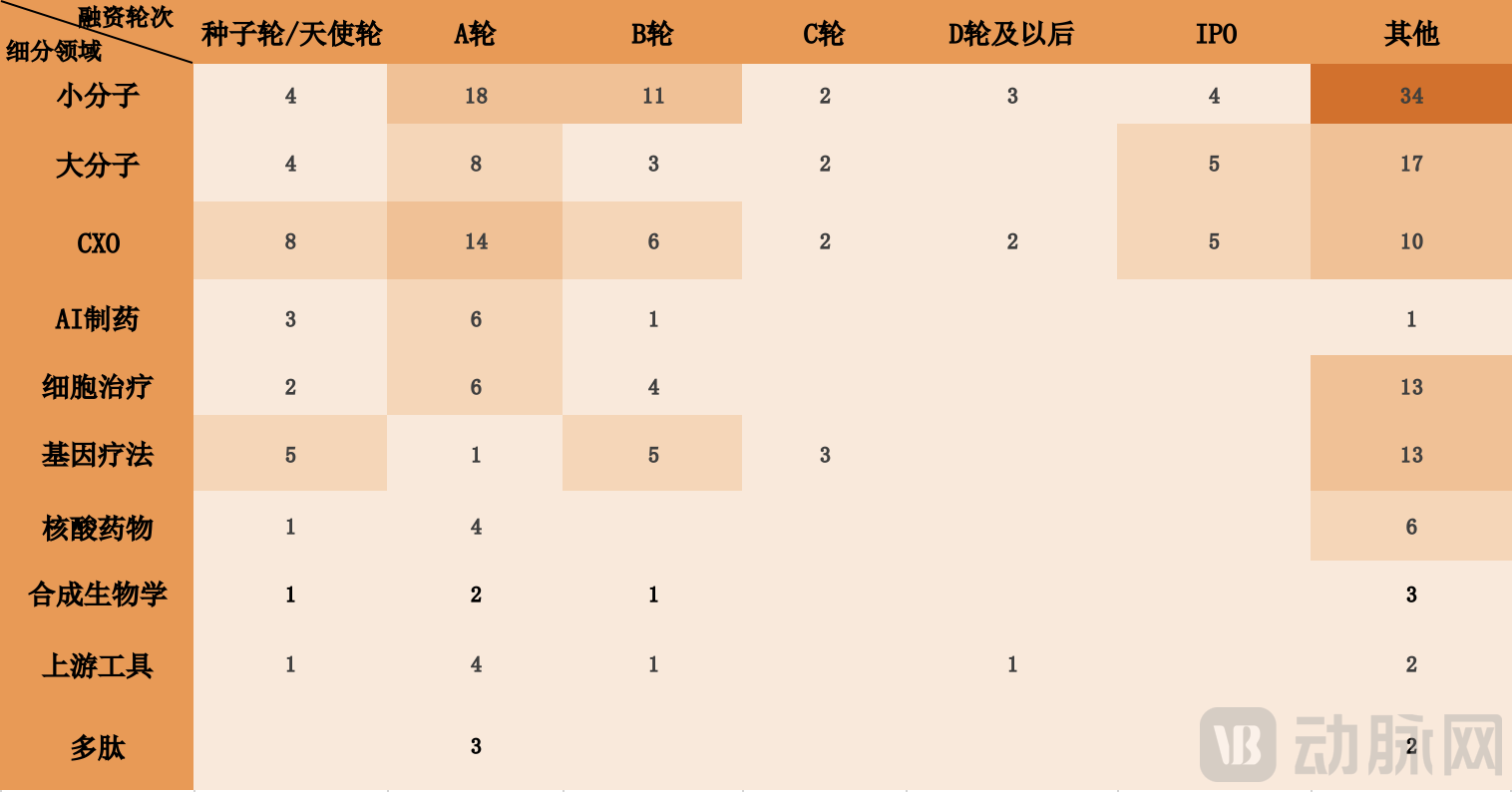

Distribution of Global Financing Rounds by Major Subsectors in Q3 2023

Data Source: Artery Orange

From the perspective of financing rounds across various sub-sectors, funding events in the small molecule and CXO tracks spanned all stages. In Q3, IPO activities were dominated by the small molecule, large molecule, and CXO sectors. Meanwhile, Seed/Angel, Series A, and Series B rounds, being early-to-mid stage investments with relatively lower risk, became the preferred financing stages for investors during the capital winter.

III. Hot Cities for Investment and Financing in China's Biopharmaceutical Industry in Q3 2023

3.1 Beijing and the Yangtze River Delta Remain Hotspots as Government Guidance Funds Intensify Support

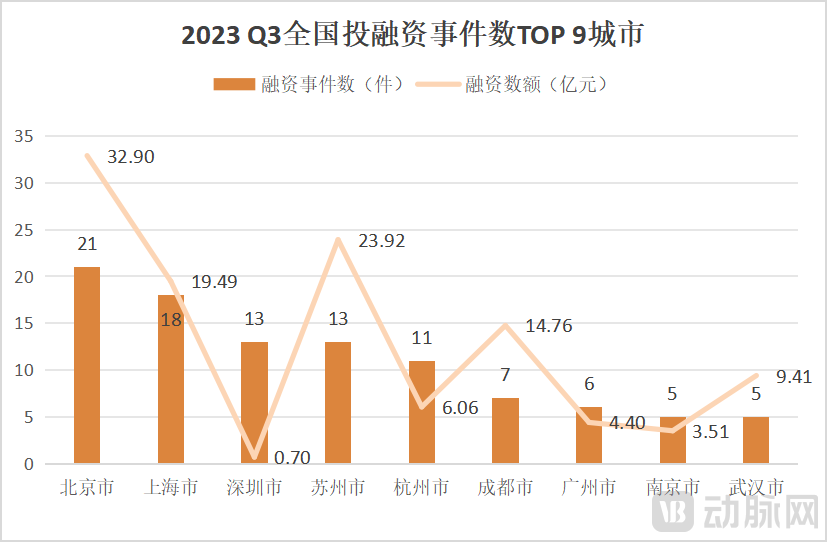

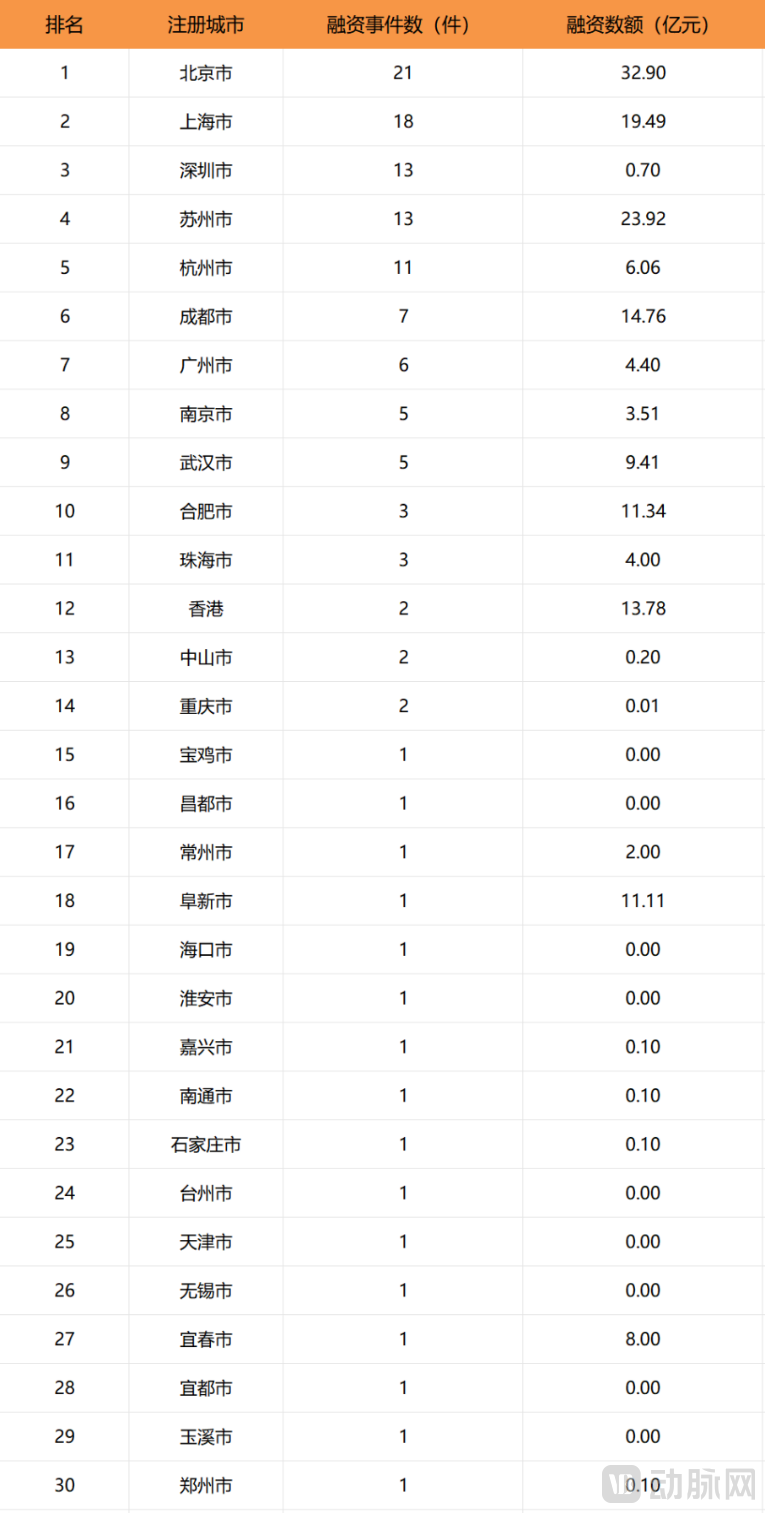

2023 Q3 Distribution of Financing Across Cities in China

Data Source: Arterial Orange

In terms of geography, financing and investment events in Q3 2023 were mainly concentrated in Beijing and the Yangtze River Delta region.Among them, Beijing recorded a total of 21 investment and financing events, with a total financing amount of RMB 3.29 billion, ranking first in both the number of events and the total financing amount.

Shanghai ranked second with 18 financing events, totaling RMB 1.949 billion, followed closely by Suzhou and Hangzhou. The financing rounds in these three cities were predominantly early-stage, with a combined total of 24 angel and Series A deals, accounting for 57% of the total. Investment was concentrated in the CXO and small-molecule sectors.

The number of investment and financing events in Chengdu and Wuhan is on par with that in Guangzhou, indicating that biopharmaceutical enterprises in central China are demonstrating increasingly strong innovation and development capabilities.

In Q3 2023, the number of government-guided funds and state-owned capital-backed funds among investment and financing institutions continued to increase.There were over 60 such funds in the first half of this year, rising to more than 70 by Q3, as local governments continue to ramp up support for investment and financing in the biopharmaceutical industry. Taking Beijing as an example, 19 government-guided funds and state-owned capital-backed funds—including Beijing Yizhuang Investment, SDIC Chuangyi, SDIC Venture Capital, and Shunxi Fund under China State-Owned Capital Risk Investment Group—have essentially covered all investment and financing activities across every sector in Beijing.

In regions such as Chongqing, Hainan, and Baoji, local governments have even emerged as the lead investors in the few financing and investment deals occurring within their respective areas.

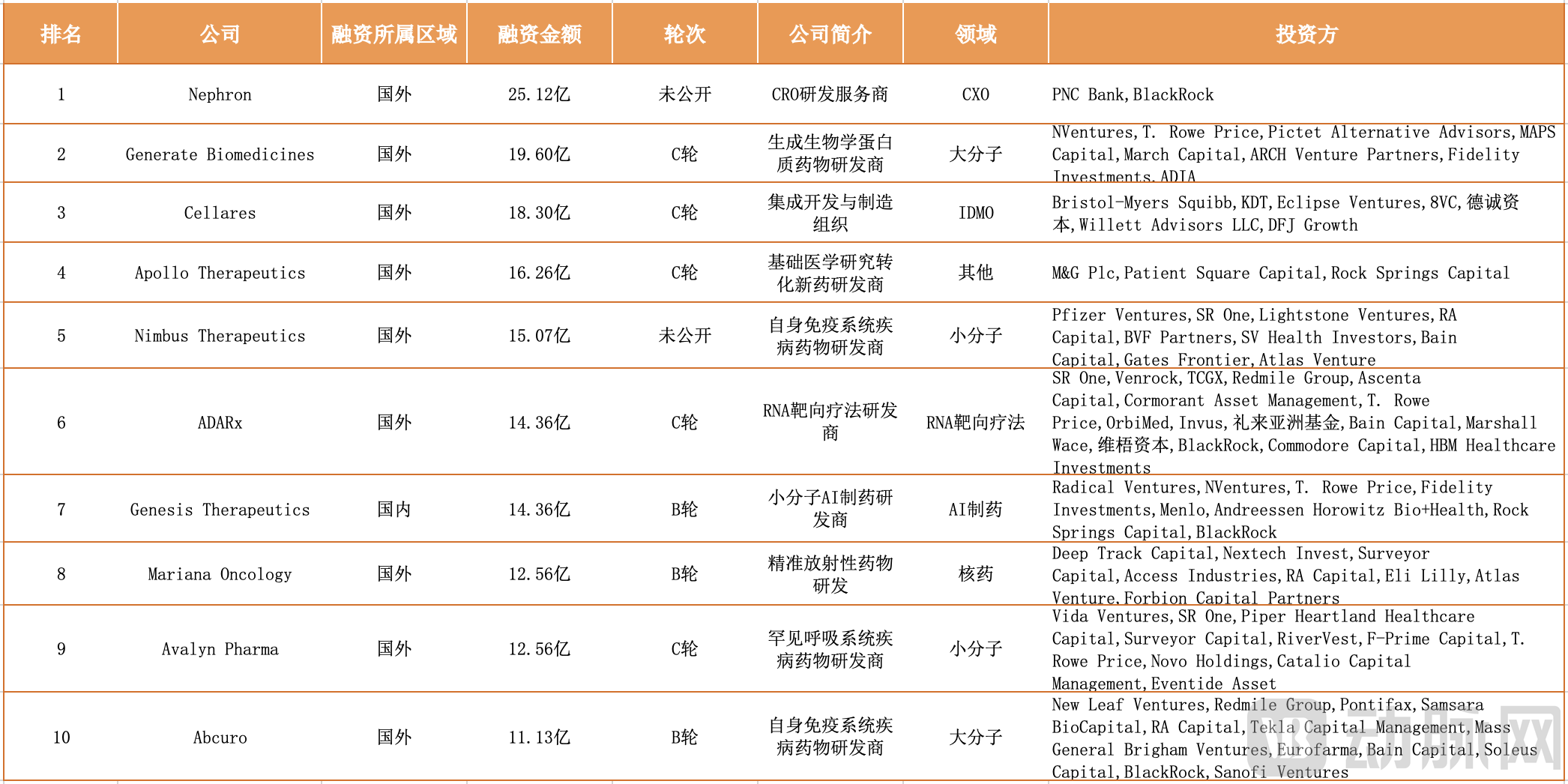

IV. Top 10 Global Biopharmaceutical Companies by Q3 2023 Financing Amount (Excluding IPOs)

4.1 Emerging Concepts Gain Favor, with Outstanding Performance in China’s Gene Therapy Sector

Overview of the Top 10 Companies by Global Biopharma Financing in Q3 2023

Data Source: Artery Orange

Among the top 10 companies by global funding, two operate in the small-molecule sector and two in the large-molecule sector, while the remaining six each belong to distinct, non-overlapping therapeutic areas.

It is worth noting that companies introducing new concepts have been well received by the capital markets.Ranked third, Cellares is the world’s first Integrated Development and Manufacturing Organization (IDMO)., they are cell therapy manufacturers but have introduced the novel concept of IDMO, offering IDMO services with advantages in hardware integration, software integration, and data integration.

Ranked fourth, Apollo Therapeutics has adopted the emerging industry business model known as the hub-and-spoke model.Distinct from traditional innovative drug companies, this model typically involves a parent company establishing multiple subsidiaries. Each subsidiary enjoys operational autonomy and shares the parent company’s resources, focusing on business areas where it holds comparative advantages. This approach aims to bridge the gap between academic research and clinical applications, thereby accelerating the translation of scientific achievements into clinical practice. Under this novel business model, Apollo Therapeutics has expanded its reach in new drug development, with therapeutic programs currently under development covering oncology, inflammatory diseases, and rare diseases.

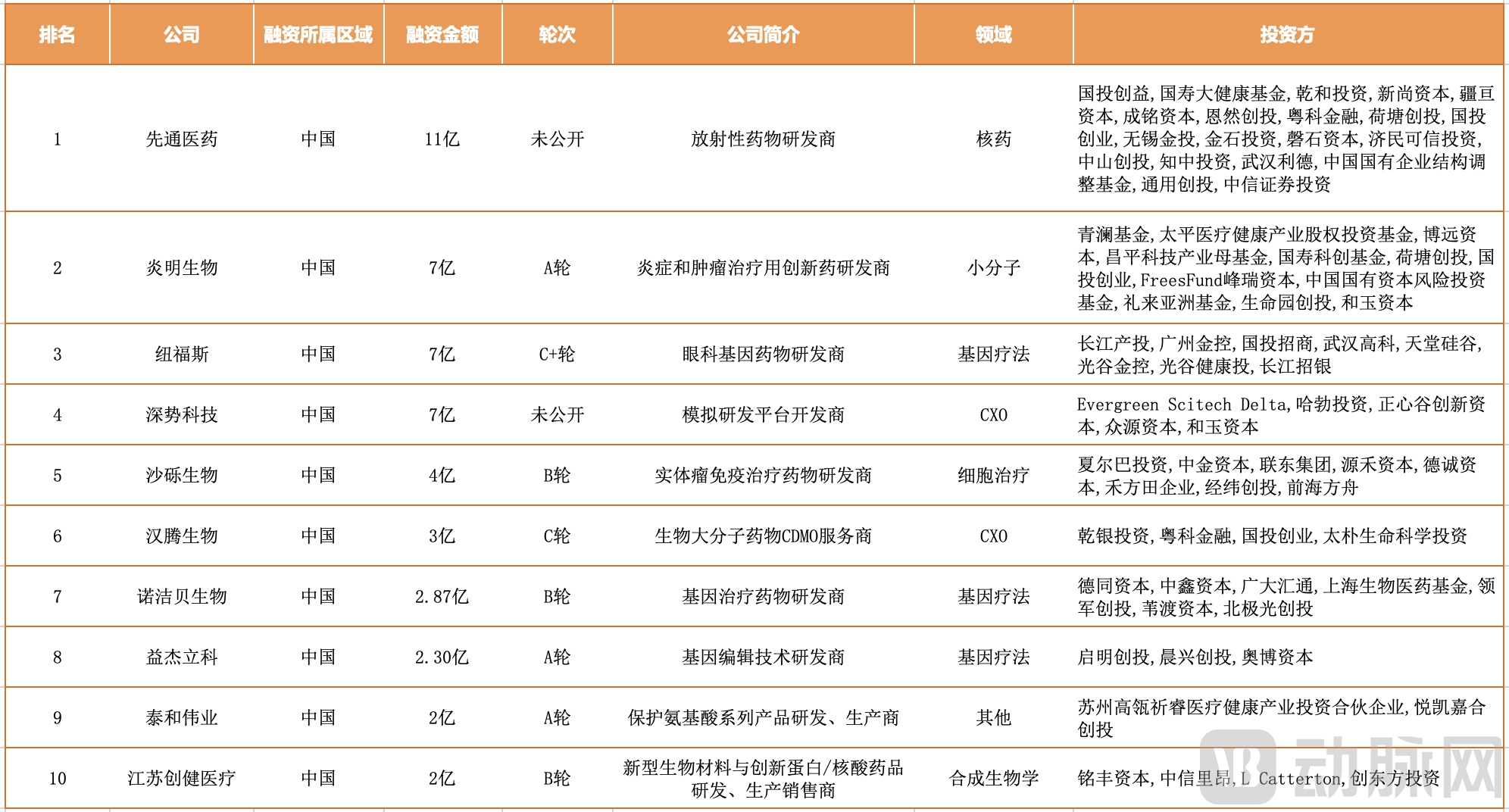

Overview of the Top 10 Companies by Biopharma Financing Amount in China in Q3 2023

Data Source: Arterial Orange

Among the top 10 companies in domestic financing and investment, three are from Beijing. Xiantong Medicine ranked first with a total financing amount of RMB 1.1 billion, while Yanming Biotechnology and DeepModel Technology tied for second place.

From a subsector perspective, gene therapy occupies three spots among the top 10 companies in China, demonstrating remarkable performance. NFOCUS, an ophthalmic gene therapy developer, ranks joint second among the top 10 companies in domestic financing and investment with RMB 700 million. Furthermore, the sectors in which Chinese companies operate show a diversified distribution pattern. Taihe Weiye and Trautec Medical are leaders in their respective subsectors and are more highly valued by the capital market.