Health Screening Emerges as the Fastest-Growing Segment in China's Resurgent Consumer Healthcare Market

health 100

Medical Examination Service Provider

As the fourth quarter begins, the traditional peak season for health checkups has arrived. Recently, health examination providers represented by Meinian Onehealth have launched initiatives to ensure medical quality and safety, preparing for the surge in business volume.

Since 2023, the consumer healthcare sector has gradually recovered. However, an analysis of financial reports from multiple listed companies (referring primarily to service providers, excluding upstream pharmaceutical and medical device manufacturers) reveals significant disparities in recovery across different sub-sectors and individual companies. Notably, health examination services have delivered strong performance even during off-peak seasons, demonstrating a trend of simultaneous growth in both volume and price.

Why Health Checkups? Is This Growth Accidental or Inevitable? What Are the Keys to Sustained Growth? VCBeat analyzes this niche sector, which has been quiet for several years, by integrating data from multiple sources.

According to data from the National Bureau of Statistics, in the first half of 2023, per capita expenditure on healthcare in China amounted to 1,219 yuan, a year-on-year increase of 17.1%, accounting for 9.6% of total per capita consumer spending during the same period. Compared with data from the past five years, the share of healthcare expenditure in total consumer spending has reached a record high.

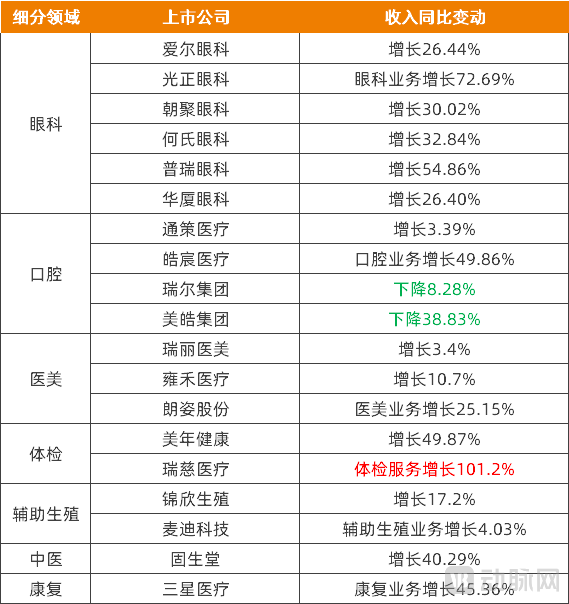

Specifically in the consumer healthcare sector, taking the performance data of 19 listed companies as an example, there was widespread growth in the first half of 2023, with clear signs of recovery; most achieved dual growth in both revenue and profit.

Core Performance Data of Major Listed Companies in the Consumer Healthcare Services Sector for the First Half of 2023; Data Source: Company Financial Reports

(Ruier Group’s data is from the annual report as of March 2023)

In the ophthalmic services sector, companies have seen significant growth in revenue and profits, with some enterprises experiencing substantial increases; cataract and optometry services have emerged as key growth drivers.

Cataract diagnosis and treatment is a relatively essential service in ophthalmology. Demand, which had been pent up in previous years, has been gradually released since 2023. Optometry services have witnessed rapid growth in patient demand in recent years, with continuous emergence of new products and technologies, and active strategic deployment by eye care institutions. They represent a key growth driver for ophthalmic services both currently and in the next phase.

In contrast, the refractive services segment, which once accounted for half of ophthalmic service revenue, is experiencing slower growth. This is primarily because refractive surgery is not an essential medical need, leading consumers to make more conservative decisions amid downward economic pressure.

In the oral care services sector, the performance changes of four companies in the first half of the year varied significantly. The combined impact of factors such as the implementation of centralized procurement policies for dental implants and weak consumer demand has led to uncertainty in revenue growth.

In the field of medical aesthetics services, despite some revenue growth, profitability remains concerning. Specifically, surgical procedures have seen slow or even negative growth; even with the full resumption of offline consultations, consumers are more cautious when opting for these high-ticket, higher-risk treatments. In contrast, non-surgical procedures, represented by "light" medical aesthetics, offer greater safety and shorter treatment times, aligning with the overall development trend of the industry. However, intense competition and high marketing costs as a proportion of expenses have weakened the profitability of institutions.

Furthermore, in the fields of assisted reproduction, traditional Chinese medicine (TCM), and rehabilitation, listed companies have achieved a certain degree of performance growth through both organic expansion and external mergers and acquisitions.

Overall, the magnitude of recovery or growth across various sub-sectors varies significantly due to factors such as the urgency of demand, public willingness to consume, and purchasing power; sectors with higher essentiality are recovering more rapidly.

In contrast, health checkups are an exception. On one hand, the mindset of “prioritizing treatment over prevention” is deeply entrenched, and it will take a long-term, gradual process for the general public to fully appreciate preventive services such as health checkups. On the other hand, enterprises and public institutions typically schedule employee health checkups in the second half of the year, making the first half a slow season for the health checkup industry.

However,Among the major sub-sectors of consumer healthcare, health examination services achieved "counter-trend" growth in the first half of the year, with a particularly notable increase.

Among them, Meinian Onehealth reported total revenue of RMB 4.405 billion in the first half of the year, a year-on-year increase of 49.87%, with net profit rising by 100.49% year on year. Ruici Medical’s total revenue for the same period reached RMB 1.284 billion, up 59.6% year on year, while its net profit surged by 232.0%; notably, revenue from its core health examination services soared by 101.2%.

Meanwhile, the health checkup service sector is witnessing a simultaneous rise in both volume and price.

According to publicly available data from Meinian Onehealth, as of June 2023, the company had 608 operational health examination centers, including 293 controlled centers. In the first half of the year, the total number of visits to these controlled centers reached 6.95 million, representing a 36% year-on-year increase. The average revenue per customer rose from RMB 514 in the first half of 2022 to RMB 594 in the first half of 2023, a year-on-year growth of 15%.

Changes in the Number of Health Checkup Visits and Average Revenue Per User at Meinian Onehealth in the First Half of 2023 (Excluding Pre-employment Examinations, Occupational Disease Screenings, and Nucleic Acid Testing)

Image source: Meinian Onehealth Semi-Annual Report

As of June 2023, Ruici Medical operated 76 health examination centers across China, 66 of which were in operation. In the first half of the year, Ruici Medical’s health examination business served 1.84 million visits, an increase of 89.2% year-on-year; the average revenue per user (ARPU) was RMB 532.6, up 6.4% from the same period last year.

The most direct reason for the “counter-trend” growth in health checkups lies in the full restoration of normal service operations by offline institutions, with some clients postponing their 2022 checkup plans to 2023. In early 2023, the widespread popularity of “post-COVID recovery” checkup packages also contributed to performance growth in the first half of the year.

So, is the rapid growth in health checkup performance solely due to the concentrated release of pent-up demand and a surge in service volume? This requires analysis from multiple dimensions.

In recent years, internet platforms and online healthcare platforms have actively strengthened their collaborations with health examination institutions.

On the Meituan platform, users’ healthcare consumption demands are shifting from traditional “treatment” to “prevention.” Over the past two years, health-related spending in areas such as dentistry, ophthalmology, medical check-ups, and Traditional Chinese Medicine has seen diversified growth.

During the 2023 “618” shopping festival, JD.com integrated leading health checkup providers such as Meinian Onehealth and Rich Healthcare into its health examination category, offering customized checkup packages valid at 500 outlets nationwide and providing interpretation services for medical reports. The gross merchandise value (GMV) of orders increased by 3.5 times year-on-year.

In the first half of 2023, Ping An Health’s B-side business saw rapid growth in its “Physical Examination+” services through collaborations with physical institutions. The cumulative number of corporate clients served reached 722, representing a year-on-year increase of 67.9%. As of the end of June 2023, the company had partnered with over 2,000 physical examination providers across China.

Internet platforms possess abundant traffic resources and precise user profiling capabilities, demonstrating significant effectiveness in driving traffic to physical institutions and empowering their digital transformation and upgrading.

Meanwhile, as public health awareness rises, the demands of health checkup consumers are becoming increasingly diversified and customized; correspondingly,The granularity of health checkup services is becoming increasingly refined, with a continuous emergence of products tailored to the general public, high-income individuals, the elderly, women and children, patients with specific chronic diseases, and working professionals. Health checkup institutions are also adopting differentiated positioning strategies based on these diverse target audiences.

Meinian Onehealth’s major brands are each positioned for different target groups: “Health 100” serves the general public across China, “Ciming” targets the mass market in first- and second-tier cities, and “Meizhao” caters to high-end clients.

Ping An Health (Testing) Center has also expanded into the high-end market. In 2023, it launched health management products tailored for high-net-worth individuals, offering customized, comprehensive, and in-depth screening services for individuals or families. Additionally, it introduced premium medical tourism services that combine high-end health checkups with travel, making health management more personalized and dynamic.

Increasingly granular market demands have even given rise to specialized services for customizing health checkup packages and interpreting medical reports. For instance, to address common issues such as the general public’s lack of self-assessment capability when selecting checkup items and difficulty in understanding checkup reports, Ke You Health offers package customization and report interpretation services. The company does not directly provide health examination services, nor does it refer users to checkup centers; it charges fees solely for customization and interpretation services.

Health checkup services are becoming increasingly refined, combining standardized and personalized products to sustainably expand mass-market coverage.

Furthermore,The rapid growth of the B2B market has become the key driver accelerating health checkup performance.

Group health examinations are the primary revenue source for most medical examination institutions. In the first half of 2023, group and individual customers accounted for 77% and 23% of Meinian Onehealth’s revenue, respectively, while corporate clients comprised 69.1% of Rich Healthcare’s medical examination business.

Currently, B-side clients are placing increasing emphasis on employee health, and medical examinations have become a standard component of employee benefits packages in many enterprises.

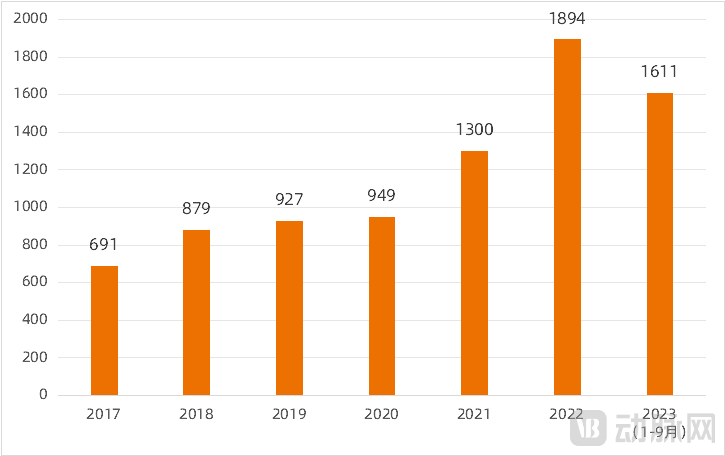

Taking government agencies and public institutions that are required to conduct open tendering for procurement as an example, data from the China Government Procurement Network shows a continuous increase in health examination service procurement projects in recent years. In 2017, there were nearly 700 winning bids for health examination services. The number of projects has grown year by year since then, with particularly rapid growth after 2020. By 2022, the number had surged to over 1,800, and from January to September 2023 alone, it already exceeded 1,600.

Number of Winning Bids for Physical Examination Services Announced on the China Government Procurement Network in Recent Years. Data Source: China Government Procurement Network

In public tendering for health examination services, contract values range from hundreds of thousands to several million yuan. Private health examination institutions have also secured a substantial number of orders from these tenders.

Finally,The National Basic Public Health Services have strengthened public awareness of the importance of regular health check-ups for the elderly, children, and other groups.With the aging of the population structure, the elderly population has an increasing demand for comprehensive prevention and control of major chronic diseases such as cardiovascular and cerebrovascular diseases, cancer, chronic respiratory diseases, and diabetes. The importance and necessity of strengthening disease prevention and early screening for the elderly are becoming increasingly prominent. Relevant departments, including the National Health Commission and the Ministry of Education, have also established requirements for health examinations of children and primary and secondary school students, and clarified the sources of funding.

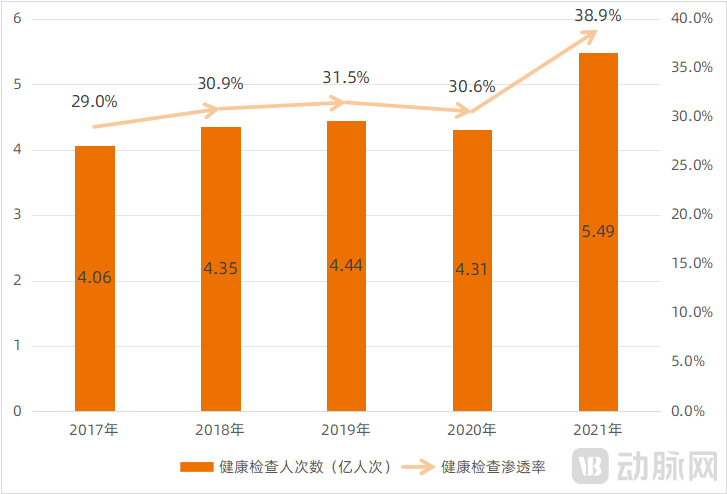

According to the China Health and Health Statistical Yearbook (2022), the national volume of health checkup services reached 549 million person-times in 2021, with a penetration rate of approximately 38.9% for the health checkup industry across China. In 2017, these figures stood at only 406 million person-times and a penetration rate of 29%, respectively.

Number of Health Checkups and Penetration Rate in China in Recent Years, Data Source: "China Health Statistics Yearbook"

Relatively speaking, the health checkup industry in developed countries started earlier and is more mature. In 2017, the penetration rate of health checkups exceeded 70% in developed countries represented by the United States and Japan, while it reached over 95% in Germany. Therefore, the domestic health checkup market in China still has considerable potential and room for development. Among them, private health checkup institutions meet market demands with diversified and multi-level services, presenting significant opportunities.

From the above dimensions, it can be seen thatThe performance growth of physical examination services in 2023 was both a contingency under special circumstances and an inevitability driven by broader trends.

In line with the seasonal patterns of the health checkup market, the industry is gradually entering its peak business period in the fourth quarter. As we navigate this busy season and look toward a future with vast market potential, how can health checkup institutions sustain their growth momentum?

First, leveraging digitalization to enhance quality and efficiency has become an imperative.

In the past, digitalization has played a significant role in service processes such as health check-up registration, queue guidance, and customer triage, improving management efficiency, shortening check-up duration, and enhancing consumer satisfaction.

Meanwhile, digitalization and intelligence are accelerating their deep integration into the core of every examination stage—such as AI-assisted medical imaging diagnosis, intelligent quality control, and smart risk early warning—thereby enhancing service quality.

Even the currently booming AIGC has application scenarios in health examination services. For instance, Meinian Onehealth is evaluating products based on the capabilities of large AIGC models to provide health consultation throughout the entire process—pre-examination, during examination, and post-examination—for its clients. These products possess general medical knowledge and proactive multi-turn dialogue capabilities, delivering accurate and personalized health guidance to customers.

Secondly, there must be a shift from “emphasizing examinations” to “emphasizing interventions.”

If the concept of “prioritizing treatment over prevention” is gradually changing, then within preventive programs represented by health check-ups, a phenomenon of “prioritizing examination over intervention” has emerged. In many cases, health check-ups are conducted merely for the sake of being checked.

Health examination institutions typically provide standardized alerts for abnormal findings in their reports. While some offer report interpretation or Q&A services for corporate employees and individual consumers, the overall level of personalization remains insufficient, limiting the scope of issues addressed.

For consumers, those with stronger health awareness will proactively seek clarification on abnormal findings. However, in the absence of immediate risk for serious diseases, most individuals remain cautious only for a short period after receiving their reports. Over time, they tend to disregard these abnormal alerts, resulting in a lack of self-management or intervention measures related to such findings.

Currently, some hospital physical examination centers are being renamed as health management centers, reflecting a shift in philosophy from “emphasizing examinations” to “emphasizing interventions.” With the aid of digital technologies, it has become possible to issue more personalized health checkup reports, provide comprehensive interpretations by integrating consumers’ historical health data, and ultimately deliver targeted health management and chronic disease management.

Finally, health examination services can accelerate close collaboration with other sub-sectors of the broader health and wellness industry.

The integration of health checkups and insurance offers inherent advantages. Big data from health screenings can support the development of innovative health insurance products, driving innovation and expanding consumer reach for offerings such as insurance for individuals with pre-existing conditions, single-disease insurance, and post-checkup disease insurance.

Health examination institutions also serve as vehicles for delivering cutting-edge testing technologies and products. By collaborating with companies that innovate in diagnostic products, they can enhance consumer access to new technologies and further facilitate their refinement.

Furthermore,The healthcare service system is advancing the mutual recognition of examination and test results. Among the lists of mutually recognized institutions published in various regions, some private health checkup centers and private hospitals have also been included.

In November 2022, the Health Commissions of Beijing and other regions issued the "Notice on the Mutual Recognition of Clinical Laboratory Test Results Among Medical Institutions in the Beijing-Tianjin-Hebei-Shandong Region for 2021–2022," which listed 813 medical institutions from Beijing, Tianjin, Hebei, and Shandong Province participating in the mutual recognition program. These included private institutions such as Meinian Onehealth, Ikang Guobin, and KingMed Diagnostics.

This means that some diagnostic and laboratory tests at large tertiary hospitals will be outsourced, especially those with inconvenient appointments and long waiting times, becoming another growth point for physical examination institutions.

Of course, all initiatives aimed at capturing market share must be built upon the foundation of medical quality management. Health examinations are clinical practices that employ medical techniques and methods to assess examinees’ physical conditions, evaluate their health status, and facilitate the early detection of disease indicators and potential health risks. Although they possess strong consumer-oriented attributes, their essence remains that of medical activities.

This holds true for health checkup services, as well as for other sub-sectors of consumer healthcare. Especially in the current context where the market is recovering but overall performance has fallen short of expectations, it is even more critical to adhere to the core principles of medical care, address the fundamental needs of the general public, and foster the healthy development of the market.

References:

Ma Xiao, Gao Xuecheng. Implementing the Management Regulations for Medical Quality Control Centers to Promote High-Quality Development of Health Checkups and Management[J]. Health Checkup and Management, 2023, 4(2): 101-102, 175.