The End of High-Growth Era: How China's Dental Industry Navigates the New Normal

Index Capital

Financial Services Institution

MEI WEI DENTAL GROUP

Oral Health Service Provider

Fortune Capital

Venture Capital Institution

ARRAI

Oral Healthcare Service Provider

“The era of rising tides lifting all boats in the oral care industry has come to an end this year.”

On October 15, 2023, on the banks of the Huangpu River, at the fourth floor of the Museum of Art Pudong in Shanghai, a small-scale sharing session for the oral health industry was underway. The host’s opening remark became one of the core topics of discussion among the attending guests.

At the event, a host of leaders from dental service institutions gathered, including Zou Qifang, founder of ARRAI; Sun Yan, Vice Chairman of Enjoy Dental Group and founder of the IDSO Dental Alliance; Ta’ergai, founder of Orangedental; Ji Xinjiang, Chairman of HAMONY LONG; Shao Zongzong, founder of Malo Clinic (China); and Song Dawei, COO/CTO of MEI WEI DENTAL GROUP. They all expressed that their current perception of changes in the dental industry is markedly different from before.

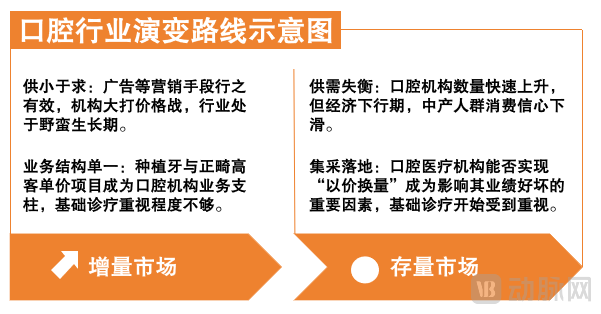

Behind this lies the dental industry’s critical leap from an incremental market to a stock market.

On the one hand, after a decade of “rapid expansion,” the number of dental institutions has risen sharply, with over 120,000 dental medical institutions now registered with industrial and commercial authorities; the compound annual growth rate from 2018 to 2022 was approximately 15%.leading to an initial imbalance between supply and demand.

It is worth noting that although there is still a certain gap between China's dental consumption penetration rate and that of Europe and the United States, the potential for growth is enormous, butCurrently, the number of consumers with both oral health awareness and purchasing power (primarily the middle class and affluent populations) is limited.These middle-class and affluent populations are predominantly concentrated in first-tier and new first-tier cities, where the core market for dental services has gradually become a red ocean over the past decade.

On the other hand, due to the current economic downturn, the middle class (the primary consumer group for dental services) has been significantly affected, leading to insufficient consumer confidence, andConsumer demand for dental services, particularly aesthetic-driven consumption, is being deferred by consumers., some oral diseases that do not affect normal life are often put off for as long as possible.

In addition, dental implants and orthodontics have always been the two pillars of business for dental institutions, while this year saw the implementation of centralized procurement for dental implants.Whether dental healthcare institutions can achieve “trading price for volume” has become a key factor influencing their financial performance.. In addition, the inclusion of orthodontic bracket consumables and all-ceramic crowns for prosthodontics in centralized procurement has further increased uncertainty within the industry. VCBeat observed this trend while recently attending the 26th China International Dental Equipment Exhibition,Centralized procurement has become a hot topic of concern across the upstream, midstream, and downstream segments of the dental industry.

(Schematic Diagram of the Evolutionary Path of the Dental Industry, Graphic by VCBeat)

“If we do not actively embrace change, the industry will follow the trajectory of real estate, where market leaders are the first to ‘perish’ when crises arise,” remarked a panelist at the aforementioned sharing session.

Undoubtedly, as the fundamental logic of the industry shifts, the era of across-the-board growth in the dental sector has come to an end, and participants urgently need to identify new breakthroughs.

The past decade-plus has been a golden age for the development of China’s dental industry.

A founder of a dental institution, who has witnessed the development of the oral health industry (particularly the private sector) over several decades, previously told VCBeat that in the early stages, the supply of dental medical services was relatively scarce. This meant that even if dental institutions published just a few popular science articles on oral health in newspapers, many consumers would seek out their services for dental care.

In an era where demand outstripped supply, dental institutions experienced rapid growth. Taking Topchoice Medical, the industry leader, as an example, its compound annual profit growth rate exceeded 20% from 2007 to 2017.

Seeing the immense potential in the dental industry, many companies have entered the market, acquiring customers through aggressive advertising campaigns and racing to capture market share. During this period, capital began to intervene, injecting substantial funds and driving mergers and acquisitions to accelerate the chain expansion of leading institutions, resulting in a growing number of private dental clinics.

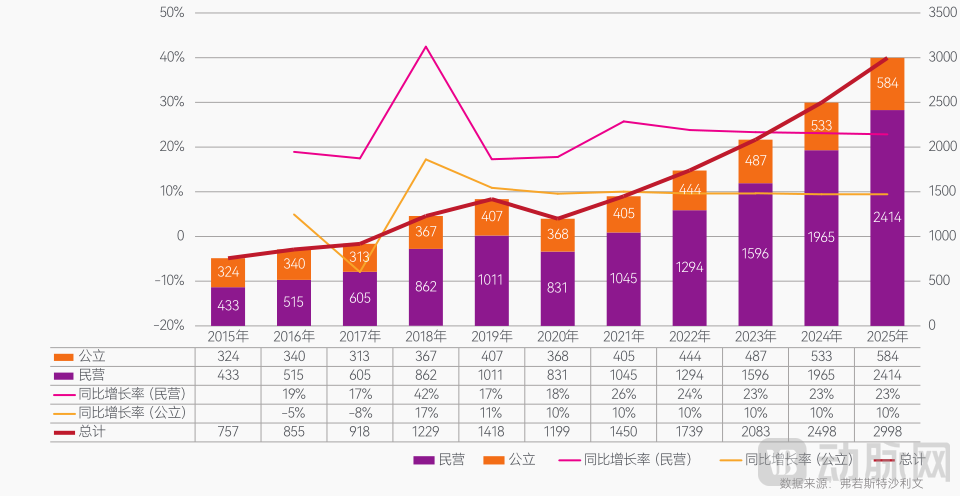

A landmark event is that, according to data from the National Health Commission, the number of private dental hospitals in China has surpassed that of public dental hospitals since 2015, with the gap between the two continuing to widen., the proportion of private dental hospitals among specialized dental hospitals has been increasing year by year, which has also driven the continuous expansion of the dental market.

(Trends in the Market Size of Public and Private Dental Care (Unit: RMB 100 million); Image Source: “2023 Insight Report on Dental Medical Services”)

(Trends in the Market Size of Public and Private Dental Care (Unit: RMB 100 million); Image Source: “2023 Insight Report on Dental Medical Services”)

The sharp increase in suppliers has intensified industry competition.At this time, marketing strategies such as “$0 Dental Implants” and “Buy One, Get One Free” have emerged in an endless stream, fueling a fierce price war. As the simplest and most direct marketing tactic with the quickest results, price wars have become the preferred choice for many dental clinic managers.

According to VCBeat, around 2015, a chain institution slashed dental implant prices by 50%, immediately attracting a large influx of patients and quadrupling its quarterly revenue. “At that time,Many business owners have formed a consensus that has since been disproven: that market share is more important than per-unit profit.“A senior practitioner in the oral health industry told VCBeat.

However, in the era of incremental growth, rapid revenue growth has led most dental institutions to consciously or unconsciously avoid this issue.

The Shift Occurred During the COVID-19 PandemicConfronted with three years of the pandemic, dental institutions faced unprecedented shocks and impacts: a large number of dental practices suspended operations during lockdowns. With revenues plummeting while expenses continued to mount, many clinics lacking sufficient cash flow were forced to close down.

Thus, as the three-year pandemic came to an end, dental institutions were full of confidence, expecting a rapid recovery in 2023. However, the reality has been that high growth rates are hard to come by. As mentioned earlier, due to supply-demand imbalance and insufficient consumer confidence among the middle class during an economic downturn, the era of stock competition has arrived.

The underlying issue is that the dental industry has failed to effectively address the widespread challenge of profitability amid its rapid expansion in recent years.The pandemic and competition in the existing market have exacerbated this issue.

How Difficult Is It for the Dental Industry to Turn a Profit? According to a report by Kan Yi Jie, approximately 30% of dental hospitals and clinics across China are struggling on the brink of survival, 40% are operating in a rather dismal state, and only about 30% are achieving favorable profitability. Even at the stage of going public, many dental institutions continue to sustain ongoing losses.

VBInsight previously surveyed 1,000 clinics and found thatThe “Three Big Mountains” Facing the Dental Industry Are Key Factors Leading to Profitability Challenges.

“The first major hurdle” is the scarcity of dental professionals, particularly high-quality dentists, which drives up labor costs. “The second major hurdle” is the low barrier to entry for establishing dental clinics, resulting in a fragmented market and intense competition. “The third major hurdle” is the difficulty in patient acquisition and the high cost of marketing.

"Faced with immense challenges, participants in the oral care industry are seeking pathways to break through."

As the dental industry enters a market characterized by stock competition, the “fight” will become more intense; facing problems squarely and finding solutions is the key.

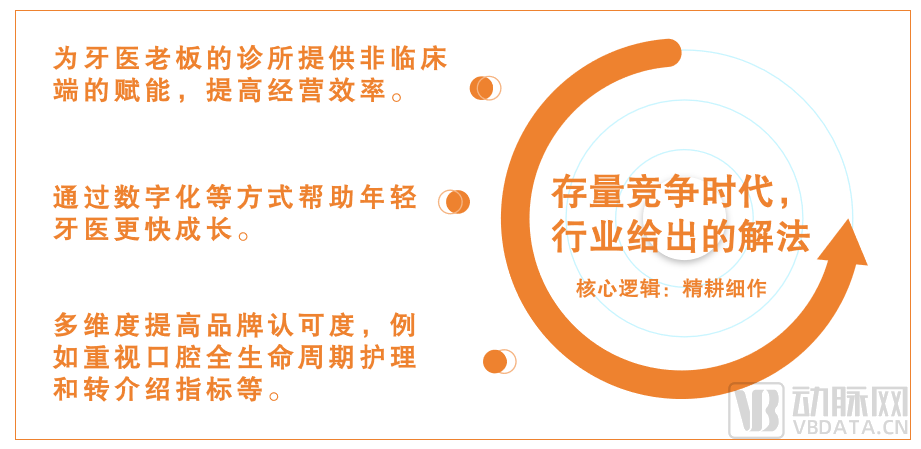

At the various roundtable forums of the 26th China International Dental Equipment Exhibition, VCBeat observed that companies across the entire value chain, from upstream to downstream, were sharing their insights and practices, offering a wide array of solutions. HoweverIn summary, the focus is primarily on tackling the "three major burdens" to achieve cost reduction and efficiency improvement for institutions.

Specifically,It is a widespread consensus in the industry to provide non-clinical operational support to dental practice owners and help young dentists accelerate their professional growth.In this direction, the DSO model and digitalization are the most frequently mentioned terms in the industry.

What Is a DSO?DSO stands for Dental Support Organization. It provides dentists and clinics with support in non-clinical areas such as management, operations, finance, legal affairs, and training, enabling doctors to devote more energy to enhancing their clinical skills and treating patients. At its core, it empowers dentists. Currently, an increasing number of companies in China are adopting the DSO model, including MEI WEI DENTAL GROUP, Beijing Enjoy Oral Outpatient Department Co., Ltd., ARRAI, and The Little Horse Shanghai Long Cci Capital Ltd.

Li Xianming (a pseudonym, at the interviewee’s request), an industry insider, told VCBeat at the exhibition that originating in the United StatesIn the localized practice of the DSO model in China, market promotion has not been ideal due to the absence of a mature health insurance market like that abroad and the fact that its enabling capabilities are still in the ramp-up phase.Therefore, the DSO model in China must accelerate innovation based on the fundamental conditions of the Chinese market.

To this end, various institutions are introducing new solutions. For instance, Malo Dental has recently launched the DPA Malo Brand Dentist Partner Alliance. This initiative builds upon the existing DSO model, which primarily focuses on empowering practices through operational management services, by strengthening support in three key areas: brand development, full supply chain procurement, and nationwide customer resources.

Additionally, Malo Dental has established a continuing education system for its publicly accessible “Medical Discipline System” to empower private dental clinics. Under this framework, the lead expert directors at Malo Dental clinics will provide one-on-one professional mentorship and on-site instructional support.

MEI WEI DENTAL GROUP has upgraded its former “Business Partner” model to the “Meiwei Star Plan,” aiming to address issues inherent in the partner-oriented model, such as a lack of sense of honor, limited management scope, and hindered career advancement.

To elaborate, the "Meiwei Star Program" adopts a dual-drive model combining "veteran and new" partners. On one hand, it incentivizes partners’ sense of ownership and involves them in more major decisions, fostering a sense of responsibility and enthusiasm to lead by example. On the other hand, it outlines a career advancement roadmap for partners, establishing a capability-oriented rapid promotion mechanism, thereby creating a more robust talent pipeline.

In this process,Digitalization has become a supportive element that co-emerges with DSOs.“DSO emphasizes empowerment, with digitization serving as a technological means to enable it. This can, to some extent, address pain points in China such as the lengthy training cycle for dentists and the imbalance between supply and demand, while also improving work efficiency and enhancing patient access and service,” said Li Xianming.

Taking dental implantology as an example, the application of digital surgical navigation systems for dental implants extends the visualization of anatomical structures that are otherwise invisible to the surgeon. This enables significant improvements in surgical precision, while simultaneously reducing surgical trauma, enhancing operational efficiency, and increasing success rates.

However, due to the high cost of digitalization investments and weak user perception, most dental institutions are unwilling to pay for digital equipment.

“There is a prevailing misconception in the industry: many institutions are willing to spend money on cost reduction initiatives but show little interest in efforts aimed at improving efficiency.“In Li Xianming’s observation, apart from leading dental institutions that are willing to invest in digitalization, it is still difficult for small and scattered clinics to carry out digital construction, which also presents greater opportunities for the DSO model.”

After providing solutions centered on dentists, the most critical factor, the next challenge to address is the fragmentation of dental clinics and the difficulty in patient acquisition.

According to several industry professionals recently contacted by VCBeat, the fragmented landscape of dental clinics will be gradually mitigated to some extent as the chain affiliation rate increases. Companies with higher operational efficiency will encroach upon those with lower efficiency, and subsequentlyThe market will enter an era where competition is driven by brand and efficiency., excessive marketing is unsustainable, and the challenge of customer acquisition can also be alleviated.

Efficiency gains can be achieved through DSO enablement and the advancement of digitalization; how, then, should brand building be approached?

“There are few high-quality domestic dental brands. This is because, during the period of rapid growth in the past, the dental industry operated on a transaction-by-transaction basis, with business focused on low-frequency, high-ticket services such as dental implants and orthodontics. After receiving treatment, patients had virtually no further contact with the institutions,” said Li Xianming.

Multiple industry insiders told VCBeat that many dentists in the past were reluctant to provide basic dental services with low per-customer transaction values. However, these services are actually the first step in building connections with patients, helping them understand their oral health conditions and encouraging repeat visits when they have future oral healthcare needs.

It is precisely based on this that,Full-Lifecycle Oral Care Has Become an Industry Consensus, ranging from comprehensive examination and diagnosis, addressing chief complaints, and developing integrated treatment plans to oral health management and post-visit satisfaction, thereby creating a closed-loop service model. This approach holds significant value: for patients, it better safeguards their oral health; for institutions, it fosters longer-term patient relationships and facilitates conversions.

(Solutions Offered by the Industry in the Era of Stock Competition, Graphic by VCBeat)

(Solutions Offered by the Industry in the Era of Stock Competition, Graphic by VCBeat)

Therefore, to build a strong brand, the industry must consider how to provide full-lifecycle oral health care for users while ensuring medical quality. In this regard, Li Xianming believes thatThe patient referral rate will become a key indicator distinguishing high from low brand recognition among dental institutions in the era of stock competition.

In summary, it is evident that as the dental industry transitions from an incremental market to a stock market, it has entered a phase of intensive and refined operations. To “overcome the three major obstacles,” the industry must, on the supply side, empower dentists—the key factor—through technologies (such as digitalization) and business models (such as DSOs); and on the demand side, provide users with superior medical services (such as full-lifecycle care) to build stronger brand recognition.

The consumer-driven nature and low penetration rate of the oral care industry inevitably point to substantial future market growth potential. Yet while the outlook is promising, the path forward will be fraught with challenges. Amid current weak consumer confidence, the industry will require an extended period of recovery, making pressure on market entrants unavoidable.

For instance, as the industry leader, Topchoice Medical facesStock Price Pressure. In the middle of this year, Topchoice Medical disclosed its 2023 semi-annual report. During the reporting period, Topchoice Medical achieved an operating revenue of RMB 1.363 billion, a year-on-year increase of 3.38%; the net profit attributable to shareholders of the parent company was RMB 304 million, a year-on-year increase of 2.99%. This represents a significant slowdown compared with the previous growth rates that often exceeded 20%.

As the earnings growth disclosed in the financial report fell short of expectations, Topchoice Medical's stock price hit the lower limit shortly after the market opened on August 25 and has remained on a downward trend. Its current market capitalization stands at approximately RMB 26 billion, far below its peak of over RMB 130 billion.

“"Without high growth in performance, the rationale for high valuations lacks support."An industry investor told VCBeat that dental institutions, whether in the secondary market or the primary market, should mentally prepare for a decline in valuations. “This will persist for a considerable period until the industry as a whole recovers.”

On the other hand, it is the industry'sPressure from Centralized Procurement. This year, the implementation of centralized procurement for dental implants has resulted in significant price reductions, characterized by large scale and intense competition. The results cover 18,000 medical institutions across China and involve 2.87 million implant systems. The average winning bid price for selected products decreased by nearly 60% compared to the median procurement price prior to the centralized procurement.

How Effective Is the Strategy of Trading Price for Volume? According to Topchoice Medical’s semi-annual report, the company performed 23,500 dental implant procedures in the first half of this year, representing a year-on-year increase of 33.8%. This indicates a significant acceleration in the growth rate of dental implants; however, the resulting revenue growth was not pronounced. The financial report shows that Topchoice Medical’s implant-related revenue in the first half amounted to RMB 229 million, a mere 2.7% year-on-year increase.

“The significant drop in dental implant prices has pushed this key revenue pillar for dental clinics into an era of thin and marginal profits. Admittedly, the surge in implant volume has also driven an increase in overall patient traffic for dental services, accelerating market education.“Li Xianming stated that it is extremely important to adjust the business structure of institutions under the centralized procurement policy and safely navigate the industry’s prolonged recovery period. The centralized procurement for orthodontics by the 16-province alliance has already been implemented. Once a nationwide centralized procurement program is launched, how should the dental services industry, with implants and orthodontics as its pillars, respond? These issues must be clearly addressed.”

In this regard, most practitioners in the oral health industry believe that,Strengthening Internal Capabilities: The Next Mandatory Course for the Industry. This includes improving the efficiency of business operations management, supply chain management, and financial management, as well as transforming mindsets and building organizational culture.

An industry practitioner provided an example to VCBeat,A healthy revenue structure for a dental institution should resemble a pyramid, with basic treatment services forming the broad base (accounting for the largest share), while implantology and orthodontics occupy the upper tiers.However, in the past, most institutions structured their consumption model into an inverted pyramid by relying on heavy marketing expenditures to acquire customers. Transforming this model will inevitably require concerted efforts in operations, supply chain management, financial management, and business philosophy.

In other words, only by solidifying their fundamentals can dental industry players achieve steady and long-term success in the era of a saturated market.

Of course, the upward trend in the dental industry remains unchanged, and opportunities continue to be abundant. At the small-scale dental industry sharing session mentioned earlier, a founder of a dental institution remarked that forests experience wildfires every few decades; these fires burn away dead wood, rotten branches, leaves, and weeds, ultimately turning them into ash.

As these ashes transform into nutrients, nourishing every individual within the forest, this ecosystem will usher in a new cycle of flourishing vitality.