Top-Tier VCs Rush to Raise Funds in County-Level Markets Amid Strategic Shift

BMF Precision Tech

3D Printing Service Provider for Single-Use Medical Application Devices

HongShan

Business Consulting, Enterprise Management Consulting Investment Institutions

SCGC

Investment Institutions in Innovative Fields

It is no longer novel for top-tier institutions to “sink” into counties and districts for fundraising.

September 7, 2023, a veteran PEWarburg PincusOfficially signed an agreement with Yixing City, Jiangsu Province, announcing the establishment of its first RMB-denominated fund in Yixing. With a total expected size of RMB 3 billion, the fund will focus on investing in leading companies in innovative drugs, innovative medical devices, and healthcare services. Two weeks later,Hillhouse CapitalAnnounced as the manager of the government-guided fund of Fuyang District, Hangzhou, with a total fund size of RMB 2 billion; healthcare remains a key focus area.

Looking further back in time, includingHongShan, SCGCSeveral leading institutions, among others, have also implemented specific initiatives to extend their reach into districts and counties. SCGC has been the most proactive in this regard, having established government-guided funds in Kunshan and Gaoyou in Jiangsu Province, as well as Huaining in Anhui Province. The total scale of these funds has exceeded RMB 10 billion, with a trend of continued expansion in the future.

Nevertheless, beneath the bustling surface, certain details warrant careful scrutiny, given that past experience suggestsTop-tier institutions and local government guidance funds still face significant challenges in achieving “mutual alignment.”, especially for district- and county-level markets, where supporting resources are relatively scarce. Furthermore, given that the pharmaceutical sector is a “hard-core market” characterized by high technical barriers and long growth cycles, it remains unclear whether local governments at these levels possess sufficient patience and perseverance at this stage.

Therefore, under the current market trend where leading institutions are collectively “sinking” to raise funds in counties and districts,Is It a Hidden, Massive Opportunity or Just a Fleeting Bubble?, all require time to validate.

Fundraising in Lower-Tier Counties and Districts: A Reluctant Necessity or a Proactive Shift?

An investor focusing on the pharmaceutical sector told VCBeat, “I now travel less frequently to Beijing, Shanghai, Guangzhou, and Shenzhen, but instead often visit industrial parks in third- and fourth-tier cities.”

In fact, this is not an isolated case but rather the norm for many investors today. In VCBeat’s previous surveys of select districts and counties, both government entities and enterprises observed a clear phenomenon: they could access numerous top-tier investment institutions locally, with most proactively reaching out. This indirectly confirms the prevailing trend of leading investment firms “descending” into district and county markets.

So, what exactly is the reason?

This issue must be examined from two perspectives. First, from the standpoint of investors—namely, district and county governments—the desire for economic growth has become extremely strong in recent years due to the impact of the pandemic. As a technology-intensive industry with substantial market potential, the pharmaceutical sector has naturally been prioritized as a key focus for investment attraction. Furthermore, in recent years, as the core pharmaceutical hubs centered on Beijing, Shanghai, Guangzhou, Shenzhen, and Suzhou have gradually reached saturation, there is a pronounced trend of the overall pharmaceutical market rapidly shifting toward inland cities.

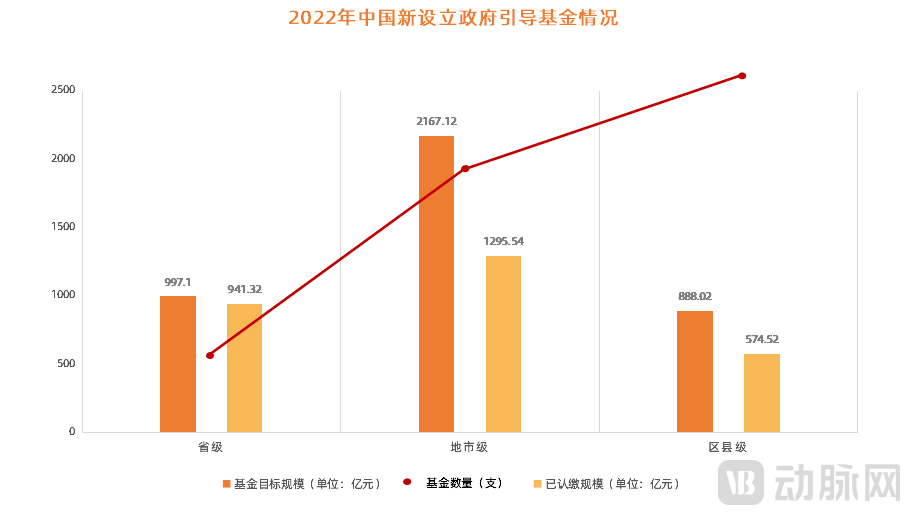

Figure 1. New Government-Guided Funds Established in China in 2022 (Data Source: Zero2IPO Research)

Figure 1. New Government-Guided Funds Established in China in 2022 (Data Source: Zero2IPO Research)

It is precisely for this reason that district- and county-level government guidance funds have emerged in large numbers over the past one to two years. According to data from Zero2IPO Research,In 2022, a total of 120 new government guidance funds were established in China. Among these, district- and county-level funds accounted for the largest share at 46.7%, and they were the only category to experience growth, with a year-on-year increase of 7.1%.。

Certainly, districts and counties possess not only financial strength but also some hidden industrial advantages. For instance, at the policy level,“Promoting the Upgrade of County-Level Medical Reform”In recent years, this has remained a key strategic indicator. At the grassroots level, it signifies that a large volume of medical device products will flood into counties and districts. In June of this year, VCBeat searched the China Government Procurement Network for bid award information from the past six months using “county-level people’s hospitals” as a keyword, identifying nearly 1,900 entries, compared to only about 1,000 during the same period last year—a near doubling in procurement volume.

In addition,Another major advantage of districts and counties is the large market demand coupled with relatively low competition.. In fact, in recent years, it is not only the pharmaceutical sector that has been extensively expanding into county-level districts; some consumer-oriented industries, including home appliances and new energy vehicles, are also gradually penetrating lower-tier markets. For instance, Starbucks, which symbolizes premium quality, business professionalism, and urban “third spaces,” has recently opened stores in Taihe County, Anhui Province. The underlying logic is straightforward,After gradually completing its layout in first- and second-tier cities, county-level markets will become the primary source of future growth., after all, China currently has over 3,000 county-level cities with a permanent population exceeding 900 million, offering immense market potential and free from the “involution” seen in first- and second-tier cities.

However, this is also a major disadvantage for district and county-level markets, as they are prone to saturation. Generally speaking,A county-level city can support at most one Starbucks.. This also means that,“Striking Gold” in County-Level Markets: Only by Entering Early Can You Reap the Dividends, therefore, according to industry insiders, many leading institutions currently track the movements of government guidance funds on a daily basis, with the aim of gaining a first-mover advantage.

However, why the “rush” to compete? The answer lies with the leading institutions themselves.

A partner at a venture capital firm stated in an interview with VCBeat, “In the past, local government guidance funds were not our first choice due to restrictions such as local reinvestment ratios. However, in recent years, as a wave of USD-denominated funds have exited and many listed companies have reduced their holdings, fundraising has become increasingly difficult. Consequently, some top-tier firms have begun to lower their stance, frequently targeting local government guidance funds during fundraising rounds, showing a gradual trend of moving down-market.”

However, during this process, some leading institutions have chosen to “sink” into districts and counties for public welfare purposes, deliberately doing so to support industrial development in underdeveloped areas. Yet, from an overall proportional perspective, this type accounts for a small share; most institutions actively embrace district- and county-level government guidance funds primarily out of consideration for their own future development.

Certainly, district and county-level government guidance funds are also highly willing to establish deep partnerships with leading institutions, given their extensive market influence and multidimensional understanding of the industry.

In an interview, a state-owned assets official from a district or county in Chongqing specifically addressed this point with VCBeat: “At the current stage, we are more inclined to collaborate with leading market-oriented institutions. On one hand, this is naturally due to their brand value, which can attract many high-quality enterprises and funds to settle in; on the other hand, it is because they possess strong industry insights, which is particularly important for us. After all, we are still relatively unfamiliar and immature in the pharmaceutical sector, so we need market-oriented institutions to provide guidance.”

Therefore, from the demand side, leading institutions are extending their reach downward and beginning to act as “catchers in the rye,”This involves both the willingness to proactively adjust and the pressure to passively adapt.。

Are there truly worthwhile investment projects in China’s district and county-level markets?

Since the end of last year, county-level cities have been producing unicorn enterprises in large numbers.

According to statistics from IT Juzi, among the 12 unicorns that emerged in the first quarter of this year, five originated from non-tier-1 cities: Zhongrun Guangneng from Xuzhou, Jiangsu; Huasheng New Energy from Xuancheng, Anhui; Yuze Semiconductor from Chuxiong, Yunnan; CHINT Solar from Jiaxing, Zhejiang; and Brighture Biopharma from Taizhou, Zhejiang. Extending this analysis further,As of April this year, there were six representative unicorn companies in China’s county-level cities., namely Kuntian New Energy, Shenghe Jingwei, Deer Technology, Weirong Technology, Rongtong High-Tech, and Zhongke Lithium Membrane.

Focusing on specific sectors, it is evident that the majority of these unicorn enterprises hidden in districts and counties come from the new energy, new materials, and semiconductor industries, while the biopharmaceutical sector is relatively underrepresented.

There are certainly reasons behind this. A founding partner of an early-stage VC firm told VCBeat, “Compared to the pharmaceutical sector’s extreme pursuit of top-tier talent and transaction efficiency, manufacturing enterprises in sectors such as new energy and new materials place greater emphasis on the costs of raw materials, land, and labor—areas where districts and counties typically hold distinct advantages. Moreover, with the rapid development of county-level economic construction in recent years, previously limiting factors such as transportation and logistics are gradually being eliminated.”Therefore, many manufacturing enterprises are currently choosing to establish factories in districts and counties to expand production capacity.。”

Following this industrial trend, the medical device sector, which shares the same growth logic as manufacturing, presents significant opportunities in county-level markets.

In fact, this view has long been validated by the market. It is reported that Jinxian in Jiangxi Province, Tonglu in Zhejiang Province, and Changyuan in Henan Province—county-level cities that collectively constitute “half the landscape” of China’s medical device industry—are currently home to nearly 4,000 medical device companies. Among them, Jinxian is known as the “Hometown of Medical Devices,” specializing primarily in disposable infusion devices; Tonglu is renowned as “China’s Largest Production Base for Rigid Endoscopes”; and Changyuan is dubbed the “Capital of China’s Medical Consumables,” with its core business focused on low-value consumables.

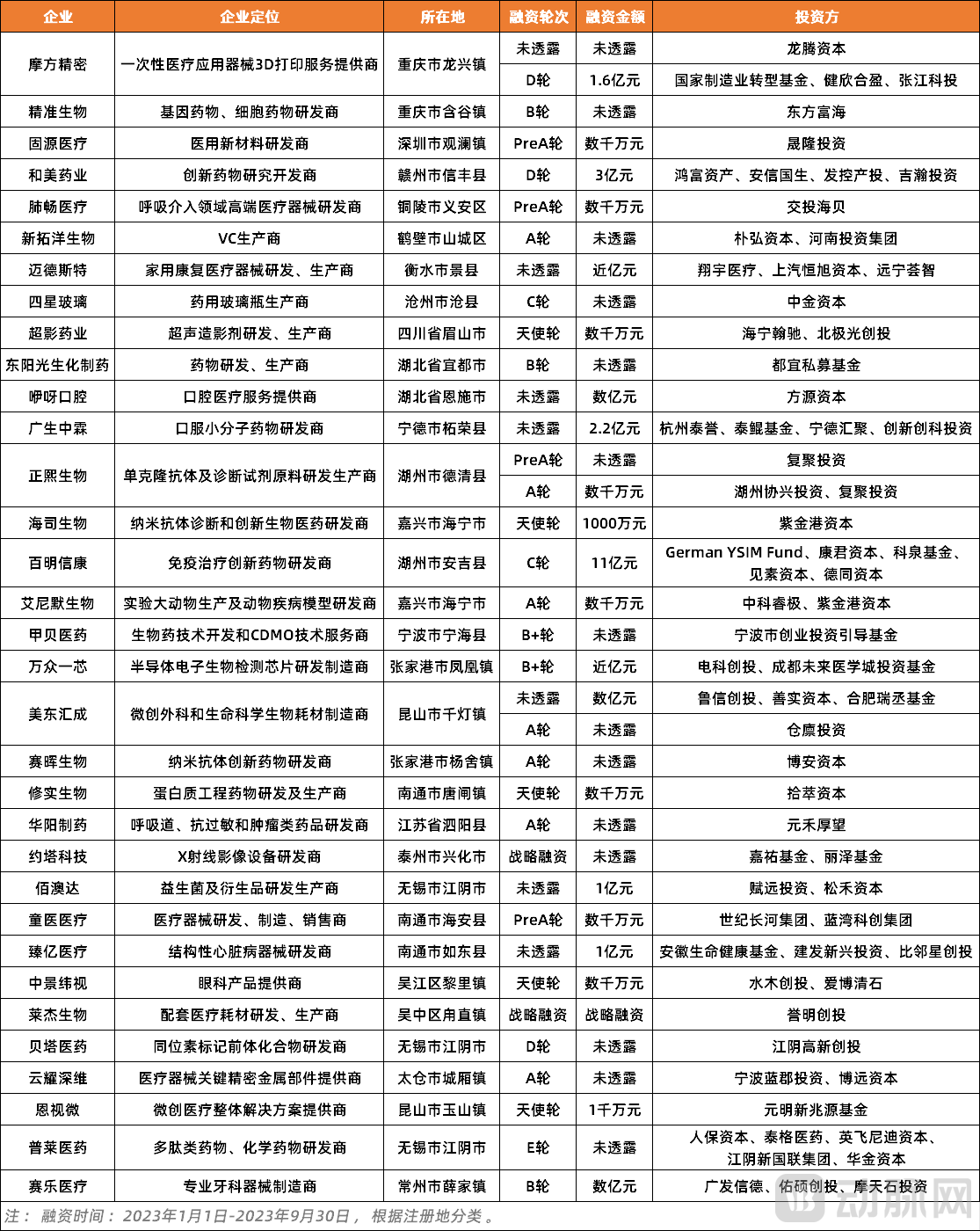

However, as supporting infrastructure in districts and counties has continued to upgrade in recent years, and numerous leading institutions have expanded their presence into these lower-tier markets, the strategic focus of the medical device industry in these areas is quietly shifting. According to incomplete statistics from the VCBeat Orange Database, as of September 30,This year, a total of 32 district- and county-level enterprises in China’s pharmaceutical sector successfully secured financing, among which 17 were medical device companies, accounting for 53.1%., and among this group of companies, most areStomatology, Ophthalmology, Minimally Invasive InterventionandRehabilitationfocusing on high-end medical device sectors.

Figure 2. Financing of County-Level Pharmaceutical Enterprises from January to September 2023 (Data Source: VCBeat)

Figure 2. Financing of County-Level Pharmaceutical Enterprises from January to September 2023 (Data Source: VCBeat)

Focused on the R&D of devices for structural heart diseaseZhenyi MedicalTaking it as an example, the company is based in Rudong County, Nantong City. Since its establishment in 2019, it has secured four rounds of financing to date, with its primary focus on transcatheter mitral valve replacement, transcatheter tricuspid valve replacement, and transcatheter aortic valve replacement products. Another representative enterprise isYota Technology, having secured over RMB 100 million in financing shortly after its establishment this year, the company is headquartered in Xinghua, a county-level city under the jurisdiction of Jiangsu Province. It is primarily dedicated to the research, development, and manufacturing of X-ray imaging equipment, and possesses independently developed core components such as detectors.

In fact, it is not only medical device companies that have attracted significant investor attention; in recent years, a number of biopharmaceutical enterprises in county-level cities, focusing on cutting-edge technologies, have also drawn widespread interest from investors. In a previous exclusive interview with VCBeat,A top-tier investor explicitly stated that they are currently evaluating synthetic biology projects in county-level cities, noting a large number of opportunities and feeling as though they have discovered a new frontier.。

However, synthetic biology is only one segment. An analysis of 15 county-level pharmaceutical companies that completed financing this year reveals their involvement in other niche sectors, including cell and gene therapies, immunotherapies, peptide drugs, and small-molecule drugs. Most of these companies have secured funding at Series B or later stages.

In response, an investor who has made multiple investments in county-level cities discussed their investment logic, “Pharmaceutical projects at the district and county level follow relatively simple logic.“, taking synthetic biology as an example, the core of such projects is usually a traditional industrial raw material manufacturer. At the time of upgrading, they choose to introduce synthetic biology technology to reduce costs and increase efficiency, ultimately passively completing the entire chain of synthetic biology technology from gene editing to application development. If we continue to dig deeper along this line of thought, we should be able to see more potential projects in the county-level pharmaceutical industry.”

In fact, compared to medical devices and pharmaceuticals,Consumer healthcare holds greater potential in county-level markets; however, expansion is largely driven by top-tier enterprises extending their reach downward, with relatively few early-stage projects originating from within counties and districts.。

Take the ophthalmology sector as an example. Recently,Aier Eye HospitalA public announcement has been issued regarding the proposed expenditure of RMB 860 million to acquire partial equity stakes in a total of 19 ophthalmic hospitals, including Hainan Aier and Zaozhuang Aier, held under six industrial investment funds. It is reported that nine of the hospitals included in this acquisition batch are located in county-level areas. Looking further back, at the end of last year, Aier Eye Hospital Group proposed acquiring partial equity stakes in 26 hospitals, such as Xi’an Aier and Quanzhou Aier, with the majority being primary healthcare institutions. This indicates that Aier Eye Hospital Group is extending its business reach into lower-tier markets across China.

In contrast, although numerous ophthalmic enterprises in districts and counties have secured financing in recent years, they are primarily engaged in the manufacturing of dental instruments, with few service-oriented companies making significant strides in the capital markets. Beyond the lack of attention from local governments, a key reason is that these entities are predominantly small clinics, which not only have limited scale but also lack comprehensive service systems, and are being gradually replaced by leading institutions expanding into lower-tier markets.

Success or Pitfall: Is the Expansion of Top-Tier Institutions into County-Level Districts a False Premise?

Among the district- and county-level pharmaceutical companies that have completed financing this year, their investor rosters indeed include numerous top-tier institutions, such asOriental Fortune Capital, CICC Capital, Northern Light Venture CapitalandProxima VenturesWait, but when viewed from the perspective of overall scale, investments in pharmaceutical projects in lower-tier counties and districts are still dominated by local state-owned assets, with top-tier institutions currently making relatively few moves.

Of course, there is an adaptation process involved, but there is also anxiety among investment institutions regarding fundraising in lower-tier counties and districts. In this regard, a head of a top-tier investment firm explicitly stated to VCBeat, “Although the investment market in county-level cities is currently booming, we are not yet considering expanding into lower-tier markets., especially in the pharmaceutical and healthcare sector, although districts and counties are currently making substantial financial commitments and possess certain advantages in terms of resources and costs,However, the industrial chain has gradually stabilized and taken shape over many years. Some preferential policies may not yield immediate results; in the long run, this will still take time.。”

These concerns are not without merit. From the perspective of the project itself, although there are many profitable businesses in lower-tier markets,However, for some local enterprises that grew up in districts and counties, market-oriented capital is often unnecessary., as these companies do not lack funding during their development, generally possessing stable capital channels. They either gained favor from local investment institutions at the early stage of entrepreneurship, with the government stepping in as an investor, or are related to the industrial chain, receiving direct support from leading local enterprises.

Moreover, enterprises attracted through investment promotion initiatives often face certain developmental limitations. For instance, some companies establish operations solely to capitalize on preferential policies, resulting in relatively low levels of actual investment. In other cases, development is hindered by a mismatch between the enterprise and the local environment. Take a medical device manufacturer as an example: during the initial planning phase for factory construction, it was discovered that the available power supply was insufficient. Subsequently, when introducing new equipment, the company found that the project exceeded its approved scope, requiring coordination across multiple levels of government to resolve. After commencing formal production, the lack of a local upstream and downstream supply chain meant that core components had to be transported from Beijing, over 500 kilometers away.

VCBeat’s analysis reveals that there are many similar corporate cases, largely because the supporting infrastructure and industrial chains in district- and county-level areas remain relatively limited and possess unique characteristics.Therefore, establishing operations in a county-level district or small town is suitable for some medical enterprises, while others may struggle to adapt.。

Of course, in addition to projects, top-tier institutions themselves also have some considerations as they move “downstream.” In interviews, one investor stated, “Although localization has become an inevitable trend, institutions accustomed to the investment strategies of USD-denominated funds and local state-owned capital still need time to align their operational rhythms at this stage.. Local state-owned assets primarily focus on investment attraction and stable returns; this need is even more direct for district and county governments, which marks a significant difference from the investment and exit strategies prevalent in the era of US dollar funds.”

Furthermore, the level of commitment and focus that top-tier institutions dedicate to county-level districts is another significant issue. For instance, achieving balance poses a challenge: in the past, it was nearly impossible for leading firms to dispatch teams to conduct in-depth research on local industries or to concentrate on the implementation and investment promotion of these industries within county-level markets. On the other hand, how to strategically select government guidance funds based on their primary and secondary objectives is also a critical consideration that top-tier institutions must address as they expand their presence into county-level districts.

Nevertheless, driven by the attraction of government guidance funds extending down to the district and county levels, it is an undisputed fact that the project sourcing scope of some top-tier institutions has gradually shifted downward. However, whether they can truly succeed remains to be seen over time. After all, we have witnessed pharmaceutical companies in certain counties become unicorns or go public, while also observing other enterprises stumble after relocating to these counties, finding themselves in a dilemma.

Therefore, a particular quote is especially fitting to conclude with:"Fishing is possible in both fish-abundant and fish-scarce waters; whether one catches fish depends on the angler."。

1. “China’s County-Level Cities Are Mass-Producing IPOs” – Investment Circle;

2. “Top-Tier USD VC Fundraising Descends to ‘Small County Towns’” — FinSMEs China;

3. “The Investment Wind Has Shifted—Six Unicorns Have Emerged from China’s Small County Towns!” — IT Juzi;

4. “Why Are Top Investors from Beijing, Shanghai, Guangzhou, and Shenzhen Suddenly Flocking to Small County Towns?” – Qianzhan Economist