China vs. Korea in CDMO: Head-to-Head Battle or Coexistence?

In 2023, when the CDMO industry was rife with news of plant closures, layoffs, and difficulties in securing orders, South Korean CDMO companies made high-profile moves. In particular, South Korean CDMOs represented by Samsung Biologics have recently seen continuous announcements of capacity expansion and major contract wins.

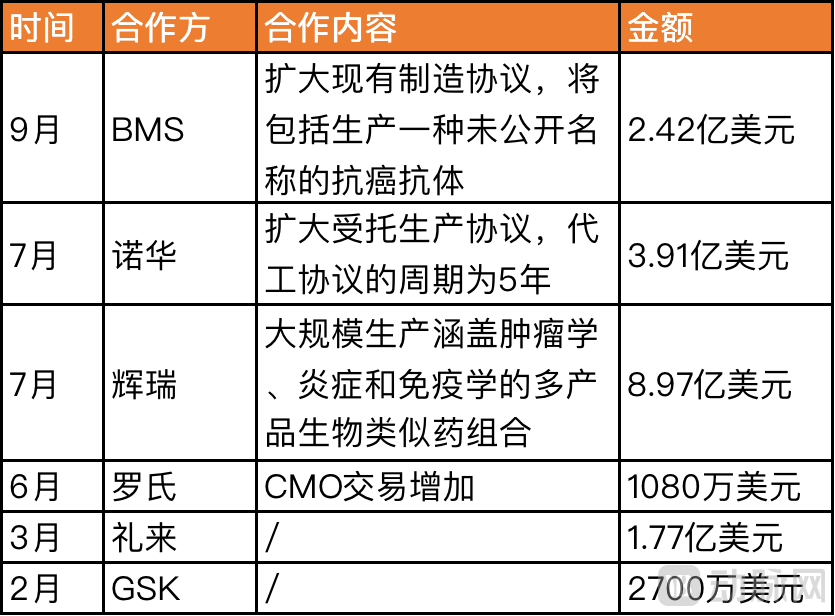

Samsung Biologics’ publicly disclosed orders this year have exceeded $1.7 billion, including a deal worth up to $242 million with Bristol Myers Squibb (BMS) last month and a major order with Pfizer that was expanded to $897 million in July. The collaborations cover the manufacturing of antibody drugs in areas such as oncology and immunology, rapidly filling the void left after the end of the pandemic.

Production Orders Secured by Samsung Biologics in 2023

This has enabled Samsung Biologics to achieve another breakthrough in its performance. According to the company’s financial report, Samsung Biologics’ revenue for the first half of 2023 exceeded KRW 1587.1 billion (RMB 8.869 billion), representing a year-on-year increase of 56.4%.

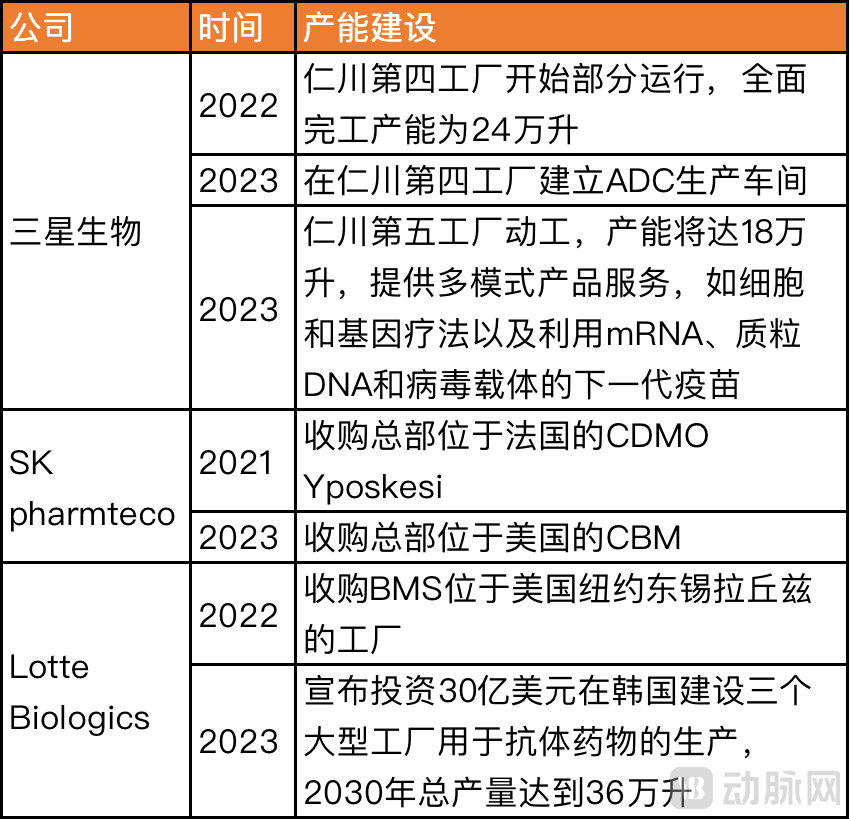

Samsung Biologics’ ample production capacity is one of the key reasons it can sustainably secure orders from multinational corporations (MNCs). The company’s existing four facilities have a combined total capacity of 604,000 liters, surpassing Lonza and Boehringer Ingelheim, while its fifth facility, with a capacity of 180,000 liters, is under accelerated construction.

Not only Samsung Biologics, but also SK Pharmteco under the SK Group and Lotte Biologics under South Korea’s Lotte Group are rapidly expanding their production capacities:

SK pharmteco previously acquired two CDMOs focused on CGT: Yposkesi and CBM (Center for Breakthrough Medicines). Yposkesi’s second manufacturing facility, currently under construction, will reach nearly 10,000 square meters upon completion this year, while CBM is expected to have approximately 65,000 square meters of production space by 2025.

Lotte Biologics announced early this year that it will invest $3 billion over the next seven years to build three large-scale facilities in South Korea for antibody drug production, with a total capacity reaching 360,000 liters.

South Korean CDMOs’ Recent Capacity Expansion Moves

Amid persistent overcapacity looming over the CDMO industry, three South Korean CDMOs backed by powerful conglomerates are pursuing an aggressive, high-profile strategy.

Why South Korean CDMOs?

The development direction of South Korea’s CDMO sector is inextricably linked to its strategic positioning in the biopharmaceutical industry,In 2014, the South Korean government formulated the “Prospects and Development Strategy for the Biopharmaceutical Industry,” opting not to compete with Europe and the United States in innovative drugs, nor to vie with India or China for the traditional generic drug market, but instead focusing on the biosimilar sector. Biosimilar development is complex and challenging to replicate, with prices and profit margins significantly higher than those of chemical generics. South Korea’s Celltrion was the first company globally to pioneer “antibody biosimilars.”

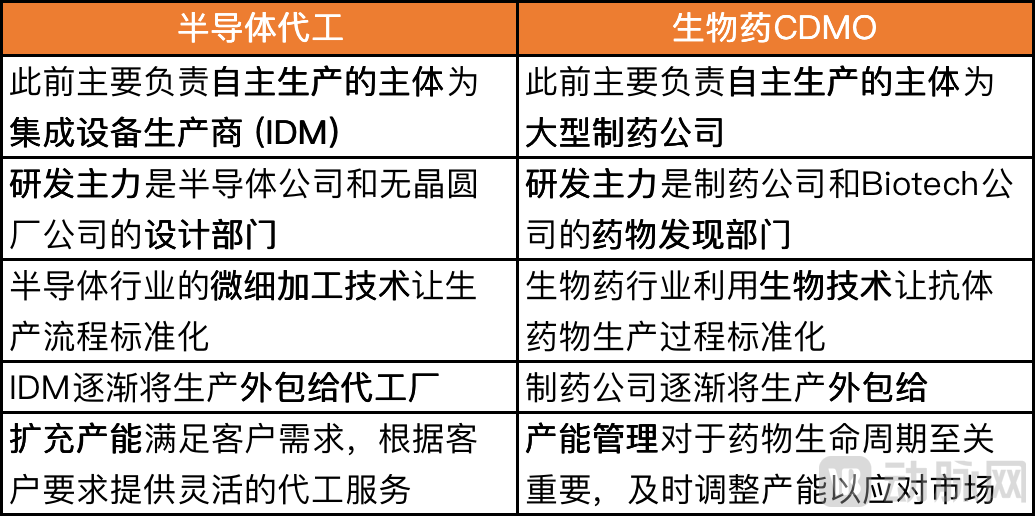

Therefore, South Korea’s CDMO industry also centers on biologics and biosimilars. Mirroring the high barriers to entry for biologics, biologic CDMOs face similarly elevated thresholds. Taking antibody production—the largest market segment and the most frequently commissioned service among South Korean CDMOs—as an example, the process involves multiple steps, including host cell selection and optimization, antibody gene cloning and vector construction, upstream process development, and downstream purification. Furthermore, as protein-based therapeutics, antibodies are sensitive to conditions such as temperature and pH, resulting in more complex quality standards and control requirements.

Compared with the production of small-molecule chemical drugs, biologic CDMOs not only demand more stringent process requirements but also require substantial production capacity, entailing high capital investment and long lead times.South Korean CDMOs typically rely on large conglomerates as their new growth curve, enabling industrialization and scalability from the outset. Meanwhile, the group’s extensive experience in the semiconductor industry can also be leveraged in biological drug CDMO services.

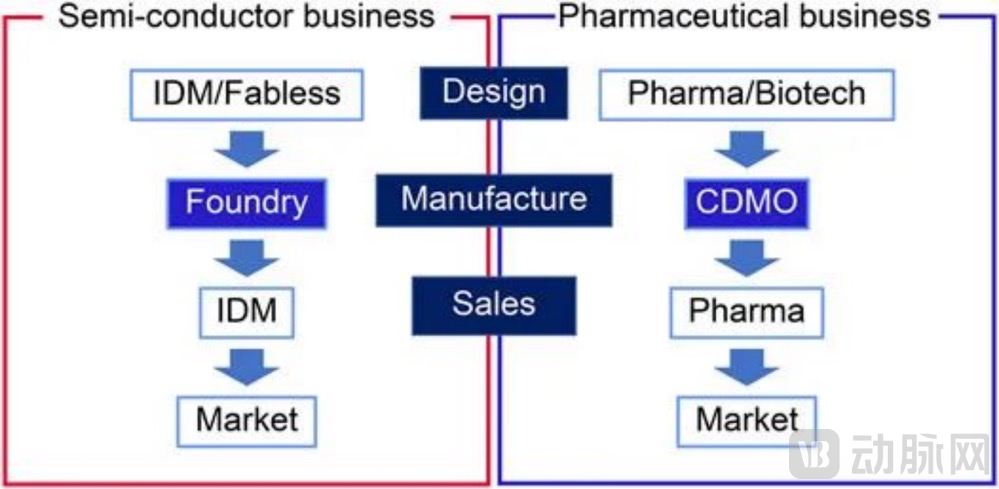

A Comparison of Production in the Semiconductor and Pharmaceutical Industries

Although the products of the semiconductor industry and the pharmaceutical industry are entirely different, both sectors bear the burden of rising costs for new product and production technology R&D. Prior to the biopharmaceutical industry’s adoption of such a model, the semiconductor industry established a horizontal division of labor in the 1980s. The development trajectory and historical evolution of technological platforms in the semiconductor sector offer insights into the key success factors for the biopharmaceutical CDMO industry.

Semiconductor Foundry vs. Biologic CDMO

Similar to semiconductor foundries, CDMOs can achieve production capabilities equal to or superior to those of originator companies by acquiring advanced manufacturing technologies and accumulating experience, thereby forming mutually beneficial and symbiotic partnerships with pharmaceutical companies and driving the rapid development of the entire industry.

For instance, in 2013, which can be regarded as the starting point for South Korea’s CDMO industry, Samsung Biologics’ first plant in Incheon was delivered and commenced operations, securing an order from Bristol Myers Squibb (BMS). BMS transferred the manufacturing technology for Opdivo to Samsung. Leveraging the technology and expertise provided by this major pharmaceutical company, Samsung Biologics soon secured orders for Roche’s rituximab, bevacizumab, and trastuzumab, and gradually expanded its client base to include multinational corporations (MNCs) such as Eli Lilly, GSK, AstraZeneca, Pfizer, and Novartis. During this process, Samsung Bioepis, a joint venture biopharmaceutical company under Samsung Biologics, rapidly developed its own biosimilar pipeline.

Of course, it is worth noting the “close ties” between the South Korean pharmaceutical industry and Western countries, particularly the United States. The National Biotechnology and Biomanufacturing Initiative signed by President Biden last September was interpreted as an effort to reduce U.S. reliance on China in the life sciences sector. Although this move did not cause significant disruption due to the inherent difficulty of decoupling in this field, the underlying concerns have yielded spillover benefits for South Korean companies.

Biotech cooperation between South Korea and the United States continues to strengthen,In April this year, the Korea Biotechnology Industry Organization and the Biotechnology Innovation Organization (BIO) of the United States signed an agreement to jointly ensure stable supply chain management. This includes sharing information on policy changes in both countries, as well as strengthening information exchange in research and development, drug production, and market trends.In this context, orders for South Korean CDMOs may proceed “more smoothly.”

China-South Korea Giants Clash: WuXi Biologics vs. Samsung Biologics

As one of the leading biologics CDMOs in Asia and globally, WuXi Biologics is a key competitor to Samsung Biologics.The IPOs of the two major CDMO companies occurred in close succession: Samsung Biologics listed on the main board of the Korea Exchange in November 2016, and WuXi Biologics spun off for a listing in Hong Kong the following July.

However, embroiled in the Samsung Group scandal and affected by the financial fraud controversy, Samsung Biologics experienced an operational crisis from 2017 to 2019, with slowed revenue growth and capacity expansion.This has provided Chinese biologic CDMOs with greater flexibility for development.

In terms of sales, WuXi Biologics’ global market share increased from 2.4% in 2017 to 12.8% in 2022, while Samsung Biologics’ figure stood at 9.2% in 2022. Based on 2022 revenue and net profit, WuXi Biologics reported RMB 15.269 billion and RMB 4.4 billion, respectively, whereas Samsung Biologics recorded RMB 16.8 billion and RMB 4.469 billion, indicating that the two companies are very similar in scale.

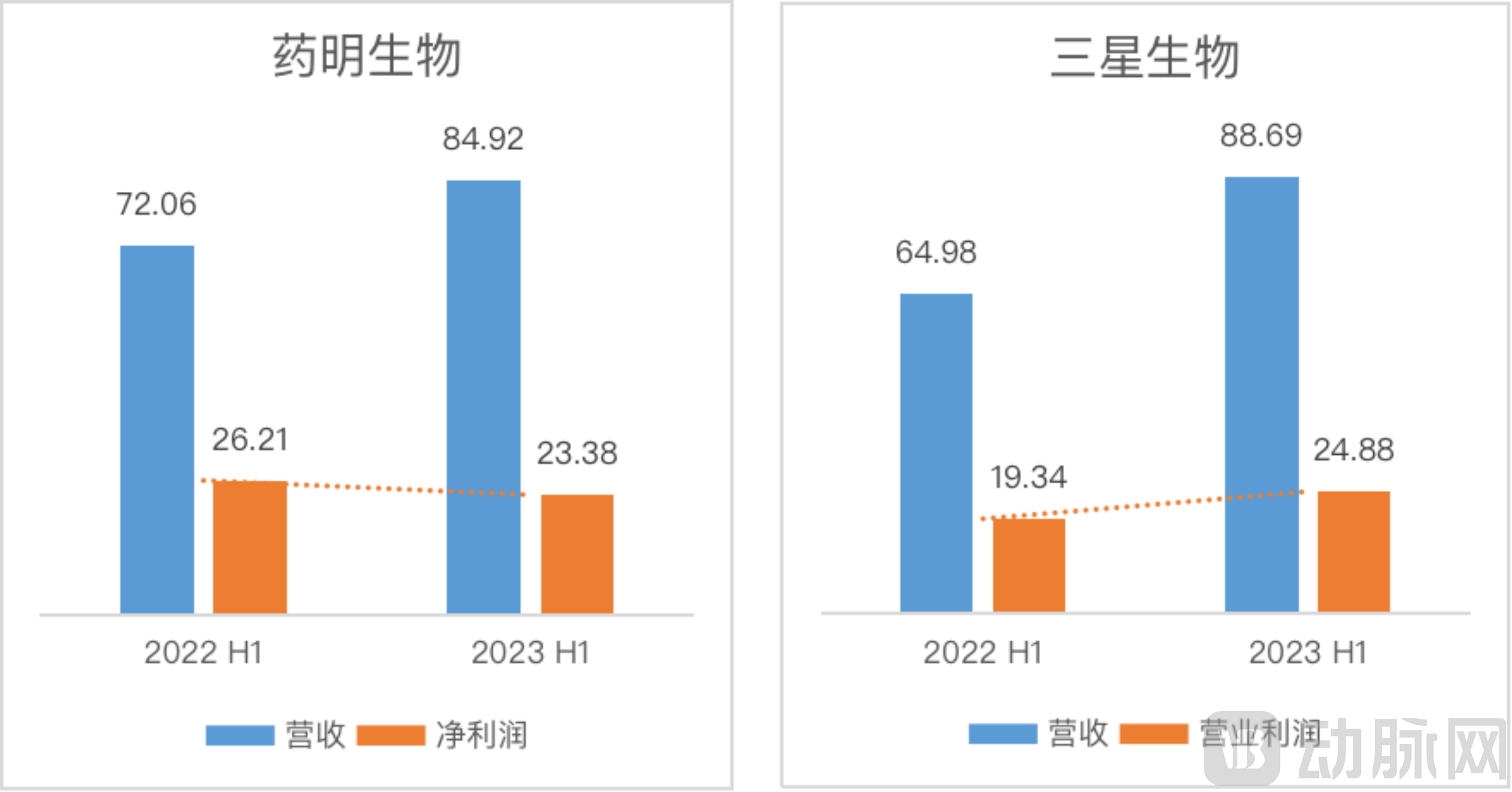

Notably, Samsung Biologics has exhibited an exceptionally rapid growth rate this year.In the first half of 2023, Samsung Biologics’ revenue reached RMB 8.869 billion, a year-on-year increase of approximately 36.5%, with operating income amounting to RMB 2.488 billion, up 28.6% year on year.

In contrast, WuXi Biologics reported revenue of RMB 8.492 billion, with a year-on-year growth rate of only 17.84%. Additionally, net profit declined by 10.81% year-on-year due to the revenue gap resulting from the end of the pandemic. At the Investor Open Day, the company disclosed that it had added 25 new CDMO projects in the first half of 2023 (before June 20), compared to 120 new CDMO projects added throughout the entire previous year.

Comparison of Revenue and Profit in the First Half of 2023 (Unit: RMB 100 Million), Compiled from Company Performance Reports

Nevertheless, WuXi Biologics’ substantial “inventory” can ensure the robustness of its business operations.As of the first half of 2023, the company’s backlog of unfulfilled orders aged over three years amounted to $3.5 billion. However, Samsung Biologics also disclosed in its earnings announcement that its order backlog for the first half of 2023 was approximately $1.566 billion, surpassing the full-year total for 2022.As Samsung Bioepis continues to secure major orders in the second half of the year, its backlog is also set to rise.

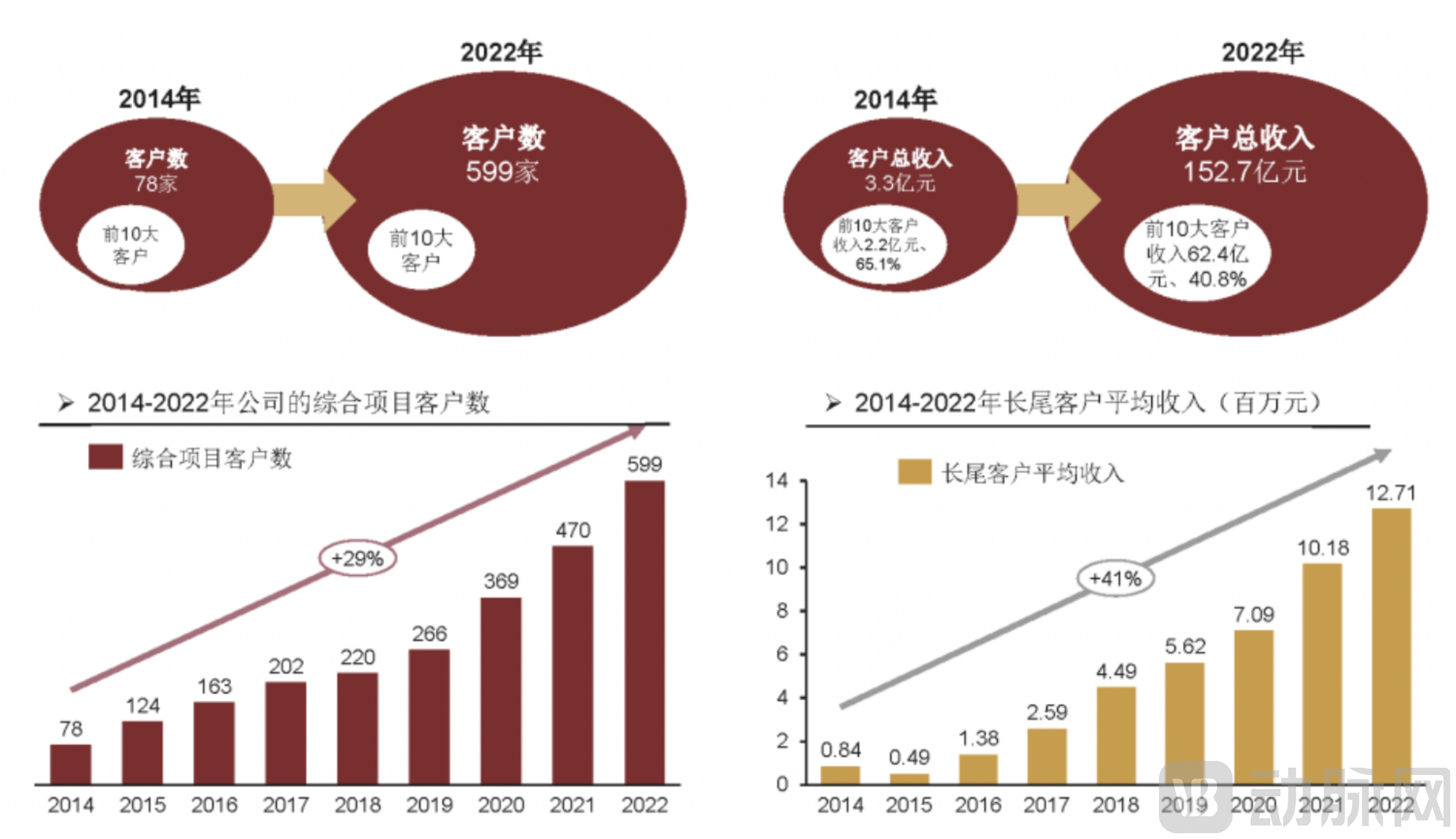

Regarding clients, Samsung Biologics has not disclosed specific details on the number or profile of its customers; however, based on orders and revenue, it can be inferred that its clientele primarily consists of large pharmaceutical companies.WuXi Biologics’ clients exhibit a distinct long-tail characteristic,While the revenue CAGR from the top 10 customers reached 52.3% between 2014 and 2022, their share of total revenue declined from 65.1% in 2014 to 40.8% in 2022.

Changes in the Number of Customers and Revenue of WuXi Biologics from 2014 to 2022, Source: China Merchants Securities

With its concentrated client base and prevalence of large orders, Samsung Biologics has achieved more full utilization of its production capacity, but this clearly entails a stronger dependence on major clients. In contrast, WuXi Biologics boasts a more diversified customer structure, particularly as the average revenue from its long-tail clients has risen year by year. This trend not only reflects deepening customer trust but also indicates that early-stage clients are progressively advancing to later-stage and commercialization phases, gradually evolving into more substantial sources of revenue.

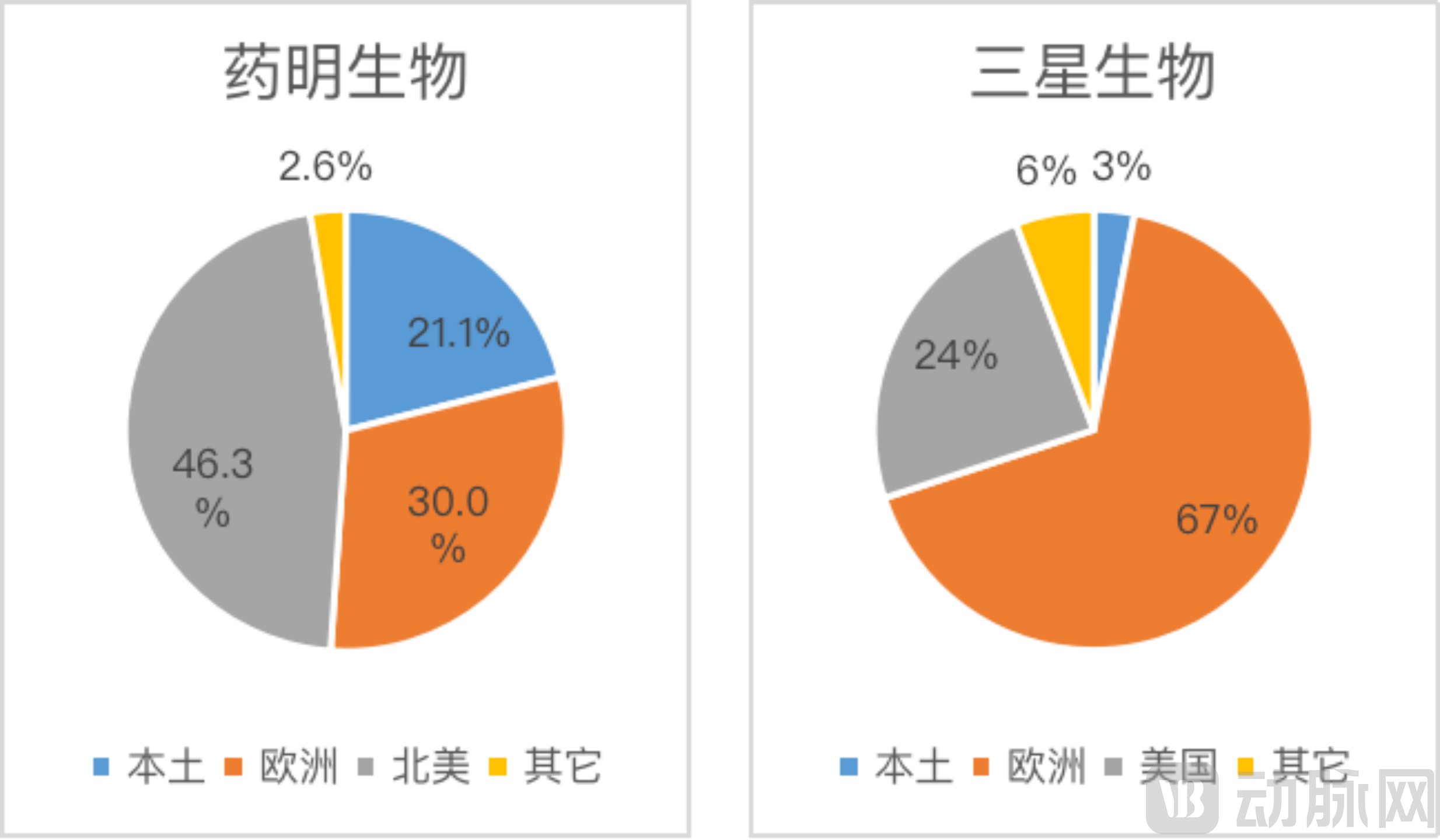

In terms of revenue distribution by region, WuXi Biologics has a more balanced profile. In the first half of 2023, 21.1% of the company’s revenue came from the domestic market, driven by the vast potential of China’s local market, whereas Samsung Biologics derived only 3% of its revenue from its home market.However, according to WuXi Biologics, its market share in Europe will gradually increase, which means it will directly compete with Samsung Biologics in its main battlefield.

Comparison of Revenue by Geographic Region in the First Half of 2023, Compiled from Company Performance Reports

What needs to match revenue is production capacity. In 2022, WuXi Biologics’ production capacity stood at 262,000 liters, still lagging significantly behind Samsung Biologics. However, WuXi Biologics’ capacity is expected to expand at an accelerated pace, reaching 588,000 liters by 2026. Moreover, unlike Samsung Biologics, whose capacity is relatively concentrated in Incheon, WuXi Biologics will have a more globalized footprint: 369,000 liters in China, 120,000 liters in Singapore, 30,000 liters in the United States, 30,000 liters in Ireland, and 15,000 liters in Germany.

In terms of production methods, Samsung Biologics’ business model relies on economies of scale, hence its commitment to using large stainless steel bioreactors. When WuXi Biologics entered the industry, it adopted single-use bioreactor technology to differentiate itself, offering greater flexibility and safety.

R&D capabilities in CDMOs will impact long-term development. In the first half of 2023, WuXi Biologics’ R&D expenditure amounted to RMB 340 million, while Samsung Biologics’ R&D spending reached RMB 670 million, more than double its full-year investment in 2022.Samsung Biologics is venturing into the ADC space and considering entry into the CGT sector, with its rapidly rising R&D expenses reflecting its expansion ambitions.Of course, the other two CDMOs in the WuXi AppTec ecosystem, WuXi XDC and WuXi Advanced Therapies, have also made substantial inroads into emerging fields.

Overall, while WuXi Biologics and Samsung Biologics differ significantly in their revenue models, as two CDMO leaders of comparable scale with closely matched growth trajectories, their competitive landscape is poised to intensify in the future.

Key Competitive Factors in Biologics CDMO: What Are China’s Advantages?

South Korea’s CDMO Sector Is Booming, Driven by the Global Race for Positioning in Biologics

In April this year, Samsung Biologics released its first report on the U.S. biosimilar market. Samsung Biologics pointed out that the introduction of biosimilars in the United States will stimulate market competition and “play a significant role in reducing healthcare costs in the U.S.” Particularly in the oncology sector, product prices dropped by nearly 50% within three years after the launch of relevant biosimilars.

Following the reduction in drug prices, biosimilar manufacturers have greater incentive to outsource production to low-cost contract manufacturing organizations (CMOs). Samsung Biologics recognized this trend more than a decade ago.

South Korea’s accurate foresight regarding biosimilars has enabled its biopharmaceutical companies to gradually enhance their influence in the Asia-Pacific region and even in the global biosimilar market in recent years. South Korean CDMOs have also established a clear identity as providers of biopharmaceutical contract development and manufacturing services, particularly for antibody drugs.

In recent years, China’s biopharmaceutical sector has been catching up, with the country’s biopharmaceutical CDMO industry also experiencing rapid growth.

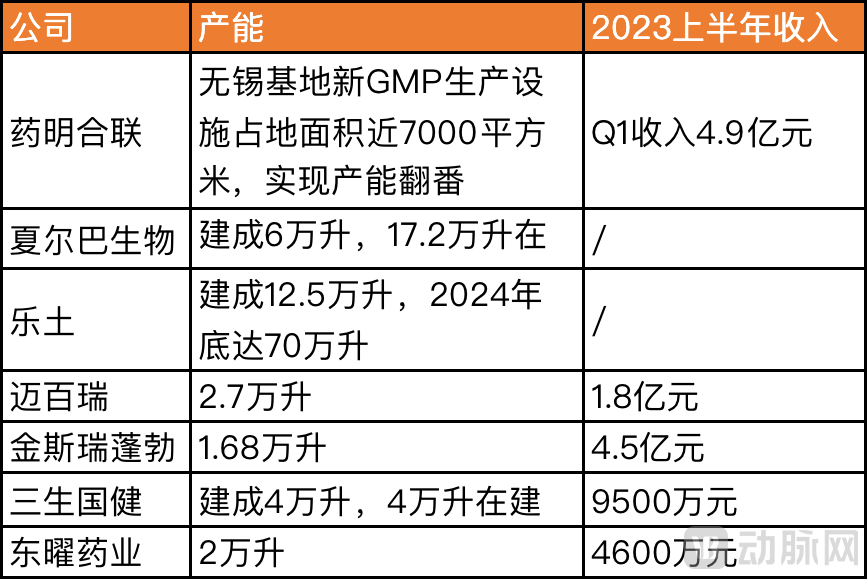

Biologic Drug CDMO Revenue and Capacity of Selected Domestic Companies, Compiled from Public Information

The most aggressive player in terms of capacity expansion is Letu. Letu previously invited Li Jianfeng, former General Manager of Lonza China, to join as Chief Commercial Officer, and engaged Michael Garvey, who oversaw the construction of Samsung Biologics’ first and second plants, for its facility development. Aiming to replicate the path of industry leaders, Letu Technology targets a production capacity of 1.05 million liters by 2025.

However, production capacity is only one metric. Higher capacity does not necessarily translate into the ability to take on more projects or generate higher revenue. Success also depends on customer acquisition, repeat purchases, accurate demand forecasting, and the agility to adapt to a rapidly changing market environment; otherwise, companies risk overextension.

There are also CDMOs established by biopharmaceutical companies, such as Sherpa Biologics. Biopharma’s manufacturing experience and product understanding provide inherent advantages. Since its establishment one year ago, Sherpa Biologics has seen a steady stream of orders and recently secured overseas contracts despite market headwinds. However, to ensure separation from Innovent Biologics, Sherpa Biologics provides only process development, manufacturing, and regulatory filing services, excluding early-stage R&D activities.

There is also the rapidly growing CDMO sector for antibody-drug conjugates (ADCs) over the past two years, represented by WuXi XDC and MabPlex. Although the principle of ADCs is clear, it is highly nuanced; the three components—antibody, payload, and linker—require iterative testing and balancing. For different tumors and tissue combinations, the experience and patience in manufacturing are precisely where domestic CDMOs excel. WuXi XDC’s market share reached 9.8% last year, and it continues to secure orders globally.

Nevertheless, the advantages of ADCs are widely recognized. Lonza continues to expand its ADC capabilities to maintain its leading position, while South Korean CDMOs are now also seeking a share of the market.

Low-price strategies can no longer serve as a competitive advantage when compared with or competing against South Korean biologic drug CDMOs.Reportedly, Samsung Biologics secured its massive orders at discounts of 20% to 30%, pushing the strategy of offering high-quality products at competitive prices to an extreme level of market competition.

Samsung Biologics’ low pricing is indeed staggering, but the crux of the matter remains whether its quality system can withstand audits.

Previously, Dr. Zhou Kaisong, CEO of Sherpa Biosciences, stated that the primary concern for overseas pharmaceutical companies remains the delivery capabilities of domestic CDMOs—specifically, their ability to deliver products on time, in full quantity, and with assured quality.

The engineer dividend is not exclusive to China’s CDMO sector; South Korea’s industrial accumulation and CDMO talent are equally capable of supporting the eastward shift of the global biopharmaceutical industry chain.Regarding compensation, South Korean CDMOs offer higher pay, yet they remain competitive compared to North America and Europe: In 2022, the average annual employee compensation at Samsung Biologics was nearly RMB 500,000, while according to WuXi Biologics’ annual report, its average employee compensation was approximately RMB 320,000.

In this regard, the life sciences team at Yuewei Capital stated that while domestic CDMOs demonstrate strong cost-control capabilities, they are also globally competitive in upstream technologies. Samsung Biologics’ current prominence lies primarily in the “M” segment—manufacturing. In contrast, Chinese CDMOs, particularly in the field of cell and gene therapy (CGT), have made significant strides in the R&D phase. For instance, GenScript ProBio had already assisted Legend Biotech in obtaining clinical trial approval for its CAR-T therapy as early as 2018, demonstrating its comprehensive end-to-end solution capabilities.

Another distinction from South Korea is that Chinese biopharmaceutical CDMOs can compete for the vast overseas market while also tapping into the immense potential of the domestic market. According to data from a Frost & Sullivan report, the size of China’s biopharmaceutical market reached RMB 449.3 billion in 2022.

As China’s biopharmaceutical industry undergoes iterative upgrades, with more innovative biologics entering the commercialization phase and expanding their global footprint, Chinese CDMOs capable of weathering the downturn are poised to embark on a new chapter alongside Chinese biopharmaceutical companies.

References:

1. “CDMOs Play a Key Role in the Biopharmaceutical Ecosystem”, https://mp.weixin.qq.com/s/D0kBypUpf3Eq9g9rvmzCVQ

2. “Are Multinational Pharma Companies Accelerating Their Decoupling from Chinese CDMOs? Samsung Biologics Receives Another Major Windfall,” https://mp.weixin.qq.com/s/RR5ysKiWHP5N9NH8FO5WJA