Eli Lilly Enters Radiopharmaceuticals Arena with $1.4B Point Biopharma Acquisition, Signaling a Strategic Shift Toward Nuclear Medicine

Eli Lilly, which has reaped substantial profits in the metabolic disease sector, announced its entry into the race for the radiopharmaceutical market by acquiring Point Biopharma in a deal valued at $1.4 billion, representing a 68% premium.The acquisition once again sends a clear signal: the radiopharmaceutical sector is heating up; beyond Novartis and Bayer, more multinational corporations (MNCs) are likely to enter the field and increase their investments in radiopharmaceuticals.

It is a clear trend visible to industry insiders that not only multinational corporations (MNCs) but also Big Pharma players are entering the radiopharmaceutical sector. Domestic participants include Grand Pharma, Hengrui Medicine, Kelun Pharmaceutical, Yunnan Baiyao, and Baiyang Pharma (which made a strategic investment in RadioDiag), among others. According to industry insiders,Since May this year, major pharmaceutical companies from Japan and South Korea have also conducted intensive visits to Xiantong Medicine, a pioneer in China’s generic drug industry transitioning into radiopharmaceuticals.

Since the beginning of this year, the question of whether radiopharmaceuticals have become a strategic battleground for major pharmaceutical companies has increasingly become a topic of discussion.

VCBeat has observed that an increasing number of industry conferences in China are establishing dedicated forums for radiopharmaceuticals. Some local governments have also recognized this opportunity, with Sichuan Province and Zhejiang Province taking the lead.

At present, radiopharmaceuticals remain a niche sector. According to industry estimates, the total domestic market in China is valued at approximately RMB 10 billion. What are the potential avenues for innovation and market growth in this field?Can it evolve from a ten-billion-yuan market into a hundred-billion-yuan market?is a critical issue for the industry.

On the flip side of this optimism, many seasoned industry insiders caution that the radiopharmaceutical supply chain is unique, and its development will require more time and patience.

An investor told VCBeat that they had been evaluating radiopharmaceutical projects throughout the first half of this year, noting that with a steady stream of new industry developments being disclosed, the sense of urgency to invest in radiopharmaceutical companies has remained constant.

From multiple perspectives, we can sense that nuclear medicine continues to gain momentum in the capital market this year.

Data shows that in the first half of 2023, global financing for radiopharmaceutical companies totaled RMB 3.047 billion. In Q2 alone, there were seven financing events, amounting to RMB 2.947 billion. Compared with mainstream modalities such as cell therapy and gene therapy, radiopharmaceuticals, as a niche sector, did not exhibit a substantial gap in total financing volume.

In Q3, nuclear medicine companies continued to demonstrate strong fundraising performance in the primary market, with global total financing reaching RMB 4.448 billion. In July, Xiantong Medicine, a leading domestic nuclear medicine enterprise, announced the completion of a new round of financing exceeding RMB 1.1 billion. Earlier this year, Xiantong had officially initiated its A-share IPO process.It is highly likely to become the first domestic radiopharmaceutical company to list on the capital market."The market reaction to its every move is likely to serve as a bellwether for the industry."

Let’s examine the current investment and financing trends in the radiopharmaceutical sector by looking at specific funding events and amounts.

First, companies across the industry chain continue to be favored by investors.In June, ITM announced the completion of a €255 million financing round led by Temasek, with participation from several renowned investment firms. This marks ITM’s third fundraising event in the past two years and represents the largest primary-market financing deal in the radiopharmaceutical sector this year.

Senior industry insiders told VCBeat that companies like ITM do not have strong competitiveness in the innovative drug sector and are currently merely followers. Investors remain bullish on ITM due to its radionuclide assets and the strategic importance of its upstream supply chain—a competitive advantage built over two decades that is difficult for other companies to replicate.

Eli Lilly’s Premium Acquisition of Point Biopharma: Beyond “Bullish on the Booming Radiopharmaceutical Industry,” William Blair Analyst Andy Hsieh Emphasized in a Report,Point: Ownership of the supply chain, namely Point’s 80,000-square-foot Core1 and 100,000-square-foot Core2 facilities in Indianapolis, as well as its 7,700-square-foot GMP facility in Toronto.

On October 17, Nucleus RadioPharma announced another oversubscribed $56 million Series A financing round,NucleusReportedly the world’s first company to fully integrate radiopharmaceutical development, manufacturing, and supply chain operations, it attracted investment institutions and funding amounts that both exceeded expectations, further validating investor confidence inFilling the Gap in Radiopharmaceutical Productionsignificant interest from enterprises. Prominent investors include GE HealthCare, the Mayo Clinic, and the University of Missouri. Through this round of financing, Nucleus RadioPharma will establish new production facilities in multiple locations across the United States, including Rochester, Minnesota, near the Mayo Clinic.

Secondly,Some early-stage R&D companies have also gained favor with investors.。

In China, this March, Hexin Pharma, which focuses on dual-target therapies, announced the completion of its Series A financing round exceeding RMB 100 million. The round was co-led by Cowin Capital and Shanlan Capital, with participation from several other institutions. Hexin Pharma’s lead product is among the first batch of innovative 68Ga-radiopharmaceuticals in China and has now entered Phase I clinical trials.

Not long ago, Hezhou Pharmaceuticals announced the completion of a seed funding round amounting to tens of millions of US dollars, co-led by FIL Capital. Notably, Hezhou Pharmaceuticals was co-founded by Professor Cheng Zhen, a renowned scientist in the global radiopharmaceutical field, and FIL Capital, with Professor Cheng serving as the Scientific Co-Founder of Hezhou Pharmaceuticals. FIL Capital also revealed that it had been actively monitoring the radiopharmaceutical sector for many years prior to establishing Hezhou Pharmaceuticals.

Various institutions are still entering the field, and leading scientists continue to launch startups, underscoring the significant innovation potential and opportunities in the radiopharmaceutical sector.

In the secondary market, RayzeBio listed on NASDAQ in late September. With a total fundraising amount of $311 million, it became the third-largest IPO globally in the innovative drug sector this year.

Foreign media outlets are discussing how such a substantial fundraising amount serves as a significant boost not only to the radiopharmaceutical sector but also to the entire biopharmaceutical industry, signaling a recovery in the market. On its first day of listing, RayzeBio’s stock closed up more than 33%. As of October 23, RayzeBio’s share price remained 7% above its IPO price.

What Should Investors Focused on the Radiopharmaceutical Sector Pay Attention to at This Stage?

First, who is behind the new domestic projects? An investor familiar with China’s radiopharmaceutical sector told VCBeat that they were unaware of Professor Cheng Zhen’s involvement in the startup before Nuclear Boat Pharma officially announced its financing news. This shows that inIn the field of radiopharmaceuticals, innovative domestic enterprises remain active, and there are also some promising under-the-radar projects.

Secondly, focus on the sales volume and indication breakthroughs of core products already on the market.

Novartis, which has secured the leading position in the radiopharmaceutical sector, is seeing substantial and continuing growth in demand for its flagship product, Pluvicto. In 2022, Pluvicto generated $271 million in revenue from just two quarters of sales. In the first half of 2023, it achieved $450 million in sales. According to Novartis’s recently released Q3 financial results, Pluvicto contributed an additional $256 million, representing a year-on-year increase of 217%. Sales over these three quarters have surpassed $700 million.Pluvicto is highly likely to become a $1 billion blockbuster drug this year.

Pluvicto is indicated for metastatic castration-resistant prostate cancer (mCRPC), a market substantially larger—potentially by an order of magnitude—than that of Lutathera, Novartis’s first approved radiopharmaceutical, which is indicated for gastroenteropancreatic neuroendocrine tumors (GEP-NETs). Moreover, Pluvicto is actively expanding its indications to include hormone-sensitive prostate cancer (HSPC), with the aim of advancing its use from third-line to second-line therapy.

As the patient population continues to expand and treatment protocols advance from third-line to second-line therapy, the supply chain for radiopharmaceuticals is being continuously strengthened.It is only a matter of time before Pluvicto’s sales surpass $2 billion.

Moreover, Pluvicto has sparked a wave of radiopharmaceutical R&D among pharmaceutical companies. Many firms have identified certain limitations in this product and see room for improvement. Novartis’s contribution extends beyond the approval of a single PSMA-targeted radiopharmaceutical; it may pave the way for the launch of a series of PSMA-based radiopharmaceuticals, creating a market worth tens of billions of dollars. For instance, Eli Lilly’s acquisition of Point Biopharma at this juncture was largely driven by the fact that Point has two radioligand cancer therapies currently in Phase 3 clinical development.

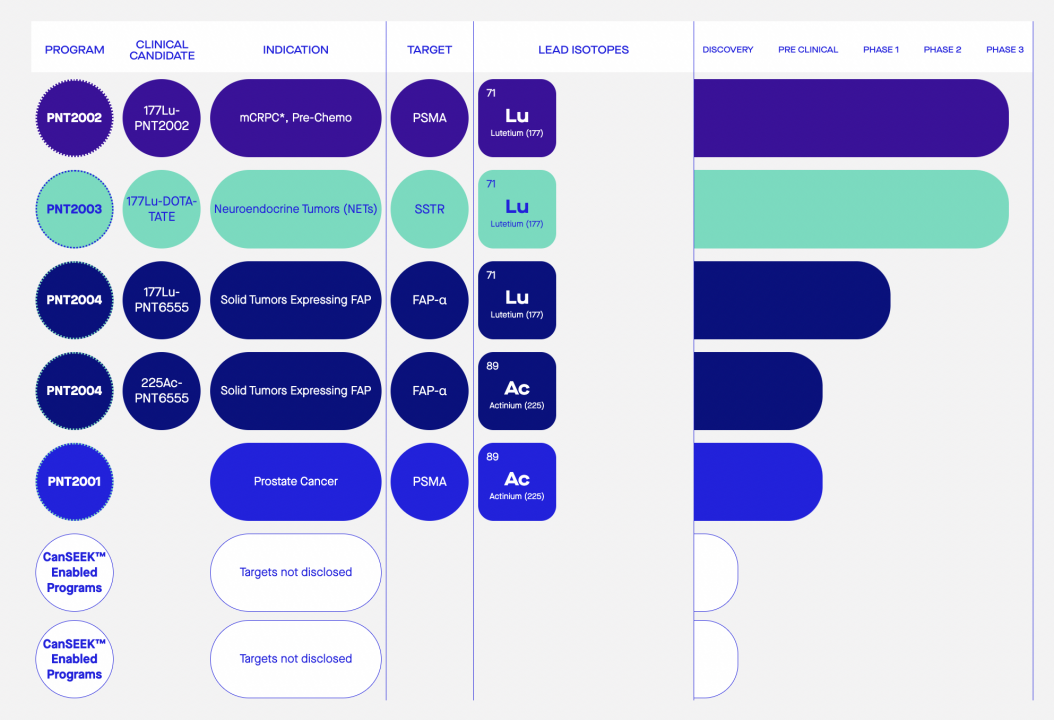

Point’s primary clinical asset is PNT2002, a PSMA-targeted 177Lu radiopharmaceutical therapy for metastatic castration-resistant prostate cancer (mCRPC).As this product is likely to compete head-on with Novartis’s Pluvicto in the future, the industry is eagerly awaiting the latest clinical data to be released this quarter.

Certainly, Point Biopharma has also made strategic moves in its innovation pipeline. Its pan-cancer FAP-α asset, PNT2004, is currently in Phase I clinical trials, while its next-generation Ac-225 PSMA project, PNT2001, is expected to enter clinical trials this year.

Point Pipeline Layout/Image from the Corporate Official Website

From a scientific perspective, the size of the future market for radiopharmaceuticals and its growth ceiling hinge on breakthroughs in novel targets and new radionuclides.

For instance, RayzeBio’s upcoming R&D pipeline is highly promising. Its core asset, RYZ101, is an investigational drug for neuroendocrine tumors that entered Phase 3 clinical trials in May this year, becoming the first Actinium-225 (Ac-225) radiopharmaceutical therapy to reach Phase 3. Previously, industry insiders were most concerned about the side effects of Ac-225-based radiopharmaceuticals; however, based on its selected targets and indications, the FDA currently considers its side effects to be manageable.

If the Phase III clinical trial of ryz101 achieves significant success, it will become the first approved Ac-225 radiopharmaceutical therapy in the industry, bringing a blockbuster product to the nuclear medicine market and unlocking greater growth potential.

From a commercial perspective, any discussion of the market potential for radiopharmaceuticals must address the factors that will become bottlenecks, including the supply of upstream radionuclides and the clinical adoption and promotion downstream.

Alpha radionuclide therapy is considered the next frontier in targeted radionuclide therapy. In addition to demonstrating superior clinical efficacy compared to beta radionuclides, alpha radionuclides offer the critical advantage of not relying on nuclear reactor production; they can be manufactured using cyclotrons, making them better suited to established manufacturing systems and market-driven operations. It is foreseeable that as the market matures, costs will gradually decline, “Once reactor-independent radionuclides become commercially available, a market worth tens of billions could be realized. However, this may not happen for another decade.“An investor emphasized.”

The issue of downstream clinical adoption and promotion—given factors such as the half-life of radiopharmaceuticals, the number of beds in hospital nuclear medicine wards, and bed turnover rates—directly determines how many patients can receive treatment, a calculation that many investors routinely perform.From a business perspective, the nuclear medicine industry chain in China still faces many challenges to reach a market size of hundreds of billions.

The true market size of radiopharmaceuticals still requires more time to validate, but senior industry insiders in China have observed a clear trend: Big Pharma is entering the radiopharmaceutical sector. In addition to Novartis, Bayer, and Eli Lilly, Genentech (a member of the Roche Group) has also joined the race. Domestic companies such as CSPC Pharmaceutical Group, Hengrui Medicine, Kelun Pharmaceutical, and Yunnan Baiyao have all entered the field. Major pharmaceutical companies in Japan and South Korea are also beginning to focus on opportunities in the radiopharmaceutical sector.

Novartis has solidified its leading position in the global radiopharmaceutical sector with Lutathera and Pluvicto, two products acquired through M&A; Targeted Radionuclide Therapy (TRT) is one of the three key pillars driving growth in Bayer’s oncology business. Having reaped the benefits of their foray into radiopharmaceuticals, both companies continue to ramp up their investments, serving as the strongest endorsement for the industry.

In the statement announcing the acquisition of Point, Jacob Van Naarden, President of Eli Lilly’s Oncology Division, made no secret of the company’s ambitions in the field of radiopharmaceuticals: “The acquisition of Point marks the beginning of our investment in developing a diverse portfolio of meaningful radioligand therapies to treat hard-to-treat cancers.”

Most importantly, with this acquisition, Eli Lilly will engage in direct competition with Novartis. Industry insiders believe that such healthy competition at this stage will have a positive impact on the entire radiopharmaceutical industry. As a relatively conservative company, Eli Lilly is rarely seen as a first mover. However, having achieved remarkable success in the metabolic disease sector, Eli Lilly needs to identify its next growth engine, and radiopharmaceuticals represent a promising option.

Just before Eli Lilly acquired Point,Genentech, a member of the Roche GroupReached a new multi-target collaboration and licensing agreement with PeptiDream, announcing entry into the field of radiopharmaceuticals through this partnership, which aims to discover and develop novelMacrocyclic Peptide–Radioisotope (Peptide-RI) Conjugate Drugs.

Endorsement by mainstream players has served as a strong catalyst for the development of the radiopharmaceutical industry, both in the capital markets and in downstream clinical applications. In China, the radiopharmaceutical sector’s activity in the capital markets began to gradually increase following Grand Pharma’s acquisition of Sirtex in 2018.

So, can radiopharmaceuticals truly become a key battleground for major pharmaceutical companies in the future, just like ADCs?

Optimistic voices suggest that,In another three to five years, multinational corporations (MNCs) may enter the radiopharmaceutical sector with the same fervor they are currently showing in their ADC pipelines, potentially even sealing deals worth tens of billions of dollars.Of course, domestic investors would also welcome seeing an increasing number of Chinese nuclear medicine products being licensed out in the future, similar to ADCs.

However, cautious voices warn that the aggressive acquisition strategies and clinical promotion capabilities demonstrated by multinational corporations (MNCs) in the radiopharmaceutical sector are not replicable for every company. The unique characteristics of radiopharmaceuticals, including stringent regulatory oversight and constraints within the upstream supply chain, indicate that not all Big Pharma companies will pursue radiopharmaceutical development at this stage. For the foreseeable future, the industry will remain constrained by supply chain challenges.

Only when supply chain challenges are resolved and radiopharmaceutical products break through into first-line therapy will this sector become a fiercely contested battleground for major pharmaceutical companies. Therefore, we must wait and see how the situation unfolds.

China’s radiopharmaceutical industry remains dominated by biotech firms. Industry veterans have called on VCBeat for practitioners to exercise greater patience and pursue more focused innovation in the development of the radiopharmaceutical sector. “Eli Lilly’s acquisition of a company signals its strategic positioning in this field; however, a single company cannot sustain an entire therapeutic area or market segment. We will certainly continue to monitor radiopharmaceutical projects in the future.”Domestic radiopharmaceutical companies can find opportunities by demonstrating innovation and executing projects to the highest standard.”