Layoffs Amid Fundraising: CGT Pioneers Strive to Avoid Becoming Washed-Up

Beam Therapeutics

Gene Technology Developer

Recently, Beam Therapeutics, co-founded by star scientists Feng Zhang and David Liu, announced that it would lay off 100 employees, representing 20% of its workforce, suspend certain research activities, and seek partners for the development of some drug candidates.

As a star company in the CGT sector, a noteworthy platform-based enterprise, and the first publicly traded base editing company, Beam Therapeutics saw its stock price reach as high as $130. Within three years of its founding, the company developed a pipeline of seven candidates and invested nearly $100 million to build its own GMP manufacturing facility.

Beam’s layoffs had long been foreshadowed; the company reportedly dismissed multiple contractors in the first half of the year, and several months later, the cuts extended to full-time employees.

An industry expert summarized to VCBeat: “Beam’s adjustments have their own specific requirements, but they also represent another ‘necessary’ move in the current sluggish market environment. The company previously spread its team and pipeline too thin. From a technical perspective, it remains a leader in the field of base editing and is still distinct from other players such as Editas. It can only be said that as new technologies continue to emerge, its competitive advantage should gradually diminish, which is a natural law.”

However, around the time of Beam’s layoffs, good news emerged from other companies competing in the in vivo gene editing space:Intellia’s in vivo CRISPR gene-editing therapy has been approved to proceed to Phase III clinical trials, while Verve has disclosed that the clinical hold on its base-editing therapy VERVE-101, designed to treat genetic forms of high cholesterol, has been lifted.

Meanwhile,Data on global biopharmaceutical financing in the first half of 2023 show that CGT companies still occupied the majority of large-scale funding rounds,Including: ElevateBio secured $401 million in Series D financing, ReNAgade Therapeutics launched a $300 million Series A financing round, Metagenomi completed a $275 million Series B financing, and Orbital Therapeutics announced the successful completion of a $270 million Series A financing—the company was spun out from Beam.

Pioneers in CGT continue to press forward, yet recreating the Moderna legend appears increasingly difficult.

Why Are Star Platform-Based CGT Companies No Longer in Favor?

Beam is primarily focused on the commercialization of the base editing technology invented by David Liu’s team. Base editing employs chemical processes to alter specific nucleotides within target genes; however, off-target deamination by deaminases may introduce biases in base editing enzymes unless precise targeting is achieved.

The FDA has always been cautious in its approach to gene editing, with even greater concerns regarding base editing. Last year, the FDA placed a clinical hold on the Investigational New Drug (IND) application for BEAM-201, a CAR-T therapy candidate, requiring additional control data from genomic rearrangement assessments, further analysis of certain off-target editing experiments, and other relevant information.

Following this adjustment, BEAM-201 has also been strategically deprioritized.

The pipelines subsequently prioritized for resource allocation are: BEAM-101, a clinical-stage ex vivo base editing therapy for sickle cell disease, and BEAM-302, an in vivo base editing therapy for alpha-1 antitrypsin deficiency (AATD).

However, Beam’s clinical recruitment progress has remained lackluster. More than a year after BEAM-101 received clinical trial approval, the administration of the first dose to a patient has yet to be reported. This may be attributable to issues with Beam’s underlying technology platform.

Platform companies like Beam Therapeutics were once the most popular type of project. Proprietary R&D platforms can help develop multiple products based on similar technologies but for different indications.

In the process of new drug development, companies with platform technologies can significantly accelerate R&D progress in areas such as target and technology validation, indication selection, lead compound optimization, and preclinical activity studies. Analysis reveals that platforms effectively reduce the time required to generate the next clinical asset. Compared with non-platform companies, platform-based companies can shorten the average time to develop their second, third, fourth, and fifth clinical assets by 7 months, 3 months, 5 months, and 8 months, respectively.

Rapid growth, swift fundraising, fast spending, and high valuations are all characteristics of platform-based companies.Moderna is undoubtedly the quintessential example of the “myth” surrounding platform-based companies, but the opportunity to leverage the COVID-19 pandemic for a meteoric rise to industry giant status was a one-time event. In the post-pandemic era, Moderna has been seeking new growth drivers in areas such as oncology, respiratory syncytial virus (RSV), and influenza. The substantial capital reserves accumulated from its COVID-19 vaccine sales will enable Moderna to sustain these strategic explorations for an extended period.

In the current high-interest-rate environment, platform companies that have failed to develop their own products will face even greater hardships.The most devastating impact of interest rate hikes on unprofitable biotech companies is the increased cost of capital, which leads asset allocation to demand higher returns or more stable profitability.

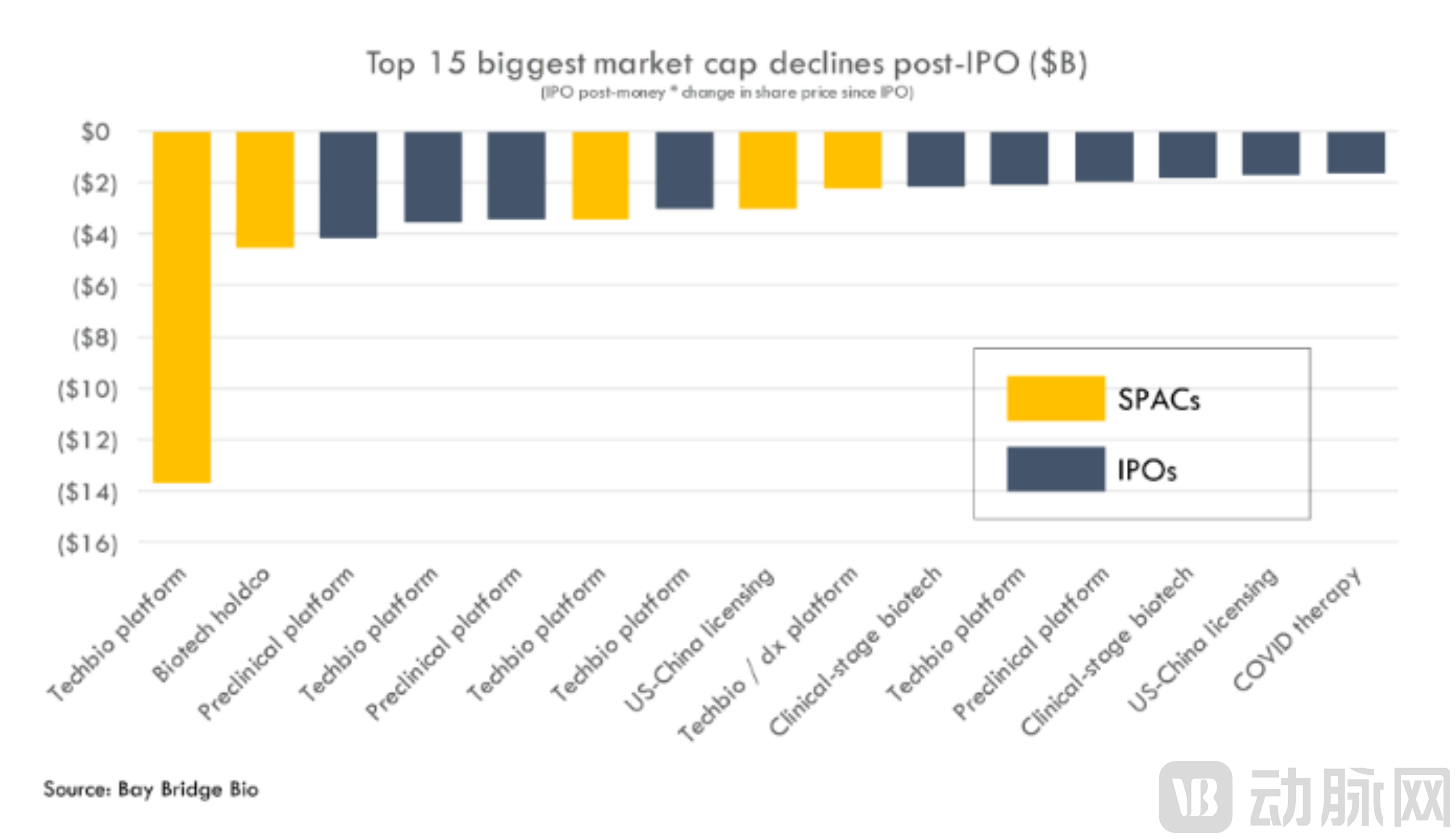

According to Bay Bridge Bio, among more than 500 listed biotech companies since 2010, 5% are platform-type companies; however, seven of the ten worst-performing companies are platform-type. On the other hand, the best-performing companies all possess de-risked assets, namely approved products or products in pivotal trials.

24 CGT Companies Lay Off Staff: Time to Return Focus to Products

In the biopharmaceutical sector, facts speak louder than words. Robust clinical data serve as the currency of value for biotechnology, and such high-quality data stem from superior products.

Most value derives from first-in-class or best-in-class products. The combined value of hundreds of R&D-stage projects pales in comparison to that of a single approved blockbuster drug. Therefore, a valuable platform is one capable of identifying a small number of high-value products, rather than generating a large volume of mediocre ones.

Cell and gene therapy (CGT) is one of the sectors with the highest concentration of platform-based companies. However, it is evident that a significant number of foreign CGT companies are refocusing their pipelines, streamlining their workforce, and reducing operational costs.According to Fierce Biotech statistics, 24 of the 119 biotech companies that announced layoffs were CGT firms, accounting for more than 20%.

CGT Companies That Underwent Layoffs and Restructuring Abroad in 2023, Compiled from Fierce Biotech

Among them are pioneers in the field of CGT, such as those who have long monopolized the ZFN technology route.Sangamo, despite implementing rigorous protection of its technology platforms and patents for many years, failed to advance any of its pipelines into late-stage development, leading major pharmaceutical companies that had previously partnered with Sangamo to withdraw one after another.

Of course, not all layoffs and downsizing will have a negative impact. For example, Nkarta, a star company in CAR-NK cell therapy that recently laid off employees,Announced its focus on applying off-the-shelf cell therapies to autoimmune diseases, and announced that the FDA had approved its Investigational New Drug (IND) application for NKX019, a CAR-NK cell therapy, for the treatment of lupus nephritis, marking the first expansion of this therapy into this indication. Following this announcement, the company’s stock price surged by 112%.

In recent years, the expansion of CGT into the autoimmune disease space reflects emerging technologies’ efforts to precisely identify and broaden their market opportunities.The global market for autoimmune disease therapies is projected to grow from $120.6 billion in 2020 to $146.1 billion in 2025, representing a compound annual growth rate (CAGR) of 3.9%. Many currently marketed drugs suffer from limitations such as lack of disease specificity, low patient response rates, and significant side effects, leaving substantial unmet clinical needs. In contrast, cell and gene therapy (CGT) offers multifaceted advantages and favorable efficacy in treating autoimmune diseases. CAR-T therapy can not only selectively eliminate aberrant B cells but also holds the promise of achieving immune reconstitution.

In addition to systemic lupus erythematosus, the disease with the strongest association, multiple companies are also attempting to tackle indications such as scleroderma, myositis, nephropathy, and neuromyelitis optica spectrum disorders.

An investor once stated to VCBeat, “The logic that a technology platform alone can attract investment no longer holds; there have been virtually no pure-platform projects this year. Investors are not disregarding platforms, but rather require the value of a platform to be validated through its products.”

Successful product validation, including whether large pharmaceutical companies are willing to invest real capital for short-term adoption and use, and whether the drug molecule demonstrates excellent clinical performance and achieves regulatory approval for market launch in the long term.

Yet enduring companies still require a platform as their foundation. This may seem paradoxical, but history shows that the way to resolve this paradox is to follow Bob Swanson’s approach when founding Genentech: focus on products and build a platform that supports them, rather than focusing on the platform for its own sake.

A CGT entrepreneur in Boston remarked, “CGT remains a widely watched hotspot, but platform companies are heavily influenced by the broader environment—with both manufacturing and application segments trending downward. This places greater emphasis on whether platform companies can support proof-of-concept efforts in manufacturing and applications, or generate revenue at an early stage. It appears that investors now have higher expectations for platform companies. These expectations have always existed, but in the current climate, ‘future aspirations’ have turned into ‘immediate demands.’”

What is the current state of the CGT sector in China?

As an emerging field, the gap between domestic and international companies in cell and gene therapy (CGT) is relatively small. In terms of addressing scientific challenges, Chinese companies with core foundational technologies are even ahead of their U.S. counterparts in certain underlying technologies. Consequently, domestic CGT companies possess strong global competitiveness; however, they must navigate uncharted territory lacking direct benchmarks, and contend with the potential impact on their business should industry pioneers suddenly halt progress or encounter significant setbacks.

“This year, I have sensed a decline in domestic enthusiasm for CGT, with the market no longer chasing mere concepts. Stakeholders are now genuinely focusing on issues related to market dynamics, commercial value, and overall market size, after all, approved drugs are either facing poor sales or commanding low prices,” said Xia Yukun, a biopharmaceutical investor.

“The overall cooling of Biotech investment means that concepts alone are no longer sufficient; certainty is now required. Therefore, it is essential to deliver valuable products. CGT platforms that rely solely on conceptual narratives are no longer viable,” summarized another investor regarding the current state of China’s CGT sector this year.

Nevertheless, financing in China’s CGT sector has not cooled off this year. As of Q3, more than 50 companies in the domestic CGT field had secured cumulative investments and financing totaling nearly RMB 9 billion. Among them, over 24 CGT companies (excluding CDMOs and others) each raised more than RMB 100 million.

Domestic CGT Companies That Secured Financing in 2023, Compiled from Public Information

An examination of companies that have secured substantial financing reveals that, in most cases, their pipeline progress and positive clinical data have demonstrated corporate certainty, thereby instilling market expectations and confidence in cell and gene therapy (CGT).

For example, BendGene’s investigational new drug (IND) application for its BD111 injection was approved by the U.S. FDA in July. The drug is indicated for herpes simplex virus type 1 (HSV-1) stromal keratitis and represents the first CRISPR-based antiviral orphan drug approved by the FDA worldwide. It is also the third in vivo gene-editing therapeutic candidate globally to enter the IND and clinical stages, following the in vivo gene-editing pipelines of Editas Medicine and Intellia Therapeutics.

Shali Biologics’ first-generation TIL product is poised to enter pivotal Phase II clinical trials, its second-generation gene-edited TIL product has received clinical trial approval in China, and its next-generation gene-edited TIL product is currently in the early stages of research and development.

During this year’s ASCO, Gracell Biotechnologies presented long-term follow-up data from a multicenter clinical study evaluating its proprietary BCMA/CD19 dual-target autologous FasTCAR-T therapy, GC012F, for the treatment of relapsed/refractory multiple myeloma (RRMM), demonstrating profound and durable efficacy. Furthermore, its FasTCAR next-day manufacturing platform for autologous CAR-T cells enables production completion within just 22–36 hours.

In June this year, Reindeer Bio’s BCMA CAR-T therapy, equecabtagene autoleucel injection, was launched for the treatment of adult patients with relapsed or refractory multiple myeloma. Although this product initially lagged behind in clinical development approvals, it managed to catch up and surpass competitors thanks to its exceptional execution capabilities.

China’s risk-based, stratified dual-track regulatory model has fueled the robust growth of the CGT industry and will inevitably continue to support Chinese innovative drug companies in pursuing a differentiated development path in frontier fields.

The number of clinical trials for cell and gene therapy (CGT) in China is growing rapidly. Between 2015 and 2020, approximately 250 CGT clinical trials were conducted cumulatively, making China the region with the second-highest number of trials after the United States. The compound annual growth rate exceeded 60%, ranking first globally. Currently, there are about 100 ongoing CGT clinical trials in China, involving approximately 80 companies.

Drawing on a previous interview with He Zhiyong, CEO of Aikai Bio, we can once again summarize the current landscape: “Pioneers have paved the way, highlighting the scientific challenges and potential risks that must be addressed in product development within this sector. As newcomers to the industry, we heed the warnings from these trailblazers and are charting our own distinct path for Chinese biotech companies.”