2023 Surgical Robotics Industry Research Report: Core Trends, Product Landscape, and Strategic Insights

Robots are hailed as the crown jewel of manufacturing. In recent years, technological research and product development in medical robotics have continued to advance. Surgical robots represent the largest and most significant segment within the medical robotics sector, and have emerged as star projects in the capital markets.

Based on continuous follow-up and the latest industry research, VCBeat will soon release the “2023 Surgical Robotics Industry Research Report.” This report analyzes recent financing activities and policy developments in the surgical robotics sector, examines the technology and commercialization across seven key sub-segments, and explores pathways for the growth of domestic surgical robotics companies amid internal and external challenges.

Below are selected charts and insights from the report. Stay tuned!

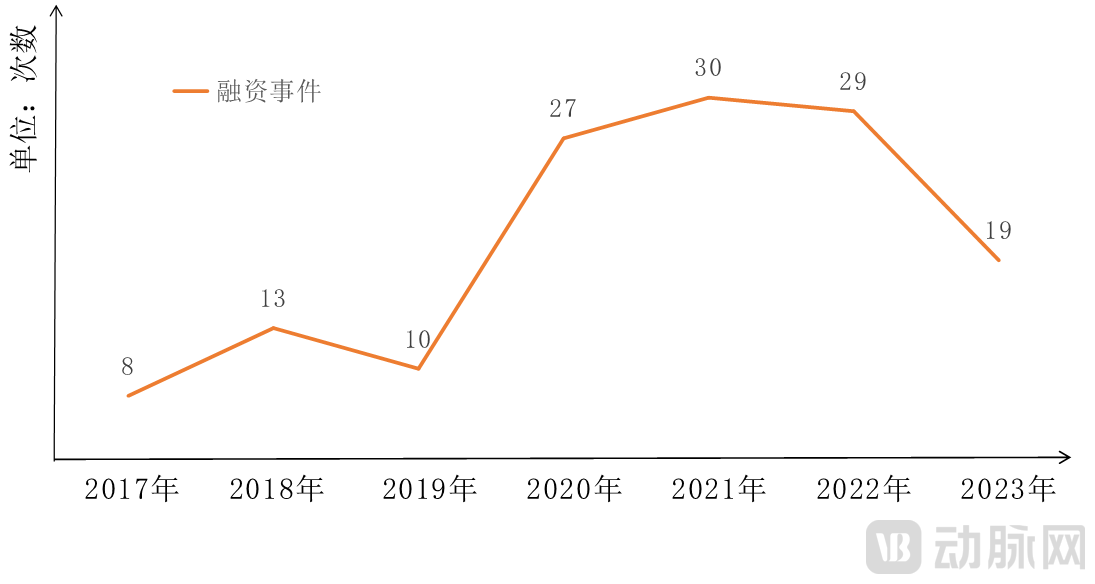

Chart: Number of Financing Rounds in the Surgical Robotics Sector in Recent Years

Image source: VCBeat

According to incomplete statistics, the surgical robotics sector saw 27, 30, 29, and 19 financing events in 2020, 2021, 2022, and 2023 (as of September 30), respectively. With over 100 financing rounds across these four years, the sector has demonstrated remarkable overall performance.

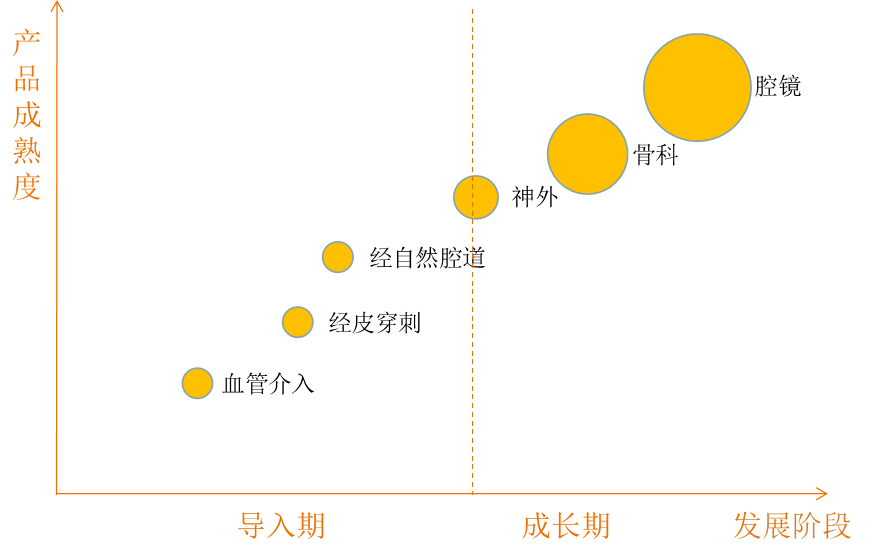

Chart: Maturity and Development Stages of Surgical Robot Products by Category

Image source: VCBeat.

Currently, apart from laparoscopic surgical robots, most surgical robots are still in the stage of "specialization."From the perspective of applicable clinical departments, the da Vinci Surgical System is indicated for urology, gynecology, and general surgery. Domestic companies specializing in endoscopic systems have largely followed da Vinci’s trajectory, expanding their approved indications from single specialties to multiple disciplines, while evolving their products from imitation to innovation under the guidance of this “benchmark.” In other categories of surgical robots, orthopedic and neurosurgical robots are relatively mature, with domestic and international products competing on the same stage. Meanwhile, vascular intervention, percutaneous puncture, and natural orifice transluminal endoscopic surgery (NOTES) robots have progressed from a nascent stage to an initial development phase, with the competitive landscape still unsettled.

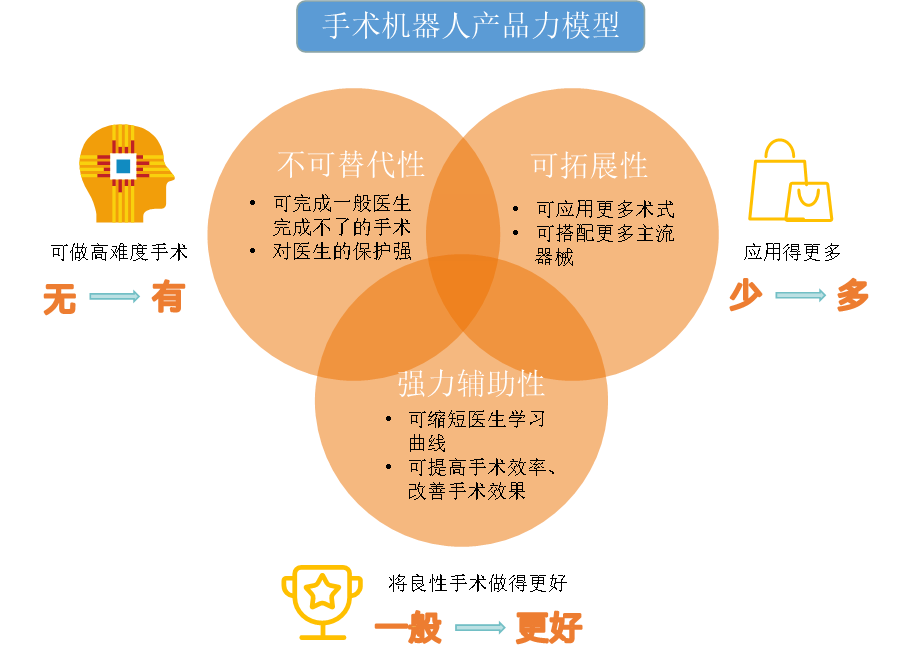

Product Competitiveness Model of Surgical Robots

In terms of application, product strength—the core value delivered by surgical robots—is fundamental.We believe that the product competitiveness of surgical robots primarily encompasses three aspects: irreplaceability, robust assistance, and scalability. Irreplaceability refers to the ability of surgical robots to perform high-difficulty procedures that are beyond the capabilities of most surgeons, thereby addressing "complex problems." This enables the initiation of certain highly complex surgeries that were previously unfeasible and provides enhanced protection for surgeons. Robust assistance refers to the capacity of surgical robots to shorten the learning curve for surgeons, improve the efficiency of routine procedures, reduce operative time, and enhance surgical outcomes, thus elevating the management of "basic problems" in standard surgeries from adequate to optimal. Scalability mainly pertains to product application and market adoption, allowing for a broader range of surgical procedures and compatibility with more mainstream instruments, thereby expanding applications from limited to extensive.

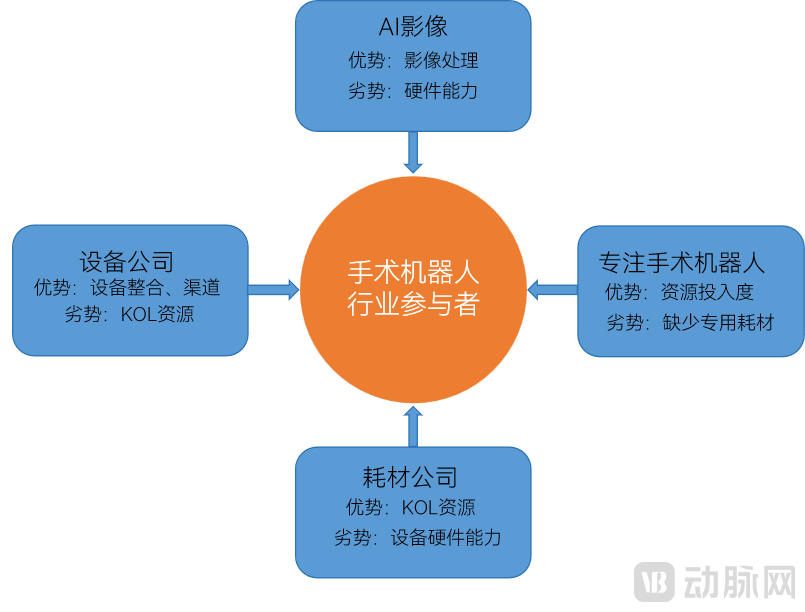

Chart: Four Types of Companies in the Surgical Robot Layout

Image source: VCBeat

From a corporate layout perspective, there are currently four main types of companies involved in the surgical robotics sector.In addition to companies focused exclusively on surgical robots, equipment manufacturers and consumables suppliers have entered the market by expanding their product portfolios or through mergers and acquisitions. Meanwhile, AI medical imaging companies are also positioning themselves in the surgical robotics sector. Overall, these four types of enterprises each possess distinct characteristics: equipment and consumables companies hold advantages in distribution channels, while AI imaging companies excel in image processing capabilities. However, equipment companies may lack sufficient Key Opinion Leader (KOL) resources, and both consumables suppliers and AI imaging companies may face limitations in hardware capabilities.

Disclosure of Views in the Report

● The surgical robotics sector is heating up, with over 100 financing rounds completed in China over the past four years. The primary drivers include substantial and unmet clinical needs, the strong market performance of the da Vinci Surgical System, and the “gap” in robotics offerings among major players in China’s medical device industry.

● The product strength of surgical robots is mainly reflected in three aspects: irreplaceability, powerful assistance, and scalability. In terms of product promotion, the da Vinci system entered the market by leveraging its irreplaceability, addressing high-difficulty surgeries that are challenging for general surgeons to perform. At the current stage, the conditions for promoting surgical robots based on their “powerful assistance” capabilities may already be in place.

● Mergers and acquisitions among international giants have largely occurred in the orthopedics sector, aiming to bundle surgical robots with consumables for joint sales. However, China’s centralized volume-based procurement of medical consumables has weakened this business model. In the field of laparoscopy, domestic single-port systems have received regulatory approval, accelerating the pace of import substitution with Chinese-made products.

● Overall, the pricing policy for surgical robots aims to steer them back toward clinical value and higher-value innovation, encourage coverage of core procedures and the entire workflow, and, in the long term, drive high-quality development across the industry.

● In terms of functional evolution, surgical robots will cover core operations throughout the entire workflow, from preoperative to intraoperative stages. Additionally, this phase will see an expansion in applications, encompassing a broader range of surgical procedures, such as comprehensive orthopedic and pan-vascular solutions.