Domestic Sequencing Instrument Industry Report: Nearly 30 Products Commercialized, Opening a Critical Window for Market Restructuring

The Rise of Domestic Sequencers Has Become a Notable Focus.

According to statistics from VCBeat Research Institute, excluding Sanger sequencers, nearly 20 companies in China have disclosed their independently developed sequencing instruments. Among these, nearly 30 models have been announced as commercialized, and eight have received approval from the National Medical Products Administration (NMPA). Chinese enterprises are deeply engaged in the development of both high-throughput sequencers and emerging single-molecule sequencers.

Nevertheless, achieving large-scale commercialization remains a major challenge for domestically produced sequencers. This requires manufacturers to continuously enhance product stability and reliability, accurately address the genuine needs of target markets, and rationally expand application scenarios. The “2023 Industry Research Report on Domestically Produced Sequencers” aims to explore the driving forces behind the surge in domestically produced sequencers and analyze how to accelerate their commercial deployment. To this end, VCBeat conducted surveys with eight sequencer manufacturers and three gene sequencing service providers, interviewed eleven industry experts, and compiled this report.

The following is an excerpt from the report:

The gene sequencing industry chain is divided into three segments: upstream, midstream, and downstream. The upstream segment comprises suppliers of gene sequencing instruments, consumables, and reagents, who develop and manufacture the equipment, materials, and reagents required for gene sequencing, thereby providing foundational support for the entire industry. The midstream segment consists of gene sequencing service providers, including laboratories, research institutions, and sequencing service companies. These entities build large-scale sequencing platforms, provide sequencing services to other users, and develop gene sequencing-related applications. This segment features numerous sub-sectors and faces more intense competition than the upstream segment. The downstream segment includes end consumers of sequencing-related applications or services, represented by research institutions, pharmaceutical companies, hospitals, and the general population.

The Position of Sequencers in the Ecosystem

Data Source: Compiled from public information; Chart by VCBeat.

The "Impossible Trinity" of Sequencing Technologies: Complementarity Among Various Approaches

Gene sequencing technologies include Sanger sequencing, high-throughput sequencing, and single-molecule sequencing.

It is first necessary to clarify the relationships among various sequencing technologies. Sanger sequencing, high-throughput sequencing, and single-molecule sequencing do not constitute a generational hierarchy; therefore, it is inappropriate to refer to them as “first-generation,” “second-generation,” “third-generation,” or “fourth-generation” technologies. These sequencing methods differ in methodology and underlying principles. Each has distinct advantages and disadvantages in terms of key performance metrics, including sequencing accuracy, data output per unit time, average read length, and cost per unit of data. Consequently, each technology occupies a unique niche and is suited to specific applications, reflecting a largely complementary relationship rather than a sequential one.

The unique advantage of Sanger sequencing is its ability to read approximately 600–1,000 base pairs (bp) in a single run, offering longer read lengths than high-throughput sequencing technologies. With an accuracy rate reaching 99.99%, it is regarded as the “gold standard” for validating sequencing accuracy. However, each Sanger sequencing reaction yields only a single sequence read, resulting in low throughput and high costs. Sequencing an entire human genome using this method could cost tens of millions of US dollars, failing to meet the urgent demand of modern scientific development for rapid and large-scale acquisition of genomic sequences.

High-throughput sequencing technology has successfully addressed the limitations of Sanger sequencing in terms of cost, throughput, and labor requirements, owing to its superior cost-effectiveness, high throughput, and accuracy. It enables the simultaneous sequencing of millions to billions of nucleic acid molecules, significantly reducing sequencing costs and accelerating sequencing speed while maintaining high accuracy. This technological breakthrough has reduced the cost of personal whole-genome sequencing from hundreds of thousands of dollars to just a few hundred dollars, thereby strongly promoting the widespread application of gene sequencing technologies across various fields.

Single-molecule sequencing technologies can be subdivided into two categories: nanopore sequencing and single-molecule fluorescence sequencing. The sequencing process of single-molecule sequencing does not require PCR amplification, enabling long-read and single-molecule-level sequencing. It can read fragments up to tens of thousands of bases in a single run, significantly reducing the difficulty of assembly and minimizing gaps that were previously unresolvable. However, compared with high-throughput sequencing technologies, single-molecule sequencing exhibits a higher per-base error rate.

Core Drivers Behind the Sequencer Boom: Policy Guidance, Demand Pull, and Talent Support

Domestic Substitution of Sequencers Has Been Elevated to the Level of National Strategy

The 2021 edition of the “Review and Guidance Standards for Government Procurement of Imported Products” explicitly stipulates that 100% of sequencers (second-generation sequencing platforms) procured must be domestically produced. Furthermore, in Guangdong Province’s 2021 published list of imported products, sequencers were removed from the import list. This clearly demonstrates the government’s firm stance in supporting domestic sequencers and indicates that domestically produced sequencers have gained sufficient competitiveness and recognition. The “Government Procurement Law of the People’s Republic of China” also explicitly provides that where domestically produced pharmaceuticals and medical devices can meet requirements, government procurement projects shall, in principle, procure domestic products, with a view to gradually increasing the proportion of domestically produced equipment configured in public medical institutions.

Downstream Markets Expand, New Demands Emerge

In recent years, as market education has matured, the scale of the sequencer market has continued to expand. The emergence of new demands has created new opportunities, driving more companies to invest in the research and development of domestically produced sequencers. According to research by VCBeat Institute, changes in the downstream market for sequencers are mainly reflected in four aspects:

Demand for High-Throughput, Low-Cost Solutions:This is mainly reflected in the increase in the volume of scientific research market data and the reduction in costs. Projects such as single-cell sequencing, spatial omics, and proteomics are becoming increasingly popular, with researchers demanding ever-higher volumes of gene sequencing data and further cost reductions.

Compact, Portable, and Flexible Requirements:Previously, sequencers were primarily utilized in large laboratories and tertiary hospitals. In recent years, there has been a significant rise in demand for sequencers in decentralized settings, such as remote areas, primary healthcare institutions, and field environments. These scenarios impose new requirements on sample concentration, sequencing modes, and sequencing speed, necessitating sequencers that are more flexible, highly portable, and have lower startup costs.

Long-read demand:The demand for long-read sequencing in research and clinical settings is growing day by day, with applications in variant detection, haplotype phasing, genome assembly, epigenetic studies, and more.

Real-Time Sequencing Requirements:The demand for gene sequencing in scenarios such as point-of-care testing and intraoperative testing is increasing, requiring sequencers to have faster detection speeds.

Technological Advancements and Commercialization Drive Accelerated Capital Deployment

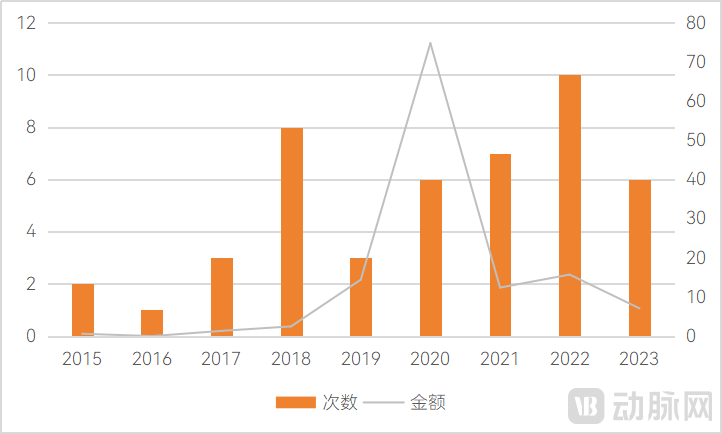

Amid the capital winter, hard technology often remains a favorite among investors. As the core of the gene sequencing industry chain, sequencers represent a high-barrier sector. Consequently, financing performance in the sequencer segment currently outpaces that of many sub-sectors within precision diagnostics and life science instruments. According to statistics from VCBeat Research Institute, 13 Chinese sequencer companies have completed 54 financing rounds in the primary market, with a total funding amount of RMB 13.234 billion.

Comparison of Financing Years in the Sequencer Industry

Data source: VBInsight; Chart by VCBeat

In terms of the number of financing events, the vast majority of financing in the sequencer industry has occurred since 2015, with a total of eight financing rounds completed in 2018. The year 2022 marked the peak for financing activity in the sector, with nine deals closed. It was also a year when multiple sequencers were commercialized, indicating a strong correlation between corporate financing performance and commercialization. The companies that secured financing in 2022—Sailu Medical, Qitan Technology, Sanogenomics, Genemind, and OncoDNA—have all advanced their sequencers to the commercialization stage.

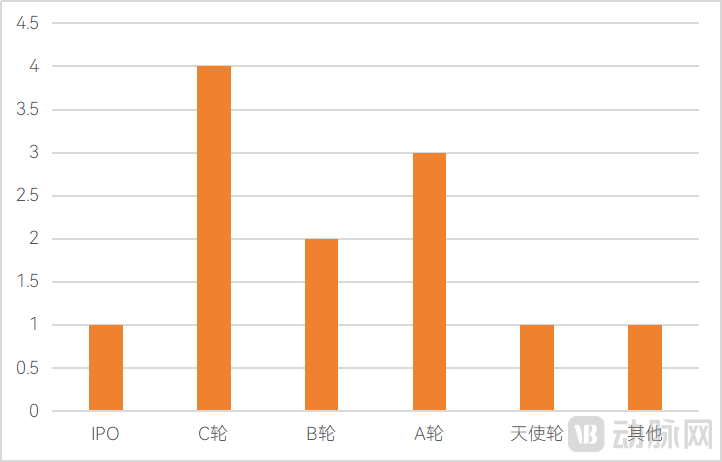

From the perspective of enterprise types, companies focused on developing high-throughput sequencers have grown relatively quickly, with MGI Tech successfully completing its IPO. In contrast, companies specializing in nanopore sequencers are generally at Series A or B funding stages, with only a few having completed Series C financing.

Distribution of Financing Rounds in the Sequencer Industry

Data source: VBInsight; Chart by VCBeat.

A significant amount of industrial capital has shown strong interest in sequencers. Currently, several IVD and precision medicine companies have invested in sequencer manufacturers, including leading enterprises in their respective niche sectors. These include Sansure Biotech, which acquired a 14.77% equity stake in Zhenmai Bio for RMB 255 million; KingMed Diagnostics, which participated in Zhenmai Bio’s Series C financing; PinFeng Medical, a company focused on smart laboratory diagnostics, and Longping Biotechnology, a biological breeding enterprise, both of which invested in Sailu Medical; Autobio Diagnostics, which made an exclusive strategic investment in Meili Technology; and Wondfo Biotech, which invested in Puyi Bio.

For IVD companies and genetic testing application service providers, business expansion and enhanced competitiveness rely on sequencers. These instruments are essential for resource integration and pursuing a second growth curve. As competition in the precision diagnostics application services sector becomes increasingly intense, the strategic importance of sequencers has become more prominent, making them an indispensable component of the IVD and genetic testing ecosystem.

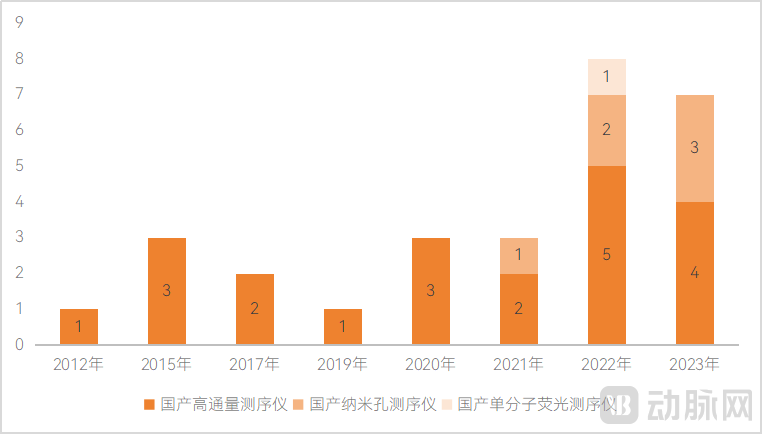

According to statistics from VCBeat, excluding Sanger sequencers, more than 10 Chinese companies have disclosed their independently developed sequencing instruments, among which nearly 30 models have been announced as commercialized and 8 have received approval from the National Medical Products Administration (NMPA).

2022 and 2023 marked a boom period for domestically produced sequencers. In 2022, eight Chinese-made sequencers were announced as commercially available, followed by seven in 2023.

Distribution of Release Years for Domestic Sequencers (Excluding Sanger Sequencers)

Source: Compiled from public information; Chart by VCBeat.

Chinese-Made Sequencers Are Embarking on a Vast Commercial Journey. How Can They Accelerate Their Path to Commercial Breakthroughs and Achieve Large-Scale Market Adoption? VCBeat Attempts to Analyze This from Multiple Perspectives, Including Product Technical Specifications, Regulatory Approvals, Product Portfolio, Business Models, and Tendering Processes. These Factors Play a Critical Role in the Large-Scale Commercialization of Sequencers.

Product Insights: Domestic high-throughput sequencers are advancing relatively quickly, while nanopore sequencers have emerged as a new hotspot

High-throughput sequencers represent the most widely adopted gene sequencing technology and a key focus for Chinese sequencer manufacturers. Currently, 19 high-throughput sequencing models from 10 companies have been commercialized, demonstrating robust vitality.

Among them, MGI Tech’s high-throughput sequencers play a highly pioneering role. MGI Tech is currently one of the few companies worldwide whose products cover sequencers across high, medium, and low throughput ranges. The company has seven commercially available sequencer models, achieving full coverage of low-, medium-, and high-throughput sequencing platforms. These instruments are suitable for small panels, small genomes, low-coverage whole-genome sequencing (WGS), transcriptomics, single-cell analysis, medium-to-large panels, and human whole-genome sequencing.

Emerging players have also delivered impressive performance. Salus Medical’s Salus Pro high-throughput sequencer is a desktop-scale solution compatible with five chip specifications offering 80M, 150M, 300M, 500M, and 1000M reads. It supports dual-module insertion and operation, covers various sequencing read lengths from SE50 to PE250, delivers 80M–1000M reads per chip, and achieves a raw Q30 score as high as 90%, featuring accuracy, speed, and flexibility.

From a product positioning perspective, emerging players in the high-throughput sequencing instrument market generally enter through the low-to-mid throughput segment, with full coverage across high, mid, and low throughput ranges becoming the prevailing trend. Ultra-high-throughput sequencers are focused on large-scale population genomics research, characterized by extremely high throughput and ultra-low sequencing costs. Desktop sequencers target customers with small-to-medium sequencing scales, suitable for independent laboratories or research groups, with a sequencing throughput of approximately 100–500 Gb. Their key features include low instrument cost, flexible chip specifications, and low startup costs.

Emerging domestic sequencer manufacturers have all entered the market with desktop sequencers. The underlying rationale is that ultra-high-throughput sequencers have stringent operational requirements and necessitate large sample volumes, making it difficult for small and medium-sized sequencing enterprises to consolidate sufficient samples. Furthermore, these smaller companies must carefully manage financial pressures. Consequently, desktop sequencers, characterized by lower instrument costs and less demanding operational requirements, have become the primary competitive focus for small and medium-sized enterprises, emphasizing convenient and flexible user experiences.

Furthermore, nanopore sequencers have become a key focus for emerging domestic sequencing instrument companies. Nanopore sequencing, still in its early stages, is regarded as a critical opportunity for Chinese enterprises to overtake competitors in the sequencing instrument industry. According to statistics from VCBeat, there are nine companies in China independently developing domestically produced nanopore sequencers. Among them, three companies have announced the commercialization of six nanopore sequencer models, with Qitan Technology having launched four commercialized nanopore sequencers.

However, there are only a few companies in China developing proprietary single-molecule fluorescence sequencers. Only the GenoCare 1600, developed by Zhenmai Biotechnology, has received approval from the NMPA, forming a stark contrast to the bustling landscape of domestically produced nanopore sequencers. According to VCBeat’s research, this situation may be determined by patent issues and technical characteristics.

Technical Patents:PacBio’s core patents, filed in 2013, remain within their patent protection term. Geneflow’s single-molecule fluorescence sequencing technology has been licensed under Helicos’ patents.

Technical Features:Here, we use the instrument characteristics of PacBio and Oxford Nanopore as examples. PacBio instruments are relatively large and costly, imposing significant pressure on corporate R&D budgets. In contrast, Oxford Nanopore devices are compact and offer greater flexibility.

Qualification Insights: 35 Products Approved by the NMPA, Multiple Based on DNBSEQ Technology

Obtaining regulatory qualifications for sequencers is critical. A sequencer is merely a tool, and downstream applications must be developed based on this platform. If the sequencer lacks an In Vitro Diagnostic (IVD) registration certificate, it will create significant obstacles during the registration testing of downstream applications. However, the difficulty of obtaining such qualifications is no less than that of early-stage R&D and technology transfer. This challenge is particularly pronounced for sequencers employing different sequencing principles, as the inability to conduct disease-specific comparative studies makes regulatory approval exceedingly difficult.

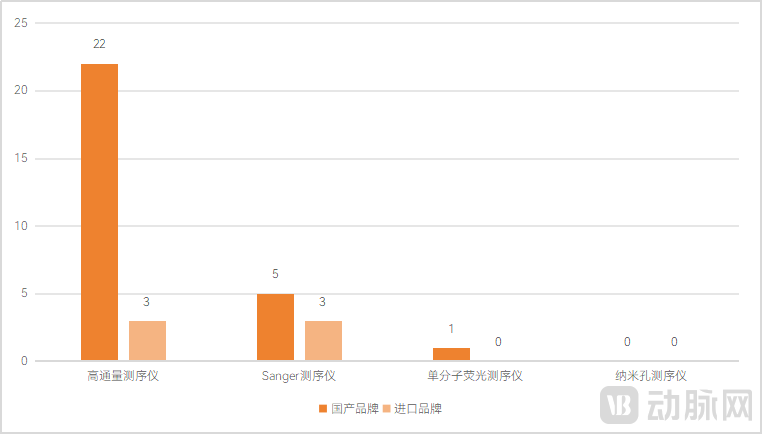

There are 25 high-throughput sequencers, one single-molecule fluorescence sequencer, eight Sanger sequencers, and one pyrosequencer approved by the NMPA; nanopore sequencers have not obtained NMPA registration certificates in China.

Classification of NMPA-Approved Sequencers

Data Source: National Medical Products Administration; Chart by VCBeat

In terms of high-throughput sequencers, according to statistics from VCBeat Research Institute, as of December 31, 2023, there were a total of 25 high-throughput sequencers approved by the NMPA, including 3 imported products and 15 models based on MGI Tech’s DNBSEQ technology.

Regarding Sanger sequencers, the NMPA has approved a total of eight models, five of which are from Chinese companies and three from overseas companies.

In the single-molecule sequencing sector, domestically produced single-molecule sequencers have obtained approval from the National Medical Products Administration (NMPA). In the field of nanopore sequencing, no nanopore sequencer has yet received NMPA approval. Due to the lack of NMPA certification, the application of nanopore sequencers is somewhat restricted in scenarios that place a high emphasis on qualifications, such as non-invasive prenatal testing (NIPT) and precision oncology diagnostics.

Obtaining regulatory approval for innovative sequencers is extremely challenging. Moving forward, regulatory authorities need to allocate more resources, establish quantitative metrics and evaluation criteria, and accelerate the certification process for nanopore sequencers.

Product System Insights: Building End-to-End Solutions

Building a comprehensive product portfolio and delivering end-to-end solutions is a model better suited to China’s specific conditions. Independent clinical laboratories account for a small share of the market in China, with hospitals holding the majority of clinical resources. However, sequencing instruments have not yet achieved a high degree of automation and standardization, and most customers have not yet mastered gene sequencing technologies. This creates a need for vendors to provide end-to-end solutions that assist customers in high-quality DNA extraction, establish bioinformatics analysis pipelines and tools, and facilitate smoother implementation of gene sequencing.

According to research by VCBeat Institute, the development of a sequencer product portfolio can be divided into three components: first, focusing on the sequencers themselves, with comprehensive coverage across high-, medium-, and low-throughput models; second, providing supporting reagents and consumables; and third, optionally extending further into related business areas such as laboratory automation.

High-throughput sequencing instrument companies are relatively more mature in building comprehensive solutions. Leading enterprises have fully covered sequencers, reagents and consumables, library preparation reagents, and bioinformatics analysis software, as well as products and technologies such as laboratory automation, single-cell analysis, and spatial omics.

Nanopore sequencers entered the product landscape relatively late, but relevant companies have attached great importance to their development, with reagents and consumables, library preparation kits, and data analysis systems being successively launched.

Furthermore, Chinese enterprises have demonstrated greater ambition in building their product portfolios, refusing to limit themselves to sequencers and associated reagents and consumables. Their business scope has expanded into areas such as laboratory automation, single-cell sequencing, and spatial omics. This strategy aims not only to better meet the personalized needs of research clients but also to establish differentiated competitive advantages for these companies.

Business Model Insights: Diversified Business Strategies to Address Diverse Scenario Needs

What Type of Sequencers Does the Market Need? This question cannot be generalized, as different application scenarios have varying requirements for throughput, cost, turnaround time, and portability.

Research Market

The research market is highly sensitive to the stability and cost of sequencers, while also valuing downstream services, including sample processing, bioinformatics analysis, and other customized solutions. Consequently, research customers have high expectations for sequencing instrument manufacturers, demanding not only high-quality, low-cost sequencers but also comprehensive supporting services.

Furthermore, the research market also values the accumulation of scholarly publications; a sequencer’s quality and stability will only gain recognition within the scientific community once a company has accumulated a sufficient number of high-impact publications.

NIPT Market

The requirements for NIPT applications center on qualifications, mandating that personnel be certified to perform the tests. Additionally, there is an expectation for faster report turnaround, lower costs, and higher throughput. It is hoped that sequencers will continue to improve in speed, cost-efficiency, and throughput to address a broader range of reproductive health issues, such as detecting genetic disorders via NIPT and conducting more in-depth analyses of fetal or maternal whole-genome data.

Precision Oncology Diagnostics Market

The tumor precision diagnostics market demands that sequencers meet stringent requirements in terms of regulatory qualifications, cost, and stability. A notable trend is the declining volume of outsourced tumor samples. In 2023, Hunan, Fujian, Shaanxi, and Tianjin issued regulations on sample outsourcing to standardize practices related to sample shipment, collaboration with third-party medical laboratories, and tumor gene sequencing. While end-users increasingly prefer conducting tests locally, many hospitals struggle with low sample volumes and difficulties in batch consolidation. This necessitates sequencers with low startup costs, flexible throughput, ease of operation, and high levels of automation, thereby lowering the barrier for end-users to perform local tumor gene sequencing.

Pathogenic Microorganism Detection Market

The pathogenic microorganism detection market does not have high throughput requirements; its core needs are to eliminate the wait for sample batching, achieve rapid sequencing, and meet point-of-care testing demands. This shortens turnaround time (TAT), thereby reducing the time required for clinical diagnosis and treatment of pathogenic infections and helping to mitigate antimicrobial misuse.

Emerging Markets

Emerging sectors such as judicial forensics, customs, agriculture, and disease control are still in their early stages. These fields are characterized by ill-defined demands and ongoing exploration, with no mature applications yet established. Meanwhile, there is a shortage of companies within the industry that possess sufficient expertise to provide services and develop applications for these emerging areas. Sequencing instrument manufacturers need to collaborate with end-users to help them develop applications, or partner with third-party sequencing service providers to jointly develop applications, thereby facilitating expansion into these emerging markets.

The application scenarios for high-throughput sequencers have become relatively mature, with widespread adoption and deep integration in areas such as non-invasive prenatal screening (NIPS), genetic disease testing, companion diagnostics, early cancer screening, and metagenomic next-generation sequencing (mNGS). Meanwhile, high-throughput sequencing technology is continuously expanding its boundaries into fields including single-cell sequencing, proteomics, spatial omics, and molecular breeding. Leading companies have already established extensive application ecosystems, creating significant competitive pressure for new market entrants.

Clinical applications of nanopore sequencers are currently being explored. Rapid testing, field-based point-of-care testing, and pathogenic microorganism detection are considered strong suits of nanopore sequencing technology. Domestic companies in China are strategically focusing on pathogenic microorganism detection, precision cancer diagnosis, and genetic disorders.

In terms of clinical applications for single-molecule fluorescence sequencing instruments, PacBio is pioneering clinical uses in rare disease diagnosis and newborn screening. Genetron Health’s single-molecule sequencers are primarily focused on reproductive health, including NIPT, CNV-seq, and PGT-A.

The above is an excerpt from the report. The overall framework of the report is as follows:

Chapter 1 The Rise and Surge of Domestically Produced Sequencers

1.1 The Impossible Trinity of Sequencing Technologies: Various Technologies Are Complementary to Each Other

1.2 Core Drivers of the Sequencer Boom: Policy Guidance, Demand-Driven Growth, and Talent Support

Chapter 2: Technological Advancements and Commercialization Drive Accelerated Capital Deployment

2.1 Cumulative Financing in the Primary Market Reached RMB 13.234 Billion, with Active Industrial Capital

2.2 Secondary Market: Strong Growth in Domestically Produced Sequencers, Emerging Sequencing Technologies in Early Stages

Chapter 3: Nearly 30 Domestically Produced Sequencers Commercialized, with Bright Prospects for Large-Scale Commercialization

3.1 Product Insights: Domestic high-throughput sequencers are advancing relatively quickly, while nanopore sequencers have emerged as a new hotspot

3.2 Qualification Insights: 35 Products Approved by the NMPA, Multiple Based on DNBSEQ Technology

3.3 Product System Insights: Building End-to-End Solutions

3.4 Business Model Insights: Diversified Business Strategies to Address Diverse Scenario Demands

Chapter 4: Future Trends – Standing Out Amidst Fierce Competition

4.1 Transitioning to Domestic Platforms Is Not as Difficult as Imagined; Performance Is Key

4.2 Broad Layout, In-Depth Exploration: Aligning with High-Frequency, Real-World Market Demand

4.3 Going Global: Engaging in International Competition

Chapter 5 Corporate Case Studies

Sailu Medical: Offering Both Sequencers and Spatial Omics Products to Achieve Domestic Substitution and Surpassance

MGI Tech: Comprehensive Sequencer Product Portfolio, with Greater Advantages in End-to-End Solutions

Please scan the QR code to add our assistant and obtain the full report. If you have already added us, please initiate a conversation to request it.

Special Acknowledgments (in order of interviews and research): Lei Ying, Director of Product Marketing at MGI China Marketing Center; Zhao Luyang, Founder of Sailu Medical; Yang Qian, Brand Director at Qitan Technology; as well as other unnamed enterprises and venture capitalists.。