ADC Development Too Costly: Even BD Revenue Falls Short as LegoChem Biosciences Secures Strategic Investment from Orion Group

LigaChem Biosciences

New Drug Developer

Orion Group

Food and Health Product Provider

A Notable Acquisition in the ADC Sector: Orion, a Food Industry Giant, Acquires 25.7% Stake in South Korean ADC Leader LegoChem Biosciences (LCB) for KRW 550 Billion (Approximately RMB 3 Billion), Becoming the Largest Shareholder of the KOSDAQ-Listed Biotech Company

However, Orion Group’s stock price fell 18% on the day the acquisition news was announced. This may be because the cross-industry acquisition diverges significantly from Orion Group’s core business, and LCB, as a biotech company, is not yet profitable.

Although Orion Group’s cash flow has reached a peak in recent years, with the company achieving a record-high operating profit of KRW 466.7 billion in 2022, and LigaChem Biosciences (LCB) standing out as a leader in the antibody-drug conjugate (ADC) sector, it remains uncertain whether Orion can join forces with LCB to build their envisioned “world-class pharmaceutical company” in this extremely capital-intensive field.

Like many South Korean conglomerates, Orion’s business scope extends far beyond its core industry. In 2019, Orion stated that while remaining focused on its primary food business, it was also paying close attention to the biotechnology sector, with plans to expand its business lines from food into healthcare solutions aimed at improving quality of life. In 2021, Orion made its first biomedical acquisition in China, purchasing a 65% stake in Shandong Lukang Biotechnology for RMB 78 million; the company was subsequently renamed Lukang Orion Biotechnology Co., Ltd. In 2022, Orion entered into an agreement with vaccine developer Quratis to jointly develop a tuberculosis vaccine. That same year, Orion and HySenseBio established Orion Biologics, a company focused on dental diseases.

Among these, Lukang Haoliyou represents Orion Group’s strategic entry into the cancer diagnostics market. Lukang Haoliyou has sequentially introduced early-stage colorectal cancer diagnostic technologies from Genomictree, a South Korean company specializing in early cancer diagnosis, and has partnered with LDT Bioscience in areas such as early tumor screening, companion diagnostics, and tumor recurrence monitoring, aiming to leverage these collaborations to penetrate the healthcare market.

Orion Group began exploring potential ADC assets in 2023, and through the acquisition of LegoChem, it has expanded its business into novel cancer drug development, progressively broadening the group’s biopharmaceutical footprint from diagnostics to therapeutics.

KRW 9 Trillion in International Collaboration for ADC Biotech

Following the wave of M&A activity among the first generation of ADC biotech companies in Europe and the United States, biotech firms from China, South Korea, and other regions have become key targets for multinational corporations (MNCs). LCB is an undeniable force in South Korea’s ADC landscape:By licensing its proprietary platform technologies and novel drug candidates to major global pharmaceutical companies, LCB has secured cumulative contracts exceeding 9 trillion Korean won (nearly $7 billion).

The most recent and striking deal is the $1.7 billion in-licensing agreement for an investigational Trop2 asset with Johnson & Johnson late last year. For LCB84, a Trop2 ADC still in Phase I clinical trials, J&J offered global rights at a high valuation, comprising a $100 million upfront payment, a $200 million option exercise fee, and $1.4225 billion in milestone payments.

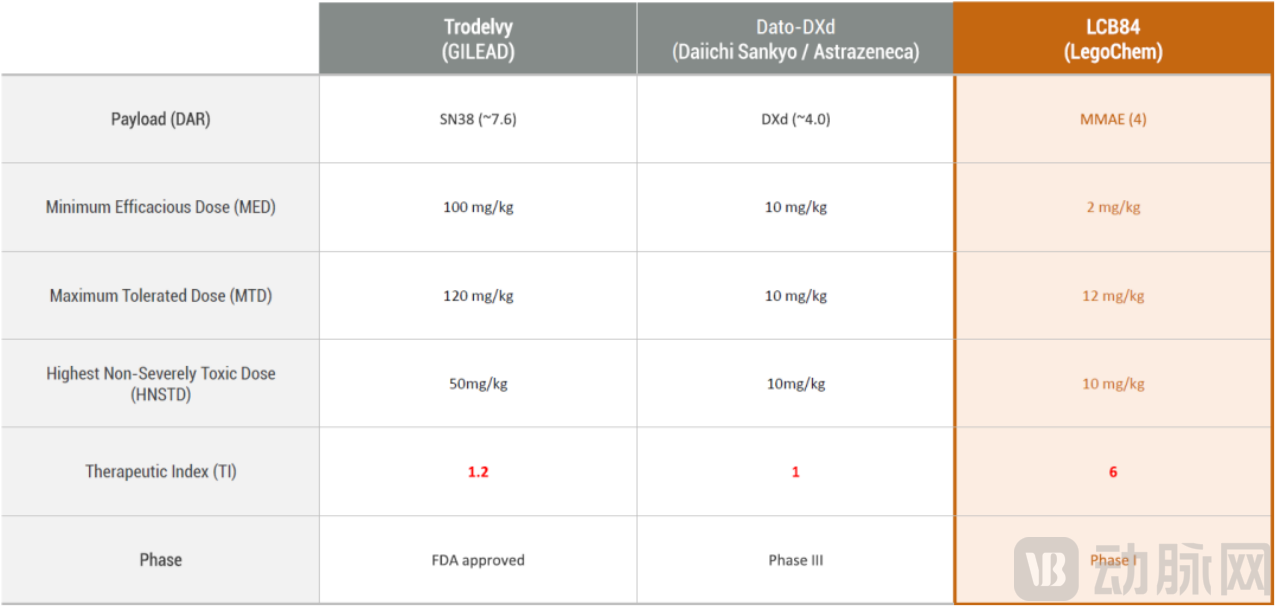

Trop2 is one of the hottest targets for ADCs after HER2. Although LCB’s product holds no developmental advantage over the many other candidates currently in the pipeline, preclinical data were used to compare it with Gilead’s marketed product, Trodelvy, and Daiichi Sankyo’s Dato-DXd.Johnson & Johnson believes that LigaChem Biosciences' Trop2 ADC has the potential to be best-in-class.

LCB84 utilizes MMAE as its toxin with a drug-to-antibody ratio (DAR) of 4. It features comprehensive differentiating designs, including binding to the tumor tissue-specific Trop2 epitope, cleavage by the tumor microenvironment-specific enzyme AMAM10, and a unique linker design that ensures reduced off-target toxicity.

Comparison of LCB84 with Trodelvy and Dato-DXd, Source: Company Official Website

In various tumor models of preclinical studies, LCB84 demonstrated superior antitumor activity. The company stated that it outperformed Trodelvy and Dato-DXd in cell-derived xenograft (CDX) models of triple-negative breast cancer (TNBC), pancreatic ductal adenocarcinoma (PDAC), gastric cancer (GC), and non-small cell lung cancer (NSCLC).

Such a pipeline is no accident; it stems from the nurturing power of LCB’s proprietary technology platform. The company’s pride lies in its self-developed ADC platform, ConjuALL, which focuses on addressing the critical challenge of reducing toxicity while enhancing efficacy:

- LCB’s Conjugation-Linkers Platform enables specific cleavage in tumor cells, featuring plasma stability and no release in non-tumor cells, while rapidly and effectively releasing toxins within tumor cells.

- LCB’s Toxin Platform achieves selective activation within tumor cells by adding removable hydrophilic masking groups to PBD toxins, thereby reducing toxic side effects and enhancing anti-tumor efficacy.

These innovations have made ConjuALL highly attractive, with numerous companies paying premium prices for this platform technology in the company’s out-licensing deals, including the UK-based Iksuda, the Czech company Sotio, and Amgen.

LCB Partial Out-Licensing

In addition to the aforementioned out-licensing arrangements, LCB has entered into multiple collaboration agreements with biotechnology companies including BostonGene, Elthera AG, NextCure, Glycotope, Harbour BioMed, Duality Biologics, Antengene Corporation, Hanmi Pharmaceutical Group, WuXi XDC, WuXi AppTec, and Pyxis.

A look at LCB’s partner list makes it evident that this is a highly globalized company.

In North America, LCB established its subsidiary, AntibodyChem Biosciences (ACB), in Boston in 2022, with the aim of expanding its business scope by building sustained and close ties with global leaders in the biotechnology sector and pharmaceutical companies.

In Asia, China is a key stronghold for LigaChem Biosciences (LCB). In terms of its pipeline, LCB has maintained a business development (BD) partnership with Fosun Pharma since 2015. Within the CDMO sector, WuXi XDC and LCB have also sustained a multi-year collaborative relationship. At last year’s XDC conference hosted by WuXi XDC, Chul-Woong Chung, CTO of LCB, appeared on stage and stated that the company would maintain closer cooperation with Chinese firms and jointly explore larger markets in the future.

Continuous Cash Burn: Is BD Still Not Enough?

Despite LCB’s frequent business development successes and steadily rising collaboration deal values, the company remains financially constrained by the high costs of ADC drug R&D and its lack of commercial-stage products. Under these circumstances, it is only logical for LCB to seek a well-capitalized strategic partner.

LCB aims to secure approximately KRW 1 trillion (RMB 6 billion) in R&D funding over the next five years to achieve its “2030 Vision.” This ambitious plan includes developing four to five ADC candidates annually by 2030, establishing a portfolio of ten clinical pipelines, advancing proprietary pipelines into late-stage clinical trials and commercialization, and becoming a leading company in the oncology field.

The development costs for antibody-drug conjugates (ADCs) are extremely high, with expenses reaching RMB 50–70 million to reach the Investigational New Drug (IND) stage. If site-specific conjugation technology is employed, which requires the use of specialized enzymes, the costs are even higher; the total investment for an ADC from research and development to the IND stage approaches RMB 100 million, equivalent to the total cost of developing two to three monoclonal antibodies or bispecific antibodies to the IND stage.

Advancing ADC pipelines to Phase II clinical trials results in a multiplicative increase in costs; RMB 500 million can support only two to three ADC pipelines reaching Phase II, even under conditions of optimal capital utilization.

By the late-stage commercial production phase, the cost of ADCs is more than double that of conventional monoclonal antibody products. “Manufacturing monoclonal antibodies typically costs around RMB 20 million, whereas ADCs can reach RMB 50 million.”

It is clearly unsustainable for a biotech company to single-handedly support the capital-intensive development of an ADC pipeline. Business development (BD) has thus become virtually mandatory for ADC-focused biotechs. However, while the total contract value in BD deals may appear substantial, only the upfront payment provides timely cash flow infusion to the biotech.Despite the support of several BD deals throughout the year, LCB’s net profit has remained negative for an extended period: in the first three quarters of 2023, LCB’s net profits were -17.7 billion KRW, -20.0 billion KRW, and -19.7 billion KRW, respectively.

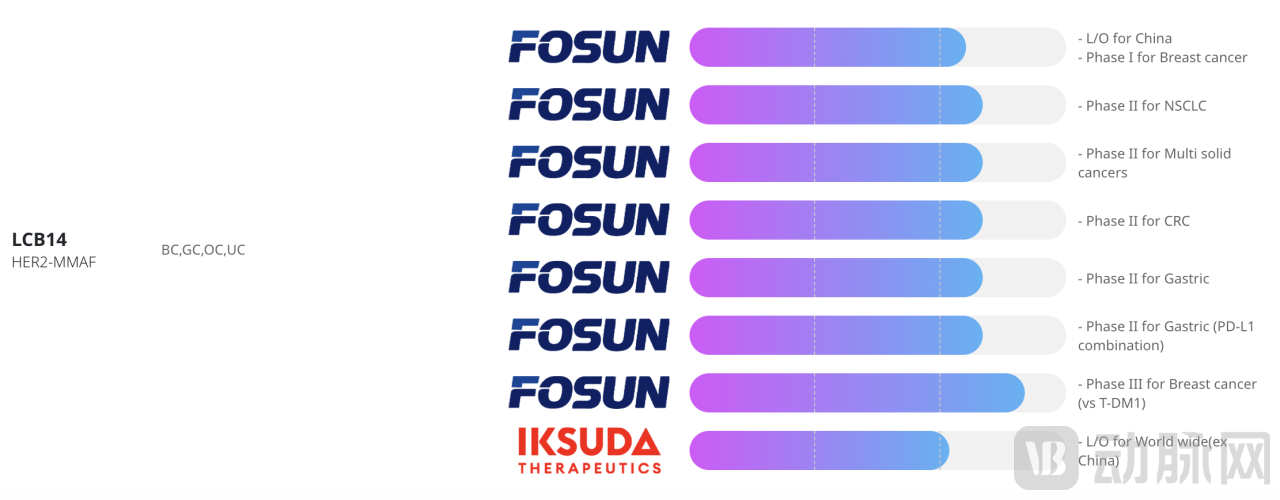

The pipeline advancement post-BD is a more protracted process,For example, regarding LCB-14, a HER2-targeted product out-licensed at an early stage by LigaChem Biosciences, the partner Fosun Pharma’s most advanced development milestone to date is a Phase 3 comparative clinical study evaluating the efficacy and safety of LCB-14 versus T-DM1 in patients with HER2-positive, unresectable locally advanced or metastatic breast cancer. Development progress for other indications, including small cell lung cancer, gastric cancer, and colorectal cancer, remains at Phase 2.

LCB14 Pipeline Progress, Source: Company Website

And potential pipeline rollbacks that may occur later.According to data from PharmaCube, as of December 18, there were a total of 56 terminated business development (BD) deals in the global biopharmaceutical industry in 2023, with 71% involving innovative drug projects. Even when the counterparty is a multinational corporation (MNC) with relatively abundant capital and higher risk tolerance, the decision to continue advancing an asset requires comprehensive consideration of multiple factors. It can even be said that the more battle-hardened an MNC is, the more decisive it becomes in making cutback decisions. For instance, last year, Merck & Co. returned two non-core preclinical ADC products from Kelun-Biotech, while simultaneously licensing in high-value projects from Daiichi Sankyo.

Even Seagen, which was sold at a sky-high price last year, had been unable to escape the fate of losses since its establishment in 1997; even after it later had two ADC products on the market, it still failed to turn a profit.

Seagen began seeking external capital support in 2019. In its 2019 annual report, Seagen tactfully stated that a portion of its revenue derived from agreements with corporate collaborators, over whose willingness and resources to invest in related products the company had no control.

If established ADC biotechs are facing such challenges, emerging ADC biotechs will encounter even greater turbulence in collaborations and intensified industry competition. Likely sensing the escalating rivalry in the ADC sector and the increasing difficulty of the upfront-payment and platform-licensing model, LCB has chosen to no longer go it alone.

As this is not a merger or acquisition, upon completion of the acquisition process, LCB will be integrated as a subsidiary of Orion Group, with its existing management team and operational systems remaining unchanged. Although Orion Group believes that the boundaries between the biopharmaceutical and food industries will become increasingly blurred, given Orion’s current accumulation in the biopharmaceutical sector, LCB’s technological strengths and professional capabilities need to continue to be leveraged through relatively independent operations.

In contrast, for domestic biotech companies, overseas business development (BD) has only just begun to serve as a source of cash flow. Statistics show that upfront payments from overseas deals in 2023 exceeded RMB 30 billion, far surpassing the total upfront payments from all previous years combined. Some biotech firms have even reported profitability, driven by the cash flow generated from these BD upfront payments.However, from the perspective of drug development, closing a business development (BD) deal is merely the beginning, and the capital provided through BD is limited and conditional. After the initial adrenaline rush brought by BD comes a brutal competition in operational efficiency and speed, as well as future commercialization challenges.

Regardless, the ADC battlefield will become even more complex in the new year.

References

Health News Bureau, https://mp.weixin.qq.com/s/hKyL4FDGPOBkZbOVdrJeuw

AntiBody Research,https://mp.weixin.qq.com/s/qmKY3q2M1GDSuq8ayku4-A

Biopharmaceutical Editor, https://mp.weixin.qq.com/s/gGI4dHa5angBKURLDFedUg